*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

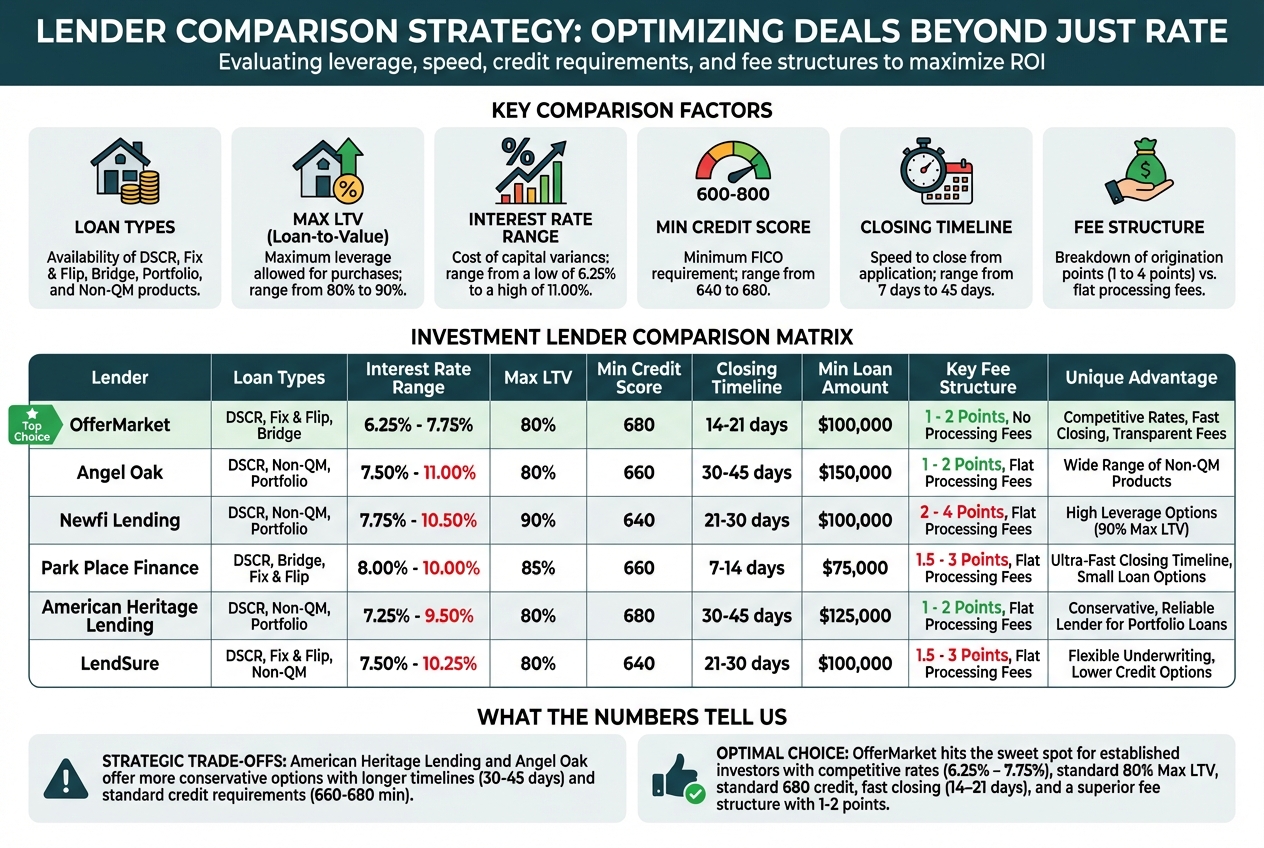

Updated Investment Property Mortgage Lenders List for 2026

Updated Investment Property Mortgage Lenders List for 2026

| Lender | Loan Types | Interest Rate Range | Max LTV | Min Credit Score | Closing Timeline | Min Loan Amount | Key Fee Structure | Unique Advantage |

|---|---|---|---|---|---|---|---|---|

| OfferMarket | DSCR, Fix & Flip | 6.25% - 7.75% | 80% | 680 | 14-21 days | $100,000 | No origination points, flat processing fee | Instant soft-pull quotes, transparent pricing, integrated property marketplace |

| Kiavi | Fix & Flip, Bridge, DSCR | 6. 75% - 9.50% | 90% (experienced) | 660 | 7-10 days | $50,000 | 2-3 points origination | Speed-focused, high-volume operator |

| Rocket Mortgage | DSCR | 6.50% - 8.25% | 80% | 700 | 30-45 days | $150,000 | 1-2 points origination | Well-known name, newer to DSCR lending |

| Visio Lending | DSCR, Portfolio | 6.50% - 8.00% | 80% | 680 | 21-30 days | $100,000 | 1.5-2.5 points origination | Strong choice for portfolio loans |

| Griffin Funding | DSCR, Conventional Investment | 6.375% - 8.00% | 85% | 680 | 21-30 days | $100,000 | 1-2 points origination | Offers both conventional and DSCR paths |

| Angel Oak | DSCR, Non-QM | 6.75% - 8.50% | 80% | 660 | 30-45 days | $75,000 | 2-3 points origination | Great for non-traditional borrowers |

| RCN Capital | Fix & Flip, Bridge, DSCR | 7.00% - 10.99% | 90% | 650 | 10-15 days | $50,000 | 2-4 points origination | Higher LTV for seasoned investors |

| Lima One | Fix & Flip, Bridge, DSCR | 6.99% - 10.50% | 90% | 660 | 10-14 days | $50,000 | 2-3.5 points origination | Solid option for rehab projects |

| LendingOne | Fix & Flip, Bridge, DSCR | 7.25% - 11.00% | 90% | 640 | 7-14 days | $75,000 | 2-4 points origination | Works with lower credit scores |

| Easy Street Capital | DSCR | 6.50% - 8.25% | 80% | 680 | 21-30 days | $100,000 | 1.5-2.5 points origination | Good rates for DSCR loans |

| Newfi Lending | DSCR, Non-QM | 6.75% - 8.50% | 85% | 680 | 25-35 days | $125,000 | 1.5-2.5 points origination | User-friendly online experience |

| Park Place Finance | DSCR, Bridge | 7.00% - 9.00% | 80% | 680 | 21-30 days | $100,000 | 2-3 points origination | Strong presence in select regions |

| Asset Based Lending (ABL) | Bridge, Hard Money | 8.00% - 12.00% | 75% | 620 | 5-10 days | $50,000 | 3-5 points origination | Lightning-fast closings, property-focused |

| Champions Funding | DSCR, Fix & Flip | 7.00% - 9.50% | 85% | 660 | 14-21 days | $75,000 | 2-3.5 points origination | Knows the Midwest market well |

| American Heritage Lending | DSCR, Portfolio | 6. 75% - 8.75% | 80% | 680 | 30-45 days | $125,000 | 1.5-2.5 points origination | Conservative underwriting, lower risk |

| CoreVest | DSCR, Portfolio | 6.50% - 8.25% | 80% | 700 | 30-45 days | $100,000 | 1-2 points origination | Large portfolio specialization |

Notes on the 2026 Update to the Investment Property Mortgage Lenders list

The investment property lending landscape in 2026 looks quite different from just a few years ago. Traditional banks have largely stepped back from this space, and specialized lenders have moved in to fill the gap. If you're a real estate investor today, here's what you're working with: DSCR (Debt Service Coverage Ratio) loans) have become the go-to financing option, rates are sitting in the 6-8% range depending on your property's performance and your borrower profile, and tech-forward lenders are giving the old guard a run for their money with faster closings and upfront pricing.

This comprehensive comparison reflects what's actually happening in the market as of early 2026, based on lender disclosures, real investor feedback, and current industry rate sheets. You'll see established players like Kiavi alongside newer names like OfferMarket that are using technology to smooth out what's traditionally been a bumpy process.

Important Context for Rate Comparisons: Investment property mortgage rates typically run 0.5% to 1% higher than what you'd pay for a primary residence, with current market conditions showing rates around 7.5% or higher for many borrowers. That said, your actual rate depends on several factors: your DSCR ratio, credit score, down payment, property type, and track record as an investor. The rates below are typical ranges—your numbers may look different based on your specific situation.

Understanding the Rate Landscape

Here's the deal: DSCR loan rates in 2026 average between 6.375% and 8.000% APR, but your actual rate depends on several key factors. Think of the "par rate" as your starting point—then adjustments kick in based on your specific situation:

- DSCR Ratio: Hit 1.25x or higher, and you'll likely see better pricing than investors hovering at 1.0x or below

- Credit Score Tiers: Scores of 720+ can shave 0.25-0.50% off your rate compared to the 680-699 range

- Loan-to-Value: Putting more skin in the game (60-70% LTV) often unlocks rate reductions

- Property Type: Single-family homes typically get the best pricing, with 2-4 units and condos costing a bit more

- Borrower Experience: Own 5+ properties? You may qualify for "pro investor" pricing tiers

- Loan Amount: Borrowing $250K+ can sometimes work in your favor with volume-based discounts

Key Observations from the 2026 Lending Landscape

The Technology Divide: Here's what really separates lenders in today's market—it's not just about rates, it's about how they work. Traditional players like Rocket Mortgage offer solid rates but still run on 30-45 day timelines with conventional processes adapted for investors. On the flip side, investor-focused platforms like OfferMarket and Kiavi have built their systems from the ground up for your needs, delivering faster quotes and significantly shorter closing windows.

The Fee Complexity Problem: Those origination point ranges in the table above? They're just the starting point. Most lenders use a "par-plus" pricing model, meaning your quoted rate ties directly to a specific point structure. Want a lower rate? You'll pay more points upfront. Prefer minimal upfront costs? Your rate increases. This makes apples-to-apples comparisons tricky—a 6.5% rate with 3 points might actually cost you more over a 3-year hold than a 7.0% rate with zero points. That's why OfferMarket's approach of ditching origination points for straightforward processing fees makes your decision so much clearer.

The Experience Premium: Here's something worth knowing: nearly every lender on this list rewards experience with better terms. A first-time investor might get 75% LTV at 7.5%, while a seasoned pro with 10+ properties could snag 80% LTV at 6.75% from the exact same lender. This "experience premium" can put $10,000+ back in your pocket annually on a $500,000 loan—making it one of the biggest factors in your lending equation.

The Speed-vs-Rate Tradeoff: You'll notice a clear pattern: faster closings mean higher rates. Hard money lenders like Asset Based Lending can close in 5-10 days, but you're looking at 8-12% rates plus 3-5 points. DSCR specialists like CoreVest offer friendlier rates (6.5-8.25%) but need 30-45 days. For most investors, the sweet spot is that 14-21 day window—lenders like OfferMarket, Champions Funding, and Visio Lending give you solid pricing without the long wait of traditional financing.

The Conventional Investment Mortgage Gap: You might notice something missing: conventional investment property mortgages (Fannie Mae/Freddie Mac products). Sure, these loans offer the lowest rates (typically 6.0-7.0% in 2026), but they come with strings attached—full income documentation, debt-to-income analysis, and a hard cap at 10 financed properties. That's exactly why most lenders here focus on DSCR and business-purpose loans instead. The reality? Serious portfolio investors outgrow conventional financing pretty quickly.

How to Research & Evaluate Your Lender Shortlist

Once you've identified potential investment property mortgage lenders, the real work begins: thorough due diligence that separates marketing promises from how lenders actually perform. Most investors skip this critical vetting phase and pay for it—literally—with surprise fees, delayed closings, and unfavorable terms discovered too late in the process.

This section gives you a clear, step-by-step approach for evaluating lenders before you commit time, documentation, or hard credit pulls to any single option.

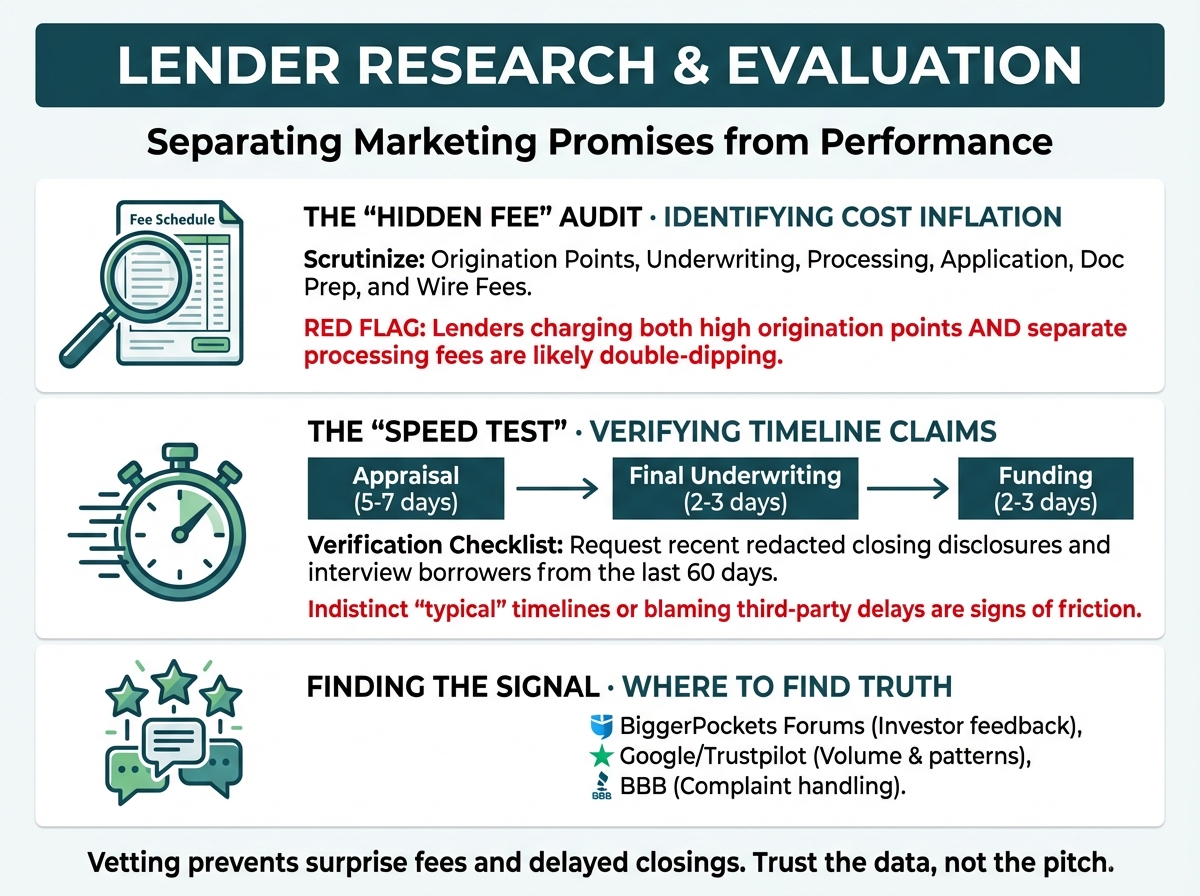

The "Hidden Fee" Audit: Identifying Cost Inflation

The advertised rate is just one piece of your true borrowing cost. Lenders often tuck profit margins into fees that aren't immediately visible in rate quotes, creating significant variance in your actual cash-to-close requirements.

Origination Points and Fees

Origination fees are what the lender charges for processing and underwriting your loan application. According to industry data, mortgage origination fees typically range from 0.5% to 1% of your total loan amount, though investment property loans often come with higher fees than owner-occupied mortgages.

On a $400,000 investment property loan, the difference between a 0.5% and 1.5% origination fee represents $4,000 in additional upfront costs—money that could otherwise fund repairs, reserves, or your next down payment.

Here's an important distinction: Origination points and discount points are two different things. Origination points compensate the lender for loan processing and don't reduce your interest rate. Discount points, on the other hand, let you buy down your rate by paying upfront—typically, each point costs 1% of your loan amount and reduces your rate by approximately 0.25%.

When comparing lender quotes, ask for explicit breakdowns that separate:

- Origination fees/points: Pure lender compensation

- Underwriting fees: Separate charges for loan evaluation (often redundant with origination fees)

- Processing fees: Administrative costs that should be included in origination

- Application fees: Upfront charges that may or may not be credited toward closing

- Document preparation fees: Charges for generating loan paperwork

- Wire transfer fees: Costs for funding disbursement

Red flag: Any lender charging both substantial origination fees AND separate underwriting or processing fees is likely double-dipping. These functions overlap significantly, and transparent lenders consolidate them into a single origination charge.

The audit process:

- Request itemized fee schedules from each lender on your shortlist

- Calculate total lender fees as a percentage of loan amount

- Flag any fees above 1.5% of loan amount for a closer look

- Question any fee that seems duplicative (e.g., both "underwriting" and "processing")

- Ask whether quoted fees are negotiable or set in stone

Here's the good news: investment property lenders in competitive markets often have wiggle room on origination fees, especially for experienced investors with solid credit or those bringing multiple deals to the table. Don't assume published fee schedules are take-it-or-leave-it.

Researching Lender Reviews: Finding the Signal in the Noise

Online reviews give you a window into what it's actually like to work with specific lenders—when you know how to read them the right way.

Where to do your homework:

- Google Reviews: Lots of volume, mixed reliability, but great for spotting patterns

- Better Business Bureau (BBB): See how they handle complaints and their accreditation status

- Trustpilot: Verified reviews with detailed stories from real borrowers

- BiggerPockets Forums: Fellow investors sharing their experiences with investment property lenders

- Facebook Groups: Real-time feedback from investors who are actively in the game

What to zero in on:

Skip the star ratings (those can be gamed). Instead, dig into the actual review content and look for themes that keep popping up:

Green flags:

- People mentioning specific loan officers or processors by name with praise

- Detailed accounts of smooth closings with clear timelines

- Stories of lenders stepping up to solve problems or handle unique situations

- Shout-outs for upfront, transparent fee disclosure

- Comments about competitive rates compared to other quotes

Red flags:

- Multiple complaints about surprise fees or last-minute cost increases

- Repeated mentions of missed closing deadlines or funding delays

- Frustration with poor communication or loan officers who ghost

- Rate locks expiring because the lender dropped the ball

- Accusations of bait-and-switch tactics or pushy upselling

Pro tip: How a lender responds to negative reviews tells you more than the complaints themselves. Lenders that engage constructively with criticism, offer specific remediation, and demonstrate accountability typically maintain better operational standards than those that ignore feedback or respond defensively.

Sample size matters: A lender with 15 five-star reviews may simply have a small customer base or actively curated feedback. A lender with 500 reviews averaging 4.2 stars—including thoughtful responses to criticism—shows you more reliable quality at scale.

Recency bias: Prioritize reviews from the past 6-12 months. Lender operations, personnel, and service quality can shift significantly over time, particularly after acquisitions, leadership changes, or rapid scaling.

The 2026 "Speed Test": Verifying Closing Timeline Claims

In competitive investment property markets, closing speed directly impacts deal success. Sellers often accept slightly lower offers from buyers with faster, more certain financing—making a lender's actual closing timeline a real competitive edge for you.

Most investment property lenders advertise 14-21 day closing timelines. Few consistently deliver.

Why closing speed matters:

- Off-market deals: Motivated sellers and wholesalers often require 14-day closings

- Competitive offers: Speed can offset 3-5% lower purchase prices in multiple-bid scenarios

- Carrying costs: Every extra week in closing adds holding costs for bridge financing or hard money

- Rate lock expiration: Extended closings risk rate lock expiration and repricing

Here's how to verify actual performance:

Ask for average closing times by loan type: DSCR loans, fix-and-flip loans, and cash-out refinances have different processing timelines. Request specific data for your intended loan product.

Request recent closing disclosure timestamps: Ask to see redacted closing disclosures showing application date and funding date for 5-10 recent similar transactions.

Interview recent borrowers: Request references from investors who closed similar loans in the past 60 days. Ask specifically: "How many days from application to funding?" and "Were there any delays, and if so, what caused them?"

Pinpoint where things slow down: Get lenders to walk you through their process step by step, along with realistic timelines:

- Initial underwriting review: 2-3 business days

- Appraisal ordering and completion: 5-7 business days

- Final underwriting approval: 2-3 business days

- Clear-to-close to funding: 2-3 business days

Put their responsiveness to the test: Reach out to several lenders at once and see who gets back to you first. Here's a reliable rule of thumb: if a lender takes more than 48 hours to respond to your initial inquiry, they're unlikely to close your loan in 14 days.

Watch out for these red flags:

- Indistinct answers about "typical" timelines without hard numbers to back them up

- Pointing fingers at third parties (appraisers, title companies) when delays happen

- Can't share recent examples of closings within your target timeline

- Speed promises with fine print ("We can close in 14 days if everything goes perfectly")

The OfferMarket difference: Our digital-first platform cuts through traditional slowdowns with automated underwriting, instant appraisal ordering, and seamless closing coordination. The result? Our median DSCR loan closes in 16 days from application to funding—and you can see the proof yourself inside your Loan File. Just open the Closing tab to access your transparent Closing Calendar, where key milestones—like loan application, credit report, appraisal, underwriting, insurance, title work, and final approval—are mapped out with target dates. As each milestone is completed, you can track whether you're on pace or ahead of schedule with the “Ahead +X” indicator, which shows how many days faster you’re progressing. The quicker each milestone is completed, the more that number increases—automatically pulling your projected closing date closer.

Experience Tiers: How Your Track Record Affects Your Loan Terms

Here's something many investors don't realize: lenders sort borrowers into experience tiers. Your track record directly impacts your pricing, LTV ratios, and which programs you can access.

Here's how the tiers typically break down:

Tier 1: First-Time Investment Property Buyers

- Who qualifies: No previous investment property ownership or completed flips but must currently own a primary residence

- Typical LTV: 75% maximum

- Rate premium: +0.25% to +0.50% above experienced investor rates

- Reserve requirements: 6-12 months PITIA

- Program restrictions: Limited access to cash-out refinance; may require prior homeownership

Tier 2: Intermediate Investors

- Who qualifies: 1-3 current investment properties or completed flips

- Typical LTV: 80% maximum

- Rate premium: +0. 125% to +0.25% above top-tier rates

- Reserve requirements: 6 months PITIA

- Program access: Full DSCR and fix-and-flip eligibility

Tier 3: Experienced/Portfolio Investors

- Definition: 4+ current investment properties or 5+ completed flips

- Typical LTV: 80-85% (some lenders offer 90% LTV for strong profiles)

- Rate premium: Best available rates

- Reserve requirements: 3-6 months PITIA

- Program access: Full program suite including portfolio loans, blanket financing, and expedited underwriting

How to make tier pricing work for you:

Keep your records organized: Good documentation is your best friend when it comes to proving your experience. Hold onto:

- Lease agreements that demonstrate your rental income

- Property management statements

- Settlement statements (HUD-1 or closing disclosures) from completed flips

Don't undersell your experience: Have you managed rentals or completed flips through a partnership where your name wasn't on the title? Bring documentation of your role—many lenders will count this toward your experience level.

Compare lenders: Tier definitions aren't universal. One lender might call you a "first-time investor" while another gives you intermediate pricing based on that single rental you've owned. It pays to shop around.

Ask the right question: "Based on my profile, what experience tier do I fall into, and what would it take to qualify for your next-best tier?" This simple question can save you money and set clear goals.

Time it right: If you're on the cusp of a better tier—say, you're about to close on property number four—consider waiting to refinance your existing properties until you cross that threshold.

A word of caution: Lenders verify your investment history through tax returns (Schedule E), title searches, and credit reports showing your mortgage tradelines. Overstating your experience will come to light during underwriting and could lead to a denied application or adjusted pricing. Honesty is always the best policy here.

Red Flags to Watch For: Disqualifying Lender Behaviors

Some lender behaviors should knock them off your list immediately—no matter how attractive their rates or terms might look on paper.

Inconsistent communication:

- Different loan officers giving you conflicting information about programs, rates, or requirements

- Can't reach your assigned loan officer within 24 business hours

- Getting passed around between team members who don't know your situation

- Vague or dodgy answers when you ask specific questions about fees or timelines

Surprise fees at closing:

- New fees popping up on your closing disclosure that weren't on the initial loan estimate

- Big jumps in previously quoted fees with no clear explanation

- "Lender credits" that mysteriously vanish between loan estimate and closing disclosure

- Pressure to close quickly without giving you time to review the final closing disclosure

Unclear loan terms:

- Won't give you written rate locks or fee commitments

- Indistinct prepayment penalty structures

- Grey reserve requirements or post-closing obligations

- Vague explanations of required insurance or entity structure

Pressure tactics:

- Pushing hard for you to submit an application before you're ready

- Claiming rates are "only available today" or using similar urgency tricks

- Discouraging you from getting quotes from other lenders

- Asking for large upfront deposits before your loan is approved

Operational disorganization:

- Asking for the same documents you've already sent

- Missing deadlines for appraisal ordering or underwriting milestones

- Can't give you clear next steps or timeline updates

- Last-minute document requests for things they should have caught earlier

Trust your gut: If a lender's behavior during the quote and application phase makes you uneasy, expect those problems to get worse at closing. You don't want to discover you're working with an unreliable partner when you're under pressure with a tight timeline and big money on the line.

The comparison framework:

Build a simple spreadsheet to track each lender across these key areas:

| Lender | Total Fees (%) | Review Rating | Avg Close Time | Experience Tier | Red Flags | Overall Score |

|---|---|---|---|---|---|---|

| Lender A | 1. 2% | 4.3/5 (250) | 18 days | Tier 2 | None | 8.5/10 |

| Lender B | 2.1% | 4.1/5 (80) | 21 days | Tier 1 | Vague fees | 6.0/10 |

This side-by-side view helps you avoid a classic trap: picking a lender just because they quoted the lowest rate. The full picture—operational quality, transparency, and total cost—matters just as much.

Up next, we'll walk through exactly how to "interview" your top lender picks. You'll learn the right questions to ask, what documents to request, and negotiation moves that set savvy investors apart from those who simply accept the first offer on the table.

The Engagement Strategy: How to "Interview" a Lender

You've got your shortlist of 3-5 investment property mortgage lenders. Now comes the important part: reaching out to each one and gathering the details you need for a true apples-to-apples comparison. This isn't about sitting back and taking whatever terms come your way—it's about running a smart, professional evaluation of each lender's strengths, responsiveness, and real loan costs. Not every lender on your list will be the right fit, and your goal is to find the one that matches your investment strategy, timeline, and financial situation.

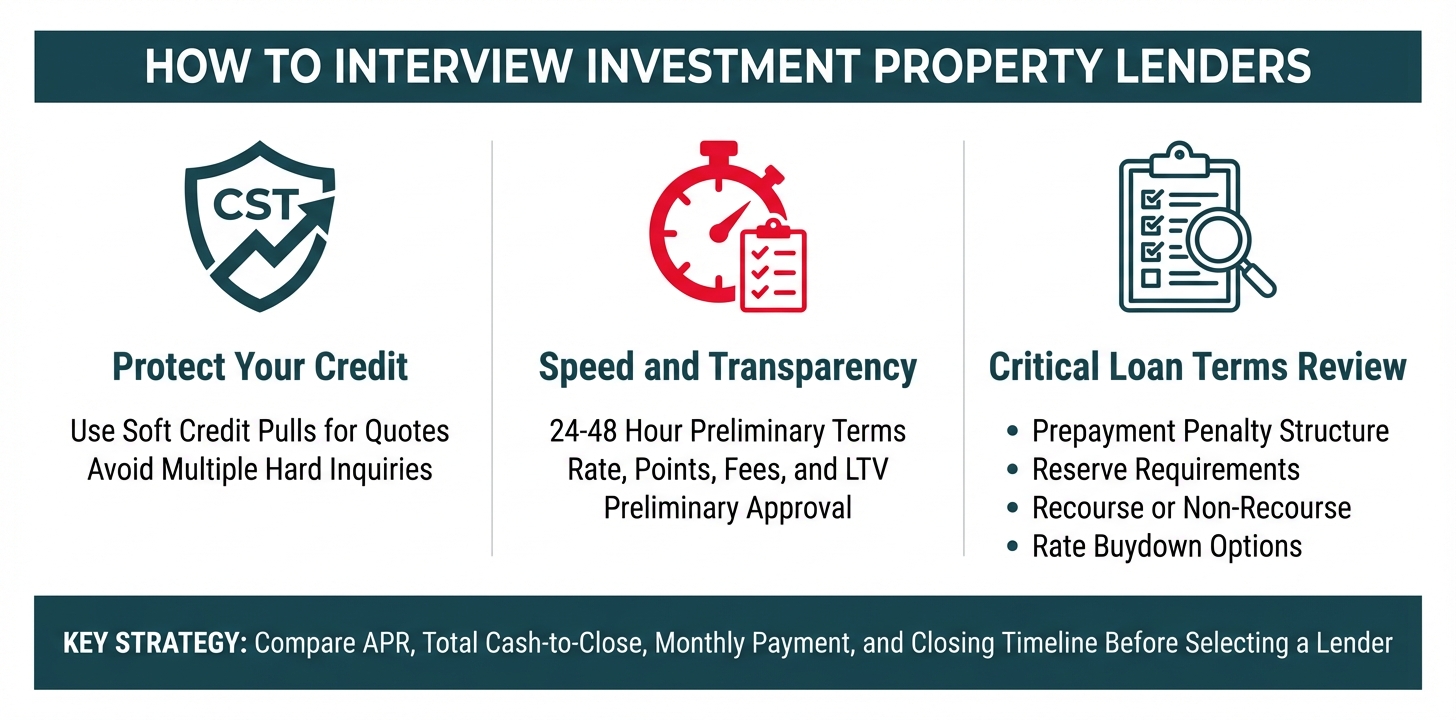

Avoiding Unnecessary Hard Credit Pulls: Protecting Your Credit Score While You Shop

Here's something that frustrates a lot of investors: hard credit inquiries. Each hard pull can knock your credit score down by 2-5 points, and a string of inquiries in a short window might make you look risky to future lenders. Yes, mortgage inquiries made within a 14-45 day period usually count as just one inquiry for scoring purposes—but not every lender plays by those rules, and the impact can still hurt if you're juggling multiple deals at once.

Here's the smart move: Look for lenders who offer soft credit pulls for initial quotes. A soft pull gives the lender enough info to provide accurate preliminary terms—rate, LTV, fees—without dinging your credit score. OfferMarket, for example, uses soft pulls to deliver instant quotes, allowing you to shop confidently without credit score erosion. Other lenders on this list may require hard pulls upfront, which should immediately raise a red flag if you're still in the research phase.

What to ask: "Do you use a soft credit pull for preliminary quotes, or will this be a hard inquiry?" If they insist on a hard pull before providing detailed terms, move them down your list. You should only authorize hard pulls once you've selected your final lender and are ready to move forward with a formal application.

Pro tip: If you're shopping multiple properties or planning to close several deals in 2026, protect your credit score by batching your lender research into concentrated windows. Complete all soft-pull quotes within 2-3 weeks, then make your decision and proceed with a single hard pull for the chosen lender.

Quoting Speed and Preliminary Loan Terms: The 24-48 Hour Test

Here's the reality: speed wins in real estate investing. That perfect deal you found today? Another investor might snag it tomorrow. Your lender's ability to deliver detailed preliminary terms quickly—ideally within 24-48 hours—directly affects whether you land the property or lose it. Slow lenders cost you money.

When you reach out to a lender, here's what you should receive within 24-48 hours:

- Interest rate: The actual rate you qualify for based on your credit profile, experience, and the property's DSCR.

- Points: Origination points and any discount points required to achieve the quoted rate.

- Fees: A clear breakdown of all lender fees, including underwriting, processing, and any third-party costs.

- LTV: The maximum loan-to-value ratio you qualify for, which determines your down payment requirement.

- Preliminary approval: A soft commitment indicating you meet basic eligibility criteria.

Lenders who take 5-7 days to provide this information—or worse, who give you vague ranges instead of specific numbers—are showing you exactly how they'll operate throughout your deal. This inefficiency will snowball as your loan moves forward, potentially costing you the deal or pushing back your closing date.

What to ask: "How quickly can you provide preliminary loan terms, including rate, points, fees, and LTV?" If the answer is anything longer than 48 hours, or if they give you a wishy-washy "it depends," take that as a red flag. The best lenders have dialed-in processes that deliver fast, accurate quotes because they've put in the work on technology and underwriting efficiency.

Critical Loan Term Identification: The Details That Determine Profitability

Once you have preliminary terms from each lender, it's time to dig into the fine print. This is where newer investors often stumble—they zero in on the interest rate and overlook the loan terms that can make or break their cash flow, exit strategy, and total cost of capital.

Prepayment penalties: Most investment property loans come with prepayment penalties ranging from 6-12 months, though some stretch to 24-36 months. These penalties—typically 1-5% of the loan balance—help the lender recoup lost interest income if you refinance or sell early. If you're running a BRRRR strategy or planning to sell within 12 months, a lengthy prepayment penalty can eat into your returns. Always ask: "What's the prepayment penalty structure, and can it be negotiated or bought out?"

Reserve requirements: Lenders usually want to see 3-6 months of PITIA (principal, interest, taxes, insurance, association dues) payments sitting in liquid reserves after closing. For a $300,000 loan with a $2,500 monthly payment, that means $7,500-$15,000 needs to stay in your bank account post-closing. When you're closing on multiple properties, reserve requirements can lock up serious capital fast. Ask: "What are your reserve requirements, and do they scale with portfolio size?"

Rate buydown options: Some lenders let you "buy down" your interest rate by paying additional points upfront. For example, paying 1 point (1% of the loan amount) might reduce your rate by 0.25%. Whether this makes sense depends on how long you plan to hold the property and your overall cash flow strategy. If you're in it for the long haul, buydowns can boost your ROI; if you're flipping or refinancing soon, you're just throwing money away. The question to ask: "What are my rate buydown options, and what's the break-even point?"

Recourse vs. non-recourse terms: Most investment property loans are recourse loans—meaning if the property forecloses and the sale doesn't cover what you owe, the lender can come after your personal assets. Some lenders offer non-recourse loans, which limit their recovery to just the property, but expect higher rates or tighter terms in exchange. If protecting your assets matters to you, ask: "Is this a recourse or non-recourse loan, and what are the terms for each option?"

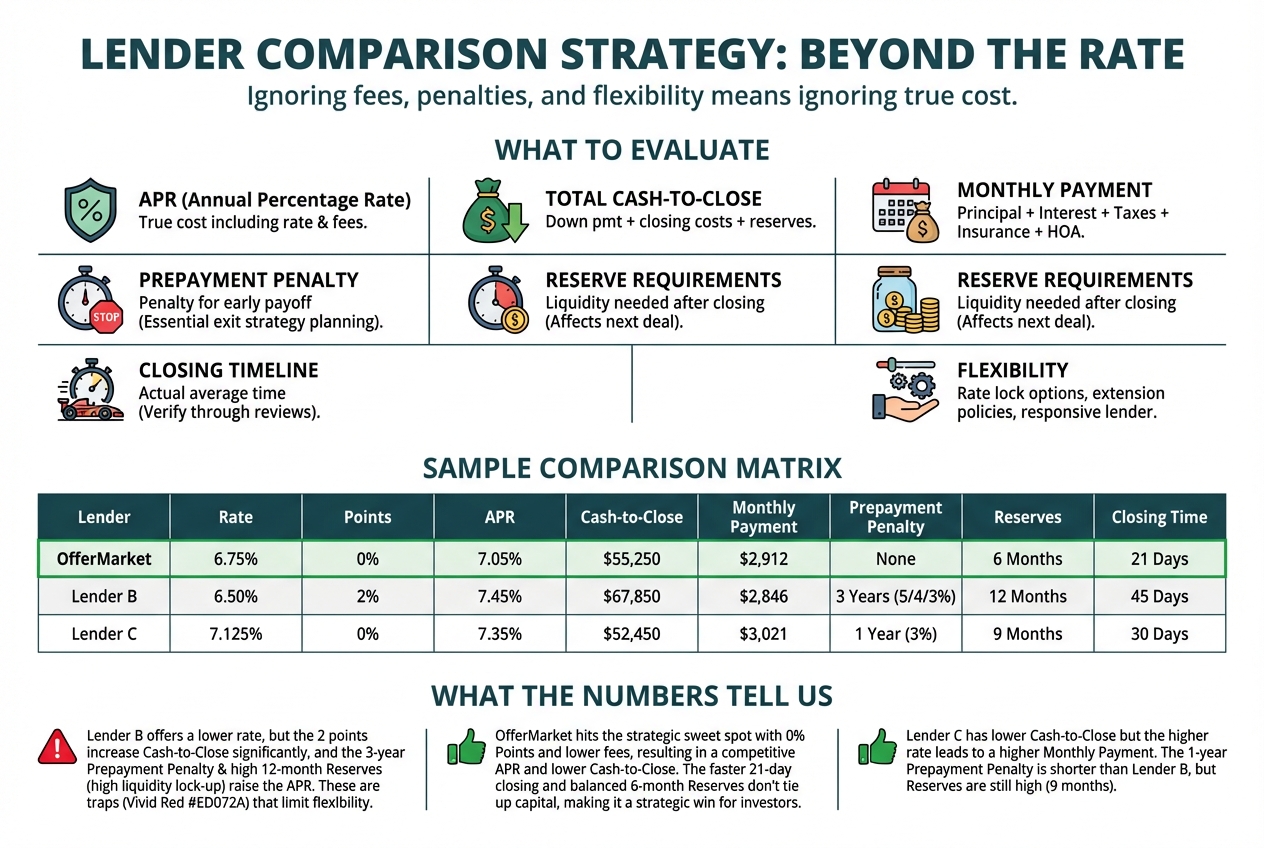

Comparing Loan Terms Between Lenders: Building Your Decision Matrix

Once you've gathered detailed terms from 3-5 lenders, you need a clear system to compare them. Looking at interest rate alone won't cut it—that ignores fees, penalties, and flexibility. Instead, build a standardized comparison spreadsheet that looks at:

- APR (Annual Percentage Rate): This rolls your interest rate and all fees into one percentage. It gives you a much clearer picture of true cost than rate alone.

- Total cash-to-close: Down payment + closing costs + reserves. This is the real number you need to bring to closing.

- Monthly payment: Principal, interest, taxes, insurance, and any HOA dues. This is what determines your cash flow.

- Prepayment penalty: How long it lasts and what percentage you'll pay. Essential for planning your exit strategy.

- Reserve requirements: What you need to keep in the bank after closing. This affects how much liquidity you have for your next deal.

- Closing timeline: The actual average closing time—not the marketing pitch. Verify through reviews or by asking directly.

- Flexibility: Rate lock options, extension policies, and how responsive the lender is throughout the process.

Sample comparison matrix:

| Lender | Rate | Points | APR | Cash-to-Close | Monthly Payment | Prepayment Penalty | Reserves | Closing Time |

|---|---|---|---|---|---|---|---|---|

| OfferMarket | 7. 25% | 0 | 7.35% | $72,000 | $2,450 | 6 months | 3 months | 14 days |

| Lender B | 7.00% | 2 | 7.45% | $78,000 | $2,380 | 12 months | 6 months | 21 days |

| Lender C | 7.50% | 1 | 7.65% | $75,000 | $2,520 | 6 months | 3 months | 18 days |

Here's what the numbers tell us: Lender B looks attractive with that 7.00% rate, but dig deeper. Those 2 points and higher reserve requirements push their APR and cash-to-close to the top of the pack. Planning to refinance within a year? That prepayment penalty becomes a real problem. OfferMarket hits the sweet spot—lower fees, faster closing, and reserve requirements that won't tie up your capital. That's a win for investors juggling multiple properties.

Questions to Ask Every Lender: Your Due Diligence Checklist

Glossy brochures and slick websites won't tell you the whole story. Here's what to ask every loan officer before you commit:

"What's your actual average closing time for investment properties in the past 90 days?" Anyone can promise 14-day closings. What matters is real performance. Get the numbers, not the sales pitch.

"What fees are refundable if I don't close?" Upfront application or underwriting fees can disappear if your deal falls apart or the appraisal disappoints. Refundable fees protect your wallet.

"How do you handle appraisal gaps?" When a property appraises below purchase price, you need to know your options. Will they adjust the loan amount, or is there room to negotiate? This detail can save your deal.

"What's your policy on rate locks and extensions?" Delays happen—title snags, seller hiccups. Find out if extending your rate lock costs extra. Some lenders charge 0.25% per week, and that adds up fast.

"Do you have experience with [your specific strategy]?" Doing BRRRR? Ask about their cash-out refi process after rehab. Eyeing a duplex or fourplex? Make sure they know small multifamily inside and out. The right experience means fewer headaches.

"What's your communication process during underwriting? " Will you have a dedicated loan officer, or will you be passed between team members? How quickly do they respond to emails and calls? Poor communication is a top complaint in lender reviews.

The lenders who give you straight, confident answers to these questions have built systems that work for investors like you. The ones who hedge, sidestep, or stay vague? That's a red flag for operational hiccups that'll pop up during your loan process—usually when you can least afford delays.

Bottom line: Choose your lender like you'd choose a business partner, not just a service provider. Your lender choice directly shapes your closing timeline, cash flow, and how fast you can grow your portfolio in 2026. Put in the work now to interview thoroughly, and you'll save yourself headaches and money later.

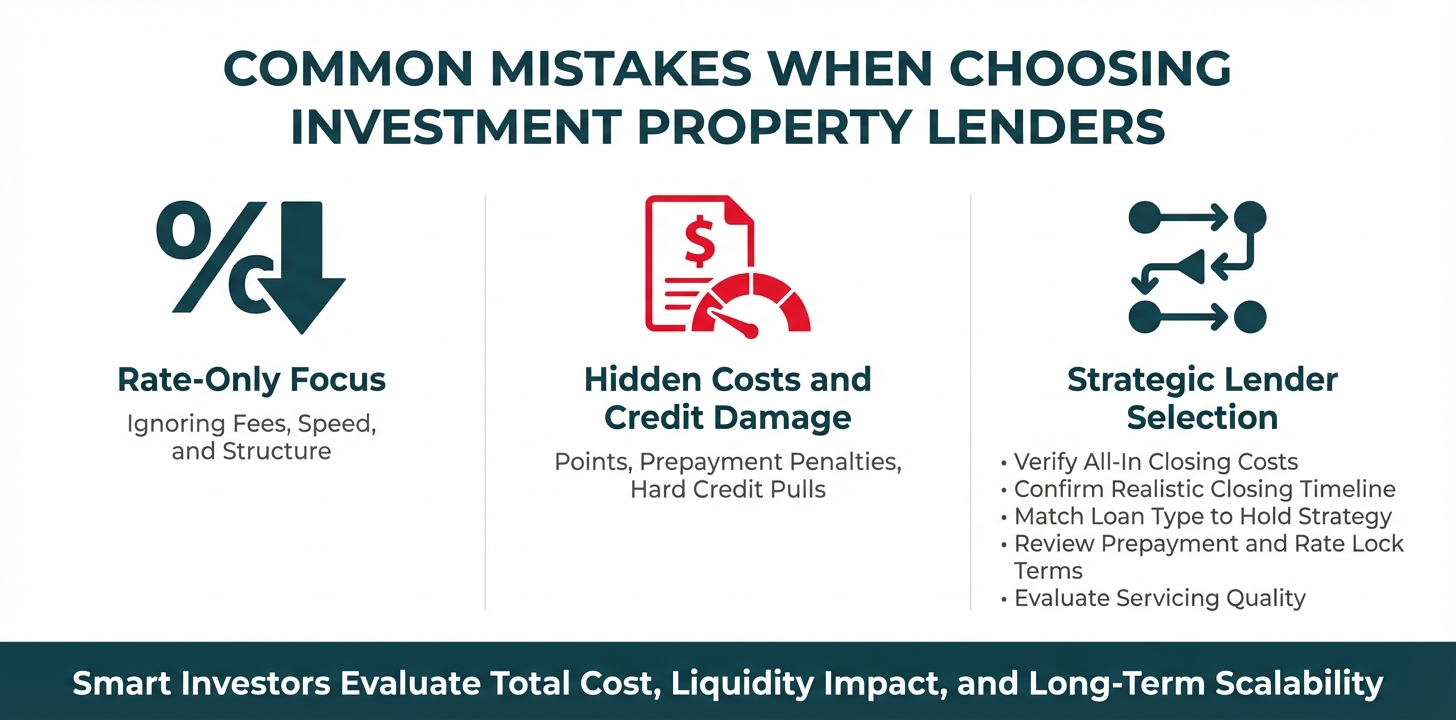

Common Mistakes Investors Make When Choosing Investment Property Mortgage Lenders

Selecting the right investment property mortgage lender involves more than comparing interest rates on a spreadsheet. Even experienced investors fall into predictable traps that cost thousands of dollars, damage credit scores, or worse—cause them to lose deals entirely. Let's walk through these common mistakes so you can avoid them and keep more money in your pocket.

Mistake #1: Shopping Based Solely on Rate Without Considering Total Cost and Closing Speed

The advertised rate is just one piece of the puzzle. A lender offering 7.25% might actually be more expensive than one quoting 7.75% once you factor in origination points, underwriting fees, processing fees, and other closing costs. Here's a real example: a loan with a 1.5% lower rate but 3 points in origination fees could cost you an additional $6,000 on a $200,000 loan—wiping out two years of interest savings.

Beyond cost, closing speed directly impacts deal viability. In competitive markets, the difference between a 14-day close and a 45-day close can mean the difference between winning and losing a property. Sellers increasingly favor cash-equivalent speed, and lenders who can't deliver on promised timelines leave you exposed to contract penalties or lost earnest money deposits.

When evaluating lenders, calculate the true all-in cost by adding origination points, underwriting fees, and any other lender fees to determine your actual cost to close. Then verify their average closing timeline with recent borrowers, not just their marketing materials.

Mistake #2: Triggering Multiple Hard Credit Pulls That Damage Credit Scores

Here's something that catches many investors off guard: each lender application can trigger a hard credit inquiry, and multiple hard pulls can drop your credit score by 10-20 points. While credit bureaus typically allow a 14-45 day shopping window for mortgage inquiries to count as a single pull, not all investment property lenders play by these rules—particularly private and hard money lenders who may pull credit multiple times throughout the process.

Let's put this in perspective. A 15-point credit score drop might push you from a 700 to a 685, potentially moving you into a higher-risk tier that increases your rate by 0.25-0.50% or reduces your maximum LTV from 80% to 75%. On a $300,000 loan, this could cost you an additional $750-$1,500 annually in interest and require $15,000 more in down payment.

Here's how to protect your credit: ask each lender upfront whether they can provide preliminary quotes using a soft pull or by reviewing your existing credit report. Only authorize hard pulls for lenders you're seriously considering after reviewing their preliminary terms. Compress your shopping window into the shortest timeframe possible to maximize the credit bureau's rate-shopping grace period.

Mistake #3: Underestimating Reserve Requirements and Running Out of Liquidity Post-Closing

Most investment property lenders require borrowers to maintain 3-6 months of PITIA (Principal, Interest, Taxes, Insurance, and Association fees) in liquid reserves after closing. On a property with $2,500 monthly PITIA, that's $7,500-$15,000 that must remain in your accounts post-closing—separate from your down payment and closing costs.

Here's where many investors trip up: they crunch the numbers for down payment and closing costs but completely overlook these reserve requirements. The result? They're cash-strapped the moment the ink dries. That's a risky spot to be in when surprise repairs pop up, tenants move out, or that next great deal lands in your lap.

Common pitfalls include failing to account for vacancy periods, maintenance costs, and market fluctuations when calculating your post-closing liquidity needs. Think of the reserve requirement as your safety net—it's there to help you handle the bumps that come with owning investment property.

Here's a simple formula to keep you on solid ground: Down Payment + Closing Costs + Reserve Requirement + Personal Emergency Fund = Your Total Cash Needed.

If that number eats up more than 90% of your available cash, pump the brakes. Look for properties with lower entry costs or take time to build up your reserves first.

Mistake #4: Choosing the Wrong Loan Type for Your Strategy

Not all investment property loans are created equal—and picking the wrong one can seriously derail your plans. The classic blunder? Grabbing a long-term DSCR loan for a quick flip, or using short-term bridge financing when you're planning to hold a rental for years.

Here's the deal: DSCR loans work best for rental properties you're keeping long-term. They come with 30-year terms, competitive rates, and prepayment penalties that sting if you pay off early. Planning to flip in 6-12 months? A DSCR loan means you're eating origination costs (1-3 points), possibly triggering prepayment penalties (1-5% of your loan balance), and racking up closing costs you didn't need to pay.

Conversely, fix-and-flip loans or bridge loans come with higher rates (9-12%+), interest-only payments, and shorter terms (12-24 months). If you use these for a rental property you plan to hold long-term, you'll be staring down a refinance in 12-18 months—meaning you'll pay closing costs twice and leave yourself exposed to rate risk if the market moves against you.

Here's the simple rule: match your loan product to your hold period. Fix-and-flip loans work best for properties you'll sell within 12 months. Bridge loans make sense for properties needing renovation before you refinance into permanent financing. And DSCR or conventional loans are your go-to for long-term buy-and-hold rentals. Your financing should support your strategy, not fight against it.

Mistake #5: Ignoring Prepayment Penalties When Planning BRRRR Strategy

The BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat) has taken the investing world by storm, but here's what catches many investors off guard: prepayment penalties. These fees can run anywhere from 1-5% of your loan balance and often stick around for the first 1-5 years of your loan.

Here's what a typical prepayment penalty structure looks like: 5% in year one, 4% in year two, 3% in year three, 2% in year four, and 1% in year five. Now imagine you're planning to refinance after stabilizing a property in 12 months, but your loan carries that 5% prepayment penalty. On a $200,000 loan, you're handing over $10,000 just to exit the financing—and that could wipe out all the profit you projected from the refinance.

The good news? You have options. Some lenders let you buy out the prepayment penalty at closing (usually 0.25-0.50% of the loan amount) or offer step-down penalties that decrease faster. Others skip prepayment penalties altogether but charge slightly higher rates. For BRRRR investors, paying that extra 0.25% in rate to dodge prepayment penalties often pencils out better given your planned short hold period.

Before you commit to a lender for your BRRRR deal, get clear answers on these questions: What are the prepayment penalty terms? Can they be bought out at closing? Does the lender offer products built specifically for the BRRRR strategy? Calculate the total cost of your planned refinance including the prepayment penalty to ensure the strategy remains profitable.

Mistake #6: Not Vetting Lender's Actual Closing Timeline and Missing Deals

You've seen the ads—"14-day closes!" or "Fast funding in 21 days!" Sounds great, right? But here's what the fine print often says: "for qualified borrowers with complete documentation" or "on select properties." Investors who take these marketing promises at face value often end up scrambling to extend contracts, paying extension fees, or watching deals slip away entirely.

Here's the truth: closing timelines depend on property type, your experience level, how complete your documentation is, and how busy the lender is. That same lender might close a seasoned investor with clean paperwork in 14 days but take 45 days for a first-timer or a property that needs extra underwriting attention.

Before you commit to a lender based on their advertised timeline, do your homework. Ask for references from recent borrowers with similar profiles—same property type, experience level, and loan amount. Get specific: "What was your timeline from application to closing?" and "Did the lender hit their initial estimate?" Online reviews can also reveal patterns of missed timelines that never make it into the marketing materials.

Here's a smart move: build buffer time into your contracts based on realistic timelines, not best-case marketing claims. If a lender promises 21-day closes but references point to 30-35 days in practice, negotiate a 45-day closing window with your seller. That cushion can save you from costly extension fees or contract penalties.

Mistake #7: Financing in Personal Name Instead of Entity, Limiting Future Growth

It's a common starting point: financing your first properties in your personal name to take advantage of conventional financing's lower rates and easier qualification. And honestly, it works fine for your first few deals. But as you grow, this approach can box you in. Most conventional lenders cap you at 4-10 financed properties in your personal name, and each one chips away at your personal debt-to-income ratio, shrinking your borrowing power.

Business-purpose loans designed for investment properties require borrowing through a legal entity (LLC, Corporation, or Partnership), but here's the good news: they offer unlimited scalability. You can finance dozens of properties through entities without bumping into conventional loan caps, and the debt stays off your personal credit report—meaning your personal [DTI ratio](https://www.offermarket.us/blog/how-to calculate-your-dti-ratio) remains untouched.

Here's the catch: switching from personal to entity financing down the road means either refinancing existing properties (hello again, closing costs) or juggling a mixed portfolio that's trickier to manage. Investors who set up entity-based financing from day one build a cleaner, more scalable foundation for growth.

If you're committed to building a portfolio beyond 4-10 properties, get your entity structure in place early and tap into business-purpose loans (DSCR, bank statement, or asset-based) right from the start. Yes, rates run slightly higher (typically 0.50-1.00% above conventional), but the unlimited scalability and streamlined portfolio management more than make up for it as you expand.

Mistake #8: Accepting 'Rate Lock' Terms Without Understanding Extension Fees

Rate locks shield you from rate increases while your loan is processing, but they come with an expiration date—usually 30, 45, or 60 days. If your loan doesn't close before that lock expires, you're looking at two options: extend the lock (which costs money) or accept whatever the current market rate happens to be—potentially much higher if rates have climbed.

Extension fees typically run 0.125-0.375% of your loan amount for each 15-day extension. Let's put that in real numbers: on a $250,000 loan, a 30-day extension could set you back $625-$1,875. If your lender keeps missing closing deadlines, you could end up paying thousands in extension fees—and none of it is your fault.

Here's the smart move: make sure your lock period matches the lender's realistic closing timeline, not their best-case-scenario marketing pitch. If a lender actually takes 35 days to close but only offers a 30-day lock, you're practically guaranteeing yourself extension fees. Request a lock period that provides at least a 7-10 day buffer beyond the lender's realistic timeline.

Some lenders offer "float-down" provisions that allow you to capture rate decreases if rates drop during your lock period, though these typically cost 0.125-0.25% at closing. In volatile rate environments, float-down provisions can provide valuable downside protection while maintaining your locked rate as a ceiling.

Mistake #9: Overlooking Lender's Servicing Quality and Long-Term Portfolio Relationship

Here's something many investors miss: they zero in on the origination experience—rates, fees, and closing speed—but completely overlook the servicing relationship that will last for years or even decades. Poor loan servicing creates ongoing headaches: misapplied payments, difficulty reaching customer service, unclear payoff quotes, and problems with insurance or tax escrow management.

Lenders handle servicing in three ways: in-house servicing (they service the loans they originate), third-party servicing (they sell servicing to another company), or immediate sale (they sell both the loan and servicing rights after closing). Each model has implications for your long-term experience.

In-house servicing typically delivers the best borrower experience—you maintain a direct relationship with the lender, and they're motivated to provide quality service to protect their reputation. Third-party servicing can range from excellent to frustrating depending on the servicer. Immediate sale means you have no ongoing relationship with your original lender, and your loan could change hands multiple times over its life.

Before selecting a lender, ask this key question: "Do you service your loans in-house, or do you sell servicing rights?" If they use third-party servicing, ask which servicer they use and research that company's reputation. For portfolio investors planning to hold properties long-term, servicing quality should be a primary selection criterion, not an afterthought.

Check online reviews specifically for servicing complaints: "payment processing issues," "escrow problems," "difficulty getting payoff quotes," or "poor customer service after closing. " These patterns indicate systemic servicing problems that will affect your long-term experience. A lender with slightly higher rates but excellent servicing may provide better overall value than the cheapest option with terrible ongoing service.

OfferMarket: The Investor's Default Choice for 2026

After evaluating dozens of investment property mortgage lenders, one thing becomes clear: most are stuck in the past. You know the drill—endless phone tag with loan officers, uploading the same documents over and over, and fee structures that only make sense when you're sitting at the closing table. And let's not forget the hard credit pulls before you even know if the numbers work for you. For serious real estate investors in 2026, this old-school approach isn't just frustrating—it's costing you deals.

OfferMarket takes a completely different approach. Created by real estate investors who've lived through these headaches while building their own portfolios, the platform finally delivers what you've been promised for years: real transparency, actual speed, and technology that works for you instead of against you.

Transparent, Tech-First Platform

Here's where OfferMarket flips the script: you get instant, accurate pricing right from the start. No application hoops to jump through. No loan officer standing between you and your numbers. No hard credit pull ding on your score before you've even decided to move forward. Just preliminary loan terms in minutes through a soft credit check that keeps your credit profile clean.

And the transparency doesn't stop there. OfferMarket's DSCR loan platform shows you all fees upfront—no origination points buried in the fine print, no surprise "underwriting fees" at closing, no mystery charges that nobody mentioned during your quote. The numbers you see at the start? They match what shows up on your closing disclosure. That kind of consistency is hard to find in investment property financing, but it's exactly what you need to make confident decisions.

The technology stack powering this transparency includes automated property analysis that evaluates rental comps, market rent potential, and DSCR calculations—no manual underwriter intervention needed. Digital document upload means you can say goodbye to endless email chains and lost paperwork that make traditional closings such a headache. Streamlined underwriting processes tap into data integrations that verify information in hours, not weeks.

Specialized Investment Property Expertise

OfferMarket focuses exclusively on two loan products that matter most to active investors like you: DSCR loans for rental properties and Fix & Flip financing for value-add projects. This specialization means the platform isn't juggling consumer mortgages, commercial real estate, or other lending verticals that dilute focus and slow things down.

DSCR loans through OfferMarket qualify you based on property cash flow rather than personal income—perfect if you're managing multiple properties, earning self-employment income, or dealing with complex tax returns.

Fix & Flip financing follows the same tech-enabled approach: instant preliminary terms, transparent fee structures, and rapid closings that keep pace with competitive markets. You can model deals, request quotes, and move toward closing without the friction that causes missed opportunities with slower lenders.

Competitive Advantages That Matter

Speed claims are common in investment property lending, but actual delivery? That's rare. OfferMarket consistently closes loans in 14-21 days—a timeline backed by investor reviews and repeat customers who've closed multiple properties through the platform. This isn't marketing fluff—it's operational reality enabled by technology that eliminates manual bottlenecks.

The pricing structure offers genuine competitive advantages. Select DSCR programs carry zero origination fees, eliminating the 1-2 point charges ($2,000-$4,000 on a $200,000 loan) that traditional lenders build into their pricing. When origination points do apply on certain programs, they're disclosed upfront in initial quotes rather than revealed during closing document review.

Prepayment penalties, when present, are clearly explained with specific terms and buyout calculations available before commitment. Some OfferMarket programs offer no prepayment penalties at all, giving you flexibility to refinance frequently or sell properties after value-add improvements. This transparency around penalties stands in stark contrast to traditional lenders who bury these terms in dense loan documents.

Reserve requirements follow the same straightforward approach. OfferMarket specifies exact reserve amounts (typically 3-6 months of PITIA payments) during the quote phase, so you can plan your liquidity needs before moving forward. Traditional lenders often leave reserve requirements vague until late in the process, creating last-minute scrambles for additional capital.

Your Complete Investor Toolkit

OfferMarket goes beyond lending to give you a complete investor ecosystem. The platform integrates property listings, letting you search inventory and request financing at the same time. This integration eliminates the disconnect between property search and loan qualification that slows down traditional acquisition processes.

Insurance offerings through the platform remove another friction point. Rather than shopping multiple carriers after loan approval, you can secure property insurance as part of the OfferMarket workflow, ensuring coverage is in place before closing and often locking in better rates through platform partnerships.

How OfferMarket Compares to Traditional Lenders

Stack us up against the major investment property mortgage lenders on this list, and the differences are clear:

Speed: Traditional lenders quote 21-30 day closings and often miss those targets. OfferMarket consistently delivers 14-21 day closings. Our technology removes the manual bottlenecks that slow down traditional processes.

Transparency: Legacy lenders reveal full fee structures late in the game. OfferMarket shows you all costs upfront in your initial quote, with final closing costs matching preliminary estimates within narrow margins.

Technology: Traditional lenders have bolted online portals onto outdated systems. OfferMarket built its platform from the ground up around how investors actually work—giving you genuinely streamlined processes instead of digitized paperwork.

Total Cost: Look at the full picture—origination fees, underwriting charges, rate buydowns, and closing costs. OfferMarket's zero-origination programs often save you more money overall, even when rates look similar to what competitors offer.

Accessibility: Most lenders make you get on the phone with a loan officer just to see a quote. OfferMarket gives you instant preliminary terms—so you can evaluate multiple properties quickly without spending hours in conversations.

Flexibility: Traditional lenders stick to rigid wholesale guidelines. OfferMarket's lending approach means more thoughtful underwriting that weighs your experience, portfolio track record, and the specifics of each deal.

If you're tired of the runaround, hidden costs, and delays that come with traditional investment property lending, OfferMarket is built differently. We don't just talk about being faster and more transparent—our technology, direct lending model, and investor-minded team are designed to actually deliver on those promises.

The 2026 investment property lending market has plenty of solid lenders, each with their own sweet spots for certain investors and deal types. But if speed, transparency, and technology that simplifies rather than complicates matter to you, OfferMarket should be your starting point—the lender you check first and the standard you measure everyone else against.

Step 1: Get Your Instant Quote

Don't waste another minute with lenders who make you jump through hoops before showing you basic loan terms. Use OfferMarket's Instant Quote to see how our 2026 DSCR rates and fees stack up against the "Big Names" on this list. You'll get preliminary terms in minutes—no credit pull, no obligation, and zero pressure. Our straightforward pricing means the numbers in your quote are the numbers at closing. No hidden fees. No bait-and-switch. No surprises.

This isn't your typical quote request form. It's a full pre-qualification that matches your scenario against our complete product lineup, pinpointing the best loan structure for your investment goals. Whether you're picking up your first rental or refinancing a portfolio of 20+ units, you'll see exactly how OfferMarket's direct lending approach puts real savings in your pocket and gets you to closing faster.

Step 2: Right-Size Your Deal Parameters

Before you make offers or refinance existing properties, ground your assumptions in solid numbers. Use our DSCR Calculator to see exactly how lenders assess your property's cash flow and determine your maximum loan amount. This isn't a back-of-the-napkin estimator—it's the same calculation engine our underwriters rely on for real loan applications.

If you're in the fix-and-flip game, our Fix and Flip Calculator breaks down acquisition costs, renovation budgets, holding costs, and projected returns. Plug in your deal details and instantly know whether your profit margins make the risk worthwhile. These aren't flashy marketing tools—they're professional-grade platforms that help you sidestep costly mistakes and focus on deals that actually fit your criteria.

Step 3: Explore Your Next Investment Opportunity

Great financing is only part of the puzzle. Even the best loan terms won't help if you can't find properties that match your investment goals. Explore OfferMarket's property marketplace to find investment opportunities that match your strategy and budget. Our all-in-one platform gives you more than financing—you get access to a handpicked selection of properties and portfolio tools that help you move faster from research to closing.

While typical property search sites show you everything under the sun, our marketplace zeros in on what matters to investors: cash flow potential, value-add opportunities, and markets with solid rental fundamentals.

OfferMarket Loans

Check your rate

60 seconds · no credit pull