*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

What Exactly is a Hard Money Loan? The Fundamentals

Hard money loans are a specialized financing tool built specifically for real estate investors tackling business-purpose transactions. Unlike traditional mortgages designed for personal homeownership, hard money loans are short-term, asset-based loans secured by non-owner-occupied investment properties. Think of them as your financial rocket fuel when you need to move fast on opportunities that traditional banks just can't keep up with.

Here's the key thing to understand: hard money loans are business loans—not consumer products. This distinction matters. A conventional mortgage finances someone's primary residence, focusing on whether the borrower can make monthly payments from their personal income. Hard money loans? They finance your investment strategy, focusing on the property's profit potential. The property itself—not your W-2 income or debt-to-income ratio—serves as the primary collateral and underwriting consideration.

Asset-Centric Underwriting: A Different Approach to Risk

Traditional banks evaluate loan applications through a consumer-lending lens. They dig into credit scores, employment history, tax returns, and debt-to-income (DTI) ratios. This approach makes sense for owner-occupied properties where personal income must reliably cover mortgage payments for 15 to 30 years.

Hard money lenders play by different rules. Their underwriting process centers on the asset's potential rather than your personal financial profile. The two most critical factors in hard money underwriting are:

After Repair Value (ARV): This is the projected market value of the property after all planned renovations are completed. Lenders analyze comparable sales in the area, assess the scope of work, and determine whether the improved property will command sufficient value to ensure loan repayment. For example, a property purchased for $200,000 requiring $50,000 in renovations might have an ARV of $325,000—creating a clear value proposition for both you and the lender.

Borrower Track Record and Project Viability: Your personal income takes a back seat here, but your experience and know-how? Those matter a lot. Hard money lenders want to see that you've successfully completed similar projects before, that you understand your local market, and that your renovation timeline and budget actually make sense. Here's the bottom line: an investor with five successful fix-and-flips under their belt will get much better terms than someone tackling their first deal.

This property-focused approach means hard money lenders can say yes when banks would shut the door. A property that needs serious work, a borrower juggling multiple mortgages, or an investor who needs to close in a week—these situations would get an instant "no" from traditional lenders. But with hard money? If your investment strategy holds water, you're in the game.

Who Uses Hard Money Loans?

Hard money loans aren't for everyone—they're built for active real estate investors with profit-driven strategies. Here's who typically benefits most:

Fix-and-Flip Investors: You buy distressed properties, renovate them, and sell for a profit—usually within 6 to 12 months. Hard money's speed lets you compete with cash buyers at auctions and in hot markets. Plus, with leverage often reaching 85-90% of total project costs, you can keep your capital working across multiple deals at once.

BRRRR Strategists: If you're following the Buy, Rehab, Rent, Refinance, Repeat playbook, hard money serves as your bridge financing. You acquire and fix up a property with short-term hard money, get tenants in place, then refinance into a long-term rental loan based on what the property earns. The result? You recycle your capital over and over while building a portfolio of properties that generate steady cash flow.

Real Estate Developers: Small to mid-sized developers turn to hard money for ground-up construction, subdividing properties, or conversions—like turning a single-family home into multiple units. These projects require flexible financing that can accommodate construction draws and evolving project scopes—flexibility that traditional construction loans often lack.

Portfolio Landlords: If you're an experienced landlord with multiple properties, you've likely hit DTI limitations that block you from getting additional conventional mortgages—even when you have substantial equity and positive cash flow across your portfolio. Hard money loans bypass these artificial constraints, letting proven investors like you continue scaling your operations.

The hard money lending market has experienced significant growth, with the global market valued at approximately $44.6 billion in 2024. This growth shows that more investors recognize a simple truth: speed, flexibility, and leverage often matter more than interest rate when you're chasing time-sensitive opportunities.

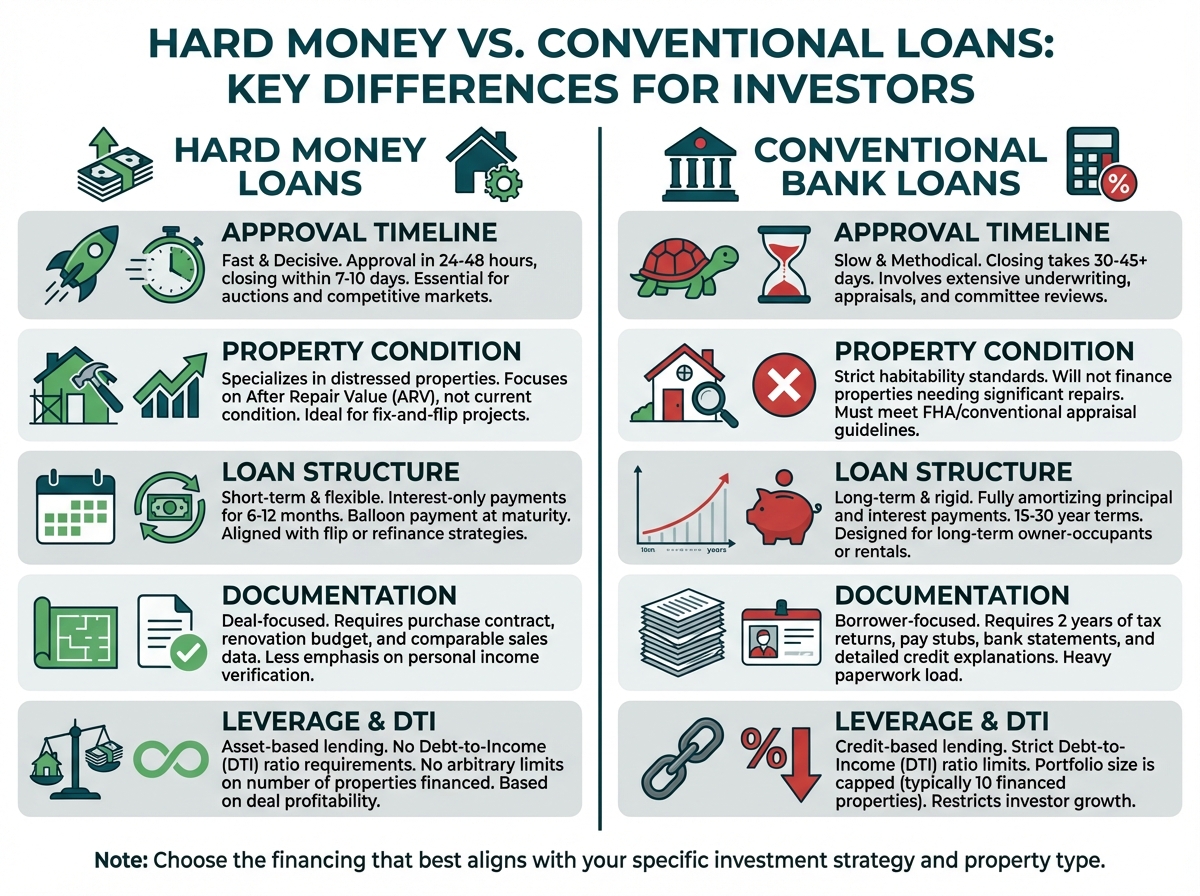

Distinguishing Hard Money from Traditional Financing

The differences between hard money loans and conventional bank financing go far beyond interest rates. Here's what you need to know:

Approval Timeline: Traditional banks typically need 30 to 45 days for loan approval and closing, involving extensive documentation, multiple appraisals, and committee reviews. Hard money lenders can approve loans in 24 to 48 hours and close within 7 to 10 days—a game-changer when you're competing for properties in hot markets or bidding at foreclosure auctions.

Property Condition Requirements: Banks generally won't finance properties in poor condition. They require properties to meet minimum habitability standards and pass FHA/conventional appraisal guidelines. Hard money lenders specialize in distressed properties. They understand the current condition is temporary and focus instead on what the property will be worth after renovation.

Loan Structure: Conventional mortgages feature fully amortizing payments over 15 to 30 years with principal and interest due monthly. Hard money loans typically structure as interest-only payments for 12 months with a balloon payment of the full principal due at maturity—perfectly aligned with your strategy of selling or refinancing rather than holding long-term.

Documentation Requirements: Traditional lenders want to know everything about you: two years of tax returns, pay stubs, bank statements, employment verification letters, and detailed explanations of any credit hiccups. Hard money lenders? They care about the deal. Bring your purchase contract, renovation budget, scope of work, comparable sales data, and exit strategy. Sure, they'll look at your experience and track record, but the paperwork load is refreshingly lighter.

Leverage and DTI: Conventional loans box you in with property limits (usually 10 financed properties) and debt-to-income ratios that get tighter with every mortgage you add. Hard money lenders skip the DTI math altogether. They want to know: Is this deal profitable? How much skin do you have in the game? This means experienced investors can run multiple projects at once without hitting arbitrary portfolio ceilings.

Once you understand these key differences, you'll know exactly when hard money financing makes sense for your strategy. If speed, leverage, and the ability to snag distressed properties that banks won't touch are priorities for you, hard money loans become an essential tool in your wealth-building toolkit.

Navigating the Hard Money Landscape: Key Factors for Investors

Here's what you'll quickly learn when you step into hard money lending: loan terms vary widely. Two factors matter most in shaping your borrowing experience and deal structure: your track record as an investor and how renovation funds flow through the draw process.

Investor Experience: The Path to Better Terms

Hard money lenders differ from traditional banks in plenty of ways, but here's one thing they have in common: they reward a winning track record. Your experience level directly influences the terms you'll qualify for, creating a clear ladder to climb as you successfully complete more projects.

The Experience Tier System

Most hard money lenders group investors into experience tiers based on how many projects you've completed. While the exact numbers vary from lender to lender, here's a typical breakdown:

- Beginner (0-2 completed projects): You're just getting started or have a limited track record

- Intermediate (3-5 completed projects): You've shown you can get deals done successfully

- Experienced (5-10 completed projects): You've built a solid portfolio and know the process well

- Expert (10+ completed projects): You're a proven performer with consistent results

According to RCN Capital, repeat investors with established track records can access significantly better terms than first-time borrowers. Simply put, your experience is one of the most valuable assets you bring to any lending relationship.

Benefits of Higher Experience Tiers

As you move up the experience ladder, the financial rewards really start to add up:

Lower Down Payment Requirements: If you're just starting out, expect to put down 20-25%. But once you've built your track record, you could secure financing with just 10-15% down. On a $250,000 purchase, that's the difference between tying up $50,000 versus $25,000—freeing up capital you can put to work elsewhere.

Higher Loan-to-Cost (LTC) Leverage: More experience means more leverage on your total project costs. Lendsure reports that experienced investors can qualify for LTV ratios up to 90% on purchase and 100% on construction costs, compared to 75-80% for beginners. That extra leverage lets you tackle bigger projects or run multiple deals at once without draining your cash reserves.

Flexible Exit Profitability Requirements: Lenders typically want to see minimum profit margins to make sure you're motivated to finish the project. As you prove yourself, you'll often get more wiggle room here—some lenders will drop minimum ROI requirements from 20% down to 15% or even 10% for investors who consistently deliver.

This flexibility can make marginal deals viable and expand your deal pipeline.

Better Interest Rates and Fees: Here's where you'll see real dollars saved. While fix and flip loan rates in 2025 typically range from 8% to 14%, investors with solid track records consistently secure rates at the lower end. Let's put that in perspective: on a $200,000 loan over 12 months, the difference between a 12% rate and a 9% rate means $6,000 stays in your pocket instead of going to interest payments.

Building Your Track Record

Here's the bottom line: every project you complete successfully makes your next deal easier to finance. Keep detailed records of your projects, nurture your lender relationships, and focus on clean exits that prove you're reliable. Think of each flip as more than just a deal—it's building your reputation and borrowing power for the future.

The "Draw" Process: Managing Renovation Funds

Hard money loans handle renovation funds differently than you might expect. Instead of getting all your money at closing like a traditional mortgage, fix-and-flip loans use a draw system. This approach protects everyone involved and keeps your project on track.

Understanding the Construction Holdback

When your hard money loan closes, you won't walk away with the full amount. Here's how it actually works:

- Purchase Funds: This money hits your account at closing so you can buy the property

- Construction Holdback: Your renovation budget sits in escrow and gets released as you hit project milestones

Let's say you land a $250,000 loan—$180,000 for the purchase and $70,000 for renovations. At closing, you get the $180,000 to acquire the property. That $70,000 renovation budget stays in escrow until you're ready to draw against it as work gets done.

Why does it work this way? This structure keeps everyone honest: it confirms funds go where they should, verifies that your improvements are actually adding value, and gives the lender confidence that their investment is protected as your project moves forward.

Staged Reimbursements at Milestones

Here's how the draw process actually works: it's a reimbursement system tied directly to your construction progress. As you knock out specific phases of your renovation, you submit draw requests to tap into portions of your construction holdback. Most lenders organize draws around major trade completions:

- Draw 1: Demolition and rough framing (typically 15-20% of renovation budget)

- Draw 2: Mechanical rough-ins—plumbing, electrical, HVAC (20-25%)

- Draw 3: Insulation and drywall installation (15-20%)

- Draw 4: Finish work—flooring, cabinets, fixtures (25-30%)

- Draw 5: Final touches—paint, landscaping, punch list (15-20%)

Your lender and project scope will determine the exact breakdown, but the core concept stays the same: finish the work first, then get paid back. This means you'll need some cash on hand to pay your contractors upfront, or you'll need to partner with contractors who are comfortable waiting for payment until your draws come through.

Draw Request Procedures and Documentation Requirements

Getting your draw request approved comes down to solid documentation. Lenders want proof that the work meets standards and that funds are being used properly. Here's what a complete draw package looks like:

Detailed Invoices: Itemized bills from your contractors breaking down labor and materials for completed work. Vague or generic invoices? Those get kicked back.

Lien Waivers: Signed statements from contractors and suppliers confirming payment (or agreeing to accept payment from draw proceeds) and releasing their right to file a mechanic's lien on your property. These keep you protected from legal headaches down the road.

Photographic Evidence: Sharp, well-lit photos showing completed work from multiple angles. Many lenders now want timestamped images or even video walkthroughs to confirm current conditions.

Updated Project Timeline: A refreshed schedule highlighting completed milestones and realistic completion dates for what's left, proving your project is staying on course.

Draw Request Form: Your lender's specific form that outlines the amount you're requesting, the milestones you've completed, and how you plan to allocate the funds.

Site Inspections: The Verification Step

Before releasing draw funds, most lenders will send someone out to verify that the work you've reported is actually done and meets acceptable standards. Here's what to expect:

An inspector (either from the lender's team or a third-party contractor) will visit your property, typically within 2-5 business days of receiving your draw request. They'll compare what they see on-site against your submitted documentation and the original scope of work, checking that:

- The reported work is actually complete

- Quality meets professional standards and local building codes

- No obvious defects or safety issues exist

- Progress aligns with your approved renovation plan

If everything looks good, the inspector approves the draw and you'll typically see funds within 1-3 business days. If there are issues, the inspector will document what needs to be corrected before your draw can move forward.

Tips for Faster Draw Processing

Savvy investors streamline the draw process to keep cash flowing and projects moving:

Front-Load Your Documentation: Don't scramble for paperwork when you need funds. Collect invoices, lien waivers, and photos as work progresses, so your draw package is ready to go the moment you hit a milestone.

Communicate Proactively: Give your lender a heads-up when you're approaching a draw milestone. Many lenders will schedule inspections in advance, which can shave days off your processing time.

Exceed Minimum Standards: Complete work to a level that clearly passes inspection. Cutting corners might save a few dollars upfront, but it creates delays and headaches during the draw process.

Build Inspector Relationships: If you're working with the same lender across multiple projects, you'll likely see the same inspectors. Professional, well-documented projects build trust and can lead to faster approvals down the road.

Understand Your Lender's Schedule: Some lenders process draws on specific days of the week or have monthly volume limits. Timing your requests strategically can prevent unnecessary delays.

The draw process might feel like a lot to navigate at first, but here's the thing—it's actually designed to protect you and everyone else involved in the deal. Once you've been through it a few times, you'll find your rhythm. Seasoned investors know how to work this system like pros, keeping cash flowing smoothly while building the kind of track record that earns them better terms down the road. And with OfferMarket in your corner, our streamlined process and experienced team turn what could be a headache into just another step in your project timeline.

Understanding Hard Money Loan Terms: What to Expect

Let's talk about what you're actually signing up for with a hard money loan. Getting clear on the terms and structure isn't just helpful—it's essential for running your numbers accurately and squeezing the most out of your investment. Hard money works differently than traditional financing, and that's by design. These loans are built for the speed and flexibility that real estate investing demands.

Loan Term Duration

Most hard money loans come with a 12-month term, giving you a focused runway to execute your game plan. For a typical fix-and-flip where you're tackling cosmetic updates or moderate renovations, a year is usually plenty of time to buy, renovate, list, and close with your buyer.

But what about bigger projects? If you're taking on major structural work, adding square footage, or converting a property (say, turning a single-family into a multi-unit), you'll need more breathing room. That's why hard money lenders typically offer extensions up to 18-24 months for these heavier lifts. More ambitious renovations mean more time for permits, construction, and getting the property stabilized before you make your exit.

When negotiating your loan term, take an honest look at your project's scope. Underestimating the timeline can put you in a tight spot and potentially push you toward exit strategies you'd rather avoid. Smart investors know this—they build buffer time into their projections to handle unexpected delays, contractor scheduling hiccups, or permit headaches.

Payment Structure: Interest-Only with Balloon Payment

Hard money loans work on an interest-only payment structure throughout the loan term. This is a different animal from traditional amortizing mortgages. With this setup, your monthly payments cover only the interest charges on your outstanding balance—you're not chipping away at any principal during the loan term.

Here's why this interest-only approach can be a game-changer for your investment strategy. It keeps your monthly carrying costs low during renovation, freeing up cash for construction expenses, surprise repairs, or that next deal you've got your eye on. Lower monthly payments mean more breathing room while you're getting your property ready for sale or refinancing.

The flip side of these lower monthly payments? The balloon payment waiting for you at loan maturity. This is one lump-sum payment covering your entire principal balance—both your initial purchase funds and any renovation funds you drew. The balloon payment comes due when your loan term ends, which should line up with your planned exit strategy.

Let's break this down with real numbers. Say you secure a $300,000 hard money loan (covering both purchase and renovation costs) at 10% annual interest on a 12-month term. Your monthly interest-only payment comes to roughly $2,500. Over the year, you'll pay $30,000 in interest while that full $300,000 principal sits untouched. When month 12 rolls around, you need to pay back the entire $300,000 principal—either by selling the property or refinancing into long-term financing.

This structure inherently requires disciplined exit planning. The approaching balloon payment creates a clear deadline that keeps you focused on completing renovations efficiently and executing your exit strategy on time. This isn't a loan designed for holding properties indefinitely—it's built specifically for active real estate investors who work with defined timelines.

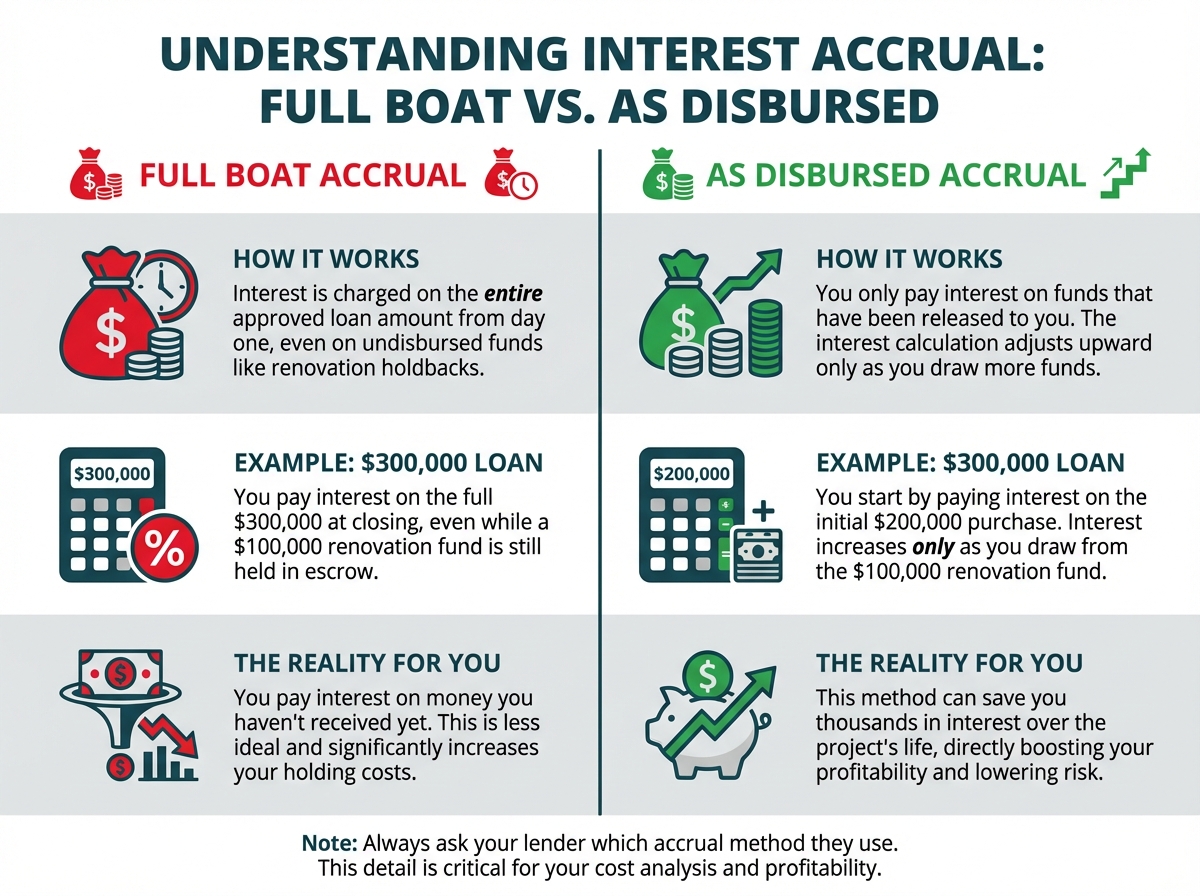

Interest Accrual Methods: Full Boat vs. As Disbursed

Here's something that trips up a lot of investors: how interest accrues on your loan. Lenders use two primary methods, and understanding the difference can save you significant money over the life of your loan.

"Full Boat" Interest Accrual means you're charged interest on the entire approved loan amount from day one—even if you haven't received all the funds yet. Let's say you're approved for a $300,000 loan ($200,000 for purchase and $100,000 for renovations). With full boat accrual, you start paying interest on the full $300,000 at closing, even though that $100,000 renovation holdback is sitting in escrow untouched.

You'll typically see this approach with smaller loans or for newer investors. It gives lenders predictable returns and simpler accounting. But here's the reality: it's not ideal for you because you're paying interest on money that's not in your pocket yet.

"As Disbursed" or "Unpaid Principal Balance" Interest Accrual works in your favor. You only pay interest on funds that have actually been released to you. At closing, you pay interest on the purchase funds. Then, as you hit renovation milestones and request draws, interest accrues on those additional amounts.

Same example, different outcome: with the "as disbursed" method, you'd start by paying interest only on the $200,000 purchase funds. Complete your first renovation phase and draw $25,000 in month two? Now you're paying interest on $225,000 going forward. As each subsequent draw is funded, your interest calculation adjusts to reflect the new unpaid principal balance.

Here's where this really matters for your bottom line. On a $100,000 renovation holdback with a 10% annual interest rate over a 12-month project where funds are drawn gradually, the "as disbursed" method could save you several thousand dollars compared to "full boat" accrual. If you're juggling multiple projects or working with tight margins, those savings add up fast and directly boost your profitability.

Bottom line: when you're comparing loan offers, ask upfront which interest accrual method the lender uses. This detail might sound technical, but it deserves a front-row seat in your cost analysis and lender selection process.

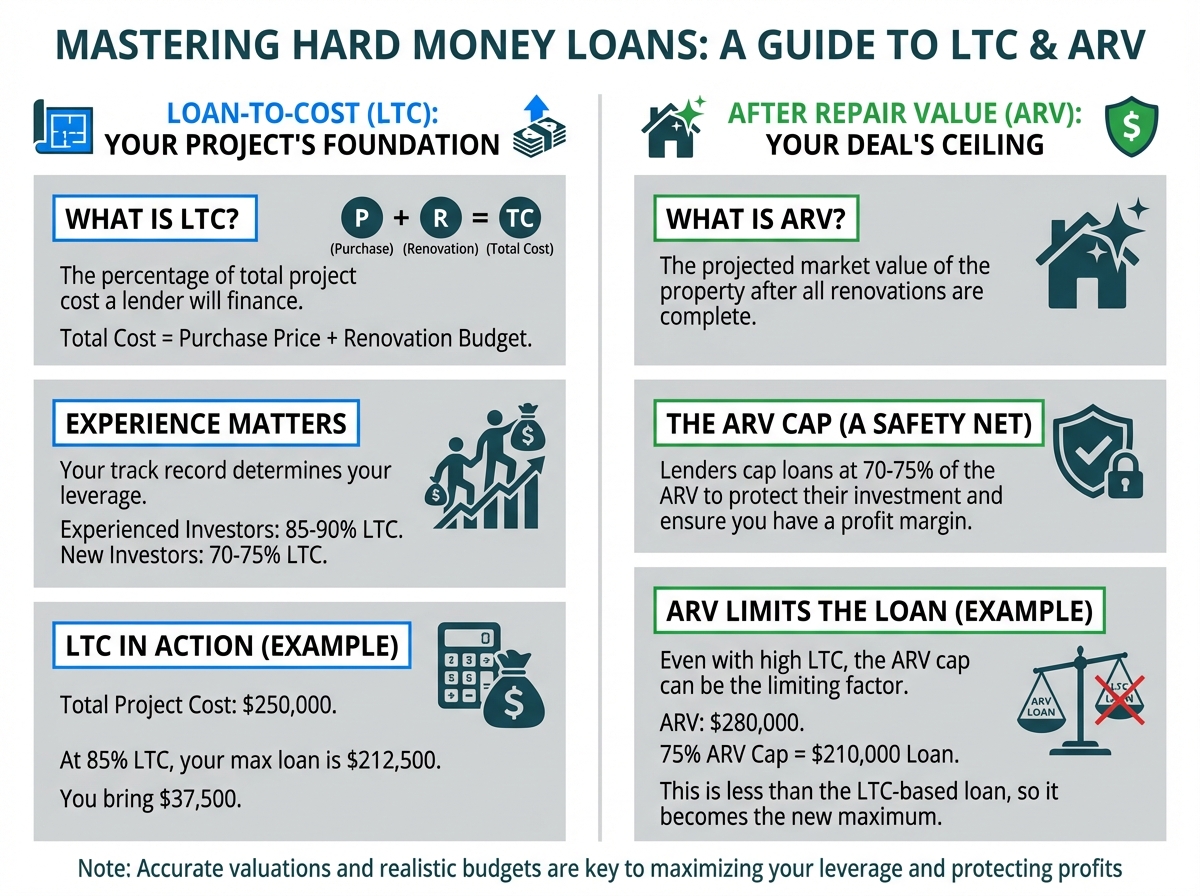

Leverage Limits: LTC and ARV Caps

Hard money lenders rely on two key metrics to determine how much they'll lend you: Loan-to-Cost (LTC) and After Repair Value (ARV). Getting comfortable with these leverage limits helps you structure smarter deals and know exactly how much capital you'll need to bring.

Loan-to-Cost (LTC) is simply the percentage of your total project cost that the lender will finance. That total includes both your purchase price and renovation budget. Good news for experienced investors: hard money lenders typically offer 85-90% LTC to those with proven track records, meaning the lender covers most of your all-in costs.

Let's make this concrete. Say you're buying a property for $200,000 and budgeting $50,000 for renovations—that's a $250,000 total project cost. At 85% LTC, your loan would be $212,500. You'd need to bring $37,500 as your down payment and initial capital contribution.

Here's something important to know: the LTC percentage you qualify for depends heavily on your experience. If you're just starting out, expect 70-75% LTC, which means larger down payments and more of your own money in the deal. But here's the encouraging part—as you complete projects successfully and build your track record, lenders reward you with higher leverage. That means you can scale your portfolio faster while putting less capital into each deal.

After Repair Value (ARV) is simply what your property will be worth once all the renovations are done. Lenders pay close attention to this number because they typically cap loans at 70-75% of the projected ARV, no matter what the LTC calculation says. This ARV cap is there to protect everyone—it gives the lender a comfortable equity cushion and makes sure you've got enough profit margin baked into your deal.

Think of the ARV cap as your lender's safety net. Here's how it works: even if your deal qualifies for 90% LTC, the lender will reduce your loan if that amount exceeds 75% of the ARV. This two-part system (LTC and ARV working together) keeps both you and the lender from getting overextended on a property that doesn't have enough upside.

Let's walk through an example. Say you're buying a property for $180,000 and planning $70,000 in renovations (total cost: $250,000), with an estimated ARV of $350,000. At 90% LTC, you'd qualify for $225,000. Now, 75% of that $350,000 ARV comes out to $262,500—since the LTC number is lower, that's your limiting factor, and your maximum loan would be $225,000.

But flip the scenario: if that same property only had an ARV of $280,000, the 75% ARV cap would be $210,000—less than the $225,000 LTC calculation. Your lender would cap the loan at $210,000, meaning you'd need to bring an extra $40,000 to the table.

Here's the bottom line: these leverage limits show why accurate valuations and realistic renovation budgets matter so much. If you overestimate ARV or lowball your renovation costs, you could face a loan denial or come up short on funding to finish your project. Smart investors build solid relationships with appraisers, contractors, and real estate agents to keep their numbers grounded in reality. That's how you maximize your leverage while protecting your profit margins.

The Investor's Advantage: Weighing the Pros and Cons of Hard Money Lending

Hard money lending is a powerful tool in your real estate investing toolkit, but like any strategy, it comes with its own set of advantages and trade-offs worth understanding.

Getting a clear picture of both the upsides and downsides helps you make smart choices about when hard money loans make sense for growing your portfolio.

Why Investors Love Hard Money Loans

Less Paperwork About Your Income

Here's something that makes hard money lending refreshing: you don't need to jump through hoops proving your income. Traditional lenders want everything—W-2s, tax returns, pay stubs, years of financial statements. Hard money lenders? They care most about the property and whether the deal makes money. That means you can get funded based on how solid your investment is, not your personal income situation. Great news if you're self-employed, have income that doesn't fit the traditional mold, or just want to skip the paperwork headache of conventional loans.

Close Fast and Win More Deals

In real estate, speed wins. Being able to close quickly can be the difference between landing a great deal and watching someone else grab it. Hard money loans give you a real edge here.

Traditional bank loans? You're looking at 30–60 days minimum for approval and funding. Hard money lenders can get you approved and funded in as little as 10 days. Often, you can close in 2-3 weeks, sometimes even faster if you're prepared and the property checks out.

This matters most in hot markets where sellers want quick, reliable closings. With hard money pre-approval in your pocket, you can compete with cash buyers by showing you can close fast—while still using your capital wisely. When a great deal lands in your lap—a distressed property, a foreclosure auction, or an off-market gem that needs a quick close—hard money lending gives you the speed to act before the opportunity slips away.

High Leverage for Distressed Assets

Here's the reality: traditional lenders don't like fixer-uppers. Banks see distressed properties as risky business and often won't touch them—or they'll offer such a small loan that the numbers just don't work. Hard money lenders? This is exactly where they shine.

If you've got experience under your belt, you can often secure 85-90% Loan-to-Cost (LTC). That means the lender covers most of your purchase price and your renovation budget. Let's break that down with a real example: say you're buying a property for $200,000 that needs $50,000 in repairs. Your total project cost is $250,000. With an 85% LTC loan, you'd get $212,500 in financing—meaning you only need to bring $37,500 to close the deal.

That kind of leverage opens doors. Projects that seemed out of reach suddenly become possible, and you can take on bigger deals or juggle multiple projects at once.

Ability to Scale Portfolio Beyond DTI Limits

If you've ever tried to grow your portfolio with traditional financing, you've probably bumped into the Debt-to-Income (DTI) wall. Banks typically cap you at 43-50% DTI, which means after just a handful of properties, you're stuck—even if every single one is cash-flowing beautifully and you've never missed a payment.

Hard money lending sidesteps this problem completely. These lenders care about the deal itself—the property's value and the project's profit potential—not your personal income or how many mortgages you're already carrying. That means you can keep growing your portfolio without running into those frustrating DTI roadblocks. This freedom allows ambitious investors to scale their operations rapidly, taking on multiple projects simultaneously and building wealth at an accelerated pace.

Picture this: an investor might have ten rental properties financed conventionally and be maxed out on DTI, yet still secure hard money financing for their eleventh, twelfth, and thirteenth fix-and-flip projects based purely on those projects' merits.

Preserves Liquid Capital for Strategic Deployment

Here's something many investors overlook: hard money lending preserves your liquid capital. With leverage ratios reaching 85-90% of total project costs, you can maintain substantial cash reserves rather than tying up all your capital in a single project.

This capital preservation strategy offers multiple benefits:

- Emergency cushion: Unexpected renovation costs, market shifts, or personal emergencies can be managed without jeopardizing the project

- Opportunity fund: When another attractive deal emerges mid-project, you have capital available to pursue it

- Operating expenses: Holding costs, utilities, insurance, and other ongoing expenses can be covered comfortably

- Quality improvements: If market conditions suggest additional upgrades would significantly increase ARV, funds are available to capitalize on that opportunity

By maximizing leverage through hard money lending, savvy investors effectively use the lender's capital to generate returns while keeping their own cash working across multiple opportunities or held in reserve for strategic purposes.

The Important Trade-Offs and Considerations

Higher Interest Rates and Origination Fees

Let's be upfront: the speed, flexibility, and accessibility of hard money loans come at a cost—literally. Hard money loans typically carry interest rates ranging from 8% to 15%, significantly higher than conventional mortgages that might be in the 6-8% range. Additionally, origination fees (points) for hard money loans commonly run 2-5 points, meaning on a $200,000 loan, you might pay $4,000 to $10,000 in upfront fees.

These higher costs reflect the increased risk lenders take on when funding distressed properties with minimal documentation and tight timelines. Think of it this way: the lender is placing a bet on your ability to execute the project and exit before the loan term ends. For taking on that risk, they charge premium rates.

Here's the good news: smart investors understand that these higher costs often pay for themselves. Consider a fix-and-flip that puts $50,000 in your pocket—those extra interest costs become a small price to pay. Plus, the ability to close fast might be exactly what wins you the deal over competing buyers. The secret? Run your numbers carefully to make sure your project's profits can cover the financing costs and still leave you with solid returns.

Strict Project Profitability Requirements

Hard money lenders won't fund just any deal—they need to see clear evidence that your project will make money. Most require a minimum projected Return on Investment (ROI), usually between 10-20%, before giving you the green light. This "exit test" confirms you have enough financial motivation to finish the project and enough cushion to handle surprise expenses or market shifts.

For fix-and-flip deals, lenders dig into your purchase price, renovation budget, holding costs, and projected After Repair Value (ARV) to verify the deal hits their profitability benchmarks. For BRRRR (Buy, Rehab, Rent, Refinance, Repeat) projects, they'll examine your projected Debt Service Coverage Ratio (DSCR) to confirm your rental income will comfortably cover the refinanced loan payments—typically requiring a minimum DSCR of 1.1x or higher.

These standards can feel tough in hot markets where profit margins are thin, or when you're eyeing properties in up-and-coming neighborhoods where ARV estimates are less certain. The key is developing your skills at spotting and analyzing deals that clear these profitability hurdles while still delivering the returns you're after.

Short Maturity Horizons with Little Room for Delays

Hard money loans are short-term tools, typically running 12 months, though you might secure extensions to 18-24 months for bigger projects. This tight timeline means you need to execute efficiently—there's not much wiggle room when things go sideways.

Contractor hiccups, permit holdups, surprise structural issues, supply chain headaches, or bad weather can all throw your schedule off track. If your project runs past the loan maturity date, you're looking at some tough choices: paying steep extension fees, rushing to refinance or sell under pressure, or potentially facing default.

Here's how smart investors stay ahead of the clock:

- Build realistic timelines with buffer periods for the unexpected

- Partner with reliable, experienced contractors who deliver on schedule

- Stay on top of project management throughout the renovation

- Have backup plans ready for different exit scenarios

- Learn your local permit processes and factor those timelines in from day one

Bottom line: hard money loans aren't built for investors who like to take their time or struggle to keep projects moving. These loans reward you for acting decisively, executing efficiently, and solving problems before they snowball.

Requires Investor Experience for Best Terms

Here's the reality: while hard money lending opens doors that conventional financing keeps locked, the sweetest deals—lowest rates, highest leverage, most flexibility—go to investors who've proven themselves. Lenders sort borrowers into tiers based on experience, usually counting how many projects you've successfully completed.

If you're just starting out, expect:

- 75-80% LTC

- Higher interest rates (12-15%)

- Tougher exit profitability requirements (15-20% minimum ROI)

- Closer oversight and more frequent inspections

Once you've got 5+ completed projects under your belt, the picture changes:

- 85-90% LTC

- Lower interest rates (8-10%)

- More flexible exit requirements (10-15% minimum ROI)

- Smoother processes and greater flexibility

What does this mean for you? New investors pay more and face tighter rules while building their reputation. It's the cost of entry—but every experienced investor started exactly where you are now. However, this structure also creates a clear pathway for progression—each successfully completed project improves an investor's standing and unlocks better terms for future deals.

Making the Strategic Decision

Here's the bottom line: hard money lending isn't for every deal, and that's okay. The key is knowing when it makes sense for you. When the project is right and the numbers work, hard money loans give you speed, leverage, and flexibility that can supercharge your portfolio growth. Yes, the costs are higher—but think of them as the price of admission to opportunities you'd otherwise miss.

Smart investors don't see hard money as "expensive money to avoid." They see it as a powerful tool to pull out when the situation calls for it. Once you understand both the upsides and the trade-offs, you're in the driver's seat—able to choose hard money when it fits and pivot to other financing when it doesn't.

Practical Application: Mastering the Construction Holdback and Draw Process

Let's get into something that trips up a lot of investors: the construction holdback and draw process. On paper, it sounds simple—finish the work, request your funds, get reimbursed. In practice? It takes careful planning, solid documentation, and clear communication with your lender. Get this right, and your renovation hums along. Get it wrong, and you could find yourself cash-strapped with a half-finished project.

Understanding the Construction Holdback Mechanics

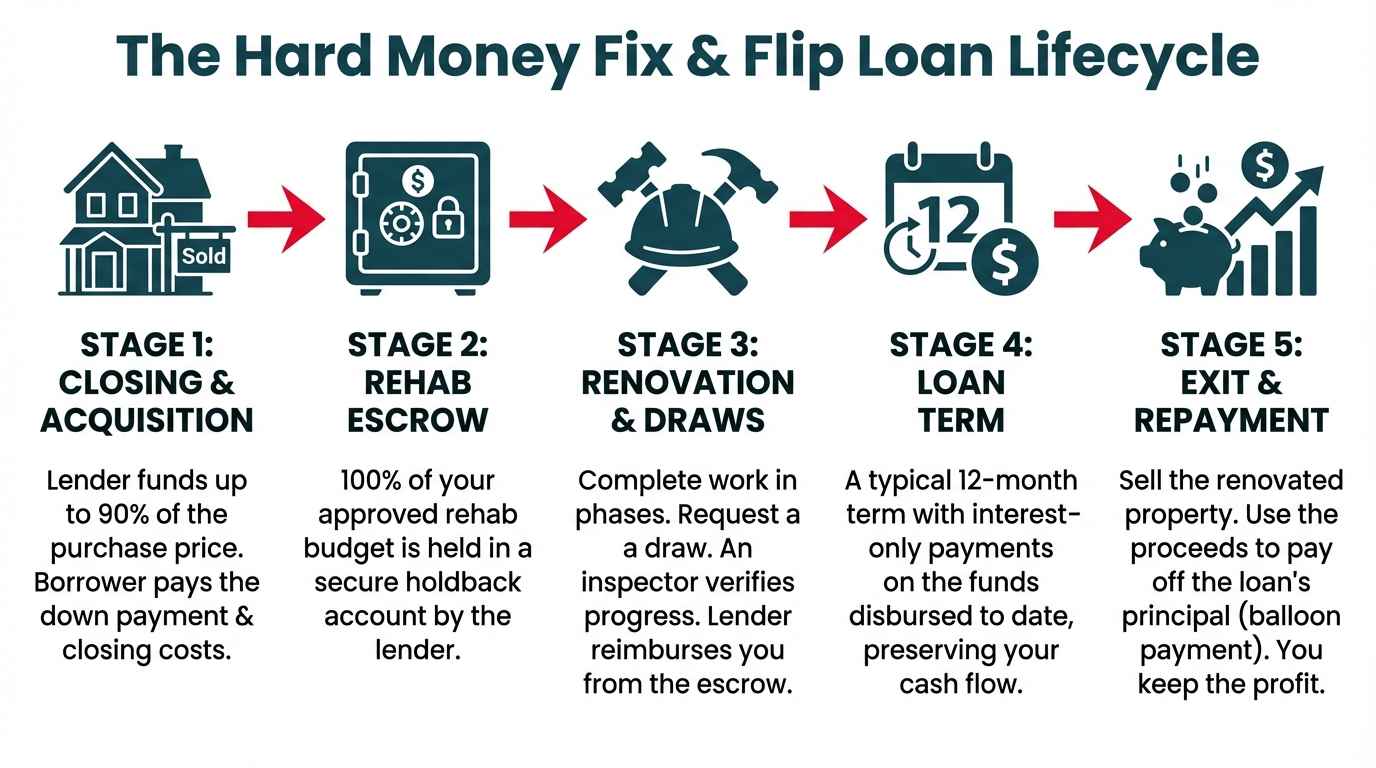

Here's how it works: when your hard money loan closes, the total amount gets split into two buckets. The first covers your purchase—that money goes out right away to acquire the property. The second is your renovation budget, held in escrow as a "construction holdback." You won't get access to those funds all at once. Instead, they're released in stages as you complete specific milestones in your renovation.

From an investor's perspective, this structure serves multiple purposes. First, it protects the lender by ensuring that loan funds are actually being used to improve the property's value. Second, it creates a built-in quality control mechanism—if work isn't completed to standard, funds won't be released. Third, it helps you maintain discipline in your renovation budget, preventing the common pitfall of overspending early in the project and running short later.

The draw process typically works on a reimbursement model. You pay contractors out of pocket for completed work, then submit a draw request to your lender for reimbursement. Some investors find this challenging initially, as it requires maintaining sufficient working capital to cover expenses between draws. But here's the upside—it keeps you closely involved in the project's financial management and prevents the temptation to draw funds prematurely.

According to industry standards, most hard money lenders structure their draw schedules with 3-5 inspection points throughout the renovation period, though this can vary based on project scope and loan size. Before you break ground, make sure you understand your specific lender's draw policies—including inspection requirements, processing timelines, and any restrictions on draw frequency.

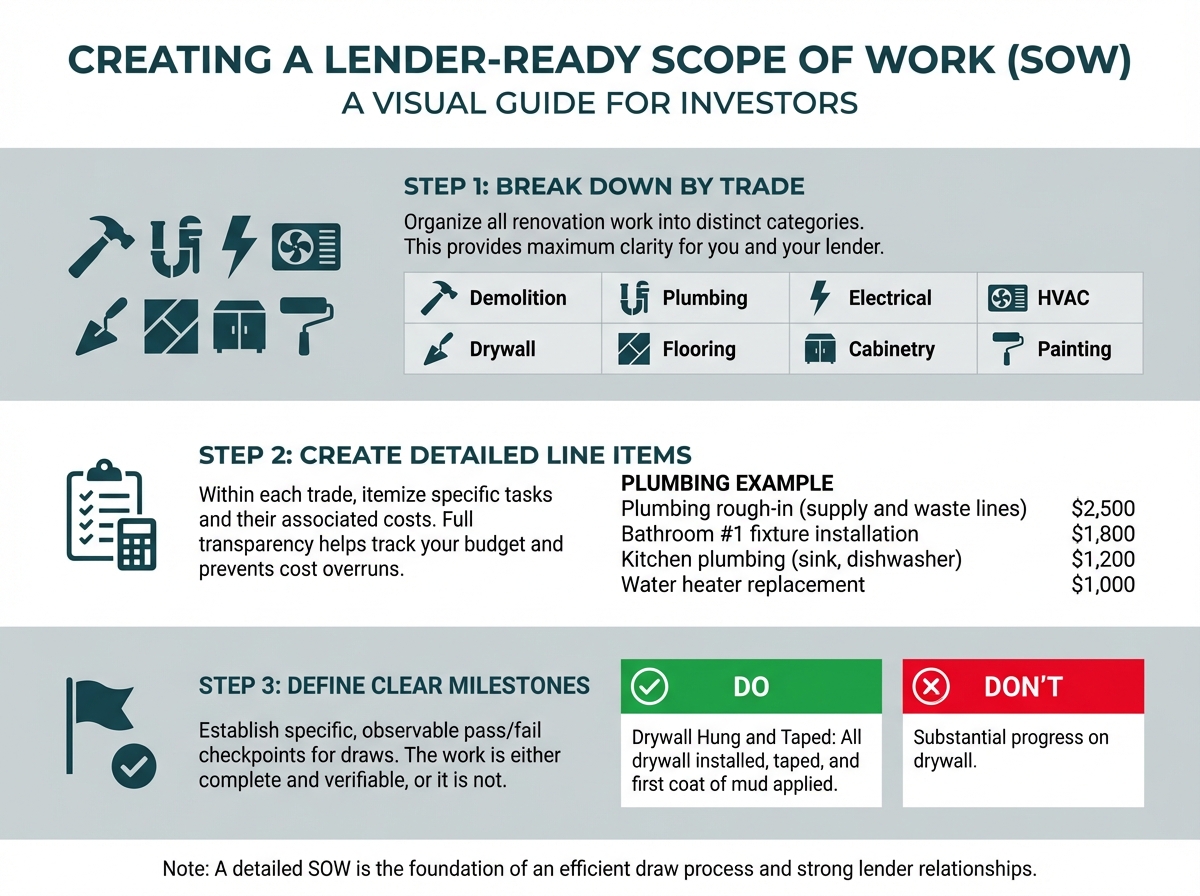

Structuring Your Scope of Work by Trade

The foundation of an efficient draw process is a meticulously structured Scope of Work (SOW). Rather than creating a general list of renovations, smart investors organize their SOW by specific trades, with detailed line items and clearly defined milestones for each phase of work.

Breaking Down by Trade

Start by categorizing all renovation work into distinct trade categories:

- Demolition and Site Preparation: Removing existing fixtures, flooring, cabinets, and preparing the space for new construction

- Structural and Framing: Any load-bearing wall modifications, additions, or structural repairs

- Plumbing: Rough-in work, fixture installation, water heater replacement, and final connections

- Electrical: Panel upgrades, rewiring, rough-in, fixture installation, and final inspections

- HVAC: System replacement or repair, ductwork modifications, and thermostat installation

- Roofing: Repairs, replacement, or modifications to the roof system

- Windows and Doors: Replacement or installation of exterior and interior doors and windows

- Insulation: Wall and attic insulation installation

- Drywall: Hanging, taping, mudding, and texturing

- Flooring: Subfloor repair, flooring installation (tile, hardwood, carpet, LVP)

- Cabinetry and Countertops: Kitchen and bathroom cabinet installation, countertop fabrication and installation

- Painting: Interior and exterior painting, trim work

- Fixtures and Finishes: Light fixtures, plumbing fixtures, hardware, and final touches

- Landscaping and Exterior: Yard work, hardscaping, exterior improvements

Creating Detailed Line Items

Within each trade category, break down the work into specific, measurable tasks with associated costs. For example, rather than listing "Plumbing - $8,000," your SOW should break it down like this:

- Plumbing rough-in (supply and waste lines): $2,500

- Bathroom #1 fixture installation (toilet, vanity, shower): $1,800

- Bathroom #2 fixture installation: $1,500

- Kitchen plumbing (sink, dishwasher, disposal): $1,200

- Water heater replacement (50-gallon gas): $1,000

Why does this level of detail matter? It gives your lender full transparency, helps you track actual costs against your budget, makes it easier to spot overruns before they snowball, and creates clear checkpoints when it's time to request draws.

Defining Clear Milestones

Each trade needs specific, observable milestones that qualify you for a draw. Think of these as pass/fail checkpoints an inspector can verify on the spot. Here's what good milestone definitions look like:

- Plumbing Rough-in Complete: All supply and waste lines installed, pressure tested, and ready for inspection

- Electrical Rough-in Complete: All wiring installed in walls, boxes mounted, and passed rough-in inspection

- Drywall Hung and Taped: All drywall installed, taped, and first coat of mud applied

- Kitchen Cabinets Installed: All base and wall cabinets installed, leveled, and secured

- Flooring Complete: All flooring materials installed and finished (excluding final cleanup)

Stay away from fuzzy language like "substantial progress on kitchen" or "most electrical work done." Stick to specific, yes-or-no criteria—the work is either complete and ready for inspection, or it's not.

Why a Well-Structured SOW Is Your Secret Weapon

Think of a solid Scope of Work as more than just paperwork—it's your roadmap to faster funding and a smoother renovation. When your SOW lines up neatly with your lender's draw schedule, inspectors can verify completion quickly, which means less waiting between submission and money in your account.

Here's the reality: lenders and inspectors review dozens of draw requests every week. A clean, logical SOW with well-defined milestones makes their job easier—and that works in your favor. When an inspector arrives and can immediately verify that "Plumbing Rough-in Complete" matches exactly what's documented in your SOW, approval happens faster. On the flip side, vague milestones invite questions, back-and-forth clarifications, and frustrating delays.

Here's another win: a detailed SOW has your back when contractor relationships get rocky. If disputes pop up about payment or scope, you've got a written document with specific line items and milestones to point to. It sets the ground rules from day one and cuts down on those "I thought that was included" conversations.

Think of your SOW as your project playbook. It helps you map out work in the right order, spot where one trade depends on another, and line up your contractors like clockwork. You'll clearly see that electrical rough-in needs to pass inspection before drywall goes up, and drywall has to be done before the painters roll in.

Tips for Faster Draw Reimbursements

Let's talk about getting your money back quickly—because in real estate investing, speed is your friend. The faster those draw reimbursements hit your account, the less cash you need tied up, and the more deals you can juggle at once. Here's how to make it happen:

Stay Ahead with Communication

Don't go radio silent until you're ready to submit a draw request. Touch base with your lender regularly, even just quick updates, to keep them in the loop on your progress. When you're closing in on a big milestone, give your lender a heads-up that a draw request is coming. This way, they can get inspections on the calendar ahead of time instead of scrambling.

Get to know your lender's inspection team. Learn when they're available and how they like to communicate. Some inspectors love getting a quick text with photos showing the work's done before they head out to your property. Others prefer everything go through the lender's official portal. Meeting them where they are shows you're a pro—and that often means faster responses.

When something unexpected throws a wrench in your timeline or you need to adjust the scope, pick up the phone right away. Lenders value honesty and are often willing to offer guidance or flexibility when you keep them in the loop early. Surprises that pop up during inspection, on the other hand, create headaches and slow everything down.

Accurate and Complete Documentation

Processing times for draw requests typically range from 3-5 business days when you submit all required documentation correctly. Missing or incomplete paperwork is the number one cause of delays, often tacking on a week or more to the process.

Here's what every draw request should include:

- Detailed invoices from your contractors showing completed work that matches your SOW line items

- Lien waivers (conditional or unconditional, depending on what your lender requires) from all contractors and suppliers for the work you're seeking reimbursement on

- High-quality photos documenting completed work from multiple angles, with clear visibility of the improvements

- Inspection reports or permits where applicable (especially for electrical, plumbing, and structural work)

- Draw request form completely filled out with accurate amounts and milestone descriptions

When it comes to photos, quality counts. Snap clear, well-lit images that capture the full scope of completed work. For rough-in work that'll end up behind walls, photograph it before the drywall goes up. Build a system—shoot each room from the same angles at every milestone so you can clearly show progression.

Keep your documentation organized and easy to navigate. Set up a folder structure on your computer or cloud storage that mirrors your SOW, so you can quickly find specific invoices or photos when it's time to submit a draw request. Many savvy investors also maintain a simple spreadsheet that tracks each line item, associated costs, contractor details, and documentation status.

Quality Work Meeting Professional Standards

Here's the truth: no amount of paperwork can make up for shoddy work. Inspectors know how to spot code violations, poor craftsmanship, and incomplete installations. When work doesn't meet standards, draws are denied until corrections are made, causing significant delays and straining contractor relationships.

Here's the smart move: invest in quality contractors with proven track records. Sure, hiring the lowest bidder might seem like a win for your budget, but experienced professionals who consistently deliver code-compliant work will actually save you time and money through faster draw approvals and fewer callbacks.

Before submitting any draw request, conduct your own pre-inspection. Walk through the property with your contractor and verify that work is truly complete and meets the standards outlined in your SOW. Here's your checklist:

- All work matches local building codes and permit requirements

- Installations are level, plumb, and properly secured

- Finishes are clean and professional-looking

- Safety standards are met (GFCI outlets in appropriate locations, handrails properly installed, etc.)

This simple step catches issues before the official inspection, saving you the frustration and delay of a rejected draw request.

Timely Draw Request Submission

Submit draw requests promptly as milestones are completed. Batching multiple milestones together might feel efficient, but it actually increases your risk and slows your cash flow. If issues pop up with one milestone, it can hold up reimbursement for all the work in that draw request.

Get into a rhythm with your draw schedule. Once you know inspections typically happen within 2-3 days of submission and funding occurs 2 days after approval, you can plan your cash flow with confidence. Be strategic about timing—submitting Monday morning gives the inspector the full week to schedule, while Friday afternoon submissions might sit until the following week.

Keep close tabs on your draw schedule. Know exactly how much of your construction holdback remains, what work is covered by upcoming draws, and how much working capital you need until the next reimbursement. This awareness is your best defense against cash flow crunches that can stall projects.

Create a draw request checklist that you follow religiously. This ensures you never submit incomplete requests and helps you maintain consistency across multiple projects. Your checklist might include items like: "All invoices collected and dated," "Lien waivers signed and notarized," "Photos uploaded to shared folder," "SOW milestone descriptions match exactly," and "Draw request form reviewed for accuracy."

When you master the construction holdback and draw process, you turn what many investors see as a paperwork headache into a real competitive edge. Your projects keep moving forward, your cash flow stays strong, and your lender relationships grow—all of which help you scale your real estate investment business with confidence.

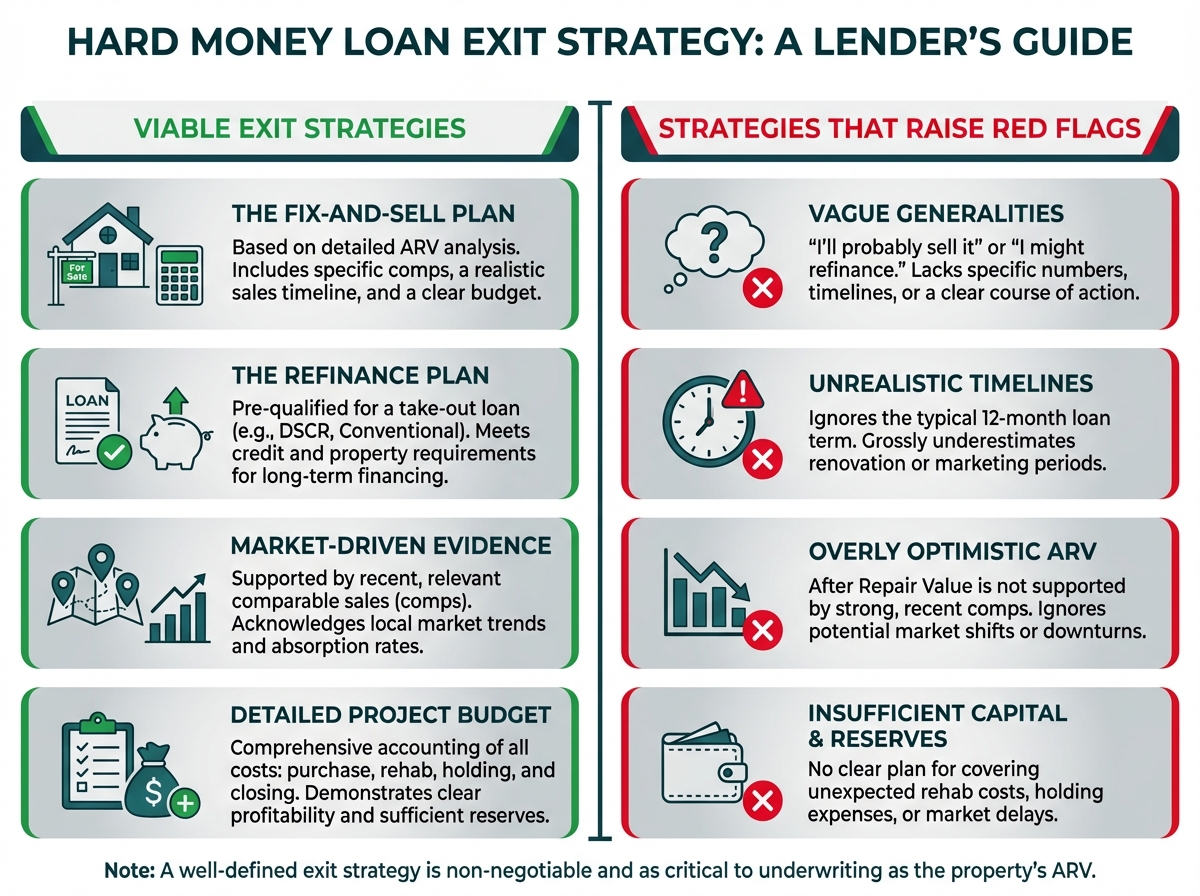

The Essential "Exit Strategy": Planning for Loan Maturity

Here's the reality: hard money loans typically run just 12 months. That means having a clear, well-defined exit strategy isn't optional—it's absolutely essential. Unlike a traditional 30-year mortgage where time is on your side, hard money loans require you to plan decisively from the very start. This tight timeline exists for a reason: these loans are designed to fund transformative projects, not to hold distressed properties long-term.

Why Lenders Require a Viable Exit Plan

Hard money lenders care about more than just the property's current condition or its potential after repairs. They need to know—with confidence—that you have a realistic, workable plan to repay the loan at maturity. This protects everyone: the lender gets repaid on schedule, and you're forced to honestly assess whether your project makes sense before putting capital at risk.

During underwriting, expect lenders to examine your exit strategy just as closely as they evaluate the property's After Repair Value (ARV). Vague answers like "I'll probably sell it" or "I might refinance" won't cut it. You need specific numbers, realistic timelines, and a solid grasp of your local market conditions.

Standard Exit Strategy #1: Selling the Property (Fix and Flip)

The fix and flip strategy is your most direct path out of a hard money loan. Here's how it works: you acquire a distressed property, complete a smart renovation that boosts its value, and sell the improved property for a profit—all before your loan term expires.

The "Exit Test" for Flips: Return on Investment (ROI)

Lenders aren't just checking that you'll turn a profit; they need to see a minimum projected Return on Investment (ROI) before they'll approve your loan. This threshold usually falls between 10% and 20%, depending on the lender, your track record, and how complex your project is.

Here's the bottom line: that ROI requirement protects both you and the lender. It ensures you have enough financial cushion to get the job done right and on schedule. If your projected profit margin is paper-thin, one unexpected cost overrun, market dip, or timeline hiccup could wipe out your profit completely—or worse, leave you struggling to repay the loan.

Calculating Your Exit ROI

Here's the straightforward formula lenders rely on:

ROI = (Sale Price - Total Project Cost) / Total Project Cost × 100

Your Total Project Cost includes:

- Purchase price

- Renovation costs

- Holding costs (interest payments, insurance, utilities, property taxes)

- Selling costs (agent commissions, closing costs, concessions)

Let's walk through a real example. Say you buy a property for $200,000, put $50,000 into renovations, spend $15,000 on holding and selling costs, and sell for $318,000. Your ROI would be:

ROI = ($318,000 - $265,000) / $265,000 × 100 = 20%

That 20% ROI clears most lenders' minimum requirements with room to spare—a solid exit strategy. But if your numbers only showed a 5% ROI? Most hard money lenders would pass on the deal or ask you to bring more cash to the table to improve the risk-reward balance.

Market Timing and Contingency Planning

Experienced investors always build buffer time into their exit timeline. If you're counting on selling in month 10 of a 12-month loan, you're leaving yourself very little margin for error. Market conditions can shift, properties can take longer to sell than anticipated, and unexpected renovation delays are common. Building in a 2-3 month buffer gives you breathing room and shows your lender you've done your homework.

Standard Exit Strategy #2: Refinancing into a Long-Term Rental Loan (The BRRRR Method)

The BRRRR method—Buy, Rehab, Rent, Refinance, Repeat—has become a go-to strategy for investors focused on building long-term wealth through rental property portfolios. Here's the idea: you use hard money for acquisition and renovation, then transition to a long-term, lower-interest rental loan once the property is stabilized and generating income.

How BRRRR Works as an Exit Strategy

Instead of selling the renovated property, you lease it to qualified tenants, establish a track record of rental income (typically 3-6 months of payment history), and then refinance into a long-term loan product like a DSCR (Debt Service Coverage Ratio) loan. This refinance pays off your hard money loan and converts your short-term, high-interest debt into long-term, lower-interest financing.

The BRRRR method lets you recycle your capital efficiently. In an ideal scenario, the refinance pulls out most or all of your initial investment, which you can then put to work on the next property—that's the "Repeat" in BRRRR.

The "Exit Test" for BRRRR: Debt Service Coverage Ratio (DSCR)

When refinancing is your exit strategy, lenders look at the property's ability to support debt through the Debt Service Coverage Ratio. DSCR requirements typically range from 1.1x to 1.25x, meaning the property's net operating income must exceed the proposed mortgage payment by 10% to 25%.

Here's the DSCR formula:

DSCR = Net Operating Income / Total Debt Service

Let's look at an example. If a property generates $2,500 per month in rent ($30,000 annually) and the proposed mortgage payment is $2,200 per month ($26,400 annually), the DSCR would be:

DSCR = $30,000 / $26,400 = 1. 14x

This 1.14x DSCR would meet most lenders' minimum requirements, showing that the rental income can comfortably cover the mortgage payment with a safety cushion for vacancies, maintenance, and unexpected expenses.

Why DSCR Loans Work Perfectly for BRRRR

DSCR loans are built with real estate investors in mind. They focus entirely on whether the property can generate enough income—not on your personal income, employment history, or debt-to-income ratio. That's what makes them such a great fit for the BRRRR strategy, especially if you:

- Are self-employed or have income that's tricky to document

- Own multiple properties and would blow past conventional DTI limits

- Want to grow your portfolio without being held back by personal income caps

- Appreciate straightforward paperwork and quicker closings

Seasoning Requirements and Timeline Considerations

Here's something important to keep in mind for your BRRRR exit: seasoning requirements. That's the minimum time you need to own a property before you can refinance. Some DSCR lenders ask for 6-12 months of ownership, while others offer no-seasoning or delayed-seasoning options that let you refinance right after renovations wrap up.

When you're mapping out your BRRRR exit strategy for your hard money lender, factor in:

- Renovation timeline (usually 3-6 months)

- Finding tenants and getting them moved in (1-2 months)

- Building up rental payment history (often 3-6 months)

- Refinance processing time (30-45 days)

All told, a BRRRR exit strategy usually takes the full 12-month loan term—and possibly an extension for bigger projects. Being upfront about these timelines in your initial hard money application shows you've done your homework and have a realistic game plan.

The Importance of a Robust, Realistic Exit Plan

Your exit strategy isn't just something to fill in on the loan application—it's the backbone of your entire investment. A solid exit plan includes:

Market Analysis: Show that you understand recent comparable sales (for flips) or rental comps and vacancy rates (for BRRRR). Generic statements won't suffice; you need specific data points from your target neighborhood.

Realistic Timelines: Factor in potential delays—renovation hiccups, permitting slowdowns, inspection hold-ups, tenant placement, or market absorption. Overly optimistic timelines are a red flag for experienced lenders.

Financial Buffers: Build contingency reserves into your budget (typically 10-15% of renovation costs) and profit projections. Deals that only work with zero margin for error rarely perform as planned.

Alternative Exit Paths: What's your backup if Plan A falls through? Planning to flip but the market cools? Could you pivot to rental? Executing BRRRR but can't hit target rents? Could you sell instead? Smart investors map out multiple scenarios before they start.

Professional Team: Line up your key partners before you need them—contractors, property managers, real estate agents, insurance providers. Lenders want to see experienced professionals ready to support your exit execution.

OfferMarket's DSCR Loan Specialty: Seamless BRRRR Exits

At OfferMarket, we know that many investors using hard money loans are running the BRRRR strategy. That's exactly why we've built specialized expertise in DSCR loans as your natural exit vehicle. Our integrated approach keeps you working with the same team from acquisition through refinance, giving you several clear advantages:

Streamlined Transition: We understand both the hard money acquisition phase and the DSCR refinance phase. That means we can structure your initial loan with your end goal in mind—no surprises when it's time to refinance.

Competitive DSCR Products: We partner with multiple capital providers to bring you DSCR loans with competitive rates, flexible terms, and options tailored to various property types and investor experience levels.

Holistic Underwriting: Our experience across the entire property lifecycle—from distressed acquisition through stabilized rental—gives us real-world insight into realistic ARVs, achievable rents, and viable exit timelines.

No Surprises: When you start with OfferMarket for your hard money loan, we give you preliminary DSCR refinance parameters upfront. That means you'll know exactly what metrics you need to hit for a successful exit before you even close on the property.

Whether you're flipping for profit or building long-term wealth through the BRRRR method, your exit strategy is the key to your hard money loan approval and project success. With OfferMarket's expertise in both hard money and DSCR products, you get a strategic partner who walks with you through the entire investment lifecycle—from distressed acquisition to stabilized, cash-flowing asset.

Putting It All Together: A Complete Fix and Flip Scenario with OfferMarket

Let's see how hard money lending actually works in the real world. We'll walk through a complete real estate investment scenario from acquisition to successful exit. This example shows how all the pieces—ARV calculation, loan terms, draw schedules, and exit strategies—fit together in an actual fix and flip project.

The Property: A Diamond in the Rough

Meet Sarah. She's an intermediate real estate investor with three successful flips under her belt. She's found a distressed single-family home in a desirable neighborhood that's been sitting on the market for 60 days. The property is a 3-bedroom, 2-bathroom home with 1,500 square feet that needs significant cosmetic and functional updates.

Initial Property Details:

- Purchase Price: $180,000

- Property Condition: Outdated kitchen and bathrooms, worn flooring, dated electrical panel, minor plumbing issues, overgrown landscaping

- Current Market Status: Non-owner occupied, vacant for 8 months

- Neighborhood Characteristics: Strong school district, low crime, increasing property values

Step 1: Calculating the After Repair Value (ARV)

Before Sarah can figure out if this deal makes financial sense, she needs to nail down the property's After Repair Value. The ARV represents the estimated market value of the property after all planned renovations are complete, and it's the cornerstone of every fix and flip deal you'll analyze.

Sarah digs into recently sold comparable properties (comps) in the same neighborhood with similar square footage, bedroom/bathroom counts, and condition. She finds five solid properties that sold within the past 90 days:

- Comp 1: 1,480 sq ft, 3bed/2bath, fully renovated - Sold for $295,000

- Comp 2: 1,520 sq ft, 3bed/2bath, fully renovated - Sold for $302,000

- Comp 3: 1,465 sq ft, 3bed/2bath, fully renovated - Sold for $288,000

- Comp 4: 1,550 sq ft, 3bed/2bath, fully renovated - Sold for $310,000

- Comp 5: 1,490 sq ft, 3bed/2bath, fully renovated - Sold for $298,000

After adjusting for slight differences in square footage, lot size, and specific amenities, Sarah lands on a conservative ARV of $295,000. Smart move—this conservative approach gives her breathing room against market shifts and appraisal surprises.

Step 2: Developing the Renovation Budget

Sarah puts together a detailed Scope of Work (SOW) broken down by trade—this will come in handy during the draw process. Here's how her renovation budget breaks down:

Kitchen Renovation: $18,000

- New cabinets and countertops

- Stainless steel appliances

- Tile backsplash

- Updated lighting fixtures

Bathroom Updates: $12,000

- Vanity replacements (both bathrooms)

- New toilets and fixtures

- Tile surrounds for shower/tub

- Modern lighting

Flooring Throughout: $8,500

- Luxury vinyl plank in living areas

- Carpet in bedrooms

- Tile in bathrooms

Electrical Upgrades: $4,500

- Panel upgrade to 200 amps

- Additional outlets

- LED lighting throughout

- Smart home integration prep

Plumbing Repairs: $3,000

- Replace old galvanized pipes

- New water heater

- Fix minor leaks

Interior Paint: $4,000

- Walls and trim throughout

- Neutral, modern color palette

Exterior Improvements: $6,000

- Fresh exterior paint

- Landscaping and curb appeal

- Mailbox and house numbers

- Pressure washing

HVAC Service: $2,500

- System inspection and tune-up

- Duct cleaning

- Thermostat upgrade

Contingency (10%): $5,850

- Your safety net for those unexpected surprises

Total Renovation Budget: $64,350 (rounded to $65,000 for planning purposes)

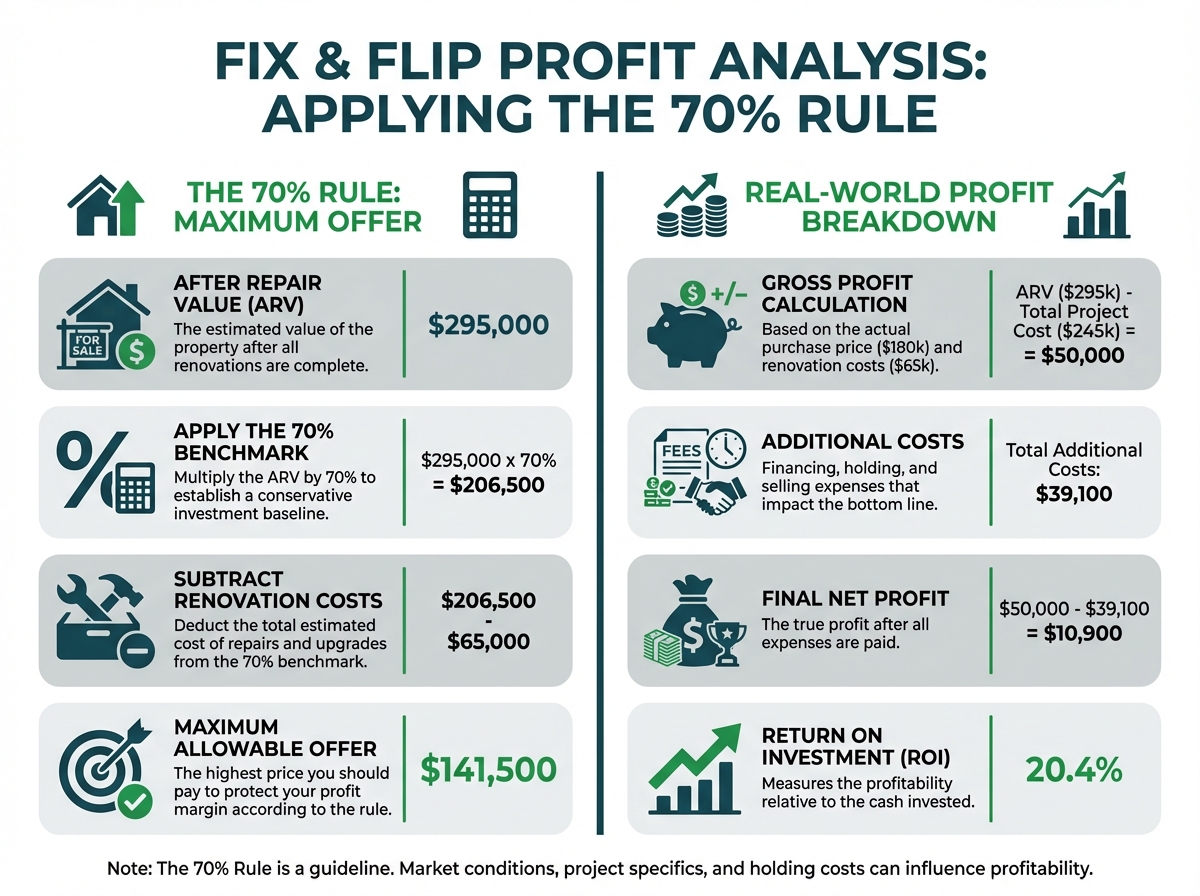

Step 3: Applying the 70% Rule and Maximum Allowable Offer

[A tried-and-true guideline that seasoned flippers swear by is the 70% Rule](https://merchantsmtg. com/fix-and-flip-calculator-how-much-financing-should-you-take-on/), which suggests you shouldn't pay more than 70% of the ARV minus renovation costs. This rule helps protect your profit margin while leaving room for holding costs, selling expenses, and those curveballs every project throws your way.

Maximum Allowable Offer Calculation:

- ARV: $295,000

- 70% of ARV: $206,500

- Minus Renovation Costs: $65,000

- Maximum Purchase Price: $141,500

Sarah's negotiated purchase price of $180,000 sits above this conservative benchmark, but here's why she's confident moving forward:

- Her ARV estimate leaves room for upside

- The market is trending upward

- Trusted contractor relationships keep her renovation costs predictable

- Strong neighborhood demand means faster sales

Let's break down her projected profit using her actual numbers:

Profit Calculation:

- ARV: $295,000

- Purchase Price: $180,000

- Renovation Costs: $65,000

- Total Project Cost: $245,000

- Gross Profit: $50,000

After accounting for additional costs:

- Hard Money Interest (estimated): $10,800

- Closing Costs (purchase): $5,400

- Holding Costs (utilities, insurance, taxes for 6 months): $4,200

- Selling Costs (6% commission + closing): $18,700

- Total Additional Costs: $39,100

Net Profit: $10,900 Return on Investment (ROI): 20.4% on cash invested

Step 4: Securing Hard Money Financing with OfferMarket

Sarah submits her fix and flip loan application through OfferMarket. With 3 successful projects under her belt, she qualifies for competitive terms:

Loan Structure:

- Purchase Price: $180,000

- Renovation Budget: $65,000

- Total Loan Amount: $245,000

- Loan-to-Cost (LTC): 100% (Sarah brings no money to closing for the purchase, though she'll cover some soft costs)

- Loan-to-ARV: 83% ($245,000 / $295,000)

- Interest Rate: 10.5% annually

- Loan Term: 12 months

- Interest Structure: Interest-only monthly payments, calculated "as disbursed" on the unpaid principal balance

- Origination Fee: 2 points ($4,900)

- Down Payment Required: $0 on purchase (OfferMarket funds 100% of acquisition)

Initial Disbursement at Closing:

- Purchase Price: $180,000 (paid directly to seller)

- Closing Costs: $5,400 (Sarah pays from her reserves)

- Origination Fee: $4,900 (Sarah pays from her reserves)

- Construction Holdback: $65,000 (held in escrow, released through draws)

Sarah's out-of-pocket cash at closing: $10,300 (closing costs + origination fee)

Step 5: The Draw Schedule by Renovation Phase

OfferMarket sets up Sarah's construction holdback to release funds at key renovation milestones. This "as disbursed" interest structure means Sarah only pays interest on funds actually released, keeping her carrying costs lower during the renovation phase.

Draw Schedule Timeline:

Draw 1 - Week 2 (Demolition & Rough-In Phase): $15,000

- Demolition of kitchen and bathrooms completed

- Electrical panel upgrade finished

- Plumbing rough-in complete

- HVAC inspection and repairs done

- Documentation Required: Invoices from electrician and plumber, photos of completed work, lien waivers

- Outstanding Loan Balance: $195,000 (purchase + first draw)

- Monthly Interest Payment: $1,706

Draw 2 - Week 5 (Framing & Mechanical Phase): $18,000

- All electrical work completed and inspected

- Plumbing installation finished

- HVAC work complete

- Drywall hung and finished

- Documentation Required: Passed electrical inspection certificate, plumbing completion photos, contractor invoices, lien waivers

- Outstanding Loan Balance: $213,000

- Monthly Interest Payment: $1,864

Draw 3 - Week 8 (Finish Work Phase 1): $20,000

- Interior painting completed

- Flooring installation finished

- Kitchen cabinets and countertops installed

- Documentation Required: Photos of completed rooms, flooring warranty documentation, cabinet installation invoice, lien waivers

- Outstanding Loan Balance: $233,000

- Monthly Interest Payment: $2,039

Draw 4 - Week 11 (Final Finishes): $12,000

- Kitchen appliances installed

- Bathroom vanities and fixtures complete

- Exterior painting finished

- Landscaping and curb appeal work done

- Final walkthrough items addressed

- Documentation Required: Final completion photos, appliance receipts, landscape contractor invoice, lien waivers

- Outstanding Loan Balance: $245,000

- Monthly Interest Payment: $2,144

Total Construction Timeline: 12 weeks (3 months)

Step 6: Run Your Numbers with OfferMarket's Fix and Flip Calculator

Before Sarah commits to this deal, she runs her numbers through OfferMarket's fix and flip calculator. This tool helps her model different scenarios and stress-test her assumptions—so she knows exactly what she's getting into. The calculator allows her to input:

- Purchase price and renovation costs

- Expected ARV and comparable sales data

- Loan terms and interest rates

- Estimated timeline from acquisition to sale

- Holding costs and selling expenses

Scenario Modeling:

Best Case Scenario (Quick Sale, Higher ARV):

- Sale Price: $305,000 (market appreciation)

- Timeline: 5 months total (3 months renovation + 2 months to sell)

- Net Profit: $18,400

- ROI: 178% annualized

Base Case Scenario (Expected Outcome):

- Sale Price: $295,000

- Timeline: 6 months total (3 months renovation + 3 months to sell)

- Net Profit: $10,900

- ROI: 127% annualized

Worst Case Scenario (Extended Timeline, Lower Sale Price):

- Sale Price: $280,000 (market softening)

- Timeline: 9 months total (4 months renovation + 5 months to sell)

- Net Profit: -$2,100 (small loss)

- ROI: -20% annualized

Here's the key takeaway: even if everything goes sideways—delays pile up and prices dip—Sarah's exposure stays manageable. That's the power of running your numbers beforehand. She moves forward with confidence, knowing she's built in a healthy cushion for the unexpected.

Step 7: Project Execution and Timeline Management

With her contractor network already in place, Sarah hits the ground running on her renovation:

Month 1 (Weeks 1-4):

- Close on property with OfferMarket financing

- Kick off demolition and rough-in work

- Submit and receive Draw 1

- Interest Paid: $1,575 (average balance during month)

Month 2 (Weeks 5-8):

- Wrap up mechanical systems and drywall

- Submit and receive Draw 2

- Move into finish work

- Submit and receive Draw 3

- Interest Paid: $1,837

Month 3 (Weeks 9-12):

- Button up all finish work

- Submit and receive Draw 4

- Final cleaning and staging

- Get the property on the market

- Interest Paid: $2,091

Month 4 (Marketing and Showings):

- Professional photography and marketing launch

- Host open houses and private showings

- Field multiple offers

- Accept offer at $297,000 (slightly above ARV—nice work, Sarah!)

- Interest Paid: $2,144

Month 5 (Under Contract):

- Buyer inspection and appraisal

- Handle minor touch-ups from inspection findings

- Coordinate closing details

- Interest Paid: $2,144

Month 6 (Closing):

- Final walkthrough with buyer

- Close on sale

- Pay off OfferMarket loan in full

- Interest Paid: $1,072 (partial month)

Total Interest Paid: $10,863

Step 8: The Exit Strategy - Selling the Property

Sarah's game plan? A straightforward sale to an end buyer. Her property hits the market in Month 3 with:

- Professional staging in living room and master bedroom

- High-quality listing photos highlighting renovations

- Competitive pricing at $299,000 (slightly above ARV to negotiate down)

- Strong marketing through local real estate agent

Within three weeks, she receives four offers and accepts one at $297,000 with a 30-day close, which extends to 45 days due to buyer financing. The property appraises at $298,000, confirming her ARV analysis was spot-on.

Sale Details:

- Final Sale Price: $297,000

- Time on Market: 21 days to contract, 45 days to close

- Buyer: Traditional homebuyer with conventional financing

- Appraisal: $298,000 (validates renovation quality and ARV estimate)

Step 9: Final Financial Settlement and ROI Calculation

Now let's break down the numbers at closing:

Revenue:

- Sale Price: $297,000

Total Project Costs:

- Purchase Price: $180,000

- Renovation Costs: $65,000

- Hard Money Interest: $10,863

- Origination Fee (2 points): $4,900

- Purchase Closing Costs: $5,400

- Holding Costs (utilities, insurance, taxes): $3,600

- Selling Costs (6% commission): $17,820

- Seller Closing Costs: $2,200

- Total Costs: $289,783

Net Profit: $7,217

Cash Invested by Sarah:

- Down Payment: $0

- Origination Fee: $4,900

- Purchase Closing Costs: $5,400

- Holding Costs (from reserves): $3,600

- Total Cash Invested: $13,900

Return on Investment (ROI): 51.9% ($7,217 profit / $13,900 invested)

Annualized ROI: 103.8% (over 6-month period)

Here's the reality: Sarah's final profit came in lower than her initial projection. The timeline stretched a bit longer, and the property sold just above—rather than at the top of—her ARV range. But here's what matters: she still walked away with an excellent return on her invested capital. That 103.8% annualized ROI? That's the power of leverage working in her favor.

Key Takeaways from This Scenario

The Power of Leverage: Sarah controlled a $245,000 project with just $13,900 of her own money, generating a 51. 9% cash-on-cash return in six months.

Importance of Conservative ARV Estimates: By estimating ARV conservatively at $295,000, Sarah built in a safety margin that protected her when the property sold at $297,000 rather than at a higher price point.

Draw Structure Efficiency: The "as disbursed" interest structure saved Sarah approximately $1,800 compared to "full boat" interest on the entire loan amount from day one.

Timeline Management: Completing renovations in 12 weeks kept the project on track, though the sales timeline extended slightly beyond projections—a common occurrence that Sarah had wisely budgeted for in her contingency planning.

OfferMarket's Calculator Value: By modeling multiple scenarios before committing, Sarah knew exactly what she was getting into—her risk exposure and profit potential—allowing her to make a confident, informed investment decision.

This complete walkthrough shows you how hard money lending through OfferMarket helps real estate investors execute profitable fix and flip projects with minimal capital investment, high leverage, and a clear roadmap to success. The combination of competitive loan terms, flexible draw structures, and practical tools like the fix and flip calculator gives you the confidence to pursue opportunities and grow your portfolio.

OfferMarket's Competitive Advantage: An Integrated Real Estate Investment Ecosystem

Here's the reality of today's real estate investment landscape: success depends on more than just access to capital. Smart investors understand that integrated financial platforms combining multiple services under one roof deliver real advantages in speed, efficiency, and cost savings. That's exactly what we've built at OfferMarket—a comprehensive ecosystem that gives real estate investors a seamless experience extending far beyond traditional hard money lending.

Multiple Capital Providers, Maximum Flexibility

Here's what sets OfferMarket apart from single-product lenders: we partner with multiple capital providers to bring you a full toolkit of financing solutions for every step of your investment journey. No cookie-cutter products here. Instead, you get access to options that actually fit your strategy:

Fix and Flip Loans: This is our bread-and-butter hard money product, built for investors who buy distressed properties, renovate them, and sell for profit. Experienced investors can tap into up to 90% LTC with competitive rates—giving you the leverage and speed to jump on deals before they disappear.

DSCR (Debt Service Coverage Ratio) Loans: Running the BRRRR strategy or picking up stabilized rentals? These loans qualify based on what the property earns, not what you earn personally. That means you can grow your portfolio without bumping into traditional DTI walls. Bonus: DSCR loans make a perfect exit from your fix and flip financing, smoothly transitioning you from renovation mode to long-term hold.

Slow Flip Loans: Some projects need more breathing room. Slow flip loans bridge the gap between fix and flip and rental financing, giving you extended timelines to finish renovations or season a property with tenants before refinancing. When your deal doesn't fit the standard mold, this hybrid product has you covered.

Low Balance DSCR Loans: Not every solid investment comes with a six-figure price tag. Our specialized low balance DSCR products work for properties under typical minimum loan amounts—opening doors in emerging markets or for investors targeting affordable, cash-flowing properties.

HELOANs and HELOCs: Already have equity sitting in your existing properties? Put it to work. Home equity loans and lines of credit give you flexible, cost-effective capital to fund your next acquisition or renovation project. These products enable experienced investors to recycle capital efficiently and maintain momentum across multiple projects simultaneously.