*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

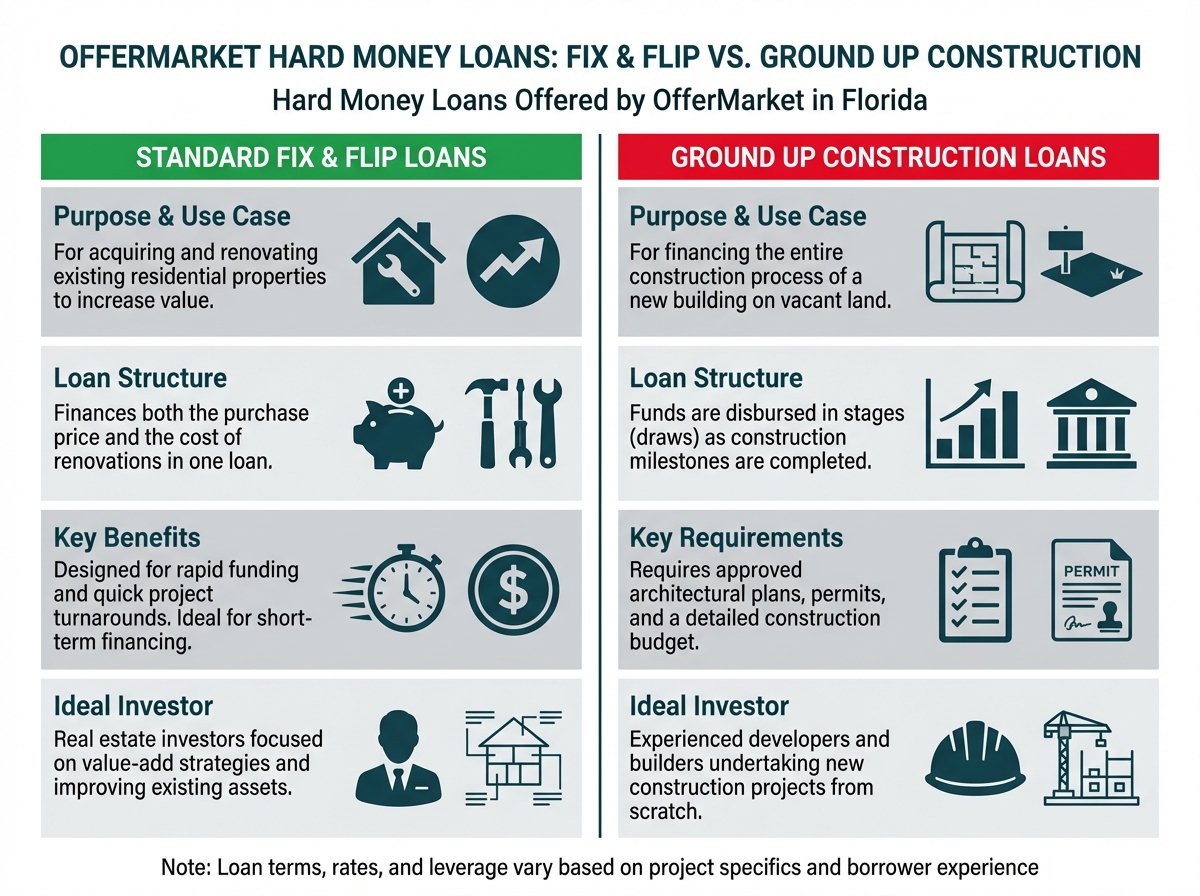

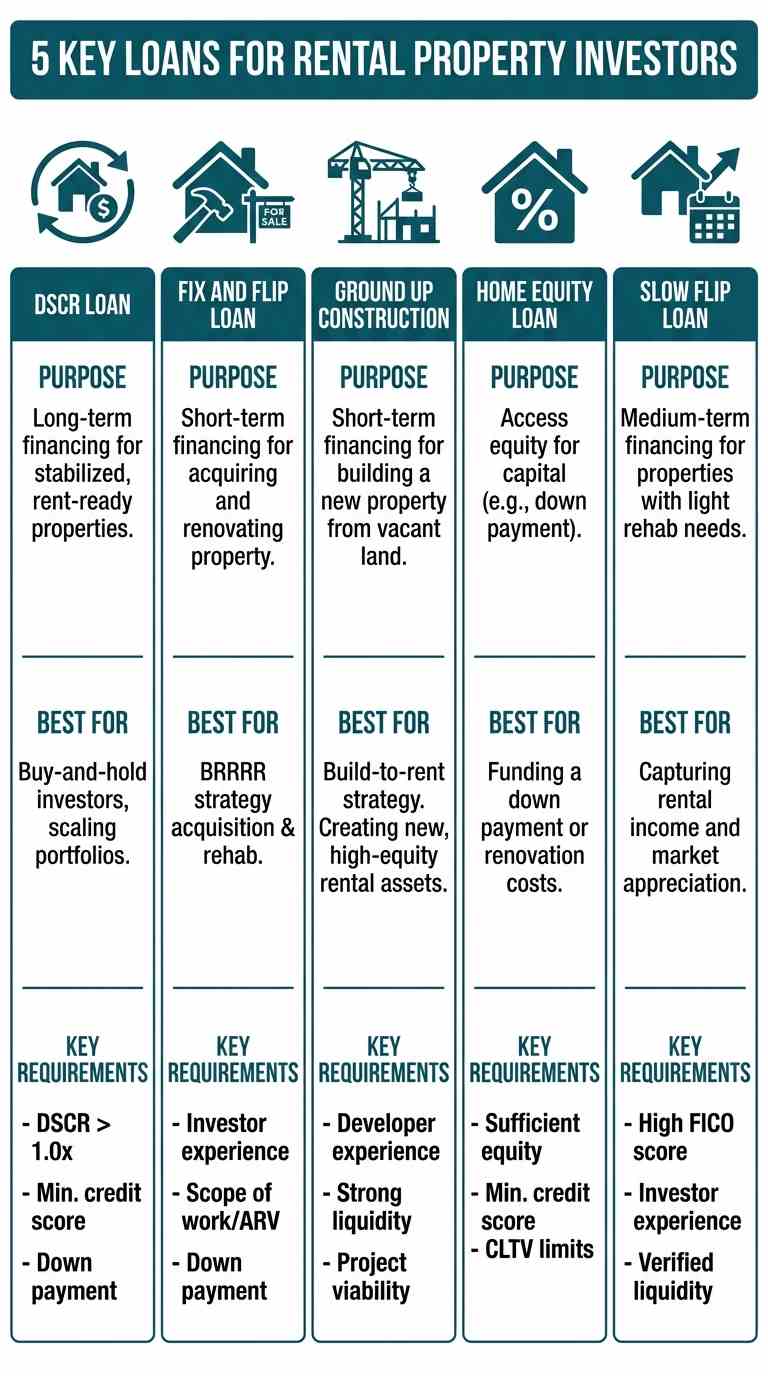

Hard Money Loans Offered by OfferMarket in Florida

OfferMarket provides two primary hard money loan products designed specifically for real estate investors operating in Florida's dynamic market: Standard Fix & Flip loans and Ground Up Construction loans. Understanding the distinctions between these financing options is critical for maximizing your investment returns and ensuring your project has the appropriate capital structure from day one.

Standard Fix & Flip Loans: Structure, Terms, and Ideal Use Cases

Standard Fix & Flip loans represent the most commonly used hard money product for Florida real estate investors. These loans are specifically designed for investors purchasing existing properties that require renovation before being sold or refinanced. The structure is straightforward: you receive funding to acquire the property and complete the necessary improvements, then repay the loan when you sell the renovated property or refinance into permanent financing.

The typical structure of a Fix & Flip loan includes funding for both the purchase price and the renovation budget. OfferMarket can provide up to 90% of the purchase price and 100% of the renovation budget, allowing investors to preserve capital and maximize leverage. However, the total loan amount is capped at 75% of the After Repair Value (ARV), ensuring that adequate equity cushion exists in the deal to protect both the lender and borrower.

Fix and flip loan rates in 2025 typically range from 8% to 14%, with final pricing dependent on your experience level, property location, and creditworthiness. Interest rates on these loans are higher than conventional mortgages because they're based primarily on the property's value rather than the borrower's income, and they offer significantly faster closing timelines—often within 10 to 19 days.

The loan terms are structured as interest-only payments, meaning you only pay the interest each month without reducing the principal balance. This structure keeps your monthly carrying costs lower during the renovation period, preserving cash flow for unexpected expenses or additional investment opportunities. The standard loan term is 12 months, though OfferMarket offers extensions to 18 or 24 months for projects that require longer timelines.

Standard Fix & Flip loans are ideal for several scenarios in the Florida market:

Single-family home renovations: When you're purchasing a distressed property in a desirable Florida neighborhood, completing cosmetic or moderate renovations, and selling to an end-user or retail buyer.

Small multifamily properties: When acquiring 2-4 unit properties that need renovation before being sold or refinanced into permanent financing.

Quick turnaround projects: Properties where you can complete renovations within 3-6 months and list for sale, allowing you to repay the loan well within the 12-month term.

Value-add opportunities: Situations where strategic improvements—such as adding square footage, updating finishes, or improving curb appeal—can significantly increase the property's market value in Florida's competitive real estate landscape.

The beauty of Standard Fix & Flip loans lies in their simplicity and speed. You're not dealing with the extensive documentation requirements of conventional loans, and underwriting focuses primarily on the deal's profitability rather than your personal income or employment history. For experienced investors with a proven track record, this can mean accessing capital for multiple projects simultaneously and scaling your Florida real estate portfolio rapidly.

Ground Up Construction Loans: When and Why to Use Them

Ground Up Construction loans serve a fundamentally different purpose than Fix & Flip loans. These loans finance projects where you're building a new structure from the foundation up, rather than renovating an existing building. In Florida's robust real estate market, ground-up construction opportunities abound, from infill lots in established neighborhoods to larger parcels in developing areas.

The structure of a Ground Up Construction loan is more complex than a standard Fix & Flip loan because the collateral—the property—doesn't exist at the beginning of the project. The lender must carefully manage disbursements throughout the construction process, releasing funds in stages (called "draws") as specific construction milestones are completed and verified by inspectors.

Ground Up Construction loans typically require more equity and a proven track record compared to Fix & Flip loans. While OfferMarket may finance up to 90% of the purchase price on a cosmetic Fix & Flip deal for beginners, ground-up projects are strictly reserved for experienced investors (Tier 3 or higher) who have a verified history of completing ground-up builds or major structural expansions. For these experienced builders, OfferMarket requires a minimum 15% to 20% equity contribution (up to 85% Initial LTC) and will finance 100% of the construction budget, provided the total loan does not exceed 70% to 75% of the After Repair Value (ARV).

The loan term for Ground Up Construction projects can be longer than standard 12-month Fix & Flip loans. OfferMarket offers 18 to 24-month terms for heavy structural and ground-up projects to accommodate unpredictable timelines—such as Florida's hurricane season delays and permitting challenges—though these extended terms do come with a loan-level pricing adjustment (a slight premium on your rate).

Interest rates on Ground Up Construction loans are comparable to Fix & Flip loans but may include additional fees for draw inspections and construction monitoring. Some lenders charge per-draw fees (typically $250-$500 per inspection) to cover the cost of verifying that work has been completed before releasing funds.

Ground Up Construction loans are ideal for these Florida investment scenarios:

Teardown and rebuild projects: When you purchase a property in a prime Florida location where the land value significantly exceeds the existing structure's value, and the highest and best use is to demolish and build new.

Infill development: Building new single-family homes or small multifamily properties on vacant lots in established neighborhoods where demand exceeds supply.

Luxury custom builds: Constructing high-end properties in premium Florida markets like Miami, Naples, or Palm Beach where buyers seek new construction with modern amenities and hurricane-resistant features.

Spec home construction: Building homes on speculation in growing Florida markets where you can sell the completed property quickly to end-users or investors.

Vertical development: Constructing single-family homes, duplexes, triplexes, or quadruplexes on parcels zoned for higher density development (Note: OfferMarket explicitly prohibit ground-up condominium construction)

The decision to pursue a Ground Up Construction loan requires careful analysis of your market knowledge, construction experience, and risk tolerance. Construction projects carry inherently more variables than renovations: permitting can take longer than anticipated, subcontractors may face scheduling conflicts, material costs can fluctuate, and weather delays are common in Florida, particularly during hurricane season.

However, for experienced investors with strong construction management capabilities, ground-up projects can offer superior returns compared to renovations. You're creating a brand-new product that appeals to buyers seeking modern design, energy efficiency, and the latest building codes—factors that command premium pricing in Florida's competitive market.

Differences Between the Two Loan Products

Understanding the key differences between Standard Fix & Flip loans and Ground Up Construction loans helps you select the right financing tool for your specific project:

Collateral type: Fix & Flip loans are secured by existing structures with established value, while Construction loans are secured by land and the future value of the completed structure.

Leverage levels: Fix & Flip loans typically offer higher leverage (up to 90% of the purchase price for experienced investors), while Construction loans require slightly more borrower equity (capped at 85% Initial LTC) and are strictly prohibited for beginner investors

Disbursement structure: Both Fix & Flip and Construction loans hold back 100% of the renovation or construction budget. The lender will never provide these funds upfront; instead, they are disbursed through a draw schedule to reimburse the borrower as specific construction milestones are completed.

Loan terms: Fix & Flip loans standard at 12 months with extensions available, while Construction loans typically start at 18-24 months to accommodate longer timelines.

Underwriting focus: Fix & Flip loans emphasize the property's current condition and ARV, while Construction loans scrutinize construction plans, budgets, contractor qualifications, and timeline feasibility.

Inspection requirements: Fix & Flip loans may require an initial inspection and final inspection, while Construction loans require multiple draw inspections throughout the project.

Risk profile: Construction loans carry higher risk due to the complexity of building from scratch, which is reflected in equity requirements and sometimes pricing.

Exit strategy: Fix & Flip loans typically exit through retail sale or refinance after renovation, while Construction loans may exit through sale, refinance, or conversion to permanent financing.

How to Determine Which Loan Type Fits Your Florida Project

Selecting the appropriate loan product requires honest assessment of your project, experience, and market conditions. Start by evaluating the property itself:

If an existing structure is present and can be economically renovated to achieve your target ARV, a Standard Fix & Flip loan is almost always the appropriate choice. Even if the property needs extensive renovation, it can qualify for a Fix & Flip loan provided the existing property remains framed and roofed. (Note: Extensive renovations and additions are strictly reserved for experienced investors)."

If the property is a vacant lot or the existing structure must be demolished because renovation costs exceed rebuild costs, a Ground Up Construction loan is necessary. Calculate the cost of renovation versus demolition and new construction; if new construction provides better returns or the existing structure is beyond economical repair, construction financing is your path forward.

Consider your experience level and construction management capabilities. Ground Up Construction projects demand significant expertise in managing contractors, navigating permitting processes, and handling the dozens of decisions required during construction. If you haven't previously completed ground-up projects, partnering with an experienced builder or starting with a Fix & Flip project to build your track record may be prudent.

Evaluate your timeline and holding cost tolerance. Fix & Flip projects typically move faster—you can often complete renovations in 3-6 months and list for sale immediately. Construction projects take longer, with 9-15 months being common from permit to completion. Longer timelines mean higher interest costs and more exposure to market fluctuations.

Assess market conditions in your specific Florida location. In rapidly appreciating markets, construction projects that take 12-18 months can benefit from price increases during the build period. In stable or declining markets, faster Fix & Flip projects that minimize holding time may be safer investments.

Finally, run the numbers comprehensively. Use OfferMarket's instant quote tool to model both scenarios if you're considering whether to renovate or rebuild. Compare the all-in costs (purchase, renovation or construction, financing costs, holding costs) against your projected ARV for each approach. The option that provides the highest return on investment while matching your risk tolerance and capability is the right choice for your Florida project.

General Terms for Florida Fix & Flip Loans

When evaluating hard money loans for fix and flip projects in Florida, understanding the fundamental loan terms is essential for structuring profitable deals. OfferMarket provides competitive financing solutions designed specifically for real estate investors operating in the Florida market, with terms that balance accessibility and prudent lending practices.

Loan Amounts and Flexibility

OfferMarket's Florida hard money loans accommodate projects ranging from smaller renovations to substantial investments. The standard loan range spans from $50,000 to $1,000,000, with higher amounts available for experienced investors with proven track records. This flexibility allows investors to pursue everything from modest single-family rehabs in suburban neighborhoods to more ambitious multi-unit renovations or higher-value properties in premium Florida markets like Miami, Tampa, or Naples.

The scalability of loan amounts means that whether you're a newer investor testing the waters with a starter property or an established professional managing multiple concurrent projects, OfferMarket can structure financing that matches your deal size and investment strategy.

Maximum Leverage: Purchase and Renovation Financing

One of the most attractive features of OfferMarket's Florida hard money loans is the high leverage available to qualified borrowers. The program offers up to 90% financing on the purchase price and 100% of the renovation budget, allowing investors to preserve capital and maximize their return on investment.

This leverage structure is particularly powerful for investors who want to scale their operations without tying up substantial cash reserves in each deal. For example, on a $200,000 purchase with a $50,000 renovation budget, a qualified borrower could potentially secure $180,000 toward the purchase and the full $50,000 for renovations, requiring only $20,000 in cash to control a $250,000 project.

The ability to finance the entire renovation budget is especially valuable in Florida's dynamic real estate market. While the lender holds these funds in escrow and reimburses the investor in 'draws' as work is completed, having the full rehab budget secured upfront provides investors with the financial confidence to execute their renovation plans without worrying about mid-project funding gaps.

Understanding the ARLTV Cap at 75%

While OfferMarket offers generous leverage on the front end, all loans are subject to a strict After Repair Loan-to-Value (ARLTV) cap—typically 70% to 75%. This metric is crucial for both lender risk management and ensuring investors maintain adequate equity in their projects.

ARLTV is calculated by dividing the total loan amount by the property's estimated after-repair value (ARV). For instance, if you're purchasing a property for $200,000, investing $50,000 in renovations, and the ARV is projected at $350,000, your total loan amount cannot exceed $262,500 (75% of $350,000).

This cap serves as a protective measure that ensures projects have sufficient equity cushion and realistic profit margins. It prevents over-leveraging and helps investors avoid situations where they're upside-down in a property if market conditions shift or renovation costs exceed expectations. The ARLTV cap also encourages conservative ARV estimates, which is a hallmark of successful real estate investing.

When structuring your deal, it's essential to work backward from the ARLTV cap to determine your maximum loan amount. If your combined purchase and renovation financing exceeds 75% ARLTV, you'll need to bring additional capital to the table or adjust your purchase price or renovation scope.

Loan Terms: Interest-Only Structure and Extensions

OfferMarket's standard Florida fix and flip loans feature a 12-month interest-only term, which aligns perfectly with the typical timeline for most renovation and resale projects. The interest-only structure keeps monthly carrying costs manageable, allowing investors to focus their capital on renovations rather than principal reduction.

For projects requiring additional time—such as more extensive renovations, permitting delays, or strategic holds to optimize market timing—extension options of 18 to 24 months are available. These extensions provide crucial flexibility for investors who encounter unexpected challenges or identify opportunities to increase returns by holding properties longer.

According to industry data, hard money loan interest rates in Florida typically range from 8% to 15%, with specific rates depending on borrower experience, property type, and project risk profile. OfferMarket's competitive rates fall within this range, with the most qualified borrowers securing terms at the lower end of the spectrum.

The interest-only payment structure significantly reduces monthly obligations compared to amortizing loans. For example, on a $200,000 loan at 9.75% interest, the monthly payment would be $1,625 interest-only, compared to $17,559 if it were a 12-month fully amortizing loan—a massive difference of $15,934 per month that can be redirected toward renovations or reserves.

Credit Score Requirements and Qualifications

OfferMarket maintains accessible yet responsible credit standards for Florida hard money loans. The minimum credit score requirement is 680 FICO, which opens the door to investors who may have experienced past credit challenges but have demonstrated financial recovery and real estate competency.

However, borrowers with credit scores of 720 or higher are highly preferred and typically receive more favorable terms, including lower interest rates, reduced fees, and higher maximum leverage. The credit score differential can translate to meaningful cost savings over the life of a loan.

For example, a borrower with a 700 FICO score might secure a rate that's 1-2% lower than someone at the 680 minimum threshold. On a $200,000 loan over 12 months, this could represent savings of $2,000 to $4,000 in interest costs—money that flows directly to the investor's bottom line.

It's worth noting that while credit scores are important, hard money lenders like OfferMarket take a holistic view of borrower qualifications. A lower credit score can be offset by strong real estate experience, substantial liquid reserves, or a particularly compelling deal with conservative leverage and strong exit strategy.

How Experience Level Affects Terms and Leverage

Your track record as a real estate investor plays a significant role in determining the specific terms and maximum leverage available on your Florida hard money loan. OfferMarket evaluates borrowers across different experience tiers, and your classification directly impacts your borrowing power.

Experienced investors—those who have successfully completed multiple fix and flip projects in the past three years—typically qualify for maximum leverage options, including the full 90% purchase and 100% rehab financing. These investors have demonstrated their ability to accurately estimate renovation costs, manage contractors, and execute profitable exits, which reduces lender risk.

Intermediate investors with one to three completed projects may qualify for slightly reduced leverage, such as 85% of purchase price and 100% of renovations, or 90% of purchase with a lower ARLTV cap. These terms still provide substantial financing while accounting for the moderately higher risk profile.

Newer investors with limited or no previous fix and flip experience will typically face more conservative leverage, often in the 75-80% purchase price range with 100% rehab financing, subject to the 70% ARLTV cap. First-time flippers may also be required to work with licensed general contractors rather than self-managing renovations, and may face additional oversight requirements such as more frequent draw inspections.

When applying for an OfferMarket loan, you'll be asked to provide details about your real estate investment track record from the past three years, including the number of projects completed, total transaction volume, and types of properties. This information helps determine your experience tier and establishes the maximum leverage and most competitive terms available for your Florida project.

Building your track record strategically—even if it means starting with more conservative leverage on early deals—positions you to access increasingly favorable terms as you demonstrate consistent success. Many successful investors view their first few deals as investments not just in properties, but in their own credibility and borrowing capacity for future projects.

State-Specific Requirements for Florida Hard Money Loans

When pursuing hard money financing in Florida, real estate investors must navigate several unique state-specific requirements that don't exist in most other markets. Understanding these regulations upfront can save you time, money, and potential deal complications during the closing process.

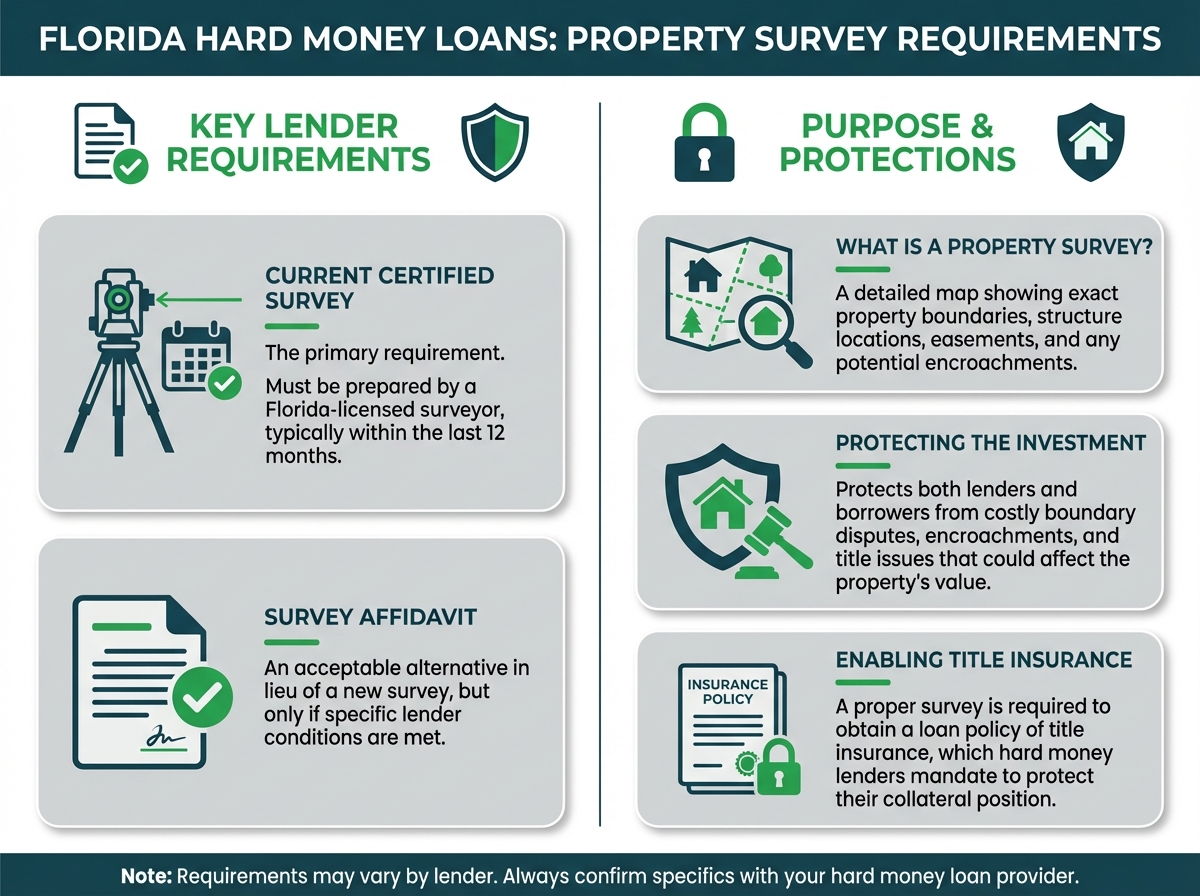

Mandatory Property Surveys in Florida

Florida is one of the few states that mandates a certified property survey for most real estate transactions involving institutional financing. A property survey is a detailed map prepared by a licensed surveyor that shows the exact boundaries of a property, locations of structures, easements, encroachments, and any potential boundary disputes.

For hard money loans in Florida, lenders typically require either:

- A current certified survey (usually prepared within the last 12 months) conducted by a Florida-licensed surveyor

- An acceptable survey affidavit in lieu of a new survey, if certain conditions are met

The survey requirement exists to protect both lenders and borrowers from boundary disputes, encroachments, and title issues that could affect the property's value or marketability. Without a proper survey, you cannot obtain a loan policy of title insurance, which hard money lenders require to protect their collateral position.

Survey Affidavit Alternatives

In some circumstances, Florida allows property owners to execute a survey affidavit instead of obtaining a new certified survey. This affidavit is a sworn statement declaring that no improvements, alterations, or boundary changes have occurred since the last certified survey was completed.

Survey affidavits are acceptable when:

- An existing survey from a previous transaction is available and relatively recent

- No structural additions, fence installations, or property line modifications have occurred

- The title company agrees to issue a loan policy based on the affidavit

- The lender approves the use of an affidavit in lieu of a new survey

However, most hard money lenders prefer new surveys for properties that haven't been surveyed within the past 2-3 years, especially for fix-and-flip projects where property improvements will be made. Budget $400-$800 for a residential property survey in Florida, with costs varying based on property size, location, and complexity.

The Florida Condo Rule: Milestone Structural Inspections

Following the tragic Surfside condominium collapse in 2021, Florida enacted comprehensive legislation requiring mandatory structural inspections for older condominium and cooperative buildings. Florida Statute 553.899 now mandates what are known as "milestone inspections" for qualifying buildings.

![**Task**: Create an infographic explaining Florida's Milestone Inspection requirements for condominium buildings, including age thresholds, coastal proximity rules, and inspection frequency.

**Visual Structure**: A three-section vertical infographic with clear headers and visual icons representing buildings, coastal areas, and inspection timelines.

**ASCII Layout Reference**:

```

┌───────────────────────────────────────────────────────────┐

│ FLORIDA CONDO MILESTONE INSPECTION REQUIREMENTS │

├───────────────────────────────────────────────────────────┤

│ │

│ BUILDINGS SUBJECT TO INSPECTION │

│ [Building Icon - 3+ Stories] │

│ • 3 or more stories in height │

│ • Condominium and cooperative buildings │

│ │

├───────────────────────────────────────────────────────────┤

│ │

│ AGE REQUIREMENTS │

│ [Calendar Icon] │

│ Standard Properties: 30 years from certificate of │

│ occupancy │

│ │

│ [Wave/Coast Icon] │

│ Coastal Properties: 25 years from certificate of │

│ (within 3 miles) occupancy │

│ │

├───────────────────────────────────────────────────────────┤

│ │

│ INSPECTION FREQUENCY │

│ [Circular Arrow Icon] │

│ Every 10 years after initial milestone inspection │

│ │

├───────────────────────────────────────────────────────────┤

│ │

│ ⚠ FINANCING IMPACT ⚠ │

│ Properties that fail inspection or reveal significant │

│ structural issues become UNFINANCEABLE until │

│ remediation is complete │

│ │

└───────────────────────────────────────────────────────────┘

```

**Image Section Breakdown**:

- Header:](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1772831792548_rpdv4x.jpg?alt=media&token=3735d2b5-b894-401c-9b01-7afaf98b2382)

A milestone inspection is a comprehensive structural assessment performed by a Florida-licensed engineer or architect that evaluates the structural integrity of a building, including:

- Load-bearing walls and columns

- Primary structural members and connections

- Foundation and structural support systems

- Exterior building envelope components

- Waterproofing and water intrusion points

- Balconies, railings, and other load-bearing attachments

These inspections must identify any structural deficiencies, safety concerns, or maintenance issues that could compromise the building's integrity. The inspection report must be submitted to the local building department and shared with the condominium or cooperative association.

Buildings Subject to Milestone Inspection Requirements

The milestone inspection requirement applies to:

- All condominium and cooperative buildings that are three or more stories in height

- Buildings that have reached 30 years of age based on the date the certificate of occupancy was issued

- Subsequent inspections every 10 years after the initial milestone inspection

For properties located within three miles of the coastline, the requirements become even more stringent. Coastal properties must undergo their first milestone inspection at 25 years of age rather than 30 years, recognizing the accelerated deterioration that occurs in salt air environments.

The building's age is calculated from the date the original certificate of occupancy was issued, not from when units were sold or when the building was substantially completed. This distinction is important when evaluating potential condo conversion projects or older buildings.

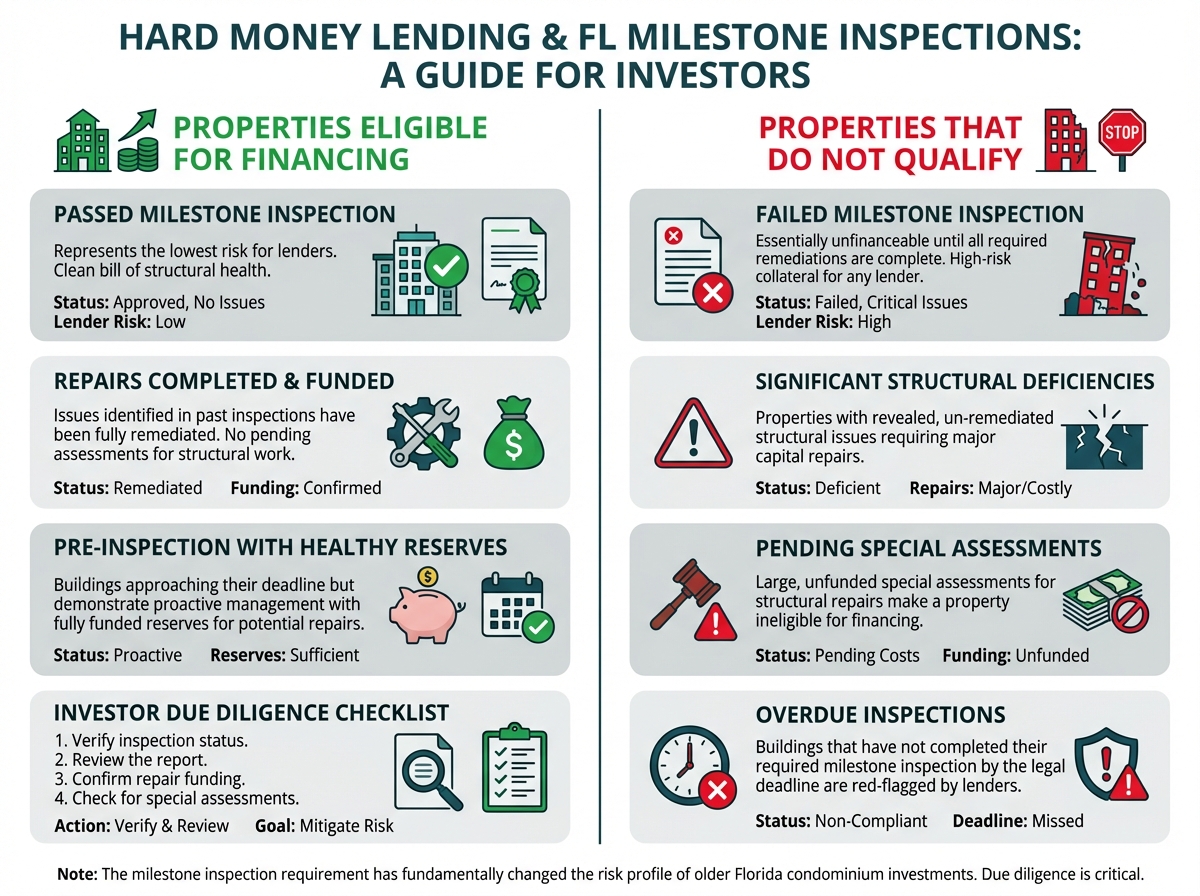

How Failing Inspections Impact Hard Money Financing

Here's where milestone inspections directly affect your ability to secure hard money financing: properties that fail their milestone inspection or reveal significant structural deficiencies become essentially unfinanceable until those issues are remediated.

Hard money lenders will not provide acquisition or renovation financing for condominium units in buildings that:

- Have failed a required milestone inspection

- Have revealed substantial structural issues requiring major capital repairs

- Are under special assessment for structural repairs exceeding certain thresholds

- Have not completed required milestone inspections when due

This creates a significant risk for investors purchasing older Florida condominiums, particularly in coastal areas. Before making an offer on any condo unit in a building approaching or exceeding the milestone inspection age thresholds, you should:

- Verify whether the building has completed its required milestone inspection

- Request a copy of the inspection report to review any identified deficiencies

- Confirm that any required repairs have been completed or are fully funded

- Check for pending special assessments related to structural repairs

Even if you're paying cash initially, failing to investigate milestone inspection status can leave you unable to refinance or sell to a financed buyer later. The milestone inspection requirement has fundamentally changed the risk profile of older Florida condominium investments, making due diligence on building structural integrity absolutely critical before closing any deal.

For buildings that haven't yet reached their milestone inspection deadline, factor in the potential cost and timeline of this requirement into your investment analysis. Inspection costs typically range from $5,000 to $25,000 depending on building size, and any required repairs could result in substantial special assessments to unit owners.

Unique Risks for Florida Hard Money Borrowers

Florida's real estate investment landscape presents distinct challenges that hard money borrowers must navigate carefully. Understanding these state-specific risks is essential for securing financing and protecting your investment from unexpected complications that could derail your project.

Aging Coastal Condos and Structural Inspection Challenges

Florida's coastal condominium market has undergone significant regulatory changes following high-profile structural failures. The state now mandates milestone structural inspections for specific condo projects under Florida Statute 553.899. These inspections apply to buildings over five stories tall and 30 years old, with the age requirement dropping to 25 years for properties located within three miles of the coast.

For hard money borrowers, these inspection requirements create a critical checkpoint in the financing process. Properties must provide passing inspection reports that verify structural integrity and safety compliance. Any revealed deficiencies in the building's foundation, load-bearing walls, or critical structural components can immediately disqualify a property from financing consideration. This means investors must conduct thorough due diligence before committing to a coastal condo project, as structural issues discovered during the inspection phase can completely eliminate financing options.

The inspection process itself adds both time and cost to your project timeline. Licensed engineers must conduct comprehensive assessments, and remediation of any identified issues can run into hundreds of thousands of dollars—costs that may not have been factored into your initial investment calculations. Smart investors order these inspections early in their due diligence period to avoid tying up capital in a property that ultimately proves unfinanceable.

How Structural and Safety Issues Lead to Financing Denial

Hard money lenders prioritize asset value above all else, and structural or safety deficiencies directly threaten that collateral value. When a property inspection reveals foundation problems, roof damage, electrical hazards, or code violations, lenders view the asset as compromised. The logic is straightforward: if the property requires extensive structural repairs before it can be safely occupied or sold, the lender's ability to recover their investment through foreclosure becomes severely limited.

Financing denials based on structural issues are typically non-negotiable. Unlike credit score deficiencies or experience gaps that might be overcome with higher down payments or co-borrowers, structural problems represent fundamental flaws in the collateral itself. A property with a failing foundation or extensive water damage cannot serve as adequate security for a loan, regardless of the borrower's qualifications.

This reality makes pre-purchase inspections absolutely critical for Florida investors. Engaging qualified inspectors who understand Florida's unique challenges—including termite damage, moisture intrusion, and hurricane-related wear—can save you from committing to a property that no lender will finance. Budget for comprehensive inspections that go beyond cosmetic issues and examine the property's structural bones, mechanical systems, and code compliance status.

Hurricane and Windstorm Insurance Requirements

Florida law mandates that residential property insurance policies include hurricane windstorm coverage, making this protection non-negotiable for hard money borrowers. Unlike flood insurance, which is optional in some areas, windstorm coverage is required by statute for properties financed with mortgages. This requirement reflects Florida's vulnerability to tropical storms and hurricanes that can cause catastrophic wind damage to roofs, windows, and structural elements.

![**Task**: Create an illustrative image showing a Florida coastal property with visual indicators of insurance requirements and cost considerations for real estate investors.

**Visual Structure**: A modern coastal Florida home as the central focus with insurance-related icons and cost callouts positioned around it.

**ASCII Layout Reference**:

```

┌─────────────────────────────────────────────────────────┐

│ │

│ FLORIDA PROPERTY INSURANCE REQUIREMENTS │

│ │

│ [$$$] [House] [Storm] │

│ Premium Windstorm│

│ Costs Required │

│ │

│ [Property] │

│ │

│ [Deductible] [Citizens] │

│ 2-5% of Insurance │

│ Value Available │

│ │

│ [Flood] [Annual] │

│ Separate Renewal │

│ Policy Required │

│ │

└─────────────────────────────────────────────────────────┘

```

**Image Section Breakdown**:

- Header:](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1772902834220_goat3u.jpg?alt=media&token=5387187e-7401-4d71-94dd-71fcab8fbd78)

For real estate investors, hurricane insurance represents a significant ongoing cost that must be factored into your project's carrying expenses. Premiums in coastal areas can run several thousand dollars annually, and hurricane deductibles are typically expressed as a percentage of the property's insured value—commonly 2% but potentially higher—rather than a flat dollar amount. This means a property insured for $500,000 might carry a $10,000 hurricane deductible, creating substantial out-of-pocket exposure if a storm strikes during your holding period.

Mortgage lenders, including hard money lenders, verify that adequate windstorm coverage is in place before closing. The policy must remain active throughout the loan term, with proof of renewal required annually. Allowing coverage to lapse can trigger default provisions in your loan agreement, potentially accelerating repayment or triggering penalties. Some lenders may even force-place insurance at the borrower's expense if they discover a coverage gap, and force-placed policies typically cost significantly more than coverage you arrange independently.

Understanding Citizens Property Insurance and Supplemental Coverage

When traditional insurance carriers decline coverage or quote prohibitively expensive premiums, many Florida property owners turn to Citizens Property Insurance Corporation, the state-created insurer of last resort. Citizens provides coverage when private market options are unavailable or unaffordable, but investors should understand both the benefits and limitations of this backstop.

Citizens policies often come with higher premiums than private insurance and may include more restrictive coverage terms. The organization operates as a non-profit entity, but its rates still reflect Florida's substantial hurricane risk. Additionally, Citizens policies may have higher deductibles and more limited coverage for certain types of damage compared to comprehensive private policies.

For investment properties, particularly those in high-risk coastal zones, supplemental coverage beyond a standard policy may be necessary. While Citizens and private insurers cover windstorm damage, flood insurance requires a separate policy through the National Flood Insurance Program (NFIP) or private flood insurers. Many coastal properties sit in flood zones where this coverage is mandatory for financing, adding another layer of insurance expense to your project budget.

Investors should also consider whether their standard policy adequately covers the specific risks of a fix-and-flip project. During renovation, properties may be vacant or partially demolished, conditions that can void certain coverages or require specialized builder's risk insurance. Consult with an insurance professional like OfferMarket who understands investment property needs to ensure you maintain continuous, adequate coverage throughout your project timeline.

Survey Mandate Impact on Closing Costs and Timelines

Florida's requirement for certified property surveys or acceptable survey affidavits adds both cost and time to the closing process for hard money loans. Unlike some states where title insurance alone suffices, Florida lenders typically require current surveys to verify property boundaries, identify encroachments, and confirm that improvements sit within legal property lines.

A new certified survey can cost anywhere from $400 to $2,000 or more, depending on property size, complexity, and location. Urban properties with clear lot lines and recent surveys may fall on the lower end of this range, while rural properties, waterfront lots, or parcels with irregular boundaries can require more extensive surveying work that pushes costs higher. This expense must be factored into your closing cost budget alongside title insurance, recording fees, and lender charges.

The timeline impact can be equally significant. Surveyors need time to schedule fieldwork, complete measurements, research property records, and prepare final documentation. In busy real estate markets, survey backlogs can extend this process to two or three weeks, potentially delaying your closing date. For investors pursuing time-sensitive opportunities—such as properties with multiple competing offers or those requiring quick closings to secure seller cooperation—survey delays can jeopardize deal completion.

Some properties may have existing surveys that lenders will accept if they're recent (typically within the last year) and show no material changes to the property since completion. An affidavit from the property owner attesting that no changes have occurred since the last survey may satisfy lender requirements in these cases, saving both time and money. However, if any improvements have been added, boundary disputes have arisen, or the existing survey is outdated, a new survey becomes mandatory.

Due Diligence Steps to Avoid Project-Killing Surprises

Successful Florida hard money borrowers approach due diligence systematically, treating it as an investment in risk mitigation rather than an optional expense. Start by ordering a comprehensive property inspection within days of going under contract. This inspection should specifically address Florida's unique concerns: termite damage, moisture intrusion, roof condition, hurricane shutter functionality, and HVAC system status in the humid climate.

For coastal properties or buildings meeting the milestone inspection criteria, obtain structural engineering assessments early in your due diligence period. Don't wait until you're days from closing to discover that a building requires $200,000 in foundation repairs or fails to meet current wind load requirements. These inspections cost more than standard home inspections—often $1,000 to $3,000—but they're essential for avoiding catastrophic surprises that eliminate financing options.

Research insurance availability and costs before committing to a property. Contact insurance agents who specialize in Florida investment properties to obtain preliminary quotes based on the property's location, age, and construction type. Discover whether standard coverage is available or if you'll need to pursue Citizens or specialized high-risk carriers. Factor realistic insurance costs into your project pro forma, as underestimating these expenses can turn an apparently profitable deal into a money-losing proposition.

Verify that any existing surveys are current and acceptable to your intended lender. If a new survey will be required, order it immediately upon contract execution to avoid closing delays. Similarly, confirm that the property's title is clear and that no unexpected liens, easements, or deed restrictions will complicate your renovation plans or exit strategy.

Finally, consult with your hard money lender early in the process about any property characteristics that might affect financing. Unusual property types, properties in special flood zones, or buildings with known code violations may require additional underwriting scrutiny or documentation. Transparent communication with your lender helps identify potential obstacles while you still have time to address them or, if necessary, exit the deal during your inspection period.

Florida's unique regulatory environment and natural hazard exposure create financing risks that don't exist in many other states. However, investors who understand these challenges and conduct thorough due diligence can successfully navigate them, securing hard money financing for profitable projects while avoiding costly surprises that derail less-prepared competitors.

Determine Your Maximum Loan Leverage in Florida

Understanding your borrowing power is essential before pursuing a hard money loan for your Florida real estate investment. Unlike traditional lenders who focus primarily on your credit score and income, hard money lenders like OfferMarket evaluate your experience as a real estate investor to determine how much leverage they'll extend on your project.

How Experience Determines Your Borrowing Power

Your track record as a real estate investor directly influences the loan-to-value (LTV) ratios and total leverage available to you. Hard money lenders assess risk based on your proven ability to successfully complete projects, which means experienced investors typically qualify for higher leverage than newcomers to the market.

OfferMarket evaluates your investment history from the past three years to place you in an experience tier. This tier determines critical loan parameters including:

- Maximum percentage of purchase price financed

- Percentage of renovation budget covered

- Overall after-repair loan-to-value (ARLTV) cap

- Interest rate and fee structure

The Three-Year Investment Track Record

When applying for a hard money loan in Florida, you'll need to provide documentation of your real estate investment activity over the previous 36 months. This track record should include:

Completed Projects: Properties you've successfully purchased, renovated, and either sold or refinanced. Each completed project demonstrates your ability to execute a deal from start to finish.

Active Projects: Current investments in progress show you're actively engaged in real estate and can manage multiple projects simultaneously.

Project Details: Be prepared to share purchase prices, renovation budgets, final sale prices or refinance values, and timelines for completion.

Geographic Experience: While projects outside Florida count toward your experience, local Florida market knowledge may provide additional credibility.

First-time investors shouldn't be discouraged—many hard money lenders, including OfferMarket, work with newer investors, though at more conservative leverage levels initially.

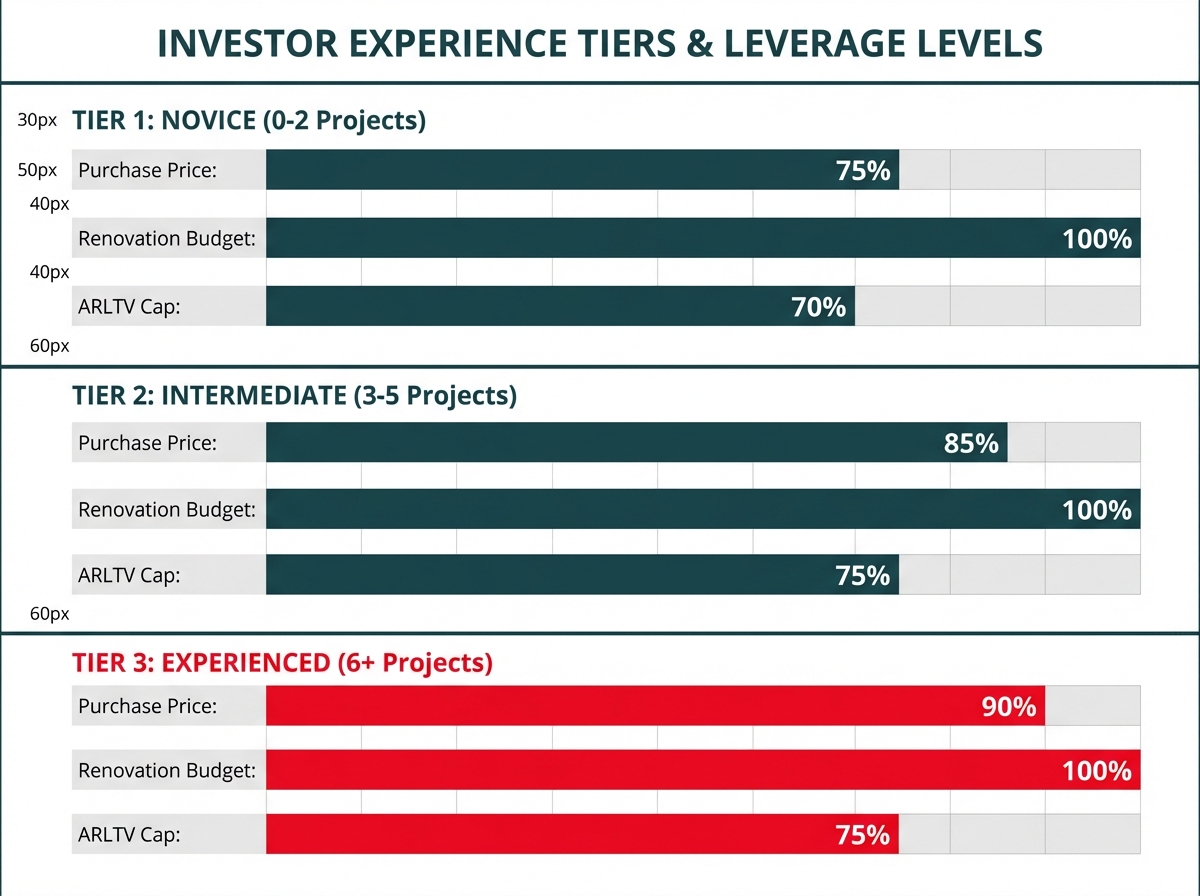

Experience Tier System and Leverage Levels

Hard money lenders typically categorize borrowers into experience tiers that directly impact loan terms. While specific tier structures vary by lender, here's how the system generally works:

Tier 1 - Novice Investors (0-2 completed projects in 3 years):

- Maximum 70-75% of purchase price

- Up to 100% of renovation budget

- ARLTV capped at 70%

- May require additional documentation or reserves

Tier 2 - Intermediate Investors (3-5 completed projects in 3 years):

- Maximum 80-85% of purchase price

- Up to 100% of renovation budget

- ARLTV capped at 75%

- Standard documentation requirements

Tier 3 - Experienced Investors (6+ completed projects in 3 years):

- Maximum 90% of purchase price

- Up to 100% of renovation budget

- ARLTV capped at 75%

- Streamlined approval process

According to research on loan-to-value ratios, hard money lenders typically offer loans with LTV ratios between 60% and 75%, depending on the property type and market conditions. Your experience tier determines where you fall within this range.

Step-by-Step Guide to Calculating Your Maximum Loan Amount

Follow this process to determine your potential loan amount for a Florida fix-and-flip project:

Step 1: Identify Your Property's Key Metrics

Start by gathering the fundamental numbers for your deal:

- Purchase price of the property

- Estimated renovation budget

- After-repair value (ARV) based on comparable sales

Step 2: Assess Your Experience Tier

Count your completed real estate projects in the past three years. Be honest about your experience level, as lenders will verify this information through documentation.

Step 3: Apply Your Tier's Purchase Price Leverage

Multiply the purchase price by your tier's maximum purchase price percentage:

- Novice (75%): Purchase Price × 0.75

- Intermediate (85%): Purchase Price × 0.85

- Experienced (90%): Purchase Price × 0.90

Step 4: Calculate Renovation Funding

Most hard money lenders, including OfferMarket, offer up to 100% of the renovation budget regardless of experience tier. Add your full renovation budget to the purchase price leverage calculated in Step 3.

Step 5: Check the ARLTV Cap

Calculate the maximum loan based on after-repair value:

- Total Loan Amount = ARV × ARLTV Cap (70-75% depending on tier)

Your actual loan amount will be the lower of either:

- The sum from Step 4 (purchase + renovation leverage), OR

- The ARLTV cap from Step 5

Step 6: Account for Closing Costs

Remember that you'll need cash for closing costs, which typically include:

- Origination fees (2-3 points)

- Title insurance and escrow fees

- Survey costs (required in Florida)

- Insurance premiums

- Attorney fees

Using OfferMarket's Instant Quote Tool

Rather than manually calculating these figures, OfferMarket's instant quote tool provides precise leverage calculations tailored to your specific situation. Here's how to use it effectively:

Input Your Property Information: Enter the Florida property's address, purchase price, estimated renovation budget, and projected after-repair value.

Share Your Experience: Provide accurate details about your real estate investment history over the past three years, including the number of completed projects and total volume.

Receive Your Custom Quote: Within minutes, you'll receive a detailed breakdown showing:

- Maximum loan amount you qualify for

- Monthly payment estimates

- Interest rate based on your experience tier

- Points and fees

- Estimated cash required to close

The instant quote tool eliminates guesswork and provides transparency into your borrowing power before you invest time in a formal application.

Example Scenarios: Different Leverage Levels in Action

Let's examine three realistic Florida fix-and-flip scenarios to illustrate how experience levels affect leverage:

Scenario 1: Novice Investor in Tampa Property Details:

- Purchase Price: $200,000

- Renovation Budget: $50,000

- After-Repair Value: $325,000

- Investor Experience: 0 completed projects (First-time flipper) Leverage Calculation:

- Purchase Price Funding: $200,000 × 75% = $150,000

- Renovation Funding: $50,000 × 100% = $50,000

- Combined Leverage: $200,000

- ARLTV Check: $325,000 × 70% = $227,500

- Maximum Loan: $200,000 (lower of the two)

- Cash Required: $50,000 (purchase balance) + closing costs

Scenario 2: Intermediate Investor in Orlando Property Details:

- Purchase Price: $180,000

- Renovation Budget: $60,000

- After-Repair Value: $310,000

- Investor Experience: 4 completed projects Leverage Calculation:

- Purchase Price Funding: $180,000 × 85% = $153,000

- Renovation Funding: $60,000 × 100% = $60,000

- Combined Leverage: $213,000

- ARLTV Check: $310,000 × 75% = $232,500

- Maximum Loan: $213,000 (lower of the two)

- Cash Required: $27,000 (purchase balance) + closing costs

Scenario 3: Experienced Investor in Miami

Property Details:

- Purchase Price: $350,000

- Renovation Budget: $80,000

- After-Repair Value: $580,000

- Investor Experience: 8 completed projects

Leverage Calculation:

- Purchase Price Funding: $350,000 × 90% = $315,000

- Renovation Funding: $80,000 × 100% = $80,000

- Combined Leverage: $395,000

- ARLTV Check: $580,000 × 75% = $435,000

- Maximum Loan: $395,000 (lower of the two)

- Cash Required: $35,000 (purchase balance) + closing costs

As these scenarios demonstrate, building your track record significantly increases your borrowing power. The experienced investor in Scenario 3 needed only $35,000 in cash for a $350,000 purchase, while the novice investor in Scenario 1 required $50,000 for a $200,000 purchase—despite the lower property price.

How to Apply for a Hard Money Loan in Florida

Applying for a hard money loan in Florida is significantly faster and more straightforward than traditional financing, but preparation is key to ensuring a smooth process. Understanding what documents you'll need, how the application works, and what timeline to expect will help you secure funding quickly and move forward with your investment project.

Step-by-Step Application Process Walkthrough

Step 1: Get Instant Quote

Start by getting an instant, soft-credit-pull quote. If the numbers align with your strategy, you’ll transition into the full loan application. This digital process is designed to be frictionless; you'll use a secure portal to upload your entity documents, and property details while tracking your progress in real-time.

Step 2: Submit Documentation & "Deal Room" Setup

Once your application is in, you’ll provide the "meat" of the deal. This includes your Scope of Work (SOW) for renovations and your track record as an investor. OfferMarket uses this data to move the file into underwriting immediately, minimizing the back-and-forth common with traditional banks.

Step 3: Property Inspection and Valuation

The lender orders a professional valuation—typically an appraisal or a Broker Price Opinion (BPO). For fix-and-flip projects, this is crucial: the appraiser determines both the "As-Is" value and the After-Repair Value (ARV) based on your SOW. Expect this to take 3–7 business days.

Step 4: Underwriting Review

The underwriting team stress-tests the deal. They verify your renovation plan’s feasibility, the accuracy of the ARV, and your experience level. In specific markets like Florida, they’ll also clear state-specific hurdles, such as condo-specific regulations or survey requirements, to ensure a clean lien.

Step 5: Loan Approval and Term Sheet

Upon clearance, you’ll receive a formal Term Sheet. This is your "green light," detailing the loan amount, interest rate, points, and draw schedule. Review this carefully to ensure the financing structure matches your projected ROI.

Step 6: Title & Closing Preparation

With the terms accepted, the lender coordinates with the title company to ensure the property has a clear title. You’ll receive a Closing Disclosure (CD) at least three business days before the finish line, outlining every penny of the final costs so there are no surprises at the table.

Step 7: Closing and Funding

Sign the final documents—often available via mobile notary for your convenience. Once the documents are recorded, funds are disbursed (typically within 24–48 hours). For rehab projects, your renovation funds are held in escrow and released via a draw schedule as you hit your project milestones.

Timeline from Application to Funding

Understanding the typical timeline helps you plan your investment strategy and coordinate with sellers, contractors, and other parties involved in your transaction.

Days 1-2: Application and Initial Review

Submit your complete application with all supporting documents. The loan officer conducts an initial review and may request additional information or clarification on specific items. Quick response to any requests keeps your application moving forward.

Days 3-7: Property Valuation

The property inspection and appraisal occur during this window. Florida properties may require additional time if surveys need to be ordered or if the property is subject to milestone inspection requirements under the Florida Condo Rule.

Days 5-10: Underwriting and Approval

The underwriting team completes their analysis and issues a loan decision. Approved applications receive a formal term sheet with final loan terms. This phase may extend slightly for complex properties or first-time borrowers requiring additional documentation.

Days 10-14: Closing Preparation

Title work is completed, closing documents are prepared, and all parties coordinate for the closing appointment. In Florida, ensuring compliance with survey requirements and obtaining appropriate insurance policies (including windstorm coverage) is essential during this phase.

Days 14-21: Closing and Funding

The typical hard money loan closes within 14-21 days from application, though experienced investors with straightforward deals can sometimes close in as little as 7-15 days. Funding occurs within 1-2 business days after closing documents are signed and recorded.

This accelerated timeline compared to conventional financing (which typically takes 30-60 days) provides a significant competitive advantage when making offers on Florida investment properties, especially in hot markets where sellers prefer quick closings.

Take Action on Your Florida Investment Today

Ready to secure financing for your Florida real estate investment? Get your instant quote from OfferMarket to see your personalized loan terms, interest rates, and monthly payments based on your specific project. The quote process takes just minutes and provides you with the information needed to move forward confidently with your investment.

The Florida real estate market moves quickly, and having your financing lined up gives you a significant competitive advantage. Whether you're pursuing your first fix-and-flip or you're an experienced investor expanding your portfolio, OfferMarket's streamlined application process and fast funding timelines help you capitalize on opportunities when they arise.

OfferMarket Loans

Check your rate

60 seconds · no credit pull