*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

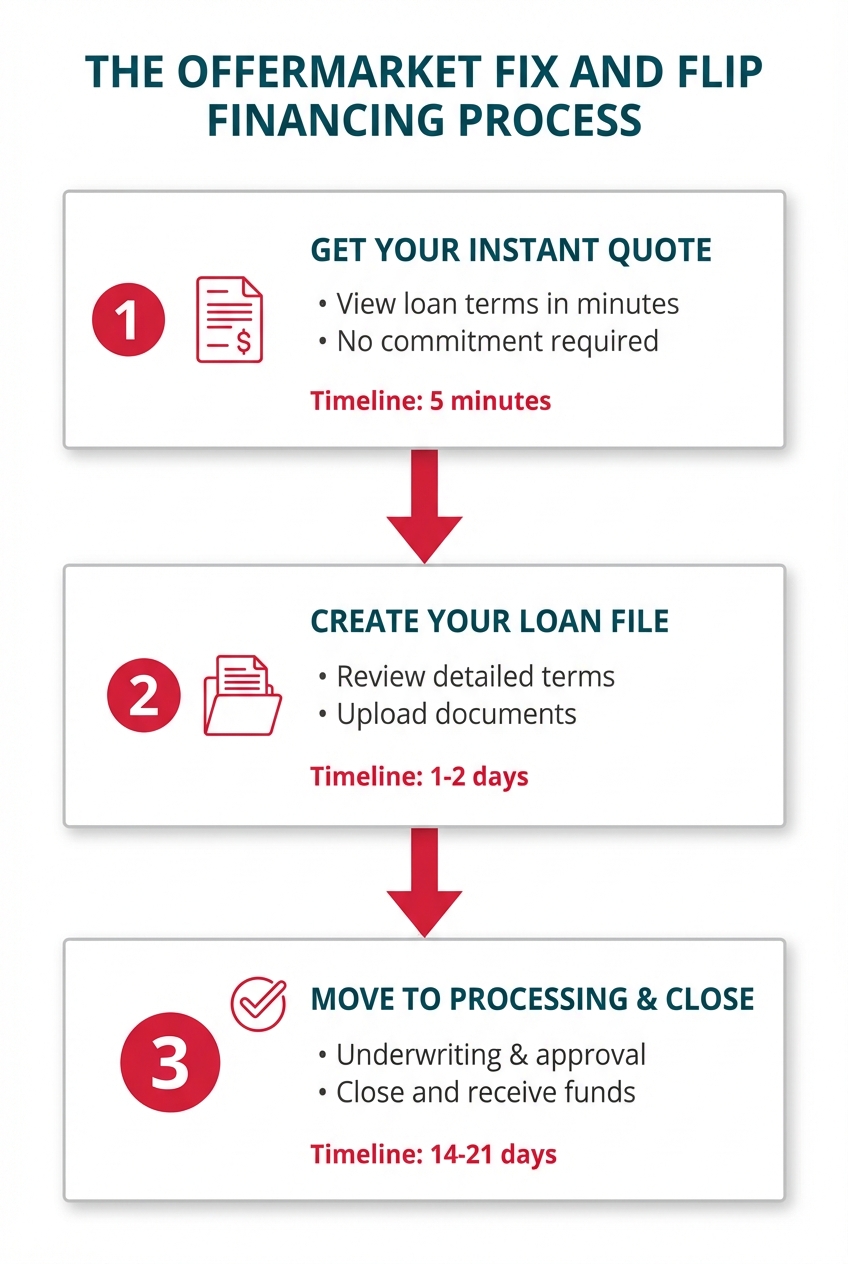

The OfferMarket Fix and Flip Financing: From Instant Quote to Close

Getting your fix and flip project financed shouldn't feel like a maze. OfferMarket has simplified the entire process into three straightforward steps that can take you from first click to funded loan in under two to three weeks. In competitive markets where great properties disappear fast, that speed can be the difference between landing a winner and watching it slip away.

Step 1: Get Your Instant Quote – The Starting Line for Your Project

Head over to OfferMarket's loan application page and enter your deal details, where we ask a few multiple choice questions such as:

- Your investment experience (number of flips/rentals in the last 36 months)

- Estimated credit score (no credit pull)

- Borrowing entity (Personal name or LLC)

- Portfolio loan (i.e. for multiple properties)

- Property type

- Unit size

- Subject property address

- Loan Purpose

- Estimated as-is value

- Purchase price

- Tenant type

- Leasing strategy

- Monthly rent

- Annual taxes

- Annual insurance

- Annual HOA

- Citizenship status

Everything starts with OfferMarket's instant quote tool—your go-to resource for immediate clarity on financing options, no strings attached. In just minutes, you'll see:

- Potential fix and flip loan terms customized to your specific project

- Estimated interest rates based on your experience level and property details

- Projected monthly payments so you can nail down your carrying costs

- Maximum loan amounts for both acquisition and renovation

Here's what makes this tool so valuable: you don't need a mountain of paperwork or days of waiting. Just a few details, and you've got a clear picture of your financing landscape. That means you can quickly decide if a deal pencils out before investing more time.

The Savvy Investor's Strategy: Smart real estate investors know that winning at fix and flip comes down to speed and sharp deal analysis. The pros don't stop at one quote—they pull instant quotes regularly as new properties pop up. This habit helps them:

- Size up deals fast and spot profitability before making offers

- Weigh financing options across multiple properties

- Submit competitive offers backed by solid financing knowledge

- Build a steady pipeline of pre-vetted opportunities

Think of instant quotes as your first checkpoint in evaluating any deal. Before you spend time on detailed property inspections or extensive due diligence, you can confirm that the financing works for your investment strategy.

Step 2: Create Your Loan File – Detailing Your Project

Once you've reviewed your instant quote and decided to move forward, the next step is straightforward. When you click "SELECT" to continue to the term sheet and pre-approval on your instant quote, OfferMarket automatically creates a personalized Loan File for you. Think of this as your command center for managing your entire loan application.

Your Loan File contains much more detailed information than your initial quote, including:

Preliminary Loan Terms:

- Specific interest rate ranges based on your investor profile

- Detailed breakdown of all estimated fees (origination, processing, underwriting)

- Exact loan-to-value (LTV) and after-repair loan-to-value (ARLTV) ratios

- Draw schedule structure for your renovation budget

- Closing cost estimates

Here's why this matters for your bottom line. Traditional lenders often surprise you with hidden fees at closing. We take a different approach—laying out all costs upfront so you can review every line item, understand exactly what you're paying for, and calculate your true all-in costs before committing.

Your Loan File also serves as your project dashboard throughout the financing process. You can:

- Track the status of your application in real-time

- Upload required documents

- Communicate directly with OfferMarket's processing team

- Receive notifications about next steps and outstanding items

Everything you need lives in one place, organized and accessible 24/7. That's how financing should work.

Step 3-7: Move to Processing & Expedite with Document Uploads

After thoroughly reviewing your preliminary Loan Terms in your Loan File, you're ready to formally begin the underwriting process. This is where you signal your intent to proceed by clicking "Move to processing" within your Loan File. This action lets OfferMarket's team know you're ready to roll and prepared to submit your documentation.

The Document Upload Phase:

Once you're here, head to the "Processing" section of your Loan File where you'll find a clear checklist of urgent section that's what we need from you.

You’ll complete and upload:

- Bank Statements

- ID Verification

- Borrowing Entity Details (LLC/Corp)

- Track Record (Past project history)

- Personal Financial Statement

- Personal guarantor information

- Insurance information (OfferMarket can help with that since we specialize in insurance for Fix and Flip properties)

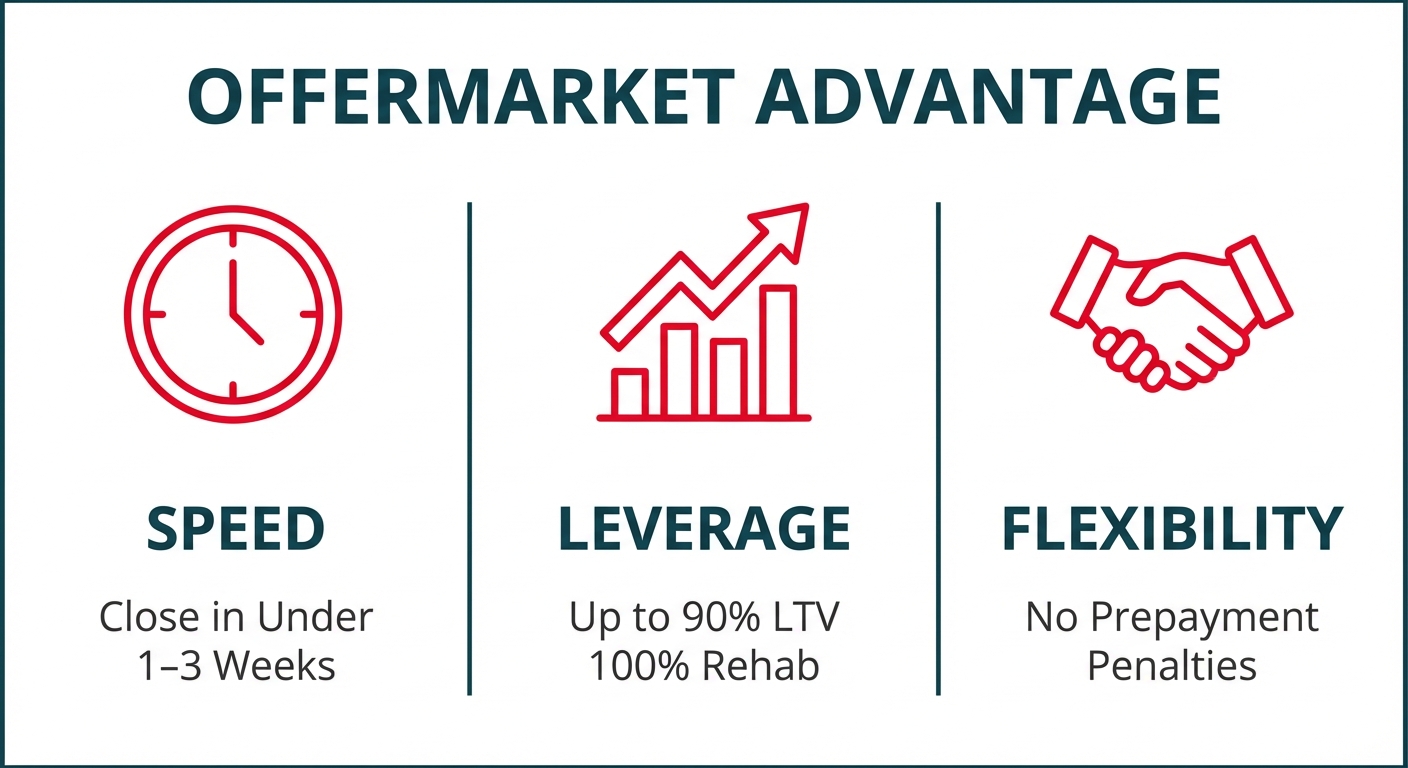

OfferMarket's Speed Promise: Closing in Under 1-3 Weeks

This is where OfferMarket really shines compared to traditional lenders. Banks? They'll keep you waiting 30 to 60 days. Even some hard money lenders drag things out for weeks. We typically get you to the closing table in under 1-3 weeks. Many of our investors see funding in just 14-21 days from application to keys in hand.

And here's why that matters beyond convenience—it's your edge in competitive markets. When sellers are juggling multiple offers, your ability to close fast can win the deal, even if someone else bids higher. Sellers value certainty and speed, and a two-week close with verified financing beats a 45-day conventional loan closing every time.

Your Role in Expediting the Process:

Here's the deal: OfferMarket's ability to close quickly depends on getting all necessary documents from you right away. Let's break down how the timeline works:

- Days 1-3: Document review and initial underwriting

- Days 4-7: Property valuation, title search, and final underwriting

- Days 8-14: Loan approval and closing document preparation

- Days 14-19: Closing and funding

This timeline holds up when you submit complete, accurate documentation immediately after moving to processing. Every day you delay providing documents adds a day to your closing timeline. Incomplete or unclear documentation can stretch things out even further, since the underwriting team will need to circle back for clarification or additional information.

Pro Tips for Fast Processing:

- Submit everything at once: Instead of uploading documents one at a time, gather everything on the checklist and send it all together

- Ensure clarity and quality: Make sure scanned documents are legible and complete (all pages included)

- Respond immediately: When the processing team asks for additional information or clarification, get back to them within hours, not days

- Stay accessible: Be available by phone and email during business hours for quick questions

- Prepare your contractor: Have your contractor ready to provide additional detail on the scope of work if needed

The difference between a 10-day close and a 20-day close often comes down to document preparation and responsiveness. Investors who treat the document submission phase with urgency consistently close faster, secure better deals, and start generating returns on their investment sooner.

Follow OfferMarket's streamlined seven-step process and stay in close communication throughout. You'll be positioned to move quickly on profitable opportunities and run your fix and flip business at peak efficiency. The platform is designed to work at your pace—but the faster you move, the faster you can get funded and start your project.

Why Choose OfferMarket for Your Fix and Flip Financing?

At OfferMarket, we've built our fix and flip financing specifically around the real challenges you face as an investor: tight timelines, cash flow juggling, and the need for smart leverage. Traditional lenders often treat your flip like a standard mortgage—but that's not how this game works. Our loan structure is designed for investors who need to act quickly, keep carrying costs low, and walk away with maximum profit. Let's break down how our financing actually works in your favor.

The Draw Process: Smart Fund Management Through Construction Holdback

When you close on your OfferMarket fix and flip loan, you won't get your full renovation budget upfront. Instead, 100% of your approved renovation funds go into an escrow account controlled by the lender—we call this the construction holdback. This setup protects both sides by releasing funds only as work gets done.

Here's how draws work in practice: As you hit specific milestones in your Scope of Work (SoW)), you submit a draw request to OfferMarket. We verify completion—usually through photos, invoices, or a third-party inspection—and then release funds for that completed work. This staged approach keeps your renovation budget working strategically throughout the project instead of sitting unused or getting spent too early.

What does this mean for you? You'll want to manage your working capital carefully in the early stages. Many experienced flippers keep a reserve fund or line of credit handy to cover initial materials and contractor deposits before that first draw comes through. But here's the good news: this short-term cash flow consideration comes with a major upside—the "as disbursed" interest calculation.

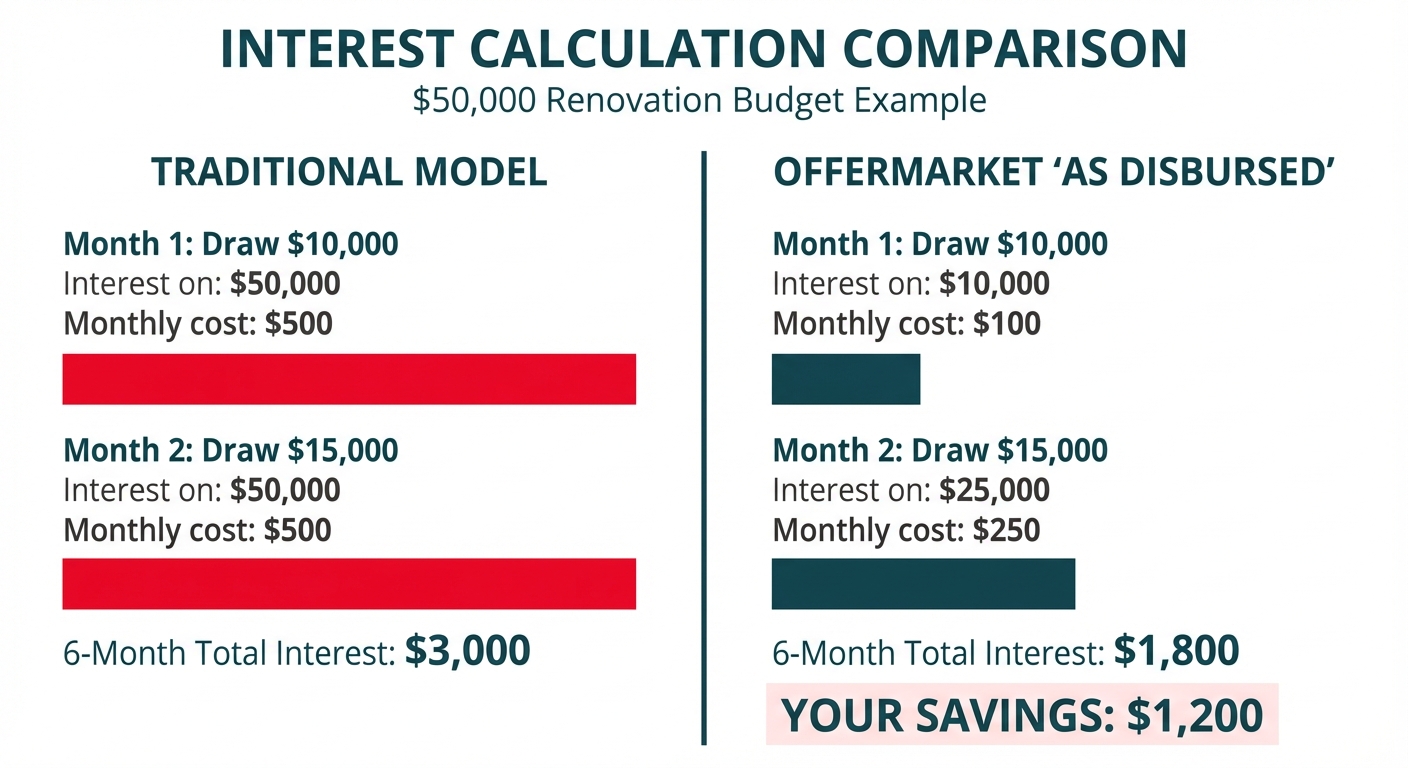

The 'As Disbursed' Interest Advantage: Pay Only for What You Use

For OfferMarket loans of $100,000 or more, interest is typically charged on an "as disbursed" basis—and this is where smart investors see real savings on carrying costs. Unlike loans where you pay interest on the entire renovation budget from day one, the as disbursed model means you only pay interest on renovation funds after they've been drawn and disbursed to you.

Let's break this down with a real-world example: Say you have a $50,000 renovation budget sitting in escrow. In month one, you wrap up demolition and rough framing, then draw $10,000. With the as disbursed model, you're only paying interest on that $10,000—not the full $50,000 waiting in escrow. At a 12% annual interest rate (1% monthly), that's $100 in interest on renovation funds for that first month, compared to $500 if you'd received the entire budget upfront.

Here's why this matters for your wallet: this structure rewards you for running a tight ship. Complete work efficiently and draw funds quickly, and you'll shorten your total interest accrual period. On the flip side, if you strategically pace your renovations and hold off on certain phases, you're not stuck paying interest on money you haven't touched yet. Across a typical 6-9 month flip, this as disbursed approach can put thousands of dollars back in your pocket—straight to your bottom line.

Flexible Terms Built for the Way You Actually Work

OfferMarket designs loan terms around how fix and flip projects really unfold. The standard 12-month term works well for most cosmetic to moderate renovations, covering you from purchase to sale. Tackling something bigger—like a major addition, a complex conversion, or a property in a slower market? Extended terms of 18 to 24 months give you the runway you need.

But here's the game-changer for your profits: OfferMarket charges no prepayment penalties. No minimum interest requirements means you're free to sell and pay off your loan the moment a qualified buyer comes along. For fix and flip investors, this flexibility is huge—because in this business, timing the market right can make all the difference in your returns.

Consider the financial impact: If you complete your renovation in four months and secure a buyer immediately, you can close the sale and pay off your loan without penalty. You'll have paid interest for only those four months (plus any additional time until closing), rather than being locked into paying interest for a minimum period. The faster you execute your flip, the less interest you accumulate, and the higher your net profit becomes. This alignment of incentives—where the lender's structure rewards your efficiency—is a hallmark of investor-friendly financing.

Here's another smart feature: OfferMarket structures its loans as interest-only during the holding period. Your monthly payments cover only the interest accrued, not principal reduction. This keeps your monthly carrying costs low, freeing up your cash for renovation expenses, unexpected surprises, or your next investment opportunity. You'll repay the principal when you sell the property—exactly how a fix and flip should work.

High Leverage Based on After Repair Value (ARV)

Here's where things get exciting. One of OfferMarket's biggest advantages is lending based on your property's future value, not just its current distressed state. While traditional lenders fixate on "as-is" value, OfferMarket looks at your project's After Repair Value (ARV)—the estimated market value once all your planned renovations are complete.

After Repair Value (ARV) is the foundation of fix and flip financing because it accounts for the value you're creating through your hard work. ARV is typically calculated by analyzing recent comparable sales (comps) of similar properties in similar condition within the same neighborhood. For example, if recently renovated 3-bedroom homes in your target area have sold for $300,000, that becomes the starting point for your property's ARV, adjusted for differences in size, features, or location.

OfferMarket's ARV-based lending puts high leverage within your reach across two key components of your project:

Purchase Price Financing: OfferMarket will typically fund 80% to 90% of the property's purchase price, depending on your experience tier (more on this below). This means if you're acquiring a distressed property for $150,000, you could receive $120,000 to $135,000 in acquisition financing, requiring only $15,000 to $30,000 as your down payment.

Renovation Budget Financing: OfferMarket funds 100% of your approved renovation budget. If your project requires $50,000 in improvements, that full amount is included in your loan and held in the construction holdback escrow we discussed earlier.

Here's how it all comes together: Say you're purchasing a property for $150,000 with a renovation budget of $50,000, and your ARV is projected at $280,000. At 90% leverage on the purchase price, OfferMarket finances $135,000 for acquisition. Add the $50,000 renovation budget (100% financed), and your total loan amount is $185,000. Your out-of-pocket investment is just the $15,000 down payment plus closing costs—that's smart leverage working for you.

![**Task:** Create a detailed financial breakdown infographic showing a real fix and flip deal example with OfferMarket's ARV-based financing, including purchase price, renovation budget, ARV, loan amounts, and investor equity requirement.

**Visual Structure:** Structured infographic with a property illustration at top, financial breakdown in the middle showing the deal structure, and a visual representation of the ARLTV calculation at the bottom.

**ASCII Layout Reference:**

```

┌────────────────────────────────────────────────────────────┐

│ FIX & FLIP DEAL BREAKDOWN │

│ OfferMarket ARV-Based Financing Example │

├────────────────────────────────────────────────────────────┤

│ [HOUSE ICON] │

│ │

│ PROPERTY DETAILS │

│ Purchase Price: $150,000 │

│ Renovation Budget: $50,000 │

│ After Repair Value (ARV): $280,000 │

├────────────────────────────────────────────────────────────┤

│ FINANCING STRUCTURE │

│ │

│ Acquisition Financing (90% LTV) │

│ ████████████████████ $135,000 │

│ │

│ Renovation Financing (100%) │

│ ██████████ $50,000 │

│ │

│ ───────────────────────────────────── │

│ Total Loan Amount: $185,000 │

├────────────────────────────────────────────────────────────┤

│ YOUR INVESTMENT │

│ Down Payment: $15,000 │

│ Closing Costs: ~$5,000 │

│ Total Out-of-Pocket: $20,000 │

├────────────────────────────────────────────────────────────┤

│ ARLTV CALCULATION │

│ $185,000 ÷ $280,000 = 66% ARLTV │

│ │

│ [VISUAL BAR: 66% filled] │

│ ████████████████ Well within 70-75% cap │

└────────────────────────────────────────────────────────────┘

```

**Image Section Breakdown:**

- Header:](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1772216955792_mi6u89.jpg?alt=media&token=c05b8254-3c97-4dd6-b4e5-c830589d239f)

Understanding the ARLTV Cap: Your Built-In Safety Net

While OfferMarket offers generous leverage, there's a smart safeguard that keeps both you and the lender protected from overleveraging: the After Repair Loan-to-Value ratio, or ARLTV. This cap ensures your total combined loan amount (purchase financing plus renovation budget) stays within 70% to 75% of the property's projected ARV.

Let's break it down with our example: Your total loan is $185,000 (purchase + renovation), and your ARV is $280,000. Your ARLTV is $185,000 ÷ $280,000 = 66%, which sits comfortably within the typical 70-75% cap. Green light—the loan is approved because there's healthy equity cushion in the deal.

So why does this cap matter to you? The ARLTV ratio acts as protection against market shifts and valuation surprises. If property values dip or your renovation doesn't boost value as expected, there's still a solid margin of safety. Think of the ARLTV cap as your built-in reality check—it helps you steer clear of deals with thin profit margins or overly optimistic ARV projections.

Understanding ARLTV is crucial when evaluating potential deals. If a property's numbers don't work within the ARLTV constraints, it's often a signal that the deal itself may not be profitable enough to pursue. Savvy investors use ARLTV calculations during their initial deal analysis to quickly determine maximum borrowing capacity and required cash investment before even submitting an offer.

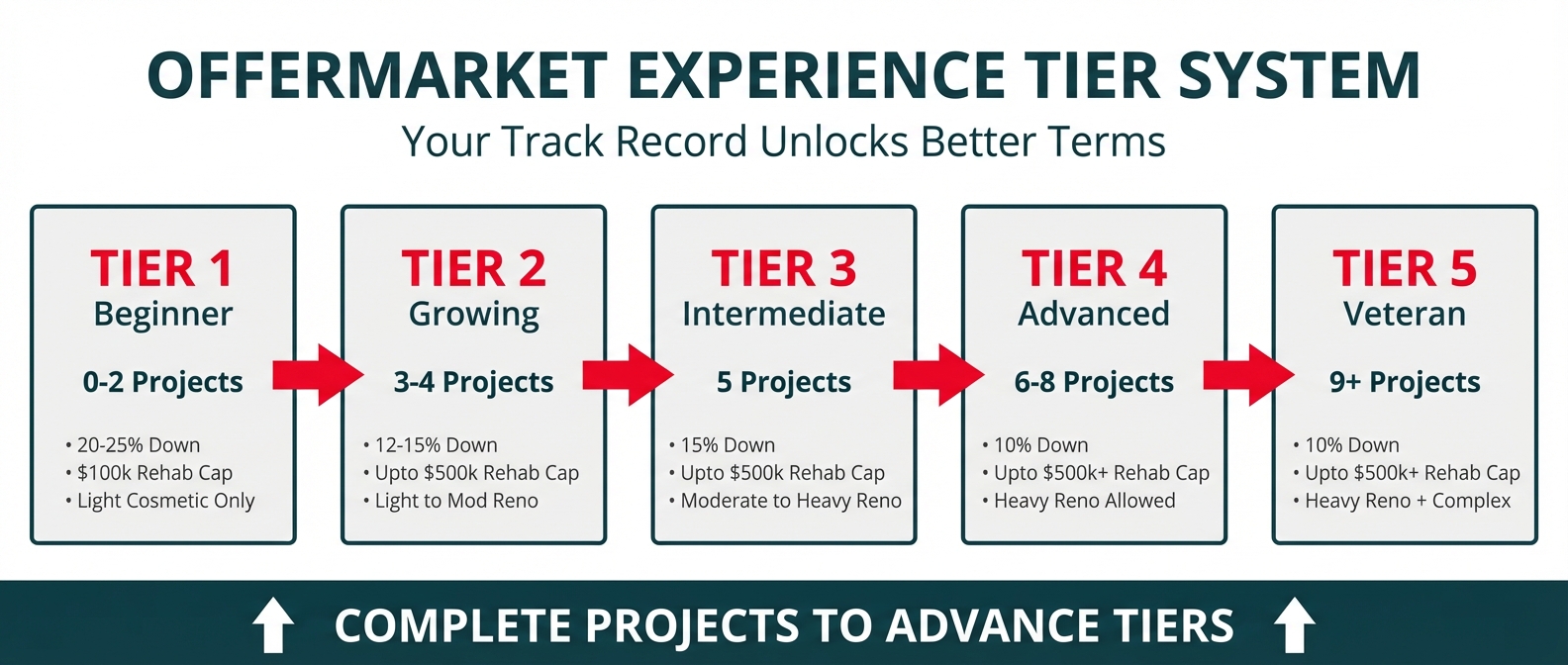

The Experience Tier System: Your Track Record Matters

Here's the deal: not all investors carry the same level of risk. A first-time flipper tackling a major structural renovation looks very different from a veteran investor with dozens of successful projects under their belt. OfferMarket gets this, which is why we use an experience tier system that adjusts your loan terms based on your proven track record.

How Experience Tiers Are Determined:

We categorize borrowers into experience tiers—typically ranging from Tier 1 (beginners) to Tier 5 (veterans)—based on the number of fix and flip or rental property projects you've successfully completed in the last 36 months. Here's how it breaks down:

- Tier 1 (Beginner): 0-2 completed projects. You're just getting started in fix and flip investing or have very limited experience.

- Tier 2-3 (Intermediate): 3-5 completed projects. You've proven you can get the job done and you're building momentum.

- Tier 4-5 (Veteran/Experienced): 6+ completed projects. You're a seasoned pro who knows how to manage renovations and exits like clockwork.

How Your Tier Affects Your Loan:

Your experience tier directly impacts several key loan parameters:

Down Payment Requirements: The more experience you have, the less cash you may need upfront. A Tier 1 borrower might need to put down 20-25% of the purchase price, while a Tier 5 investor could access the maximum 90% leverage with only a 10% down payment. That difference can seriously boost your cash-on-cash returns and let you take on more projects at once.

Maximum Renovation Budget: Lenders cap the size and complexity of renovations for less experienced investors. A Tier 1 borrower might be limited to $100,000 in cosmetic renovations, while a Tier 4-5 investor could qualify for up to $500,000 budgets involving structural changes, additions, or complex mechanical upgrades.

Project Scope Eligibility: Here's where the tiers really make a difference. If you're just starting out, you'll typically work with light, cosmetic renovations—think paint, flooring, kitchen and bath updates, and landscaping. These projects are great entry points because they're straightforward, predictable, and less likely to throw you curveballs.

As you build your track record, you'll unlock heavy renovation projects: major structural modifications, additions that expand square footage, property conversions (single-family to multi-unit, or vice versa), and projects requiring extensive mechanical, electrical, or plumbing overhauls. Yes, these are more complex—but they also open the door to higher profit potential once you've got the experience to back it up.

Why This System Works in Your Favor:

Think of the experience tier system as your personal growth roadmap. You start with smaller, simpler projects that sharpen your skills and build your reputation. As you complete successful flips and document your wins, you unlock larger budgets, better leverage, and more ambitious projects with greater profit potential. It's a win-win: lenders manage risk appropriately while you get accessible financing at every stage of your investing journey.

When you grab your instant quote from OfferMarket, we'll evaluate your experience and place you in the right tier. New to the game? Don't sweat the initial limitations—they're your stepping stones. Knock out a few successful projects, keep good records, and you'll move up to higher tiers with better terms and bigger opportunities before you know it.

Structuring Your Scope of Work for Maximum Cash Flow and Rapid Reimbursement in Fix and Flip Financing

Your Scope of Work (SoW) isn't just a renovation to-do list—it's your financial game plan. Get it right, and you'll speed up reimbursements and keep cash flowing smoothly throughout your fix and flip project. A well-structured SoW can mean the difference between smooth sailing and cash flow headaches that stall your project and cut into your profits.

Here's the deal: understanding how lenders reimburse based on completed line items is key to your success. Construction draw schedules work as a payment plan that maps out when and how renovation funds hit your account throughout your project. Since OfferMarket reimburses you only after specific line items are completed and verified, the way you organize and group your work directly impacts how fast you get paid. A poorly structured SoW can leave you waiting weeks for reimbursement on work that's already done, forcing you to cover costs out of pocket and potentially delaying the next phases of your renovation.

Best Practices for SoW Structure to Maximize Liquidity

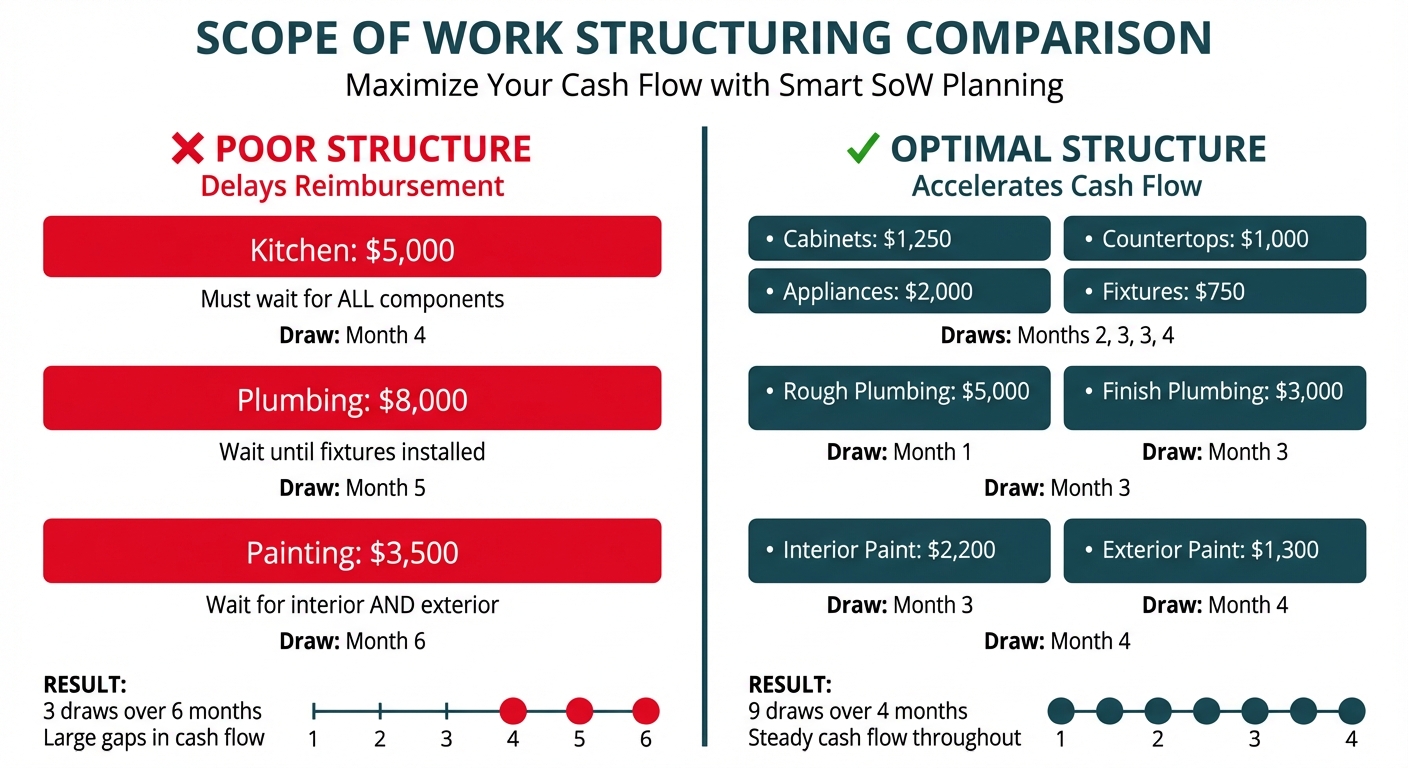

Structure by Trade or System, Not Room-by-Room

Here's a mistake we see all the time: investors organize their SoW by room rather than by material and trade. If you list "Kitchen: $5,000" as a single line item, you won't see a dime until every single detail of that kitchen is 100% complete—even if you're just waiting on a backsplash tile or cabinet hardware. This approach creates unnecessary cash flow bottlenecks that can really hurt.

The smarter move? Break down work by specific materials and trades. Rather than "Kitchen," list separate line items such as "Cabinets ($1,250)," "Countertops ($1,000)," "Appliances ($2,000)," and "Fixtures ($750)." This granular approach lets you get reimbursed incrementally as each specific component is installed and inspected. When your cabinets are hung, you can immediately draw those funds—even if countertops won't arrive for another week. This strategy keeps cash flowing steadily throughout your project rather than in large, infrequent chunks.

Separate "Rough" and "Finish" Work

Major systems like electrical, plumbing, and HVAC span multiple stages of construction, from initial rough-in work to final fixture installation. Grouping these into single line items forces you to wait until the very end of your project—when final fixtures are installed—before receiving full reimbursement for work completed months earlier.

Here's a smarter approach: always separate these critical systems into two distinct line items: "Rough" and "Finish." For example, create separate entries for "Rough Electrical" and "Finish Electrical," or "Rough Plumbing" and "Finish Plumbing." Why does this matter? This separation allows you to draw funds immediately after the rough-in phase passes inspection, typically early in your renovation timeline. You'll then receive the second disbursement when finish work is complete. The bottom line: you'll access capital faster for subsequent construction stages and avoid financing completed work out of pocket for extended periods.

Separate Interior vs. Exterior Work

The same logic applies here. Grouping interior and exterior work under single categories can create unnecessary reimbursement delays. If you list simply "Painting" as one line item, you must wait until both the entire interior and exterior are painted before drawing those funds.

The fix is simple: create separate line items like "Interior Paint" and "Exterior Paint." This allows the lender to reimburse you as soon as one section is finished, rather than waiting for the entire house to be painted. Since weather, contractor availability, and project sequencing often mean these tasks happen weeks apart, this separation keeps your cash flow moving consistently.

Itemize Deliverables and Costs Clearly

Provide detailed descriptions and accurate cost estimates for each line item to avoid ambiguity during the draw request process. Vague entries like "Miscellaneous repairs: $3,000" will likely face scrutiny and delays during inspection. Instead, get specific about what work is included: "Replace water-damaged drywall in master bathroom (materials and labor): $800" or "Install new interior doors (6 units, materials and installation): $1,200."

Clear itemization speeds up approval because inspectors can easily verify completion against your documented scope. It also protects you from disputes about what was or wasn't included in your original budget.

Balancing Your Budget and Respecting Valuation Limits

OfferMarket carefully reviews your SoW to make sure your budget stays balanced from start to finish. This keeps you from drawing too much capital early on and potentially running out of funds before the project wraps up—a situation that puts both your success as an investor and the lender's security at risk.

Strict Caps on Early-Stage and Non-Material Work

To make sure your funds go primarily toward value-adding materials and labor that directly support your property's After Repair Value (ARV), OfferMarket enforces specific caps on certain budget categories:

Demolition: Capped at 10% of your total renovation budget. This covers site cleanout and dumpster removal. Quick heads-up: if the dumpster is still on site during inspection, the lender may hold back part of your demolition reimbursement until it's hauled away and the site is cleaned up.

Soft Costs: Also capped at 10% of the total budget. These include permits, architectural plans, engineering fees, surveys, and inspection fees—necessary expenses that don't directly add physical value to your property.

Contingency: Limited to 10% of the total budget. We'll dive deeper into contingency management shortly, but here's the bottom line: include this buffer. It covers unexpected expenses without requiring formal scope revisions.

Combined Total Cap: If your SoW includes all three categories (demolition, soft costs, and contingency), their combined total can't exceed 25% of your overall renovation budget. This guarantees that at least 75% of your budget goes toward tangible improvements that boost your property's value.

These caps are here to protect both you and the lender by making sure renovation funds are strategically directed toward work that maximizes your ARV and sets you up for a profitable exit.

Handling Scope of Work Revisions Mid-Project

Here's the truth about construction: projects rarely go exactly as planned. Hidden structural surprises, material shortages, shifting costs, and smart opportunities to boost value based on market feedback make SoW revisions part of the game. Knowing how to handle these changes smoothly keeps your project moving forward and your finances on track.

When Revisions Are Needed

You'll likely need scope revisions when you encounter:

- Hidden structural problems (foundation issues, outdated wiring, failing plumbing)

- Major swings in material costs or availability

- Smart opportunities to upgrade finishes based on what buyers want or recent comps

- Planned work that turns out to be unnecessary or just won't work

- New regulations that require additional permits or modifications

How to Submit a Revision

When changes come up, reach out to OfferMarket's processing team right away. Put together clear documentation of what you're proposing—detailed descriptions of the new work, updated cost estimates, and your reasoning for the change. The better your documentation, the quicker you'll get the green light.

Reallocating Contingency Funds

Your contingency fund is there for exactly these moments. When smaller unexpected costs pop up, you can usually tap into this reserve without formally adjusting your main budget line items. This gives you the flexibility to handle issues fast without getting bogged down in paperwork. Just keep close tabs on what you're spending so you don't burn through your contingency too soon.

Removing Line Items

If planned work no longer makes sense or simply can't be done, document your reasoning and show how you'll redirect those funds. Lenders typically approve sensible removals, especially when you're putting that money toward other improvements that add value.

Adding New Line Items

When you need to add new work to your project, come prepared with solid justification and clear cost documentation. Think about how this addition supports your ARV or tackles a critical issue you've uncovered during renovation. Gather your contractor quotes and put together detailed breakdowns of materials and labor—this makes the approval process smoother for everyone.

Avoiding Jeopardizing Your Approved ARV

Here's the bottom line for any scope revision: it needs to align with your original ARV projections. Major changes that shift your property's finish level, square footage, or target market may trigger a fresh look at your ARV. And if your revisions drive up costs without adding proportional value, you could push past your approved loan-to-ARV ratio—putting your financing at risk.

Before you submit significant revisions, ask yourself: will these changes protect or boost my projected ARV? Smart revisions that respond to market shifts or fix critical problems can actually make your project more profitable—but only when you manage them carefully and keep your lender in the loop.

Master your SoW structure and revision process, and you'll keep cash flowing, avoid costly delays, and maximize your returns throughout your fix and flip journey.

Key Considerations for Successful Fix and Flip Investors

Getting the right financing through OfferMarket gives your fix and flip project a solid foundation—but lasting success takes more than capital. The investors who consistently profit know that financing is just one piece of the puzzle. The rest? Careful planning, thorough due diligence, and smart risk management.

Thorough Market Analysis and Understanding Local Comps

Before you even request that instant quote from OfferMarket, get to know your market inside and out. Successful fix and flip investors don't just buy properties—they buy opportunities backed by solid data.

Start by analyzing local market trends, including average days on market, price appreciation patterns, and seasonal fluctuations. Dig deep into comparable sales (comps), zeroing in on recently sold properties within a half-mile radius that match your target property's profile. Take note of what buyers in that neighborhood actually want—maybe it's a modern kitchen, an extra bathroom, or a great backyard for entertaining.

Knowing your target buyer matters just as much. Are you renovating for first-time homebuyers, growing families, or downsizing retirees? Each group has different priorities, and those preferences should shape every renovation choice you make. Research shows that failing to assess the current real estate market conditions is one of the most common pitfalls that can lead to extended holding periods and reduced profitability.

Here's the bottom line: OfferMarket's high-leverage financing based on After Repair Value (ARV) delivers the best results when your ARV projections rest on solid market data. Nail your comps analysis, and you'll feel confident about your financing terms and profit projections.

Comprehensive Property Due Diligence and Inspections

Don't skip the inspection—even if you've walked through hundreds of properties. Think of that inspection fee as insurance against budget-busting surprises that can throw your whole project off track.

Bring in qualified inspectors to check every major system: foundation, roof, electrical, plumbing, HVAC, and structural elements. Look past the surface-level cosmetic stuff and hunt for hidden issues like water damage, mold, outdated electrical panels, or foundation problems. Do your homework on the property's history too—previous permits, additions, and any code violations that could complicate your renovation.

Make sure you understand the zoning regulations and building codes in your area. What renovations are permitted? Will you need special approvals for structural changes or additions? Getting clear answers to these questions before you buy saves you from expensive delays and frustrating scope changes down the road.

This homework directly shapes the Scope of Work you'll submit to OfferMarket. The better you pinpoint needed repairs from the start, the more accurate your renovation budget becomes—and the smoother your draw process runs as you complete each line item just as you planned.

Building a Reliable Contractor and Professional Team

Your project lives or dies by the people you bring on board. A strong team often makes the difference between a successful flip and a costly headache, so take this step seriously.

Start by interviewing several contractors. Call their references, look at their past projects, confirm their licenses and insurance, and pay attention to how they communicate. The lowest bid rarely equals the best deal—dependability, quality craftsmanship, and sticking to deadlines usually outweigh saving a few thousand dollars at the outset.

Beyond your general contractor, connect with skilled subcontractors for electrical, plumbing, and HVAC work. Having go-to pros who can jump in when problems pop up keeps your timeline intact. Line up dependable suppliers who deliver materials on time and may offer you contractor pricing.

Don't skip the professional advisors either. Partner with real estate agents who know investment properties and can help you spot opportunities and sell your finished project. Team up with accountants who specialize in real estate to maximize your tax benefits. Keep a real estate attorney ready for contract reviews and any legal questions that come up.

When you're tracking your project through OfferMarket's draw process, a contractor who keeps solid records and submits clean draw requests makes getting reimbursed quick and hassle-free.

Realistic Budgeting and Contingency Planning

One of the most dangerous mistakes in fix and flip investing is underestimating costs. Many investors fail to account for all expenses involved in a project, focusing only on the purchase price and obvious renovation needs while overlooking carrying costs, permit fees, and unexpected repairs.

Here's what smart investors do: create a detailed, line-item budget that captures every expense. Think acquisition costs, renovation materials and labor, permits and inspections, insurance, property taxes, utilities, marketing costs, and closing costs for both purchase and sale. Don't forget your financing costs—use the terms from your OfferMarket instant quote, and remember that with interest charged "As Disbursed," your actual interest expense depends on how quickly you draw funds and complete the project.

Now, here's a golden rule: always include a contingency fund. Following OfferMarket's Scope of Work guidelines, set aside up to 10% of your renovation budget for the unexpected. Because let's be honest—construction projects love surprises. Hidden water damage, outdated wiring, supply chain hiccups that spike material costs. Your contingency fund handles these curveballs without forcing you to cut corners or compromise your final sale price.

One more tip: build conservative timelines into your budget. If you're thinking three months, plan for four. That extra month of carrying costs is much easier to swallow than scrambling for capital before you've crossed the finish line.

Developing Clear Exit Strategies Before Purchase

Here's what separates successful fix and flip investors from the rest: they know exactly how they'll exit a property before they ever make an offer. Your exit strategy deserves as much attention as your renovation plan—because without a clear path to sale, even perfect financing and flawless execution won't put profit in your pocket.

Start by defining your target buyer profile and ideal sale price range based on your comps analysis. Identify the key features and finishes that will appeal to this buyer and justify your target price point. Research the best marketing channels for reaching your audience—whether that's traditional MLS listings, social media marketing, or working with investor-friendly agents who have extensive buyer networks.

The OfferMarket Marketplace: A powerful tool for selling your deal directly to a massive network of verified real estate investors. By listing on OfferMarket, you can often bypass expensive agent commissions and the "staging" headaches of the retail market, allowing you to exit quickly at a competitive price point.

Consider multiple exit scenarios. What's your primary plan? If the market softens, what's your backup strategy—holding as a rental, seller financing, or adjusting your price? Here's the truth: most flips don't fail because the property is bad; they fail because the plan was too rigid or overly optimistic. Building contingency exit strategies into your plan protects you when the market throws you a curveball.

OfferMarket's flexible terms are designed with your exit strategy in mind. With no prepayment penalties and terms ranging from 12 to 24 months, you have the freedom to sell when you find the right buyer—or hold a bit longer if patience makes more sense. The interest-only structure keeps your carrying costs low while you work toward your ideal outcome.

Your Partner in Fix and Flip Success – OfferMarket

Navigating fix and flip financing can feel overwhelming, especially when you're balancing speed, cost, and flexibility. While hard money lenders generally have flexible eligibility requirements and can provide fix and flip loans as quickly as one to three weeks, OfferMarket builds on this foundation to deliver a comprehensive solution designed specifically for real estate investors at every experience level.

OfferMarket isn't just another lender in a crowded marketplace—we're a strategic partner committed to your success from the moment you evaluate a potential deal to the day you close on your profitable sale. The platform's integrated approach combines financing, property listings, and insurance solutions in one seamless ecosystem, eliminating the need to juggle multiple vendors and streamlining your entire investment workflow.

The competitive advantages that set OfferMarket apart are substantial and directly impact your bottom line:

Speed That Captures Opportunities: In real estate investing, timing is everything. OfferMarket's ability to close loans in under three weeks means you can compete with cash buyers and secure properties before your competition even gets pre-approved. This speed advantage, combined with the instant quote system that lets you evaluate deal profitability in minutes, transforms how quickly you can move from identifying an opportunity to securing financing.

High Leverage That Maximizes Your Capital Efficiency: With up to 90% financing on the purchase price and 100% of your renovation budget—all based on the property's After Repair Value (ARV) rather than its distressed current state—OfferMarket helps you preserve capital for multiple projects at once. This high leverage approach puts your investment dollars to work harder, allowing you to scale your portfolio faster than traditional financing methods would permit.

Experience-Based Terms That Grow With You: The tiered system that adjusts loan terms based on your track record isn't just fair—it's designed to support your journey. Whether you're completing your first flip or your fiftieth, OfferMarket provides accessible financing that matches your expertise level. As you build your portfolio and demonstrate success, you unlock better terms, larger budgets, and more ambitious project opportunities, creating a clear pathway for growth in your investment business.

Strategic Interest Calculation That Saves You Money: The "As Disbursed" interest structure on renovation funds represents a smarter approach to how carrying costs impact your profitability. Unlike lenders who charge interest on your entire renovation budget from day one, OfferMarket only charges interest on funds after they've been drawn and deployed into your project. Combined with interest-only monthly payments, this approach can save thousands of dollars on each project—money that goes straight into your pocket.

Flexibility That Works for You: With no prepayment penalties and terms built for quick turnarounds, OfferMarket fits the fix and flip model like a glove. The faster you finish renovations and sell, the less interest you pay and the more profit you keep. This flexibility carries over to your Scope of Work management too, where smart structuring helps you get reimbursed quickly and maintain healthy cash flow throughout your project.

Beyond these real-world benefits, OfferMarket gives you the educational resources, transparent processes, and responsive support that turn financing from a headache into a genuine edge. The platform's Loan File system acts as your command center, showing you exactly where your application stands, your preliminary terms, what documents you need, and your draw requests—all in one easy-to-use dashboard.

Ready to see what OfferMarket can do for you? Don't let financing hold back your investment potential. Whether you're exploring your first fix and flip or you're an experienced investor looking to sharpen your capital strategy, OfferMarket delivers the speed, leverage, and smart advantages you need to win.

Get an Instant Quote from OfferMarket Today and find out exactly how much you can borrow for your next project. In just minutes, you'll see personalized loan terms, estimated interest rates, and projected monthly payments—no commitment required and no hit to your credit. Change the way you evaluate deals, lock in financing faster than the competition, and tap into the full potential of every opportunity that comes your way.

Your next successful flip starts with one simple step. Get your instant quote now and join the growing community of investors who've learned that the right financing partner is what separates a good investment from a great one.

OfferMarket Loans

Check your rate

60 seconds · no credit pull