*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Current rental property loan rates (Q2 2026)

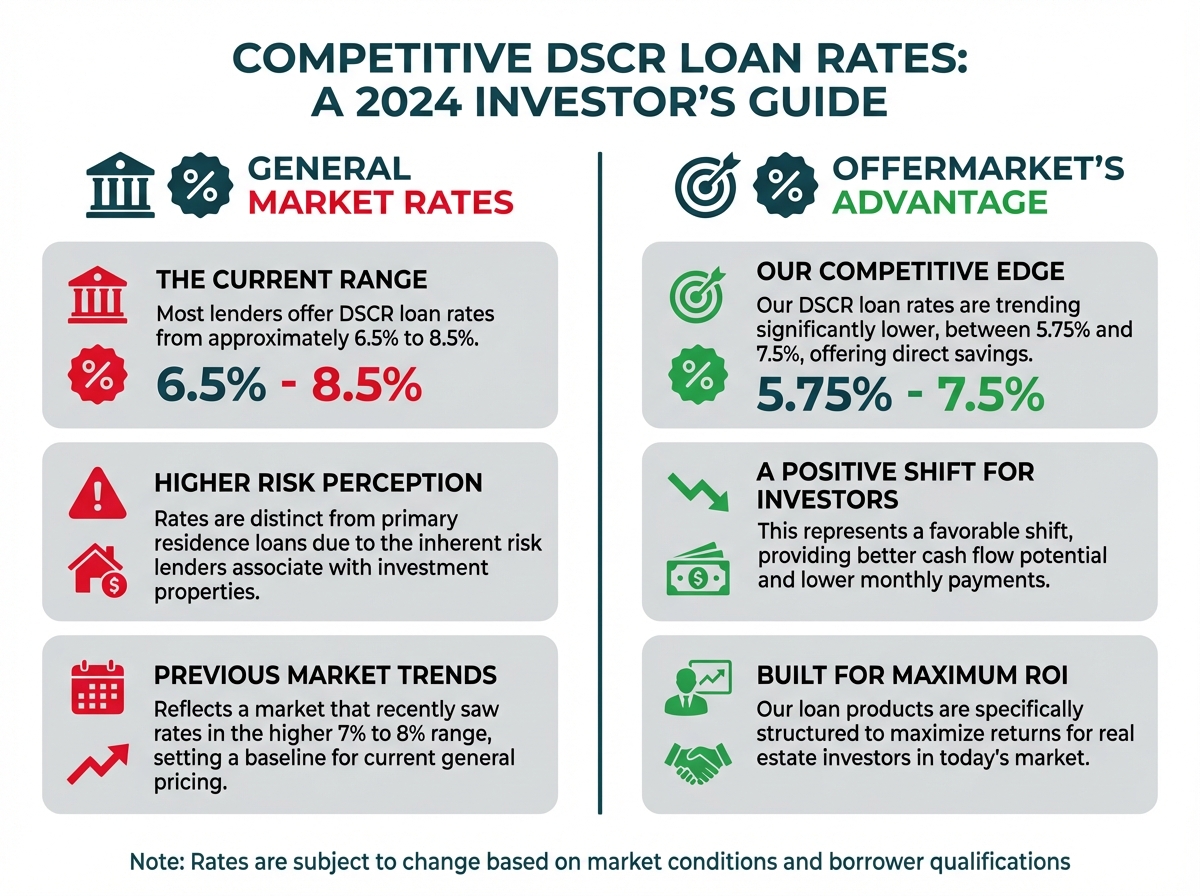

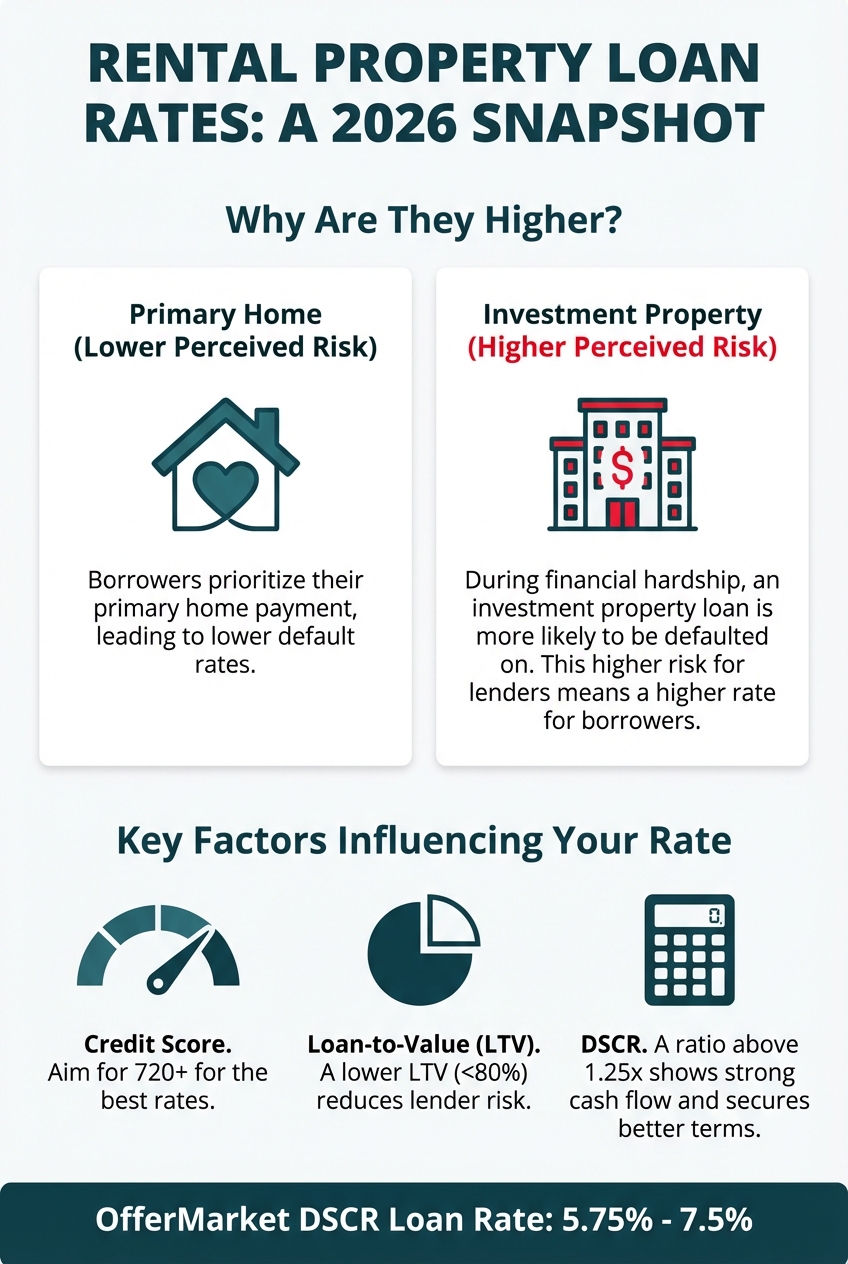

Rental property loan rates currently range from approximately 6.5% to 8.5% for products like DSCR loans. At OfferMarket, our competitive DSCR loan rates are trending between 5.75% and 7.5%, reflecting a positive shift for investors from the higher 7% to 8% range seen in 2025. These rates are distinct from those for primary residences due to the inherent risk lenders associate with investment properties.

Understanding the factors that influence these rates is crucial for maximizing your return on investment. Key metrics such as your credit score, the loan-to-value (LTV) ratio, and especially the property's Debt Service Coverage Ratio (DSCR) directly impact the interest rate you'll be offered. A strong property cash flow and a solid financial profile can unlock the most competitive financing terms available.

Summary Comparison Table: 2026 Guidelines

| Program | Est. Rate 2026 | Max Leverage | Key Metric |

|---|---|---|---|

| DSCR Rental | 6.5% – 8.5% | 80% LTV | Cash Flow (DSCR) |

| Fix and Flip | 9.75% – 13.5% | 90% LTC | After-Repair Value (ARV) |

| Ground Up | 11.0% – 12.5% | 85% LTFC | Construction Experience |

| Slow Flip | 15% | 100% As-Is | Low Purchase Price |

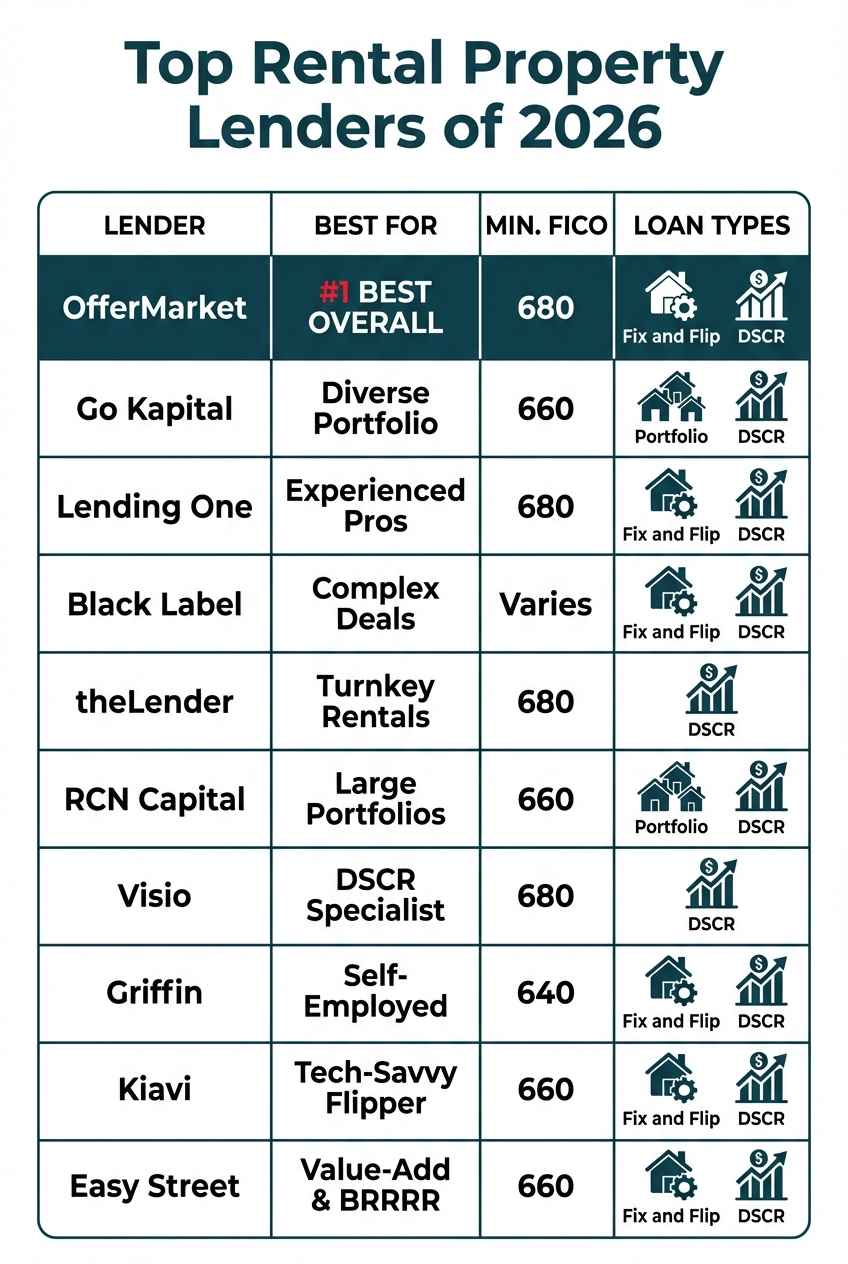

Comparison of Loan Products for Real Estate Investors

Choosing the right loan is as important as choosing the right property. Your financing strategy must align with your investment strategy. A long-term buy-and-hold investor needs a different loan than a short-term fix-and-flipper. Below is a summary of OfferMarket's loan products, designed to meet the diverse needs of modern real estate investors.

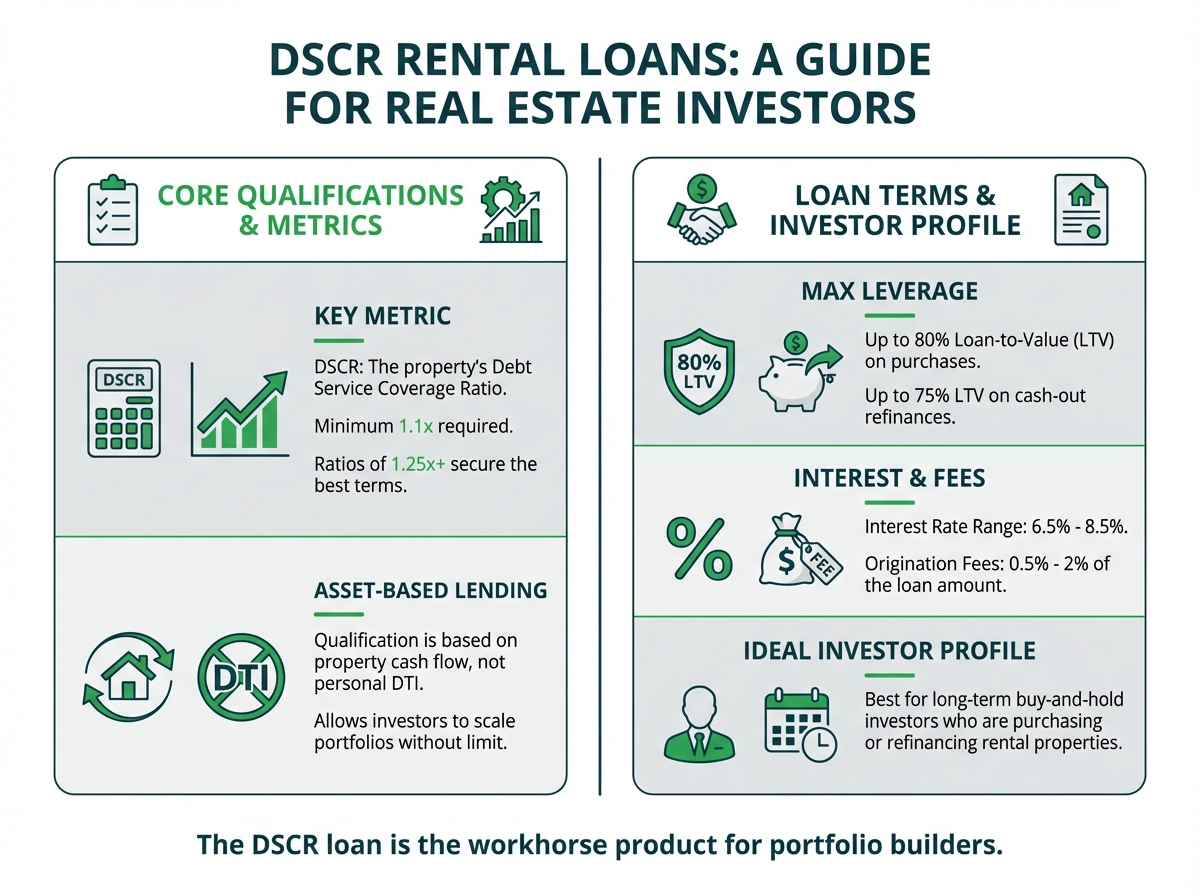

DSCR Rental Loans

- Best For: Long-term buy-and-hold investors purchasing or refinancing rental properties.

- Interest Rate Range: 6.5% - 8.5%.

- Max Leverage: Up to 80% Loan-to-Value (LTV) on purchases and 75% on cash-out refinances.

- Key Metric: The property's Debt Service Coverage Ratio (DSCR). A ratio of 1.1x is typically the minimum required, with 1.25x+ securing the best terms.

- Fees: Origination fees generally range from 0.5% to 2% of the loan amount.

The DSCR loan is the workhorse product for portfolio builders. Its primary advantage is asset-based qualification, allowing you to scale your investments without being limited by your personal DTI.

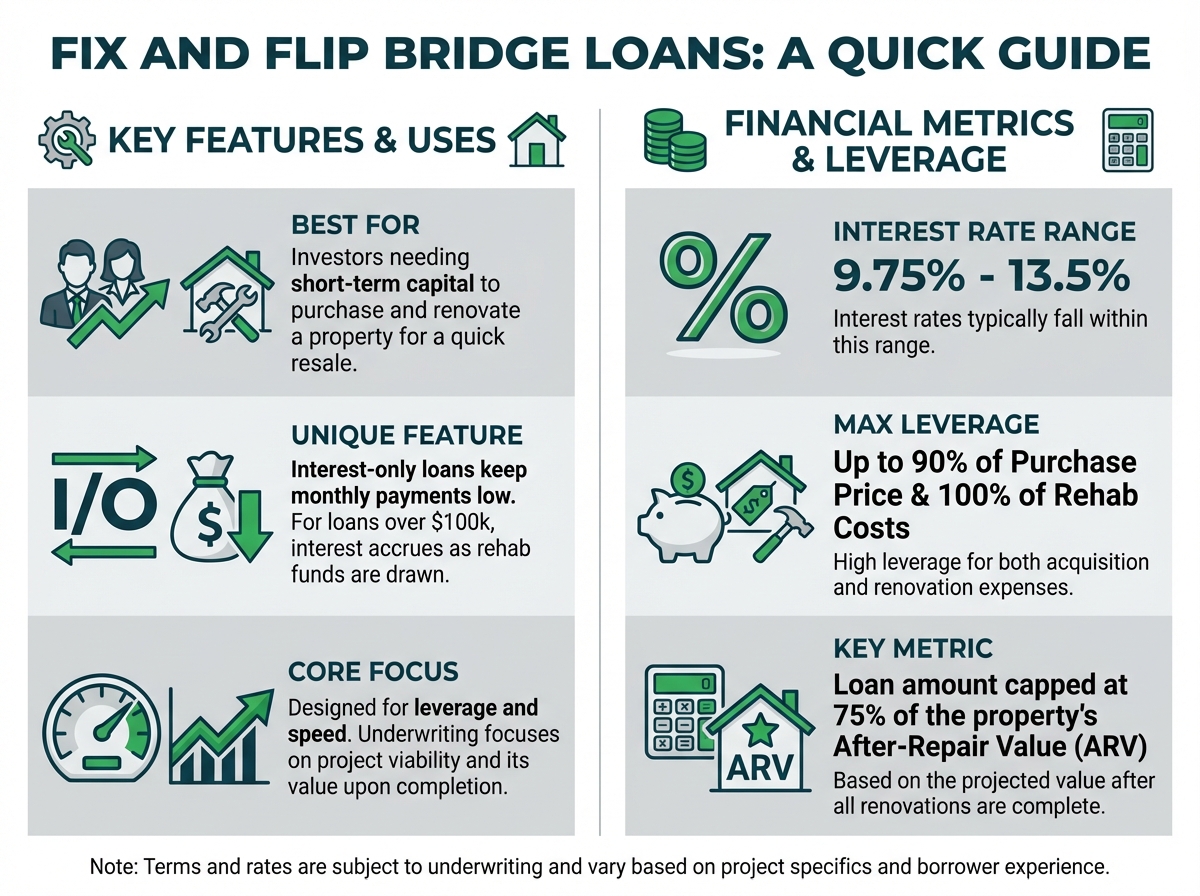

Fix and Flip Bridge Loans

- Best For: Investors who need short-term capital to purchase and renovate a property for a quick resale.

- Interest Rate Range: 9.75% - 13.5%.

- Max Leverage: Up to 90% of the purchase price and 100% of the rehab costs.

- Key Metric: The loan amount is capped at 75% of the property's After-Repair Value (ARV).

- Unique Feature: These are interest-only loans, which keeps monthly payments low and maximizes capital available for the renovation. For loans over $100k, interest only accrues as the rehab funds are drawn.

Fix and flip loans are all about leverage and speed. They provide the high-leverage financing needed to acquire a property and fund its transformation, with underwriting focused on the viability of the project and its value upon completion.

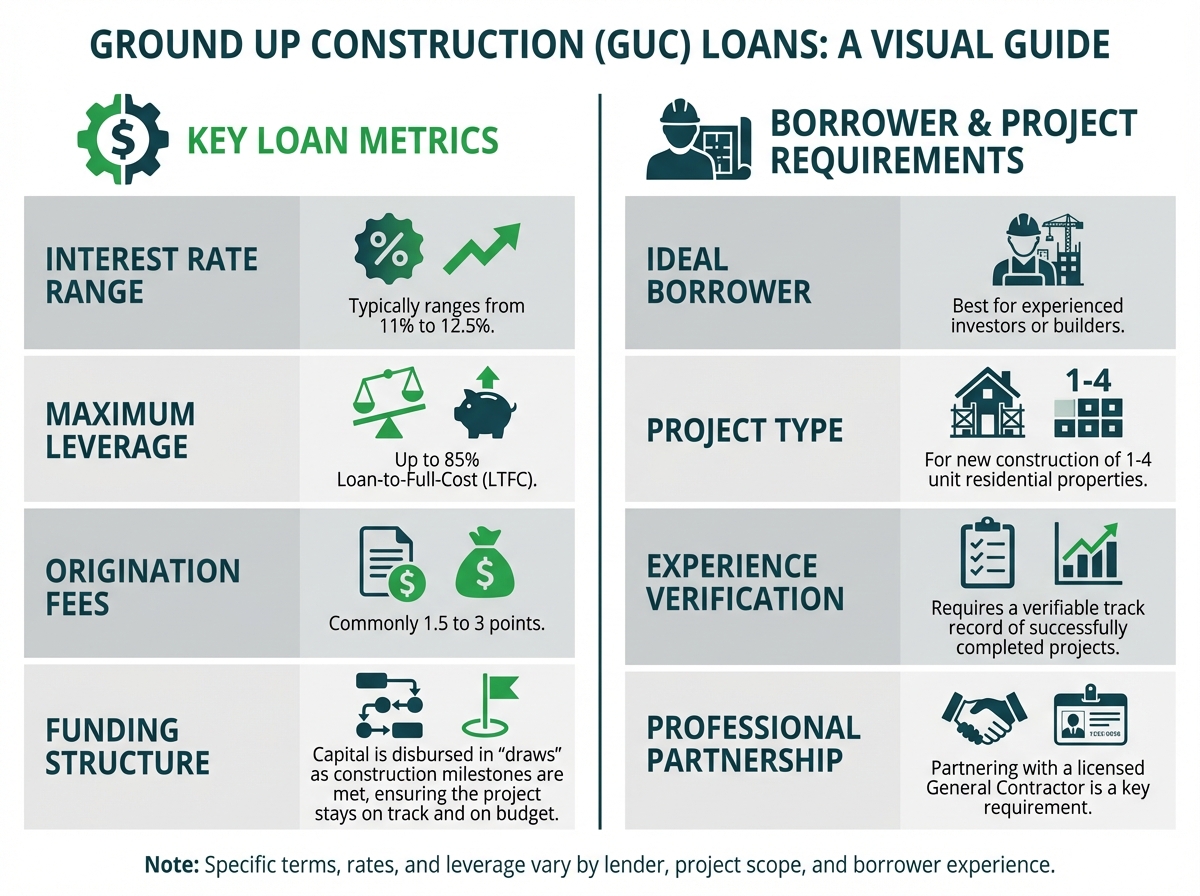

Ground Up Construction (GUC) Loans

- Best For: Experienced investors or builders constructing new 1-4 unit residential properties from the ground up.

- Interest Rate Range: 11% - 12.5%.

- Max Leverage: Up to 85% Loan-to-Full-Cost (LTFC).

- Key Metric: Verifiable prior construction experience or partnering with a licensed General Contractor is required. Lenders need to see a track record of successfully completed projects.

- Fees: Origination fees are typically 1.5 to 3 points.

Ground up construction loans are more complex and are structured to fund a project in stages. Capital is disbursed in "draws" as construction milestones are met, ensuring the project stays on track and on budget.

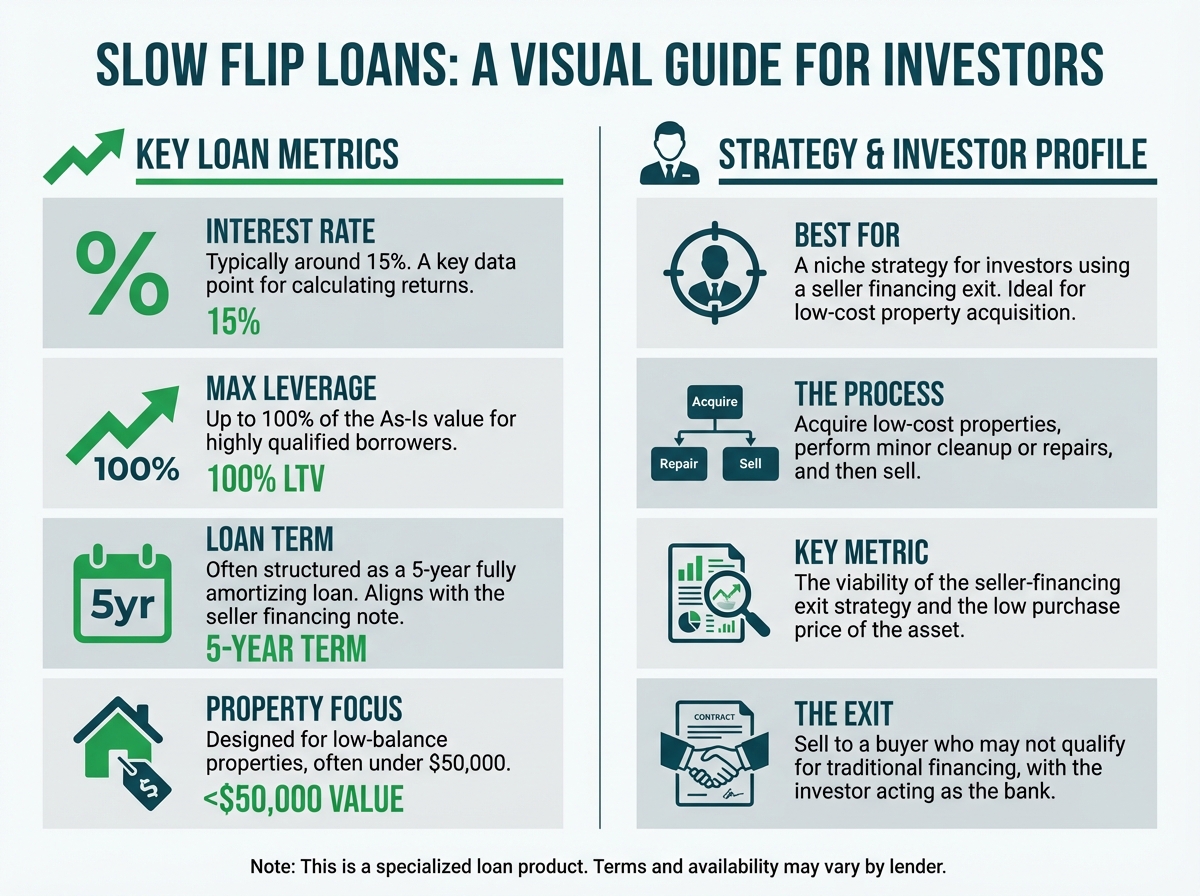

Slow Flip Loans

- Best For: A niche strategy involving low-balance properties (often under $50,000) where the exit strategy is seller financing.

- Interest Rate: Typically around 15%.

- Max Leverage: Up to 100% of the As-Is value for highly qualified borrowers.

- Key Metric: The viability of the seller-financing exit strategy and the low purchase price of the asset.

- Term: Often structured as a 5-year fully amortizing loan to align with the seller financing note the investor will create.

The Slow Flip loan is a specialized tool for a very specific investment model. It allows investors to acquire low-cost properties with maximum leverage, perform minor cleanup or repairs, and then sell them to a buyer who may not qualify for traditional financing, with the investor acting as the bank.

Compare Your Rate Options

See how today’s averages translate to your specific deal. View custom rates, terms, and max LTV in minutes—no credit check required

Get Your Quote →Why Investment Property Loan Rates Are Higher Than Primary Mortgages

The core reason rental property loan rates are higher is risk. From a lender's perspective, a loan for an investment property carries a greater risk of default than a loan for an owner-occupied primary residence. During periods of financial hardship, a borrower is statistically far more likely to miss a payment on a rental property than on the home they live in.

This isn't a reflection on you as an investor, but a broad statistical reality that lenders must account for. The Federal Housing Finance Agency (FHFA) has studied mortgage performance for decades, and the data consistently shows higher delinquency and default rates for non-owner-occupied properties.

Lenders price this elevated risk into the loan in several ways:

Higher Interest Rate: The most direct way to compensate for risk is by charging a higher interest rate. This "risk premium" ensures the lender is rewarded for taking on the additional uncertainty.

Higher Down Payment Requirements: Lenders typically require a larger down payment (lower LTV) for investment properties, often 20-25% or more, compared to as little as 3-5% for some primary home loans. More equity in the property means the borrower has more to lose, making them less likely to default.

Stricter Underwriting: While asset-based lenders like OfferMarket focus on property performance, the overall financial health of the borrower is still a factor. Lenders need to be confident that the investor can handle vacancies and unexpected repairs.

Essentially, a loan on your primary home is a consumer debt for personal housing. A loan on a rental property is a commercial debt for a business venture. Lenders underwrite and price these two categories of loans differently to reflect their distinct risk profiles.

Key Factors That Determine Your Rental Property Loan Rate

Your final interest rate isn't a single, static number. It's a dynamic figure calculated based on a specific risk assessment of you, the property, and the loan structure. Understanding these components empowers you to take control and actively work towards securing a more favorable rate.

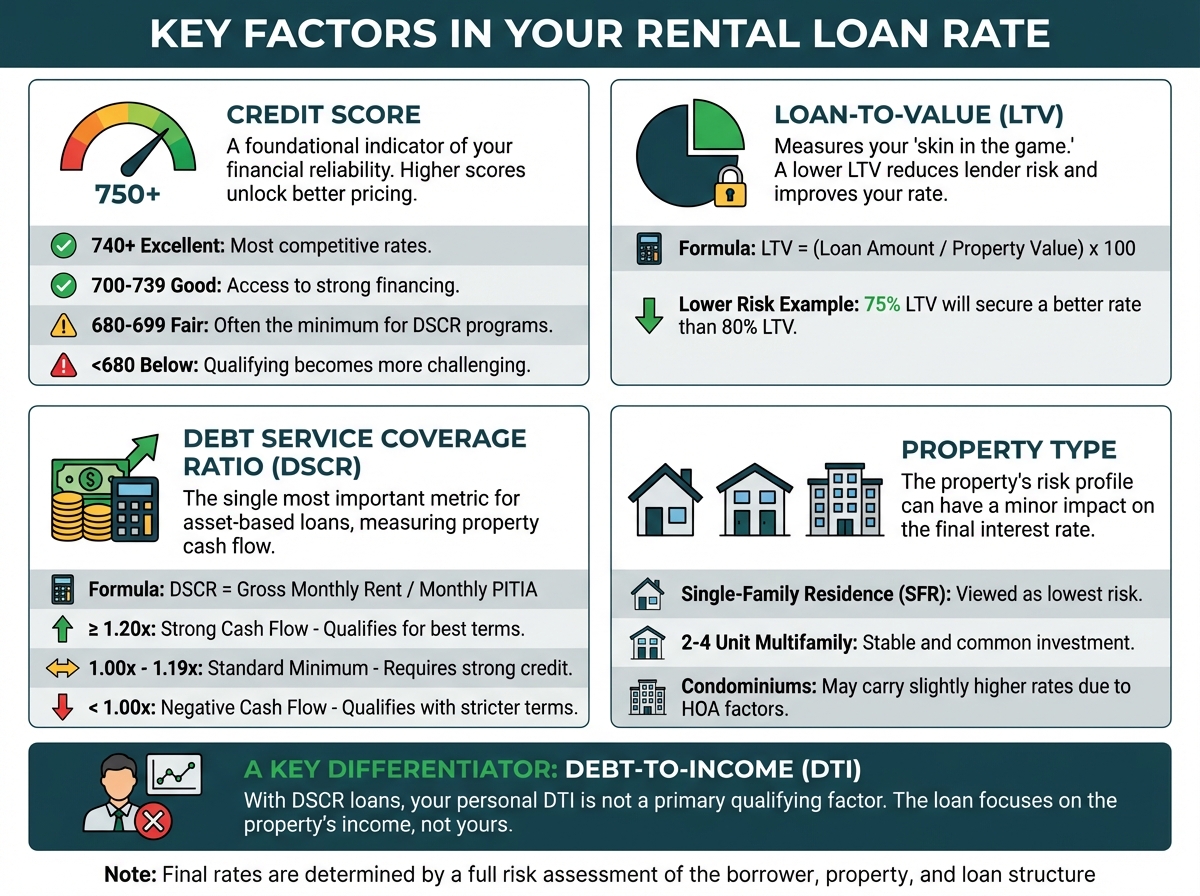

Credit Score

Your personal credit score remains a foundational element in a lender's risk assessment, even for asset-based loans. It serves as a reliable indicator of your history with and commitment to managing debt. Lenders use a tiered system, where higher scores unlock better pricing.

- Excellent Credit (740+): Borrowers in this range are considered very low risk and will be offered the most competitive interest rates and terms. This is the target for any serious investor.

- Good Credit (700-739): You can still secure good financing in this range, but the rate may be slightly higher than the top tier.

- Fair Credit (680-699): This is often the minimum score required for many investment property loan programs, including DSCR loans. Rates will be noticeably higher to compensate for the perceived increase in risk.

- Below 680: Qualifying for a rental property loan becomes significantly more challenging and expensive.

According to Experian, one of the major credit bureaus, a higher FICO Score can save you thousands of dollars over the life of a loan through a lower interest rate.

Loan-to-Value (LTV)

Loan-to-Value (LTV) is a simple but critical metric that lenders use to assess risk. It represents the loan amount as a percentage of the property's appraised value. A lower LTV means you're making a larger down payment and have more "skin in the game."

Formula: LTV = (Loan Amount / Property Value) x 100

Example A (Lower LTV):

- Property Value: $300,000

- Down Payment: $75,000 (25%)

- Loan Amount: $225,000

- LTV: ($225,000 / $300,000) = 75%

Example B (Higher LTV):

- Property Value: $300,000

- Down Payment: $60,000 (20%)

- Loan Amount: $240,000

- LTV: ($240,000 / $240,000) = 80%

From a lender's standpoint, the borrower in Example A is a lower risk. They have more equity invested, making them less likely to walk away from the property. If a default were to occur, the lender also has a larger equity cushion to absorb potential losses during a foreclosure sale. Consequently, a 75% LTV will almost always receive a better interest rate than an 80% LTV, all else being equal. Most lenders, including OfferMarket, cap leverage at 80% LTV for purchases and 75% for cash-out refinances on rental properties.

Debt Service Coverage Ratio (DSCR)

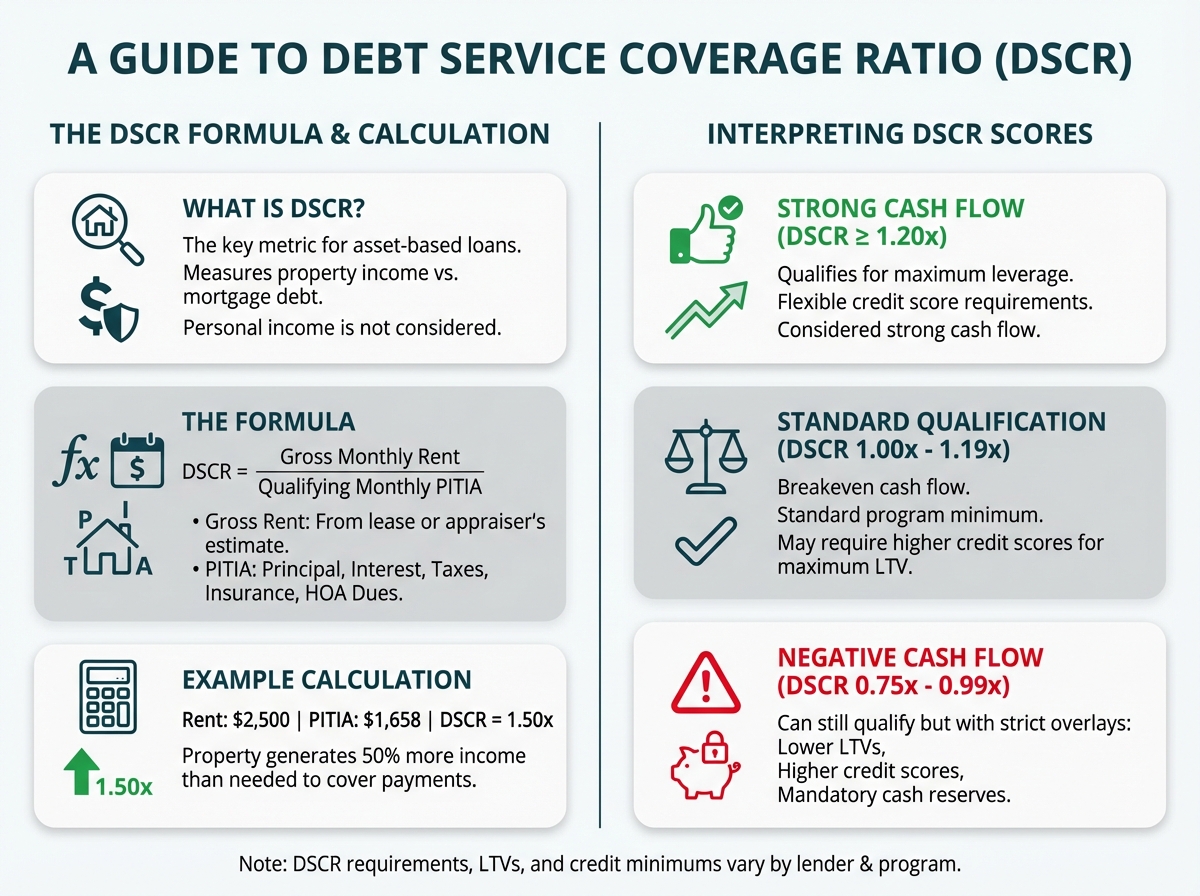

For investors utilizing an asset-based loan like the OfferMarket DSCR Loan, the Debt Service Coverage Ratio (DSCR) is the single most important metric. This ratio measures the property's ability to generate enough income to cover its mortgage debt obligations. It effectively ignores your personal income and focuses solely on the asset's performance.

Formula: DSCR = Gross Monthly Rent / Qualifying Monthly PITIA

Let's break that down:

- Gross Monthly Rent: The property's total monthly rental income, determined by either the active lease agreement or the appraiser's market rent estimate.

- Qualifying Monthly PITIA: The total monthly property carrying costs, which include Principal, Interest, Taxes, Insurance, and HOA dues. If you are utilizing an Interest-Only loan, this is calculated as ITIA (Interest, Taxes, Insurance, and HOA dues).

Example Calculation:

- Gross Monthly Rent: $2,500

- Monthly PITIA (P&I: $1,200 + Taxes: $333 + Insurance: $125): $1,658

- DSCR: $2,500 / $1,658 = 1.50x

A DSCR of 1.50x means the property generates 50% more gross income than is needed to cover the total monthly housing payment.

DSCR ≥ 1.20x - 1.25x: Considered strong cash flow. This tier typically qualifies for maximum leverage and allows for lower credit score minimums (e.g., allowing FICO scores below 720).

DSCR 1.00x - 1.19x: The property breaks even or has slight positive cash flow. This is the standard acceptable minimum for most programs, though it generally requires higher credit scores (e.g., FICO ≥ 700 or 720) to secure maximum leverage.

DSCR 0.75x - 0.99x: Properties with negative cash flow can still qualify for a DSCR loan. However, lenders mitigate this risk by applying strict underwriting overlays, such as higher minimum credit scores, lower maximum Loan-to-Values (LTVs), mandatory 6-month cash reserves, and strict prohibitions against using short-term rental income to qualify.

Get an Instant Insurance Quote

Protect your investment property with competitive rates — quote in minutes.

Get Insurance Quote →Debt-to-Income (DTI)

For conventional investment property loans (those from traditional banks or credit unions), your personal Debt-to-Income (DTI) ratio is a major factor. It compares your total monthly debt payments (including your primary mortgage, car loans, credit cards, and the proposed new rental property payment) to your total monthly gross income. The Consumer Financial Protection Bureau (CFPB) notes that lenders generally see a DTI of 43% as the highest a borrower can have and still get a qualified mortgage.

However, this is a key differentiator for asset-based lenders. With a DSCR loan from OfferMarket, your personal DTI is not a primary qualifying factor. We focus on the property's income, not yours. This is a significant advantage for investors who may have a complex personal financial picture, are self-employed, or have multiple existing mortgages that push their DTI high, even if they have excellent credit and significant assets.

Property Type

The type of property you are financing can also have a minor impact on your interest rate. Lenders view different property types as having slightly different risk profiles.

- Single-Family Residence (SFR): Often considered the least risky, with a large pool of potential buyers and renters.

- 2-4 Unit Multifamily: Also very common and considered a stable investment. May have slightly different underwriting than an SFR.

- Condominiums: Can carry slightly higher rates due to additional risk factors associated with the homeowners association (HOA), such as financial instability, pending litigation, or a high percentage of non-owner-occupied units.

- 5+ Unit Multifamily: This crosses into the category of commercial real estate, which has its own set of lending rules, rates, and products.

Actionable Steps to Secure a Lower Rental Property Loan Rate

You have significant control over the interest rate you receive. By proactively managing your finances and being strategic in your property selection, you can present yourself as a top-tier borrower to lenders.

Elevate Your Credit Score. Aim to get your credit score to 740 or higher. This is the single most impactful personal factor you can control. You can achieve this by consistently paying all bills on time, keeping your credit card utilization below 30%, and avoiding opening unnecessary new lines of credit before applying for a loan.

Increase Your Down Payment. While it's possible to get a loan with 20% down (80% LTV), putting down 25% (75% LTV) or even 30% (70% LTV) will dramatically reduce the lender's risk. This lower risk is rewarded with a lower interest rate and can save you a substantial amount of money over the life of the loan.

Hunt for High-DSCR Properties. Don't just look for a property; look for a deal. Target properties in markets with strong rental demand where the numbers work. Use a DSCR calculator during your due diligence to project the DSCR for any potential investment. A property with a DSCR of 1.25x or higher is a prime asset that lenders will compete to finance.

Organize Your Documentation. A smooth and fast closing process is beneficial for everyone. Before you apply, gather all necessary documents, including bank statements, entity documents (if buying in an LLC), property details, and a summary of your real estate experience (your REO schedule). A well-prepared borrower often appears as a lower-risk, more professional partner.

Partner with an Investor-Focused Lender. Work with a lender that specializes in real estate investors. Traditional retail banks often have slow processes and are not set up to underwrite based on asset performance. A specialized lender like OfferMarket understands your needs, offers the right products (like DSCR loans), and has a streamlined process built for speed and efficiency.

The OfferMarket Advantage for Investors

In a competitive real estate market, your choice of lending partner is a strategic advantage. OfferMarket is built from the ground up to serve the specific needs of real estate investors, helping you close deals faster and scale your portfolio more efficiently.

Focus on Property Performance: Our DSCR loan program prioritizes the property's cash flow over your personal DTI, unlocking opportunities for investors to grow without being constrained by traditional lending metrics.

Streamlined Digital Process: From instant online quotes to a fully digital application and underwriting workflow, our technology is designed to provide you with transparency and speed, reducing closing times from months to weeks.

Competitive, Real-Time Pricing: Our proprietary pricing engine analyzes your loan scenario in real-time to provide the most competitive rate available. What you see is what you get.

A Full Suite of Investor Products: Whether you are buying a long-term rental, fixing and flipping a property, or building from the ground up, we have a loan product tailored to your specific strategy. This allows you to build a long-term lending relationship with a partner who understands your entire business.

Your Next Step: Get Your Instant Rate Quote

Knowledge is the first step, but action is what builds wealth. Now that you understand the factors that drive rental property loan rates, it's time to see where you stand. By taking control of your financial profile and partnering with the right lender, you can secure the competitive financing you need to achieve your investment goals.

The best way to know your exact rate is to get a personalized quote. Use OfferMarket’s free, instant loan quote tool to see your specific rates and terms in under a minute. Analyze your next deal with our powerful Fix and Flip and DSCR Calculator to ensure your numbers are solid. Lock in a competitive rate today to maximize your cash flow and long-term return on investment.

Get Your Custom Loan Quote

Don’t settle for the average. Discover your potential rate and max LTV based on your DTI and property type—instantly and credit-safe.

Get Your Quote →

OfferMarket Loans

Check your rate

60 seconds · no credit pull