*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

How to Find and Vet the Right Investment Loan Broker

Finding the right investment property loan broker can be the difference between a stalled portfolio and accelerated growth. A great broker acts as your strategic partner, unlocking financing that aligns perfectly with your goals. A subpar one can cost you time, money, and the deal itself. Vetting is non-negotiable. Start by asking targeted questions that reveal their true capabilities and experience.

Key Questions to Ask About Their Lender Network and Experience

Before committing, treat the process like a job interview—because you are hiring them for a critical role.

"How many active lenders are in your network, and what are their specialties?" A broker's value is their network. A broad network is good, but a deep, specialized one is better. You want to hear names of national private lenders, regional banks, and niche hard money sources, not just a handful of go-to options. Ask if they have direct relationships with the underwriters or just a general submission portal.

"Can you describe a few recent deals you've closed that are similar to mine?" This question tests their direct experience. If you're flipping a house in Baltimore, a broker who primarily funds new construction in California may not be the best fit. Listen for their understanding of your specific market, property type, and deal structure.

"What is your process for packaging and submitting a loan?" A professional broker won't just "shotgun" your application to every lender. They should describe a methodical process: analyzing the deal, identifying the 3-5 best-fit lenders, and tailoring the loan package to meet each lender's specific underwriting guidelines.

"How are you compensated?" Transparency is key. Most brokers are paid via origination points (typically 1-2% of the loan amount) paid at closing. This fee is often built into the loan or paid out of pocket. Be wary of anyone who is vague about their compensation structure.

"What is your communication policy?" The loan process involves many moving parts. Ask how often you can expect updates and their preferred method of communication (email, phone, portal). A good broker will keep you informed proactively, especially when challenges arise.

Verifying Their Specialty Aligns with Your Investment Strategy

Not all brokers are created equal. A broker who excels at securing DSCR loans for long-term rentals may not have the right lender network for a high-leverage fix and flip loan.

For Flippers: Ask about their experience with deals requiring rehab draws. Do their lenders fund 100% of the renovation costs? How quickly are draws disbursed? They need to understand the importance of speed and leverage (Loan-to-Cost and After-Repair-Value).

For Rental Investors: Inquire about their top lenders for DSCR products. What are the typical DSCR and LTV requirements? Do they have options for portfolio loans or cash-out refinances? Their expertise should be in long-term, cash-flow-based financing.

For BRRRR Investors: The "Buy, Rehab, Rent, Refinance, Repeat" strategy requires a broker who understands both short-term bridge financing for the acquisition/rehab and long-term DSCR financing for the exit. Ask if they can seamlessly facilitate the transition from the bridge loan to the permanent financing.

For Builders: If you're doing ground-up construction, you need a specialist. Ask about their experience with construction loans, draw schedules, and lenders who understand the development lifecycle.

Red Flags: Vague Answers, Upfront Fees, and Guaranteed Approvals

Protect yourself by spotting warning signs early.

Upfront Fees: A reputable broker's compensation is tied to successfully closing your loan. Be extremely cautious of anyone asking for a significant, non-refundable "application," "processing," or "due diligence" fee before they've even submitted your deal to a lender. Legitimate third-party costs like appraisals are normal, but large upfront broker fees are a major red flag.

"Guaranteed Approval": No one can guarantee a loan approval. The final decision always rests with the lender's underwriter. A broker who promises a 100% guarantee is being dishonest and likely desperate for your business. They should speak in terms of confidence based on their experience, not in absolutes.

Vague or Evasive Answers: If you ask about their lender network and they say, "We have a lot of them," or you ask about fees and they say, "We'll figure it out," press for specifics. A lack of transparency at the beginning often leads to problems later.

Lack of a Digital Presence or Professionalism: Check their website, LinkedIn profile, and online reviews. Look for a professional presence and a history of successful closings. It's also wise to verify their license through the NMLS Consumer Access website.

Requesting Case Studies or References for Similar Deals

The ultimate proof is in their track record. Ask for anonymized case studies or "tombstones" of recent deals. This should outline the property type, loan scenario, challenges, and the final loan terms they secured.

If you're considering a long-term partnership, ask for references from past clients whose investment strategy mirrors yours. A quick call with a fellow investor can provide invaluable insight into the broker's communication style, problem-solving skills, and overall effectiveness. A confident, successful broker will be happy to connect you with satisfied clients.

Why Use an Investment Property Loan Broker?

While some investors prefer to go directly to a lender, a skilled investment property loan broker provides four distinct advantages that can be crucial for scaling a real estate business: access, expertise, time savings, and negotiation leverage.

Access to a Diverse Network of Private and Hard Money Lenders

A single bank or direct lender has one set of guidelines, one "credit box," and one product sheet. If your deal doesn't fit perfectly, the answer is a simple "no." A broker, on the other hand, maintains relationships with dozens, sometimes hundreds, of lenders. This network includes:

National Private Lenders: Large, institutional-style lenders with competitive rates for standard fix-and-flip or DSCR loans.

Regional Banks & Credit Unions: Sometimes offer portfolio loans for investors with a strong local presence.

Hard Money Lenders: Asset-focused lenders who can close quickly on value-add projects that traditional institutions won't touch.

Niche Capital Sources: Lenders specializing in specific asset classes like ground-up construction, short-term rentals, or small-balance commercial properties.

This variety means that instead of trying to force your deal into one box, a broker can find the box that was built for your deal. This is especially critical for investors with unique scenarios, such as a property needing significant renovation, a borrower with a complex income history, or a desire to use creative financing strategies.

Expertise in Structuring Complex or Non-Traditional Deals

Experienced brokers are more than just matchmakers; they are deal architects. They understand the nuances of how different lenders underwrite risk and can structure your loan application to highlight its strengths.

Example Scenario:

An investor wants to buy a vacant, unrentable triplex (a "value-add" project). A conventional bank sees no income and a distressed asset, leading to a quick rejection.

- The Broker's Approach: The broker recognizes this isn't a bank deal. They position it as a bridge loan opportunity for a hard money lender. They help the investor create a detailed scope of work, a realistic budget, and a strong pro-forma analysis showing the property's potential income after renovation. They submit this package to lenders who specialize in funding based on the "After-Repair Value" (ARV), securing financing not just for the purchase but also for 100% of the construction costs. The broker has transformed a "no" into a funded deal by understanding how to structure and present it to the right capital source.

Significant Time Savings in Sourcing and Managing the Loan Process

As an investor, your most valuable asset is time. Sourcing a loan is a time-intensive process: researching lenders, filling out multiple applications, fielding calls, and submitting documents over and over. A broker streamlines this entire workflow.

One Application, Many Options: You provide your information and deal documents to the broker once. They then use that single package to shop your loan with multiple suitable lenders.

A Single Point of Contact: Instead of juggling communications with several loan officers, you have one point of contact who manages the entire process. The broker chases down underwriters, coordinates with the title company, and pushes the loan toward the closing table, freeing you up to find your next deal.

This efficiency can easily save you 40-50 hours of administrative work on a single transaction.

Negotiation Leverage for Better Rates, Terms, and Lower Fees

Brokers who bring significant deal volume to lenders often have preferred relationships. This can translate into tangible benefits for the borrower.

Better Rates: A broker might have access to a preferred pricing tier not available to the general public. Even a 0.25% rate reduction can save thousands over the life of a loan.

More Favorable Terms: They can negotiate for higher leverage (e.g., 80% LTV instead of 75%), a longer interest-only period, or the removal of a prepayment penalty.

Reduced Fees: In some cases, a broker's relationship can lead to a reduction in the lender's origination points or underwriting fees.

While the broker charges a fee for their service (typically 1-2 points), the value they provide through better terms can often outweigh their cost. By securing a loan with higher leverage, you preserve more of your own capital for the next investment, effectively increasing your ROI and ability to scale.

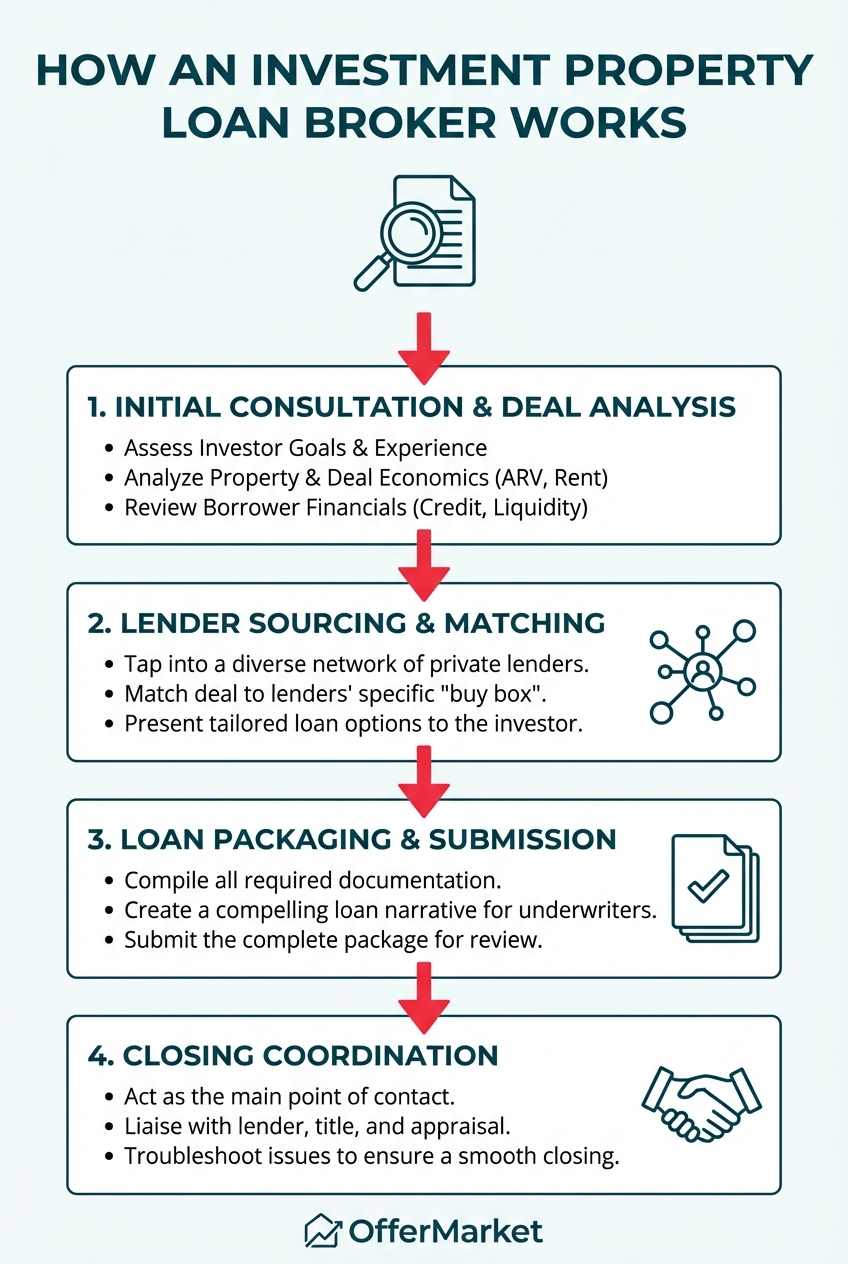

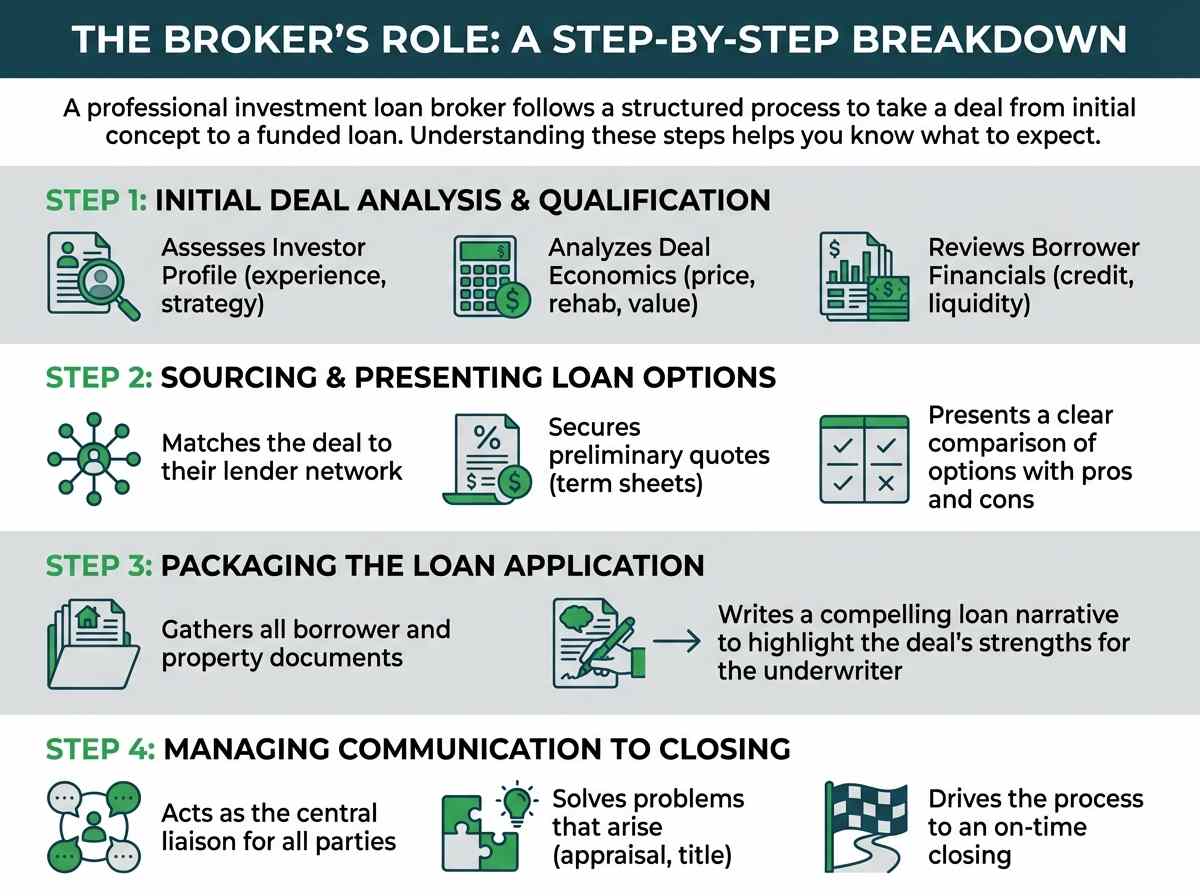

The Broker's Role: A Step-by-Step Breakdown

A professional investment loan broker follows a structured process to take a deal from initial concept to a funded loan. Understanding these steps helps you know what to expect and how to best collaborate with them.

Initial Deal Analysis and Borrower Qualification Assessment

This is the discovery phase. The broker's first job is to understand you and your deal inside and out.

Investor Profile: They'll ask about your real estate experience (number of flips or rentals owned in the last 24-36 months), your overall strategy (fix and flip, long-term rental), and your goals for this specific transaction.

Deal Economics: You'll provide the property address, purchase price, rehab budget (if any), and projected after-repair value or rental income. The broker will perform a preliminary analysis to see if the numbers meet general lender guidelines for metrics like LTV, LTC, and DSCR.

Borrower Financials: They will ask for a high-level overview of your credit score, liquidity (cash on hand for down payment, closing costs, and reserves), and any other real estate you own. This helps them pre-qualify you and identify which lender programs you're likely to fit into.

Sourcing and Presenting Tailored Loan Options

Once the broker has a clear picture of the deal, they move to the matchmaking phase.

Lender Matching: Drawing on their network, they identify a shortlist of 3-5 lenders whose "credit box" aligns with your deal. They consider factors like the lender's preferred property type, location, loan size, and investor experience level.

Preliminary Quotes: The broker will often send a brief, no-names deal summary to these lenders to gauge interest and get preliminary terms (a term sheet). This includes the interest rate, origination points, LTV/LTC, and any other key conditions.

Presenting Options: The broker consolidates these term sheets and presents them to you in an easy-to-compare format. A great broker will also provide context, explaining the pros and cons of each option. For example: "Lender A has the lowest rate, but they are known to be slow to close. Lender B is slightly more expensive, but they can close in 10 days and have a very smooth draw process for your rehab funds."

Packaging the Loan Application for Underwriter Review

After you select a lender, the broker's role shifts to that of a project manager. They are responsible for assembling a complete and compelling loan package that makes the underwriter's job easy. This package typically includes:

Borrower Documents:Schedule of real estate owned (SREO), entity documents (LLC operating agreement), and bank statements for liquidity verification.

Property Documents: Purchase and sale agreement, scope of work/rehab budget, and lease agreements (for rental properties).

The Loan Narrative: A skilled broker writes a cover letter or summary that tells the story of the deal. It highlights the strengths of the borrower and the property, explains the business plan, and justifies the loan request. This narrative can be critical in getting a borderline deal approved.

Managing Communication and Documentation Through Closing

From submission to closing, the broker is the central hub of communication.

Liaison: They act as the single point of contact between you, the lender's processor and underwriter, the appraiser, and the title/escrow company.

Problem-Solving: When issues arise—an appraisal comes in low, a title issue is discovered, or the underwriter asks for more documentation—the broker takes the lead in finding a solution. Their experience and relationships are invaluable here.

Driving to Close: They are responsible for keeping the process moving, following up on outstanding items, and ensuring all parties meet their deadlines to get the loan closed on time.

Get Your 2026 Term Sheet in 2 Minutes

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →Understanding the Lender's Playbook: What Your Broker Navigates

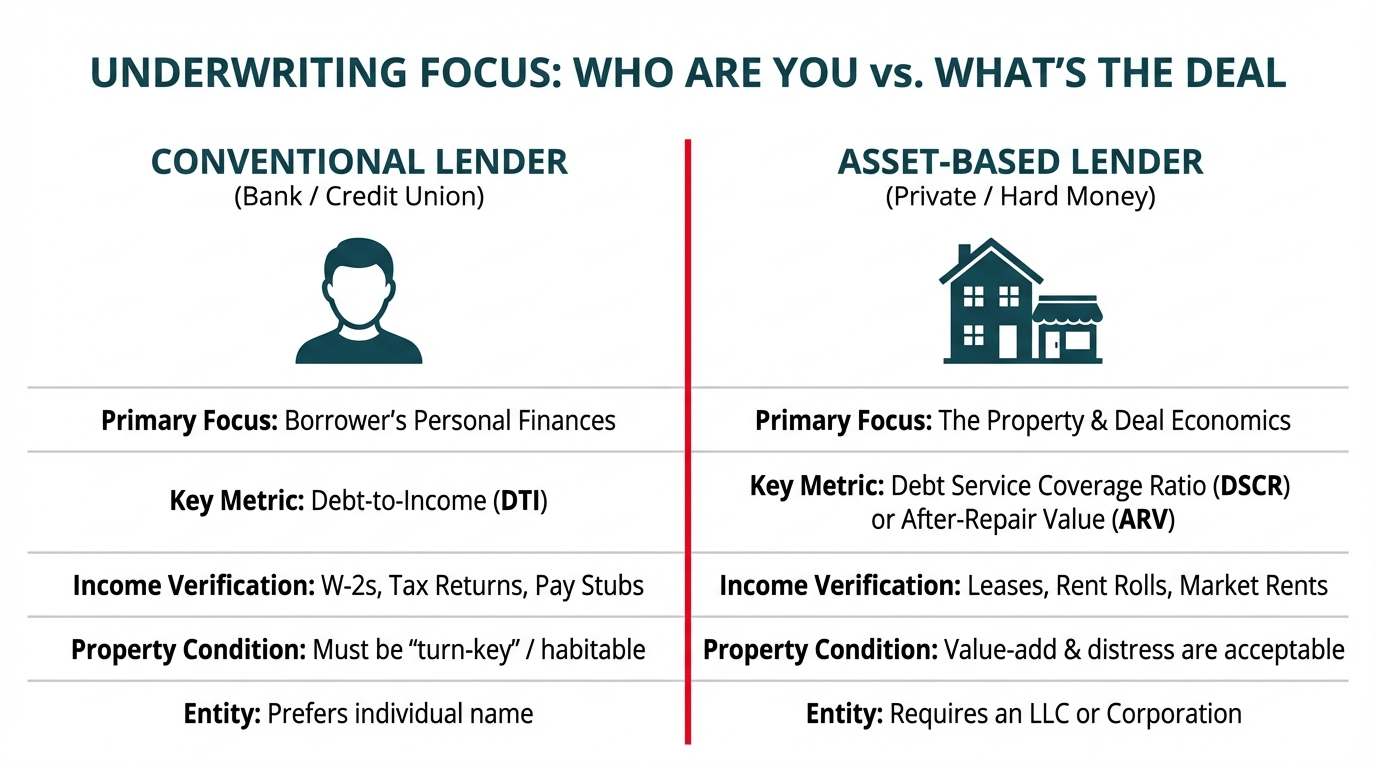

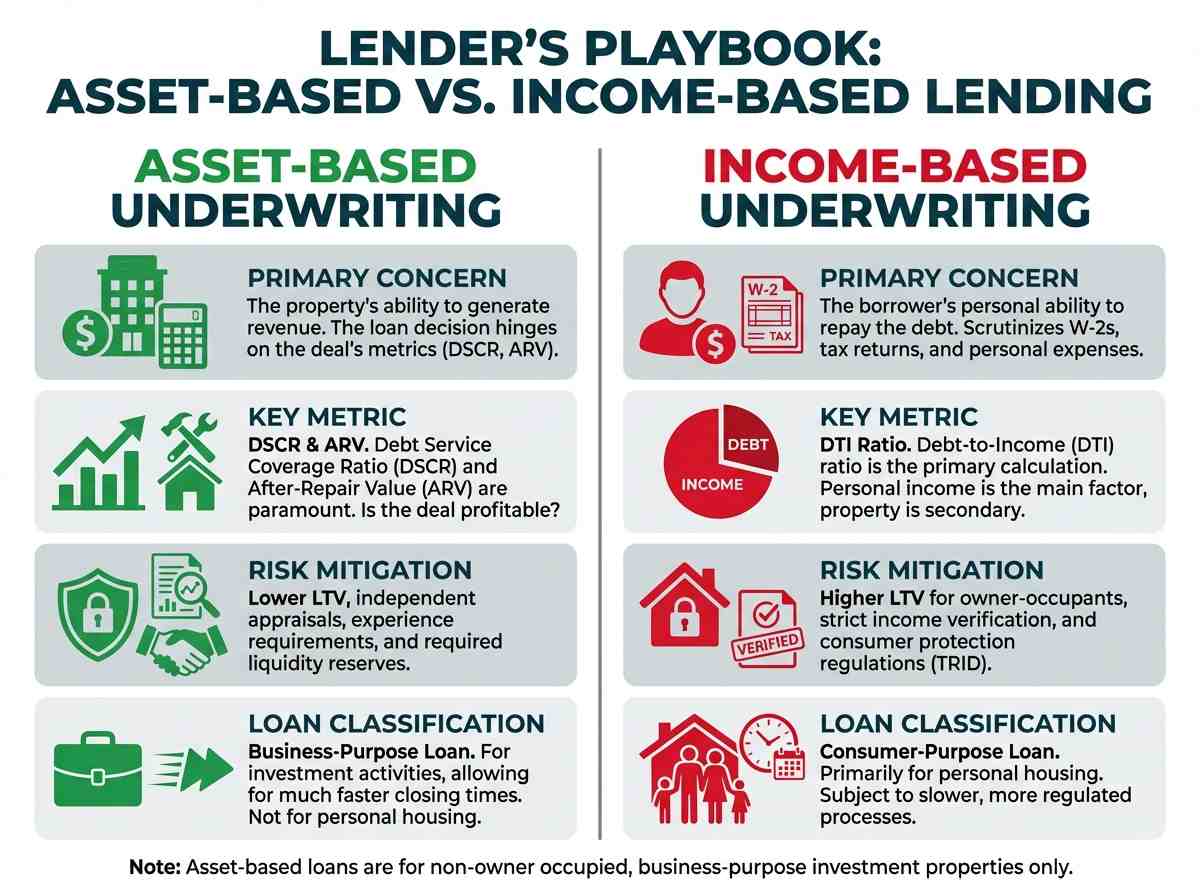

To appreciate your broker's role, you must understand the mindset of the lenders they work with. Private and hard money lenders operate in a different universe than the conventional mortgage world. Their playbook is built on asset performance, not personal income.

The Fundamental Difference: Asset-Based vs. Income-Based Underwriting

This is the single most important concept to grasp.

Income-Based Underwriting (Conventional): A bank's primary concern is your personal ability to repay the debt. They scrutinize your W-2s, tax returns, and personal expenses to calculate your Debt-to-Income (DTI) ratio. The property is secondary; your personal income is primary. This is why self-employed investors or those with "lumpy" income struggle to get conventional loans.

Asset-Based Underwriting (Private/Hard Money): An asset-based lender's primary concern is the quality of the real estate asset and its ability to generate revenue or be sold for a profit. They underwrite the deal. Your personal finances are still checked for creditworthiness and liquidity, but the loan decision hinges on the property's metrics, like the Debt Service Coverage Ratio (DSCR) or the After-Repair Value (ARV).

Your broker's job is to frame your loan request in the language of asset-based lending, focusing on the strength of the deal itself.

The Focus on Property Performance Over Personal DTI

For an asset-based lender, a low DTI is irrelevant if the property itself can't support the debt.

For DSCR Loans: The lender asks, "Does the property's rental income cover the proposed mortgage payment, taxes, insurance, and any association fees?" They use the DSCR calculation (Gross Rent / PITIA) to answer this. A ratio of 1.00x to 1.20x or higher is typically required, meaning the rent covers the debt service with a 20% buffer.

For Fix and Flip Loans: The lender asks, "Is there enough profit margin in this deal to ensure our loan gets paid off when the property is sold?" They focus on the ARV and the total cost basis (purchase + rehab). They want to see a clear path to a profitable exit.

How Lenders Mitigate Risk Without Relying on W-2s or Tax Returns

Asset-based lenders have several tools to protect their investment without digging through your tax returns:

Lower Leverage: They typically lend at a lower Loan-to-Value (LTV) than owner-occupied loans. This creates an immediate equity cushion. If the borrower defaults, the lender can foreclose and sell the property with a higher probability of recouping their capital.

Appraisals and Valuations: They rely heavily on independent, third-party appraisals to validate the property's current value and, for flips, its potential after-repair value.

Experience Requirements: They often have tiered programs where more experienced investors get access to higher leverage and better rates. A track record of success is a powerful risk mitigator.

Liquidity Reserves: They require borrowers to have cash reserves (typically 3-6 months of PITIA payments) to cover unexpected vacancies or expenses, ensuring the loan can be serviced even if the property is temporarily not performing.

The Importance of a Business-Purpose Loan Classification

All loans from private and hard money lenders are classified as "business-purpose loans." This is a critical legal and regulatory distinction. These loans are for commercial investment activities, not for personal housing.

To ensure this, you will be required to sign a Business Purpose Affidavit at closing, certifying that you will not occupy the property as your primary or secondary residence. This classification exempts the loans from certain consumer protection regulations like TRID, which allows for much faster closing times. Your broker ensures all documentation correctly reflects the business nature of the loan.

Core Loan Programs: Matching the Product to Your Strategy

An investment loan broker has a toolkit of different loan programs, each designed for a specific real-estate strategy. Choosing the right product is essential for maximizing profitability and aligning the financing with your business plan.

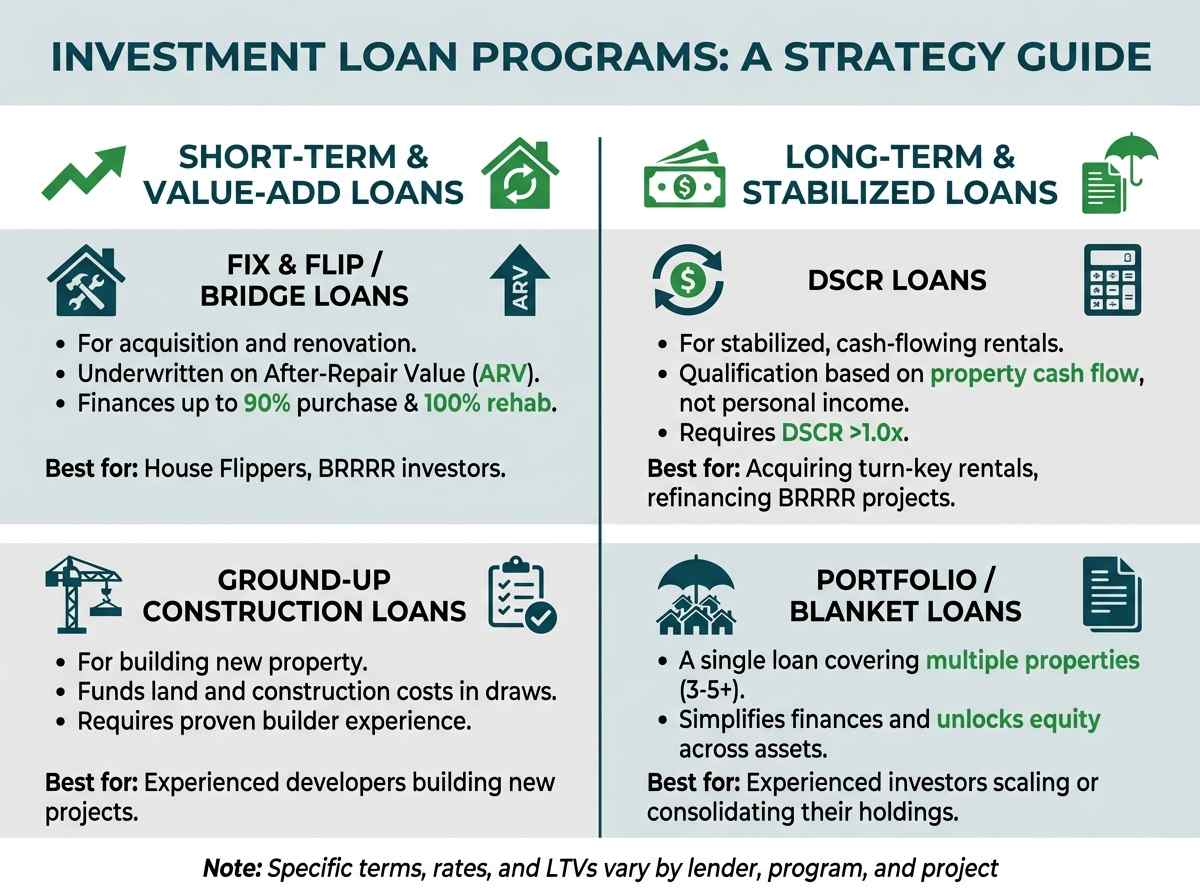

Fix and Flip / Bridge Loans for Acquisition and Renovation

These are short-term, interest-only loans (typically 12-24 months) designed for acquiring and renovating properties you intend to sell.

Key Features: They are underwritten based on the property's After-Repair Value (ARV). Lenders will often finance up to 90% of the purchase price and 100% of the renovation budget, with the total loan amount not exceeding 70-75% of the ARV.

Best For: House flippers, BRRRR investors (for the "Buy" and "Rehab" phases), and investors buying a property that needs stabilization before it can qualify for long-term financing.

Why it Works: This product provides the high leverage needed to preserve capital and funds the renovation, which traditional loans won't do. The interest-only structure keeps payments low during the rehab period when there is no rental income. Use a fix and flip calculator to model your potential profit.

DSCR Loans for Stabilized, Cash-Flowing Rental Properties

A DSCR (Debt Service Coverage Ratio) loan is the workhorse product for long-term rental investors.

Key Features: Qualification is based on property cash flow, not personal income. The lender verifies that the property's gross monthly rent is greater than the proposed monthly mortgage payment (PITIA). Most lenders require a DSCR of 1.00x to 1.20x+. These are typically 30-year fixed-rate or ARM loans.

Best For: Acquiring new turn-key rentals, refinancing a completed BRRRR project, or cashing out equity from an existing rental property.

Why it Works: DSCR loans allow investors to scale their portfolios without being limited by their personal DTI. As long as you can find properties that cash flow, you can continue to get financing. OfferMarket's DSCR loans are a prime example of this flexible financing.

Portfolio and Blanket Loans for Scaling and Consolidation

A portfolio or blanket loan is a single loan that covers multiple properties.

Key Features: Instead of having five separate loans for five properties, you have one loan and one monthly payment. Lenders typically require a minimum of 3-5 properties to qualify. The underwriting is based on the blended performance (rent, value, expenses) of the entire portfolio.

Best For: Experienced investors with a number of stabilized properties who want to simplify their finances, free up capital through a portfolio-wide cash-out refinance, or cross-collateralize properties to acquire a new one.

Why it Works: This is a powerful tool for portfolio management. It can lower your total monthly payments, reduce administrative hassle, and unlock trapped equity across multiple assets simultaneously.

Ground-Up Construction Loans for Experienced Builders

These are specialized loans for building a property from the ground up.

Key Features: These are short-term loans that fund the land acquisition and construction costs. Funds are disbursed in draws as construction milestones are completed and verified by an inspector. Underwriting is heavily focused on the builder's experience, the project's feasibility, and the "as-completed" value.

Best For: Experienced developers and builders with a proven track record of completing projects on time and on budget.

Why it Works: Provides the necessary capital in stages to match the construction timeline, minimizing interest costs. It's a highly specialized product that requires a broker with direct experience in construction finance.

Borrower Underwriting: How Lenders Evaluate You

While the property is the primary focus in asset-based lending, the borrower is still a critical piece of the puzzle. Lenders need to know they are partnering with a reliable, experienced, and financially sound operator. Your broker's job is to present you in the best possible light.

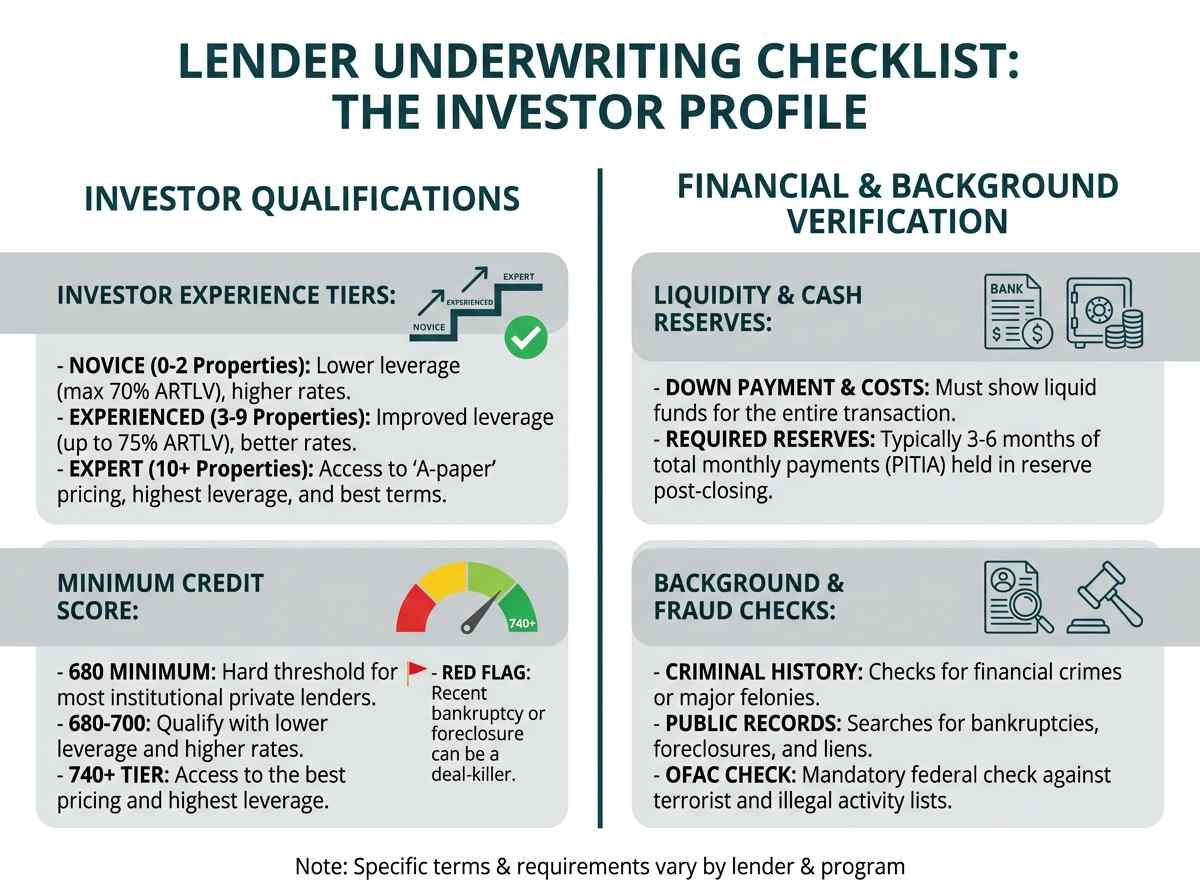

The Investor Experience Tier System from Novice to Expert

Most private lenders categorize borrowers into experience tiers, which directly impacts the loan terms they are offered. More experience equals less perceived risk, which translates to better terms.

Novice/First-Time Investor:

- Definition: 0-2 flips or rental properties owned in the last 24-36 months.

- Impact: Lenders will offer lower leverage (e.g., maximum 80% LTC on a flip, or 70% ARTLV on a rental). Rates and fees will be on the higher end of the spectrum. They may require a more detailed scope of work or a higher liquidity reserve.

Experienced Investor:

- Definition: 3-9 properties in the last 24-36 months.

- Impact: This tier unlocks better terms. Leverage may increase to 85-90% LTC / 75% ARTLV. Rates may improve by 0.25% - 0.50%. Underwriting becomes more streamlined as the investor has a proven track record.

Expert/Pro Investor:

- Definition: 10+ properties in the last 24-36 months.

- Impact: These borrowers get the "A-paper" pricing. They have access to the highest leverage, lowest rates, and most flexible terms. Lenders compete for their business, and they will be eligible for home equity loan or portfolio programs not available to less experienced investors.

Minimum Credit Score Requirements and Their Impact on Leverage

Credit score is used as a measure of financial responsibility. While asset-based lenders are more forgiving than conventional banks, a minimum score is still required.

Minimum Threshold: Most private lenders have a hard minimum FICO score of 680. Below this range, it becomes very difficult to secure financing from institutional sources, and you may be limited to more expensive hard money.

The Tiers:

- 6680-700: You can get approved, but expect lower leverage and higher rates.

- 700-720: This is the standard tier where you can access most programs and good terms.

- 740+: This is the top tier. A high credit score gives you access to the best pricing and highest leverage available. It signals to the lender that you are a low-risk borrower.

A significant credit event like a recent bankruptcy, foreclosure, or a pattern of late payments can be a deal-killer, even with a high score.

Liquidity Verification and Required Cash Reserves

Lenders need to see that you have enough "skin in the game" and the financial capacity to handle unforeseen issues. This is verified by reviewing your recent bank, brokerage, or retirement account statements.

Down Payment & Closing Costs: You must show sufficient liquid funds to cover the down payment and all closing costs (origination points, appraisal, title fees, etc.). Gift funds are typically not allowed.

Required Reserves: After paying the down payment and closing costs, most lenders require you to have an additional amount of cash in reserve. This is typically calculated as 3-6 months of the total monthly payment (PITIA) for the subject property. For a fix and flip loan, they may also want to see reserves to cover several months of interest payments. The purpose of reserves is to ensure you can service the debt if the renovation takes longer than expected or the property sits vacant for a few months.

Comprehensive Background, Fraud, and OFAC Checks

Every lender will conduct a thorough background check on all principals (anyone owning 20-25% or more of the borrowing entity).

Criminal History: Lenders are looking for financial crimes, fraud, or any major felonies. A clean record is essential.

Public Records: They will search for bankruptcies, foreclosures, judgments, and liens. While an older, discharged bankruptcy might be acceptable, a recent foreclosure is a major red flag.

OFAC Check: As required by federal law, every borrower is checked against the Office of Foreign Assets Control (OFAC) list, which contains names of individuals and entities involved in terrorism, drug trafficking, and other illegal activities.

Your broker will ask about any potential issues upfront so they can address them proactively with the lender, rather than letting them be discovered at the last minute.

The Cost-Benefit Analysis: When a Broker Makes Financial Sense

Using an investment loan broker is a strategic decision, not a requirement. The choice comes down to a simple cost-benefit analysis: Does the value the broker provides (in time, access, and better terms) exceed the cost of their fee?

Typical Broker Compensation: Origination Points and Fees

Brokers are typically compensated through origination points, which are a percentage of the final loan amount.

Standard Fee: The industry standard is 1 to 2 points, where one point equals 1% of the loan amount. For a $300,000 loan, a 1-point fee would be $3,000, and a 2-point fee would be $6,000.

How it's Paid: This fee is paid at closing. It can either be paid out-of-pocket by the borrower or, more commonly, rolled into the total loan amount.

Factors Influencing the Fee: The complexity of the deal, the size of the loan (smaller loans often have a higher point percentage), and the strength of the borrower can all influence the broker's fee. A straightforward DSCR loan for an experienced borrower might be 1 point, while a complex construction loan for a first-time developer might be 2 points or more.

Scenarios Demanding a Broker

In certain situations, the value of a broker is almost indispensable.

Complex Deals: If your deal involves non-standard elements like a seller-held second mortgage, a mixed-use property, or a portfolio of properties with different characteristics, a broker's expertise in structuring the deal is critical.

Poor Credit or Financials: If your credit is bruised (in the 620-660 range) or you have a recent financial hiccup, a broker can navigate the sub-market of lenders who specialize in "story" credits and can get a deal done that a prime lender would reject.

Scaling Quickly: If your goal is to acquire multiple properties in a short period, a broker becomes an essential part of your team. They handle the financing so you can focus on deal sourcing and project management. Trying to manage 3-4 loan applications simultaneously with different direct lenders is a recipe for burnout and missed opportunities.

Time Constraints: If you're a busy professional, the hours a broker saves you from researching lenders and managing paperwork can be worth far more than their fee.

Calculating the Value of Improved Terms vs. the Broker's Fee

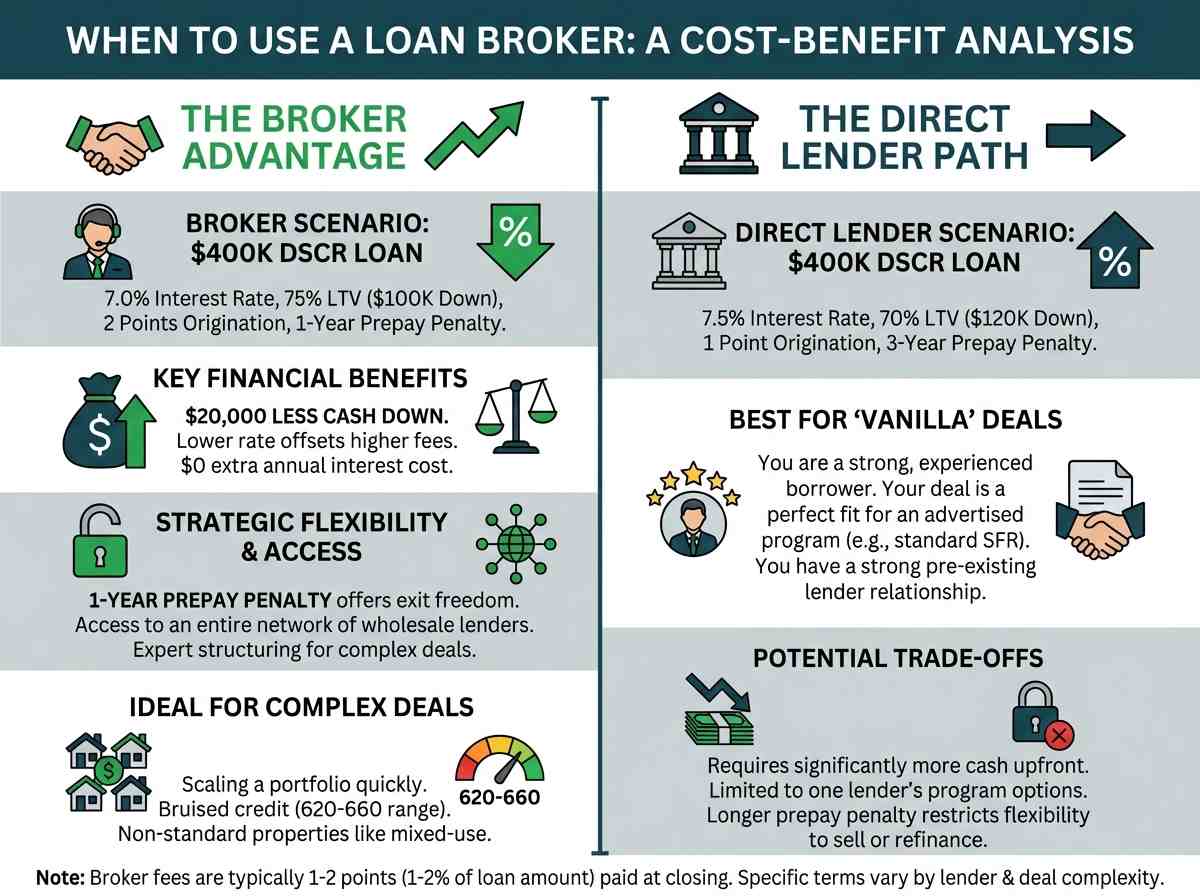

You can quantify a broker's value. Let's compare two scenarios for a $400,000 DSCR loan.

Scenario A: Going Direct

You find a direct lender offering:

- Interest Rate: 7.5%

- LTV: 70% ($280,000 Loan Amount / $120,000 Down Payment)

- Origination: 1 point to the lender ($2,800)

- Prepayment Penalty: 3 years

Scenario B: Using a Broker

Your broker, leveraging their wholesale network, secures a loan with:

- Interest Rate: 7.0%

- LTV: 75% ($300,000 Loan Amount / $100,000 Down Payment)

- Origination: 1 point to lender + 1 point to broker = 2 points total ($6,000)

- Prepayment Penalty: 1 year

The Analysis:

Upfront Cost: The broker route costs $3,200 more in origination fees at closing ($6,000 vs $2,800).

Capital Saved: The broker's loan requires a $20,000 smaller down payment. This is raw liquidity you keep in your pocket to immediately deploy into your next deal or use as required reserves.

Interest Efficiency: Even though you are borrowing $20,000 more in Scenario B, the 0.5% lower interest rate means your annual interest payments are exactly the same in both scenarios ($21,000/year). You essentially received $20,000 in extra leverage for free.

Flexibility: The shorter 1-year prepayment penalty gives you the strategic freedom to sell or refinance much sooner without facing thousands of dollars in exit fees.

Conclusion: In this common scenario, the broker's value far exceeds their cost. Paying $3,200 in extra fees preserves $20,000 in working capital and buys significant exit flexibility, which is a massive benefit for an investor focused on growth.

When to Go Direct to a Lender vs. Using a Broker

If your deal is a "vanilla" straightforward transaction, and you are a strong, experienced borrower, you may benefit from going direct.

You're a Perfect Fit: If you have 3+ flips under your belt, 680+ credit, and are buying a standard 1-4 unit SFR that fits perfectly into a lender's advertised program, you may be able to secure the best terms on your own.

You Have a Pre-existing Relationship: If you have a long and successful track record with a specific direct lender, they will likely give you their best terms without a broker's involvement.

However, for the vast majority of investors and deals, a broker provides a strategic advantage that is well worth the cost.

The Alternative: Broker Access with Direct Lender Speed

While the traditional investment property loan broker has long been the gatekeeper to creative financing, the evolution of financial technology has created a "third way." You no longer have to choose between the narrow product line of a single bank or the high-cost, multi-layered experience of a traditional broker.

Modern, tech-enabled direct lenders offer a streamlined alternative that combines the broad market access of a broker with the execution speed and cost-efficiency of a direct source.

The Drawbacks of the Traditional Broker Model: Added Fees and Potential Delays

For years, investors tolerated the broker model because it was the only way to access "off-Wall Street" capital. However, that access comes at a price—both in terms of your capital and your time.

The "Broker Load": Most brokers charge an origination fee (often 1% to 2% of the loan amount) on top of the lender’s own fees. On a $500,000 loan, that’s an extra $5,000 to $10,000 stripped from your project’s liquidity.

Communication Lag: A broker acts as a literal middleman. When an underwriter has a question about your rehab budget or your DSCR calculation, the message must travel from the lender to the broker, then to you, and back again. In a competitive market where "time is of the essence," these 24-to-48-hour delays can cost you a winning bid.

The "Middleman" Disconnect: Brokers often "shop" your deal to multiple lenders simultaneously. While this sounds beneficial, it can lead to multiple credit pulls and a fragmented experience where the person you are talking to isn't actually the person making the final credit decision.

How Tech-Enabled Direct Lenders Provide Variety and Transparency

New-age direct lenders have disrupted the status quo by bringing the "broker's network" in-house through technology. Instead of acting as a simple pass-through, these platforms use proprietary software to match your specific deal parameters against a vast array of institutional capital.

Real-Time Data Integration: Rather than waiting for a broker to call around for rates, tech-enabled platforms provide instant quotes. By entering your property’s address code and estimated value, you see live terms based on current market conditions.

Centralized Portals: All your documents—from LLC operating agreements to "as-completed" appraisals—live in a single secure environment. This transparency allows you to see exactly where your loan sits in the underwriting queue, eliminating the "black hole" of traditional broker communication.

The Financial Benefit of Eliminating the Middleman's Markup

In real estate, your profit is often made at the buy. If you can lower your cost of capital, your ROI immediately improves. By working directly with a lender that operates with broker-level variety, you recapture the middleman's markup.

| Cost Component | Traditional Broker Model | Tech-Enabled Direct Lender |

|---|---|---|

| Origination Fee | 2% - 3% (Lender + Broker) | 1% - 2% (Direct) |

| Processing Fees | Often Double-Charged | Single Flat Fee |

| Yield Spread Premium | Often Hidden in Rate | Transparent/Non-Existent |

| Total Closing Costs | Higher | Lower |

By cutting out the broker, you aren't just saving on the fee; you are often securing a lower interest rate because there is no "yield spread premium" (a kickback paid to brokers for placing you in a higher-interest loan).

Gaining Direct Access to Loan Specialists for Expert Deal Structuring

One of the primary arguments for using a broker is their expertise in "shaping" a deal. However, when you work with a specialist direct lender, you gain access to in-house loan strategists who understand the nuances of asset-based lending without the broker's conflict of interest.

Nuanced Underwriting: Direct specialists can help you navigate complex scenarios, such as moving a property from a Fix and Flip / Bridge Loan into a long-term DSCR Loan seamlessly.

Experience Tiering Optimization: A direct specialist knows exactly how to document your track record to move you from a Tier 1 (Novice) to a Tier 3 or 4 investor, unlocking higher leverage (up to 90% LTC) and lower interest reserves.

Strategic Structure: Whether you are dealing with a Portfolio (Blanket) Loan for 20 units or navigating the "Cost Basis" seasoning rules for a quick refinance, you are speaking directly to the source of the capital. This ensures that the way your deal is "pitched" to the credit committee is accurate, professional, and optimized for approval.

Take the Next Step: Get Your Personalized Loan Options

Navigating the world of investment property financing can be complex, but you don't have to do it alone. Whether you choose to work with a traditional broker or a modern direct lender, the key is to partner with experts who can help you achieve your goals.

Get an instant quote to see direct-from-lender rates and terms

The best way to see how your next deal stacks up is to get real numbers. Get an instant quote to see personalized rates and terms from our network of lenders, with no broker markup.

Use our DSCR and Fix and Flip calculators to model your next deal

Before you even make an offer, run the numbers. Use our free online tools to estimate your payments, cash flow, and potential profit.

Speak directly with a loan specialist to bypass broker fees

Ready to discuss your strategy? Skip the broker fees and speak directly with one of our loan specialists. We'll help you structure your deal for maximum cash flow and a fast, seamless closing.

Compare our transparent financing against traditional broker offers

We're confident that our combination of variety, speed, and cost-efficiency provides a superior financing experience. Get a term sheet from us and compare it to any offer you receive from a traditional broker. See for yourself how eliminating the middleman can put more money back into your pocket.

Get Your Instant Loan Quote

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →

OfferMarket Loans

Check your rate

60 seconds · no credit pull