*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

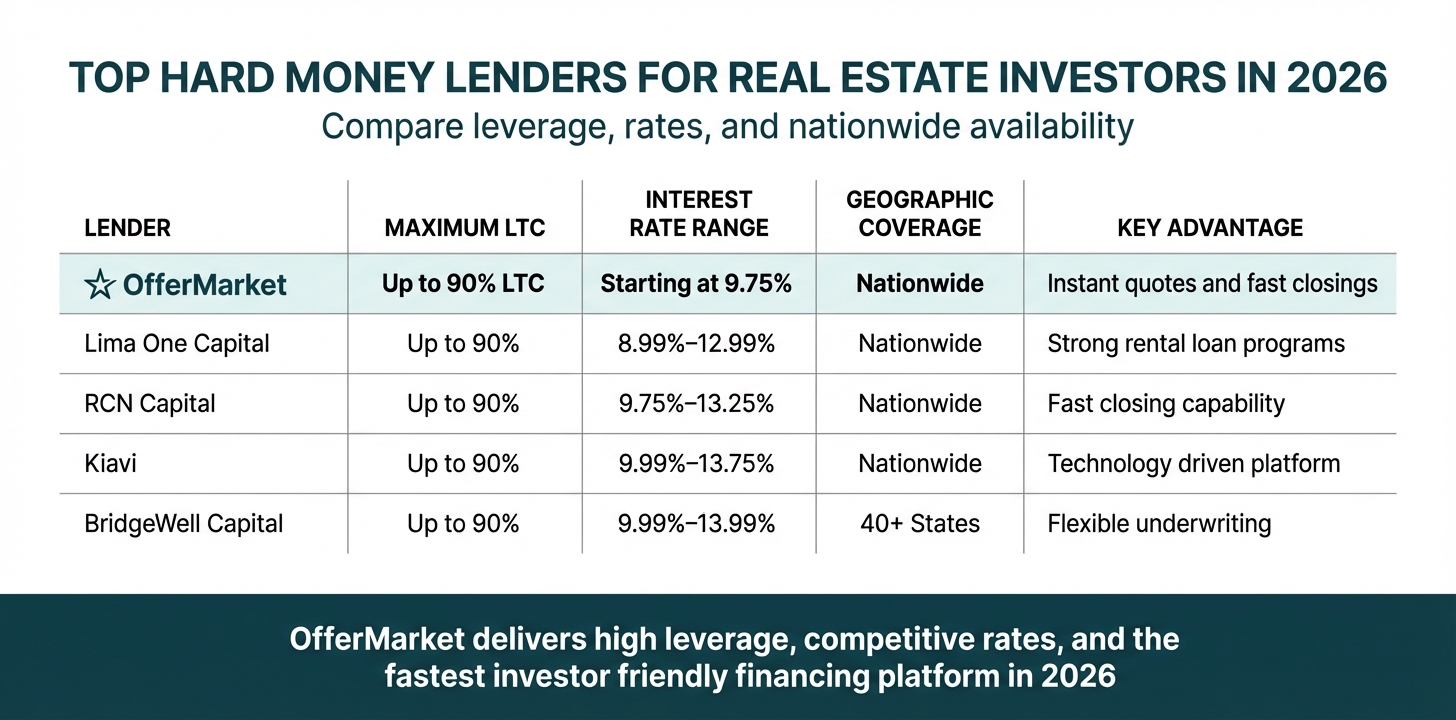

Top Hard Money Lenders for Real Estate Investors

Choosing the right hard money lender is a critical decision that can significantly impact the profitability and timeline of your real estate investment projects. The best lenders offer a combination of speed, transparency, competitive terms, and technology-driven efficiency. While many lenders exist, they are not created equal. Below is a detailed review of the top hard money lenders in the industry, starting with OfferMarket, to help you identify the partner that best aligns with your investment strategy.

1. OfferMarket

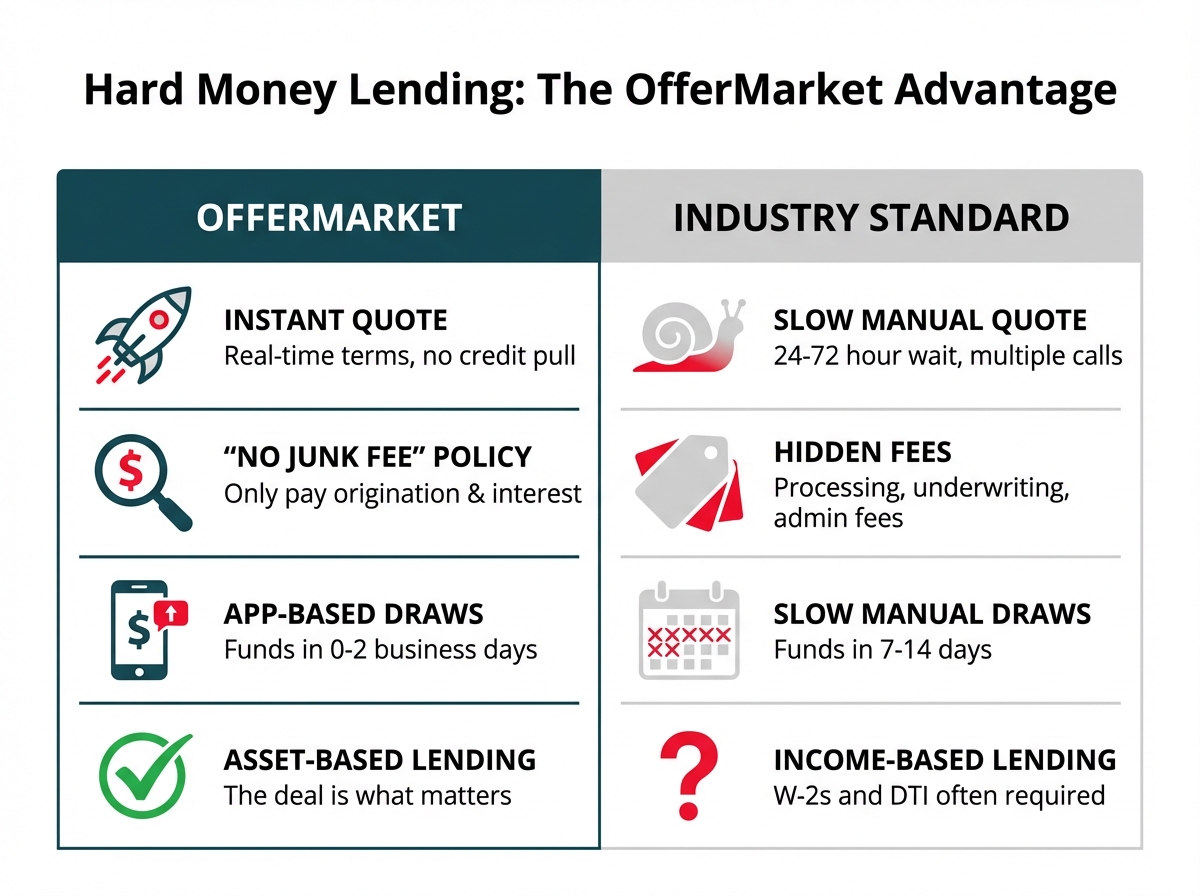

OfferMarket has established itself as a top-tier hard money lender by building its platform around the core needs of modern real estate investors: speed, transparency, and flexibility. Their technology-first approach streamlines every step of the lending process, from initial deal analysis to the final renovation draw.

Instant Quote Technology: One of OfferMarket's most significant advantages is its Instant Quote tool. This allows investors to enter property details and get a real-time, accurate term sheet without a credit pull or the need to speak with a loan officer. This empowers investors to analyze deals and make offers with confidence, knowing their financing terms upfront. This speed is a massive competitive advantage in hot real estate markets where deals can be lost in hours, not days.

Transparent "No Junk Fee" Policy: Many lenders in the hard money space attract borrowers with low advertised rates, only to add on a variety of "junk fees" at closing. These can include processing fees, underwriting fees, administrative fees, and document preparation fees, which can add thousands of dollars to an investor's closing costs. OfferMarket has a strict "No Junk Fee" policy. The costs are simple and transparent: an origination fee and the interest rate. This straightforward approach saves investors money and eliminates unpleasant surprises at the closing table.

Flexible Product Suite: OfferMarket caters to the most popular real estate investment strategies with a robust suite of loan products.

Fix and Flip Loans: Designed for investors purchasing and renovating properties to sell, these loans cover up to 90% of the purchase price and 100% of the rehab costs, ensuring investors can keep more of their capital liquid for other opportunities.

DSCR Loans: Ideal for investors using the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) method or acquiring turnkey rental properties. These loans qualify based on the property's cash flow (Debt Service Coverage Ratio) rather than the borrower's personal income, making them perfect for self-employed investors and those scaling large portfolios.

Streamlined, App-Based Draw Process: Managing renovation funds is one of the most critical parts of a fix and flip project. Delays in receiving draw funds can halt construction, increase holding costs, and derail a project's timeline. OfferMarket has modernized this process with an app-based, self-serve draw request system. Investors can submit photo and video evidence of completed work directly through the app, triggering a virtual inspection. This eliminates the need to schedule and wait for a third-party inspector, allowing for the release of funds in as little as 0-2 business days—a stark contrast to the industry standard of one to two weeks.

2. Park Place Finance

Park Place Finance is a direct hard money lender known for its focus on providing financing solutions for a wide range of property types, including residential, multi-family, and commercial. They pride themselves on flexibility and the ability to fund complex deals that may not fit into the rigid boxes of other lenders. They are often a good choice for experienced investors with unique projects.

3. Lima One Capital

Lima One Capital is one of the larger and more established names in the private lending space. They offer a broad spectrum of loan products, including fix and flip, rental, and multifamily financing. Their strengths lie in their institutional scale, which allows them to offer competitive rates and terms, particularly for experienced investors with a strong track record. They have a national presence and a well-defined process, which can be appealing for borrowers who value structure and predictability.

4. New Silver

New Silver is a technology-focused lender that, similar to OfferMarket, leverages software to streamline the lending process. They are known for their "FlipScout" tool, which helps investors analyze potential deals. They offer fast funding for fix and flips, rentals, and ground-up construction, with an emphasis on making the application and approval process as quick and painless as possible through their online platform.

5. BridgeWell Capital

BridgeWell Capital has been in the hard money industry for over 30 years, giving them a deep well of experience. They offer loans for residential and commercial properties and are known for their customer service and willingness to work with borrowers on a case-by-case basis. They are a good option for investors who prefer a more traditional, relationship-based lending experience.

6. We Lend

We Lend is a national hard money lender that focuses on providing financing for non-owner-occupied residential properties. They are known for their aggressive leverage, often lending up to 90% of the purchase price and 100% of the rehab costs for qualified borrowers. Their focus is squarely on the fix and flip and BRRRR investor communities.

7. LendingOne

LendingOne is another large, national private lender offering a comprehensive suite of products for real estate investors. They provide financing for fix and flips, rental properties, and multi-family units. A key differentiator for LendingOne is their rental property loan program, which is designed for investors looking to build a long-term portfolio. They offer competitive 30-year fixed-rate terms for stabilized properties.

8. Fund That Flip

As their name suggests, Fund That Flip specializes in providing short-term residential bridge loans for fix and flip projects. They operate on a crowdfunding model, where accredited investors can invest in the loans originated by the company. For borrowers, this means access to a reliable source of capital with a focus on speed and efficiency. They have a strong reputation for transparency and excellent customer service.

9. RCN Capital

RCN Capital is a major national direct lender that provides financing for a wide array of non-owner-occupied residential and commercial real estate projects. They are known for their robust product line, which includes short-term fix and flip loans, long-term rental loans, and financing for multi-family and mixed-use properties. Their ability to handle both simple and complex transactions makes them a versatile choice for investors at all levels.

10. Rehab Financial Group

Rehab Financial Group (RFG) carves out a niche by focusing specifically on financing the rehab portion of a project. They are known for providing 100% of the purchase and rehab costs, up to 70% of the ARV, which is particularly appealing for investors who want to minimize their out-of-pocket cash requirements. They also do not require appraisals for some of their loan products, which can speed up the closing process.

11. Griffin Funding

Griffin Funding offers a diverse range of mortgage products, including hard money loans alongside more traditional options like VA and conventional loans. Their hard money program is geared towards real estate investors and business owners who need fast access to capital. They can fund a variety of property types, including residential, multi-family, and commercial. Their broader mortgage expertise can be beneficial for investors who may have other financing needs.

12. Easy Street Capital

Easy Street Capital is a direct private lender with a strong focus on providing financing solutions for rental property investors. While they offer bridge loans for fix and flip projects, their flagship products are their long-term DSCR rental loans. They are known for their innovative and flexible rental loan programs, which include options for short-term rentals (like Airbnb), multi-family properties, and large portfolios.

13. Kiavi

Kiavi (formerly Lending Home) is one of the largest and most technologically advanced hard money lenders in the nation. They have funded tens of thousands of loans and have a highly refined online platform that makes the application and loan management process incredibly smooth. They offer competitive rates for fix and flip and rental loans, and their scale allows them to provide a high degree of certainty of execution for borrowers.

14. Private Lender Link

Private Lender Link is not a direct lender, but rather a platform or marketplace that connects borrowers with a network of direct private and hard money lenders. It can be a useful resource for investors to see multiple loan offers by filling out a single application, especially for those with unique or hard-to-place deals. However, the experience can vary greatly depending on the specific lender you are matched with.

Key Underwriting Characteristics of Hard Money Lenders

Hard money lending operates on a fundamentally different set of principles than traditional banking. While a conventional mortgage from a bank is primarily underwritten based on your personal financial health (income, credit score, tax returns), hard money lenders focus almost exclusively on the quality of the real estate deal itself. Understanding these core underwriting characteristics is crucial for successfully securing financing.

Asset-Based Qualification

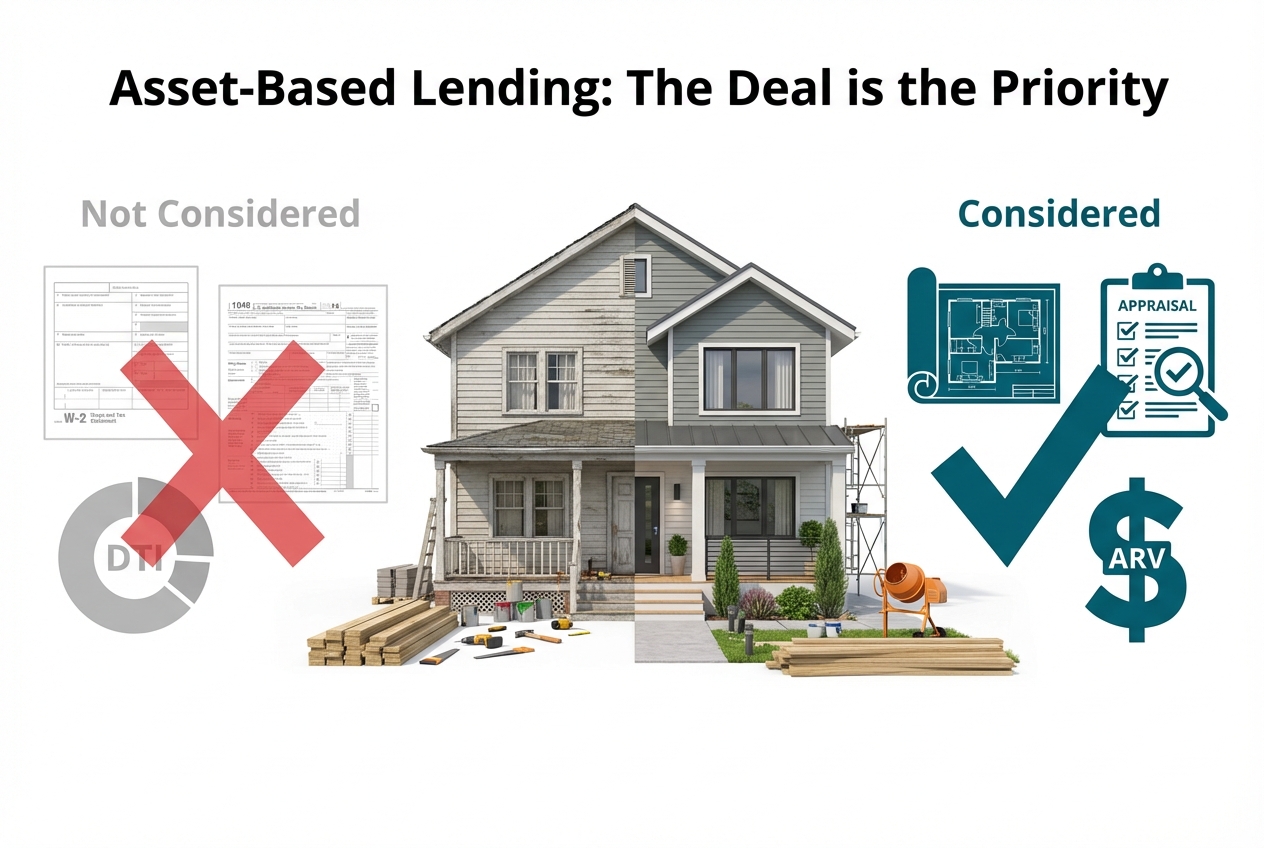

The single most important concept in hard money lending is that the property is the borrower. Lenders are primarily concerned with the viability and profitability of the real estate asset, not your personal income.

The Deal's Profitability is Paramount: A hard money lender's first question will always be about the numbers of the deal. What is the purchase price? What is the renovation budget? And most importantly, what is the After Repair Value (ARV)? Their entire risk assessment is based on the spread between their loan amount and the value of the stabilized property. This is why W-2s and tax returns are generally not required. An investor could have a low personal income but if they bring a deal with a projected 30% profit margin to the table, the lender will be interested. The property's ability to generate profit and cover the debt is what secures the loan.

The Critical Role of the Appraisal and Scope of Work: The lender verifies the deal's profitability through two key documents. The first is a detailed Scope of Work (SOW), which outlines every planned renovation, from paint and flooring to kitchen and bath remodels, with associated costs. The second is a third-party appraisal. The appraiser will determine two values: the "as-is" value of the property and the "After Repair Value" (ARV), which is a professional opinion of the property's market value after the renovations detailed in the SOW are completed. The ARV is the most critical number in hard money underwriting, as it determines the maximum loan amount the lender is willing to offer.

Why Personal Debt-to-Income (DTI) is Not a Factor: In conventional lending, your Debt-to-Income ratio is a make-or-break metric. Banks need to ensure your personal income can support your existing debts plus the new mortgage. Hard money lenders, particularly for short-term fix and flip loans, do not factor in DTI. They assume the property will either be sold (paying off the loan) or refinanced into a long-term rental loan (where the property's rent, not your personal income, will cover the new mortgage). This asset-based approach opens the door for full-time real estate investors, entrepreneurs, and those with fluctuating or hard-to-document income to secure financing.

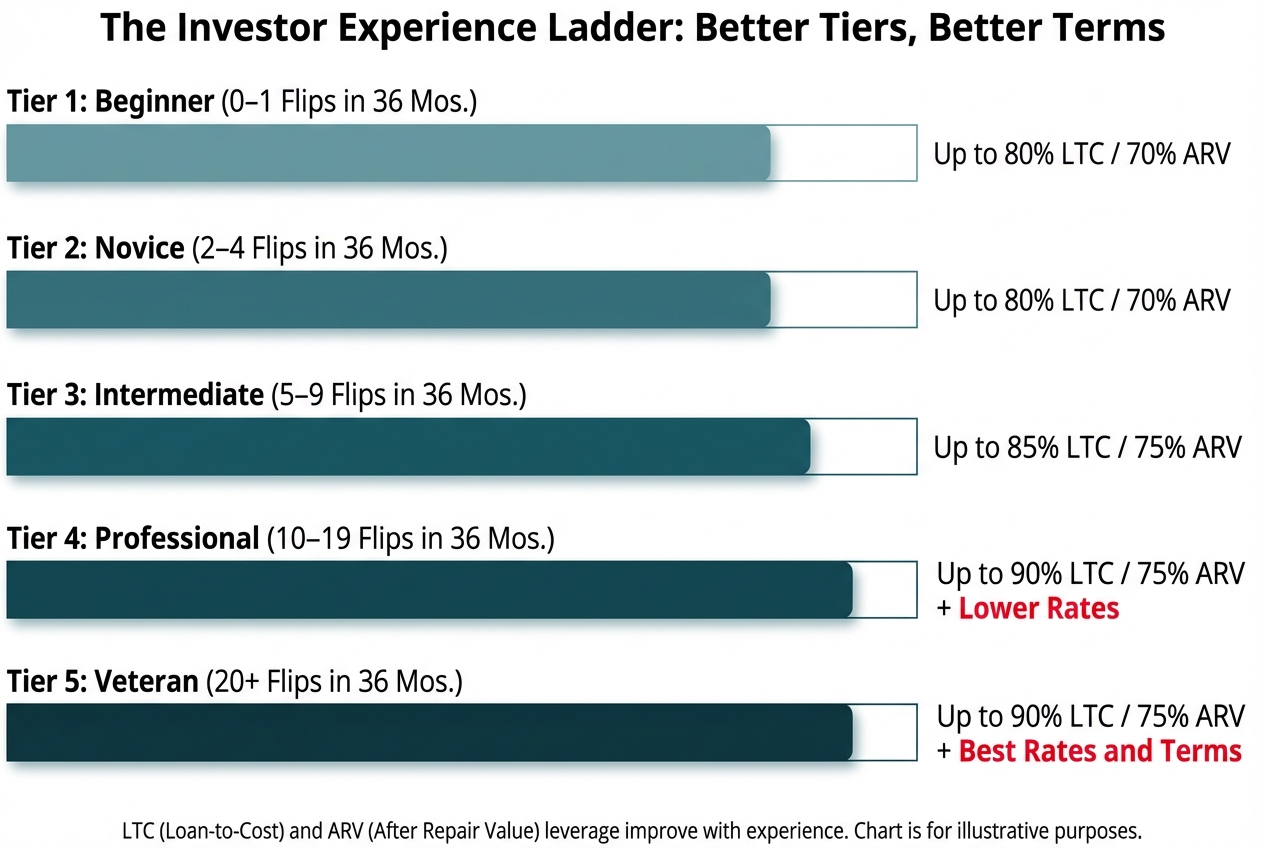

The Investor Experience Tier System

Hard money lenders mitigate risk by evaluating not just the deal, but also the investor's track record. Most sophisticated lenders use an internal tier system to categorize borrowers based on their experience. This tier placement directly impacts the loan terms you'll be offered, including leverage (LTV/LTC), interest rates, and the size of the rehab budget they are willing to finance.

How Lenders Categorize Borrowers: While the exact criteria can vary, the tier system generally looks like this:

Tier 1 (Beginner): 0-1 completed projects in the last 36 months. These are new investors. Lenders will scrutinize their deal more carefully and may require them to have a mentor or experienced contractor on their team.

Tier 2 (Novice): 2-4 completed projects in the last 36 months. These investors have some experience but are still building their track record.

Tier 3 (Intermediate): 5-9 completed projects in the last 36 months. These are considered experienced investors who have a proven system for finding, renovating, and exiting deals.

Tier 4 (Professional): 10-19 completed projects in the last 36 months. These investors are operating a full-fledged real estate investment business.

Tier 5 (Veteran): 20+ completed projects in the last 36 months. These are elite-level investors, often managing multiple projects simultaneously.

The Impact of Your Track Record: Your tier directly affects your financing. A Tier 1 investor might be offered 85% of the purchase price and 100% of the rehab, with a maximum loan-to-ARV of 70%. In contrast, a Tier 4 or 5 investor might qualify for 90% of the purchase price, 100% of the rehab, and a higher loan-to-ARV of 75%. Furthermore, experienced investors typically receive lower interest rates and origination fees because the lender views them as a lower risk. They have proven they can execute a business plan and deliver a profitable project on time and on budget.

Defining an "Experienced" Investor: The key phrase is "in the last 3 years" (or 36 months). A deal you completed five years ago, while valuable experience for you, likely won't count towards your tier status. Lenders want to see recent and relevant experience. They are underwriting your ability to perform in the current market conditions. To prove your experience, you will need to provide the closing statements (HUD-1s or ALTA statements) for the properties you have bought and sold within that timeframe.

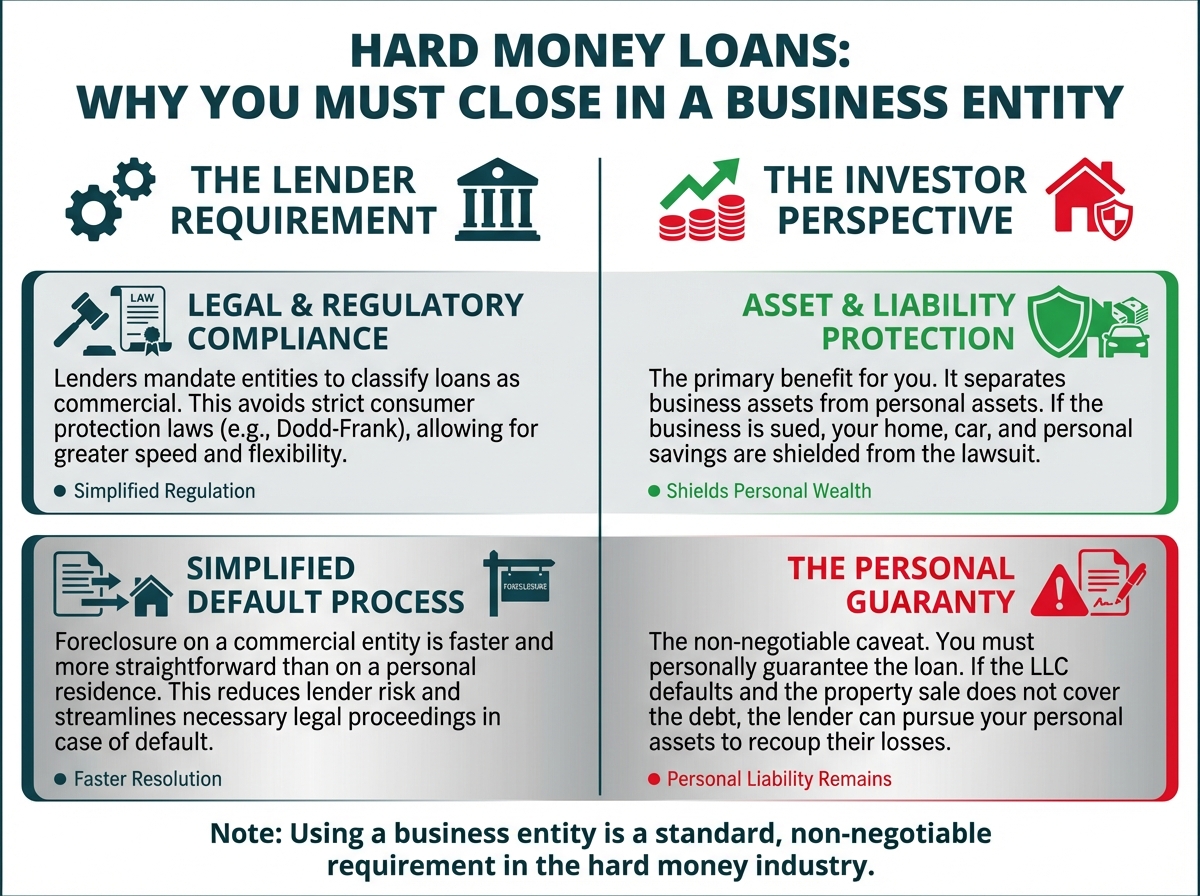

Entity Vesting and Personal Guaranties

When you get a hard money loan, you won't be closing in your personal name. Lenders universally require borrowers to take title to the property in the name of a business entity, typically a Limited Liability Company (LLC) or a corporation.

The Requirement to Close in a Business Entity: Lenders mandate the use of an entity for several key legal and regulatory reasons. Loans made to business entities for a commercial purpose (like a fix and flip) are generally not subject to the same stringent consumer protection regulations (like Dodd-Frank) as loans made to individuals for personal use. This allows lenders to operate with more speed and flexibility. It also simplifies the foreclosure process for the lender in the unfortunate event of a default, as it's a commercial rather than a consumer foreclosure.

Benefits of Entity Vesting for the Investor: While it's a lender requirement, using an entity is also a best practice that offers significant protection for you, the investor. The primary benefit is liability protection. By holding the property in an LLC, you separate your business assets from your personal assets. If someone were to be injured on the property and sue, they would sue the LLC. Your personal assets, such as your primary home, cars, and savings, would be shielded from the lawsuit. It also helps with accounting and professionalism, as you can run all project income and expenses through a dedicated business bank account.

Understanding the Standard Requirement for a Personal Guaranty: A common point of confusion for new investors is the personal guaranty. Even though the loan is made to your LLC, the lender will still require all owners of the LLC (typically anyone with 20-25% or more ownership) to sign a personal guaranty. This is a legal agreement stating that if the LLC defaults on the loan and the sale of the property does not cover the outstanding debt, the lender can pursue your personal assets to recoup their losses. This may seem counterintuitive to the asset protection of an LLC, but it is a standard, non-negotiable requirement in the hard money industry. It ensures that the investor has "skin in the game" and is personally committed to the success of the project.

Understanding the Costs, Fees, and Requirements

Beyond the core underwriting principles, it's essential to have a firm grasp of the specific costs, fees, and borrower requirements associated with hard money loans. These financial details will directly impact your project's budget, profitability, and your ability to qualify for the loan in the first place.

Rates and Origination Fees

The two primary costs of a hard money loan are the interest rate and the origination fees (often called "points").

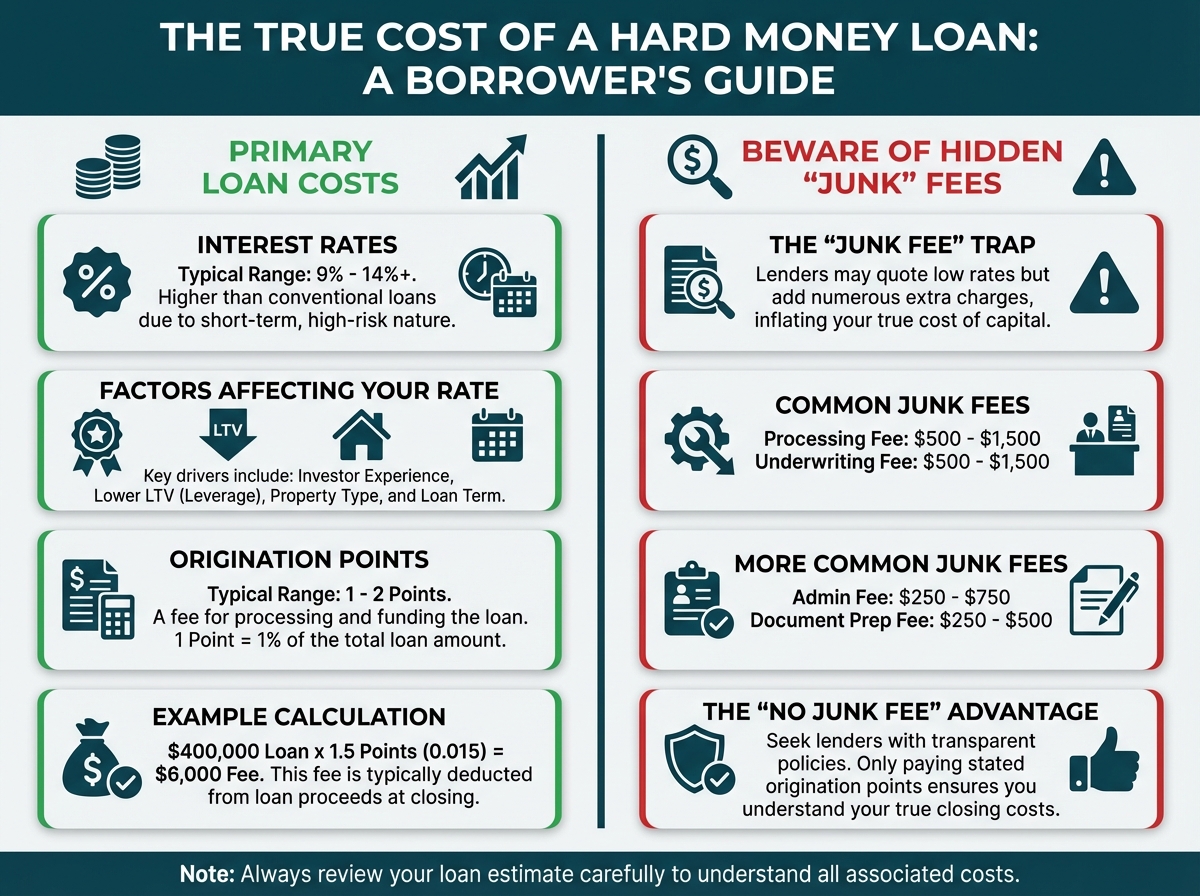

Typical Interest Rate Ranges: Hard money interest rates are higher than conventional mortgages because the loans are shorter-term, higher-risk, and funded by private capital. As of today, you can expect interest rates to range from 9% to 14% or higher. The specific rate you receive depends on several factors:

Your Experience: As discussed in the tier system, more experienced investors receive lower rates.

Leverage: A lower LTV (meaning you're putting more of your own cash down) will often result in a lower interest rate.

Property Type: A standard single-family home is less risky and will have a lower rate than a unique property or a commercial building.

Loan Term: Shorter loan terms may sometimes have slightly different rates than longer ones.

Defining Origination Points: An origination fee, or "point," is a fee charged by the lender to cover the costs of processing, underwriting, and funding the loan. One point is equal to 1% of the total loan amount. Most hard money lenders charge between 1 to 2 points.

- Example Calculation: If you are taking out a $400,000 hard money loan and the lender charges 1.5 points, your origination fee would be 6,000(400,000 × 0.015). On a refinance, this fee is typically deducted directly from your loan proceeds. On a purchase, it is added to the total cash-to-close you must bring to the settlement table.

The "No Junk Fee" Advantage: This is where investors need to be vigilant. Many lenders will quote a low rate and a 1-point origination fee, but the loan estimate will be littered with additional charges. These are often called "junk fees" and can include:

Processing Fee: $500 - $1,500

Underwriting Fee: $500 - $1,500

Admin Fee: $250 - $750

Document Prep Fee: $250 - $500

These can quickly add up to thousands of dollars, effectively increasing your true cost of capital. Lenders like OfferMarket with a transparent No Junk Fee policy only charge the stated origination points. This makes it much easier to compare loan offers and understand your true closing costs.

Liquidity and Reserve Requirements

Lenders need to know that you have enough cash on hand to handle the financial demands of the project beyond the loan itself. This is verified by checking your "liquidity" and ensuring you meet their "reserve" requirements. Liquidity refers to cash or assets that can be quickly converted to cash, such as funds in checking/savings accounts, brokerage accounts, or vested retirement funds (like a 401k, though lenders may only count 50-60% of the vested value).

Proving Liquid Cash: You will be required to provide recent bank or financial statements to prove you have sufficient funds for three key things:

The Down Payment: The portion of the purchase price not covered by the loan.

Closing Costs: This includes origination points, appraisal fees, title insurance, attorney fees, and prepaid taxes/insurance.

Reserves: Extra cash set aside to cover unforeseen expenses and loan payments.

Fix & Flip Interest Reserves: For a fix and flip loan, the lender knows you won't have rental income to cover the monthly payments during the renovation. Therefore, they require you to have "interest reserves." This is typically 3 to 6 months' worth of the estimated monthly interest payments held in your bank account. They want to see that if your project takes a few months longer than expected, you can still make your loan payments without financial distress.

DSCR PITIA Reserves: For a long-term DSCR rental loan, the reserve requirement is calculated differently. Lenders will require you to have a certain number of months' worth of *PITIA* in reserves. PITIA stands for:

Principal

Interest

Taxes (property taxes)

Association Dues (if applicable)

A common requirement is 6 months of PITIA reserves. For example, if the total monthly PITIA payment for your new rental property is $2,000, the lender would require you to show at least $12,000 ($2,000 x 6) in liquid reserves in your bank account at the time of closing. This ensures you can cover the mortgage and other property expenses during a potential vacancy or if a tenant fails to pay rent.

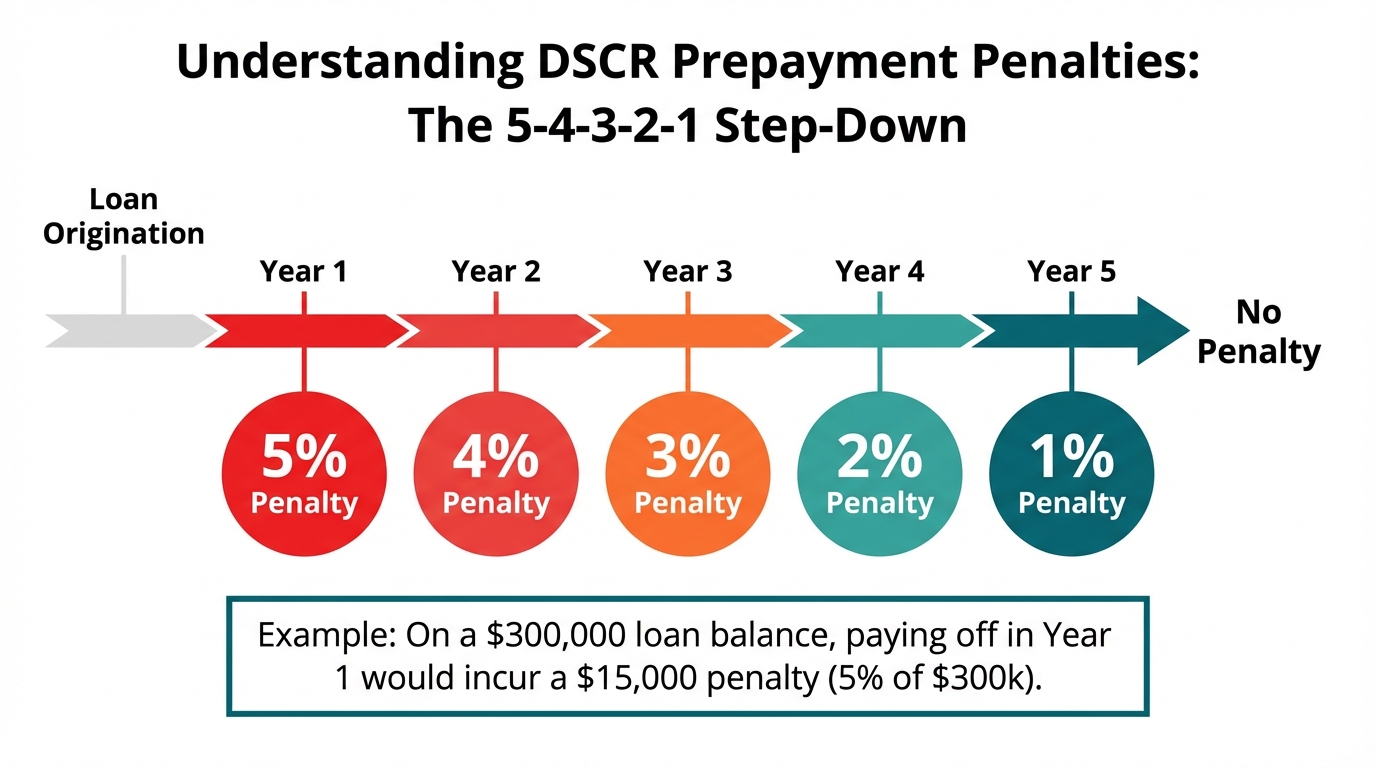

Prepayment Penalties on DSCR Loans

While short-term fix and flip loans typically do not have prepayment penalties (they are designed to be paid off quickly), they are a standard feature on long-term DSCR rental loans. A prepayment penalty is a fee the lender charges if you pay off the loan within a specified period, usually the first 1 to 5 years.

How Step-Down Structures Work: The most common prepayment penalty structure is a "step-down" model, such as 5-4-3-2-1. This means:

If you sell or refinance the property in Year 1, you pay a penalty equal to 5% of the outstanding loan balance.

If you pay it off in Year 2, the penalty is 4%.

Year 3: 3%

Year 4: 2%

Year 5: 1%

After 5 years, there is no penalty.

Some lenders may offer a 3-year (3-2-1) or other variations. Generally, a loan with a shorter prepayment penalty period will have a slightly higher interest rate, and vice versa.

The Lender's Rationale: The reason for these penalties is tied to the secondary market. Lenders often package and sell these long-term DSCR loans to larger institutional investors (like insurance companies or pension funds) who are seeking a stable, long-term return. The prepayment penalty guarantees that these investors will receive their expected yield for a certain period. If the loan is paid off too early, the penalty compensates the investor for the loss of future interest payments.

State-Specific Limitations: It's important to be aware that some states have specific laws that limit or even prohibit prepayment penalties on residential investment properties. For example, states like Illinois and New Jersey have regulations that can affect how these penalties are applied. It is crucial for investors to consult with a local real estate attorney and carefully read their loan documents to understand the specific prepayment penalty terms and how they comply with local state laws.

The Step-by-Step Process of Securing a Hard Money Loan Through OfferMarket

Securing a hard money loan is designed to be a much faster and more streamlined process than obtaining a conventional mortgage. While specific steps can vary slightly between lenders, the overall journey from deal analysis to closing and renovation follows a consistent path.

Step 1: Get Your Instant Quote

This is the initial phase where you vet a potential investment property and determine if the financing makes sense. Speed is of the essence here, as you often need to make an offer quickly.

Head over to OfferMarket's loan application page and enter your deal details, where we ask a few multiple choice questions such as:

- Your investment experience (number of flips/rentals in the last 36 months)

- Estimated credit score (no credit pull)

- Borrowing entity (Personal name or LLC)

- Portfolio loan (i.e. for multiple properties)

- Property type

- Unit size

- Subject property address

- Loan Purpose

- Estimated as-is value

- Purchase price

- Tenant type

- Leasing strategy

- Monthly rent

- Annual taxes

- Annual insurance

- Annual HOA

- Citizenship status

Within seconds, the platform analyzes the data and provides a detailed term sheet outlining the potential loan amount, interest rate, origination points, and estimated cash-to-close.

- The OfferMarket Advantage: The key benefit of a true instant quote tool is that it provides a real-time, reliable term sheet with no credit pull and no need to talk to a loan officer. This empowers you to run numbers on multiple properties quickly and write offers with confidence, knowing that your financing is already preliminarily lined up. You can attach this term sheet to your offer to show the seller you are a serious, well-funded buyer.

Step 2: Create Your Loan File Application

Once you've reviewed your instant quote and decided to move forward, the next step is straightforward. When you click "SELECT" to continue to the term sheet and pre-approval on your instant quote, OfferMarket automatically creates a personalized Loan File for you. Think of this as your command center for managing your entire loan application.

Your Loan File contains much more detailed information than your initial quote, including:

Preliminary Loan Terms:

- Specific interest rate ranges based on your investor profile

- Detailed breakdown of all estimated fees (origination, processing, underwriting)

- Exact loan-to-value (LTV) and after-repair loan-to-value (ARLTV) ratios

- Draw schedule structure for your renovation budget

- Closing cost estimates

Here's why this matters for your bottom line. Traditional lenders often surprise you with hidden fees at closing. We take a different approach—laying out all costs upfront so you can review every line item, understand exactly what you're paying for, and calculate your true all-in costs before committing.

Your Loan File also serves as your project dashboard throughout the financing process. You can:

- Track the status of your application in real-time

- Upload required documents

- Communicate directly with OfferMarket's processing team

- Receive notifications about next steps and outstanding items

Everything you need lives in one place, organized and accessible 24/7. That's how financing should work.

Step 3-7: Move to Processing & Expedite with Document Uploads

After thoroughly reviewing your preliminary Loan Terms in your Loan File, you're ready to formally begin the underwriting process. This is where you signal your intent to proceed by clicking "Move to processing" within your Loan File. This action lets OfferMarket's team know you're ready to roll and prepared to submit your documentation.

The Document Upload Phase:

Once you're here, head to the "Processing" section of your Loan File where you'll find a clear checklist of urgent section that's what we need from you.

You’ll complete and upload:

- Bank Statements

- ID Verification

- Borrowing Entity Details (LLC/Corp)

- Track Record (Past project history)

- Personal Financial Statement

- Personal guarantor information

- Insurance information (OfferMarket can help with that since we specialize in insurance for Fix and Flip properties)

OfferMarket's Speed Promise: Closing in Under 1-3 Weeks

This is where OfferMarket really shines compared to traditional lenders. Banks? They'll keep you waiting 30 to 60 days. Even some hard money lenders drag things out for weeks. We typically get you to the closing table in under 1-3 weeks. Many of our investors see funding in just 14-21 days from application to keys in hand.

And here's why that matters beyond convenience—it's your edge in competitive markets. When sellers are juggling multiple offers, your ability to close fast can win the deal, even if someone else bids higher. Sellers value certainty and speed, and a three-week close with verified financing beats a 45-day conventional loan closing every time.

Your Role in Expediting the Process:

Here's the deal: OfferMarket's ability to close quickly depends on getting all necessary documents from you right away. Let's break down how the timeline works:

- Days 1-3: Document review and initial underwriting

- Days 4-7: Property valuation, title search, and final underwriting

- Days 8-14: Loan approval and closing document preparation

- Days 14-19: Closing and funding

This timeline holds up when you submit complete, accurate documentation immediately after moving to processing. Every day you delay providing documents adds a day to your closing timeline. Incomplete or unclear documentation can stretch things out even further, since the underwriting team will need to circle back for clarification or additional information.

Pro Tips for Fast Processing:

- Submit everything at once: Instead of uploading documents one at a time, gather everything on the checklist and send it all together

- Ensure clarity and quality: Make sure scanned documents are legible and complete (all pages included)

- Respond immediately: When the processing team asks for additional information or clarification, get back to them within hours, not days

- Stay accessible: Be available by phone and email during business hours for quick questions

- Prepare your contractor: Have your contractor ready to provide additional detail on the scope of work if needed

The difference between a 10-day close and a 20-day close often comes down to document preparation and responsiveness. Investors who treat the document submission phase with urgency consistently close faster, secure better deals, and start generating returns on their investment sooner.

Follow OfferMarket's streamlined seven-step process and stay in close communication throughout. You'll be positioned to move quickly on profitable opportunities and run your fix and flip business at peak efficiency. The platform is designed to work at your pace—but the faster you move, the faster you can get funded and start your project.

Managing Renovation Draws

After you close on the loan and take ownership of the property, the renovation work begins. Your rehab budget is held in an escrow account by the lender and is disbursed to you in "draws" as you complete phases of the work.

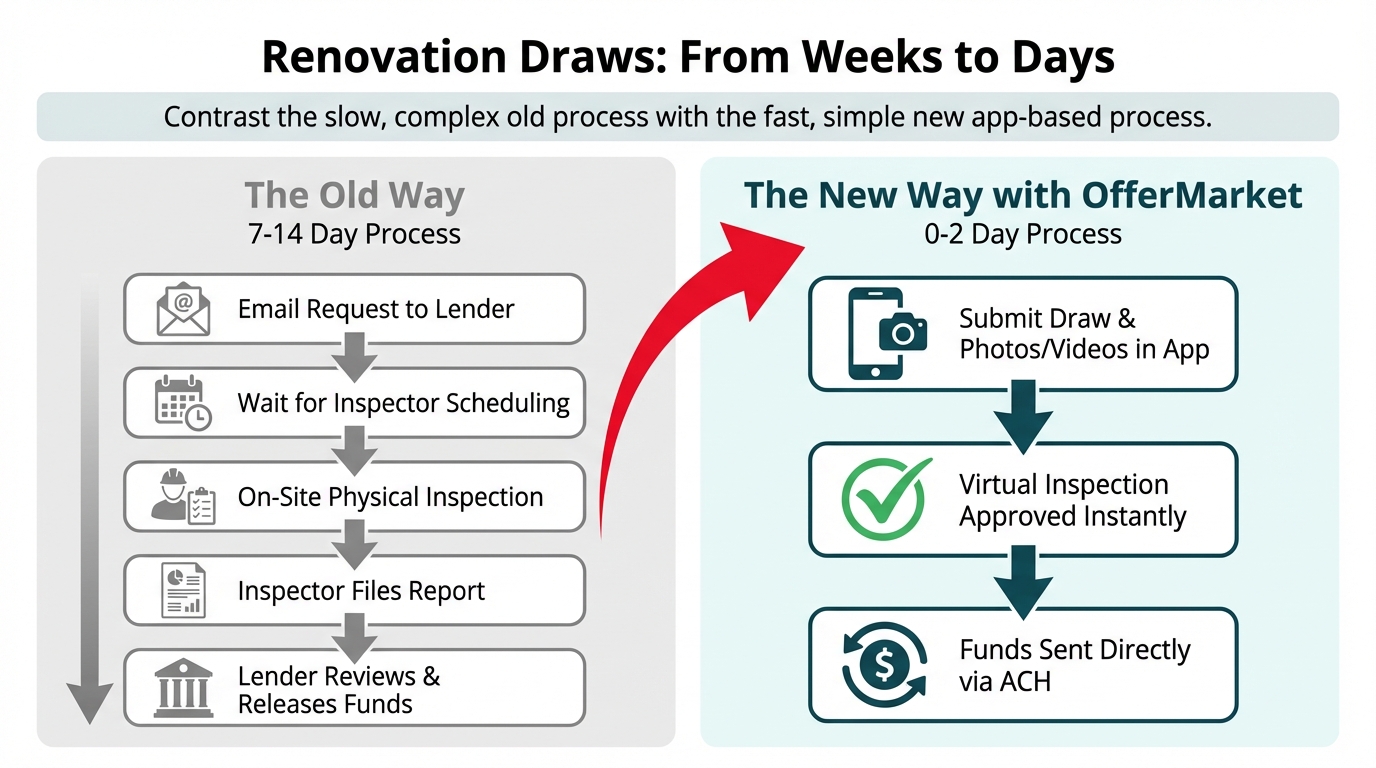

The Process for Requesting Rehab Funds: Traditionally, this has been a slow, cumbersome process. An investor would complete a portion of the work (e.g., demolition and framing), email a request to the lender, and then wait for the lender to schedule a third-party inspector to visit the site. The inspector would then file a report, and only then would the lender release the funds. This cycle could take 7-14 days, causing significant project delays.

Modernizing the Process with App-Based, Self-Serve Inspections: Technology-forward lenders have revolutionized this process. Using a dedicated mobile app, you can walk through the property, take photos and videos of the completed work, and submit your draw request directly from your phone.

OfferMarket's Streamlined Draws for 0-2 Business Day Funding: OfferMarket's platform uses this modern, app-based approach. The virtual inspection eliminates the need for a third-party inspector, dramatically cutting down the timeline. Once your virtual inspection is approved, the funds are sent via ACH transfer directly to your bank account, typically arriving in 0-2 business days. This incredible speed allows you to pay your contractors immediately, keep your project momentum high, and ultimately finish your rehab faster and more efficiently.

Conclusion: Finance Your Next Deal with Confidence

Hard money lending is an indispensable tool for the modern real estate investor. It provides the speed and leverage necessary to acquire and renovate properties, whether for a quick flip or as part of a long-term rental portfolio strategy. The traditional barriers of income verification and slow processing times are replaced by a focus on the quality of the asset, empowering investors to scale their businesses based on their ability to find profitable deals.

However, the success of your projects often hinges on the quality of your lending partner. Choosing a lender that prioritizes speed, transparency, and technological efficiency is paramount. A partner who can provide instant terms, eliminate costly junk fees, and deliver renovation funds in days instead of weeks becomes a true competitive advantage. By understanding the underwriting process, the associated costs, and the step-by-step journey, you can approach your next investment with the knowledge and confidence needed to succeed.

Ready to see how a modern hard money lender can transform your real estate investing? Get a transparent, real-time term sheet for your next deal in under 60 seconds.

Get Your Instant Quote from OfferMarket

Want to analyze the numbers on a potential project? Use our free calculator to estimate your costs and potential profits.

OfferMarket Loans

Check your rate

60 seconds · no credit pull