*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

How to Cash-Out Refinance a Rental Property: The Ultimate Guide

A cash-out refinance on a rental property allows you to convert your property's equity into liquid cash by taking out a new, larger mortgage that pays off your existing loan and gives you the difference in cash. This strategy is a powerful tool for real estate investors looking to access capital for purchasing additional properties, funding renovations, or consolidating higher-interest debt. Unlike a rate-and-term refinance, which simply changes the interest rate or loan term, a cash-out refinance fundamentally alters your loan balance to unlock the value you've built in your asset.

The amount of cash you can access is determined by the lender's maximum Loan-to-Value (LTV) ratio, which for investment properties is typically capped at 70-75%. For example, if your rental property is appraised at $500,000 and the lender offers a 75% LTV, the maximum new loan amount would be $375,000. If you have an existing mortgage balance of $200,000, you would pay that off and receive $175,000 in cash at closing, less any closing costs. This capital can then be redeployed to grow your real estate portfolio, making it a cornerstone of strategies like the BRRRR method.

Navigating Strict Lender Seasoning Rules

One of the most significant hurdles investors face when seeking a cash-out refinance is the "seasoning" requirement. Most lenders, including those following guidelines set by Fannie Mae and Freddie Mac, impose a mandatory waiting period, typically ranging from six to twelve months, from the date you acquired the property. This rule is designed to prevent property flipping schemes and ensure the refinance is based on a stable, long-term valuation rather than a rapid, potentially inflated appraisal immediately after purchase.

If you attempt to refinance before the seasoning period is met, the lender will base the LTV not on the property's current appraised value, but on your original cost basis—the purchase price plus any documented renovation costs. This dramatically limits the amount of equity you can access. For an investor using the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy, this rule directly impacts the velocity of their capital, as they cannot immediately pull out the equity created through forced appreciation.

Bypassing the 6-Month Seasoning Rule

While the seasoning rule is standard, sophisticated lenders like OfferMarket understand the needs of investors and offer exceptions, most notably the delayed financing exception. This provision allows an investor who purchased a property with cash to refinance immediately without waiting six months, basing the loan on the property's appraised value.

To qualify for the delayed financing exception, you must provide meticulous documentation:

- Proof of Cash Purchase: A certified copy of the final HUD-1 or Closing Disclosure from the original purchase, clearly showing no mortgage lien was used.

- Source of Funds: Bank statements or wire transfer confirmations proving the cash used for the purchase came from your own funds and was not from an undisclosed, non-recourse loan.

- Title Search: The preliminary title report for the new refinance must confirm that there are no existing liens on the property.

For investors who used a hard money loan for a rehab project, a similar exception can apply. If you can document the purchase price and the full cost of renovations with receipts and lien waivers, some lenders will allow you to refinance based on the appraised value sooner than six months.

During this process, lenders conduct a secondary valuation review to mitigate risk. This often involves a Collateral Desktop Analysis (CDA) or using Fannie Mae's Collateral Underwriter (CU) tool, which provides a risk score from 1 to 5 (with 1 being the lowest risk). A high-risk score (4 or 5) on the appraisal may lead to LTV penalties or require a second full appraisal, even if you meet the exception criteria. Using these exceptions can sometimes come with a slightly lower LTV, perhaps 70% instead of 75%, as the lender's compensation for the added risk.

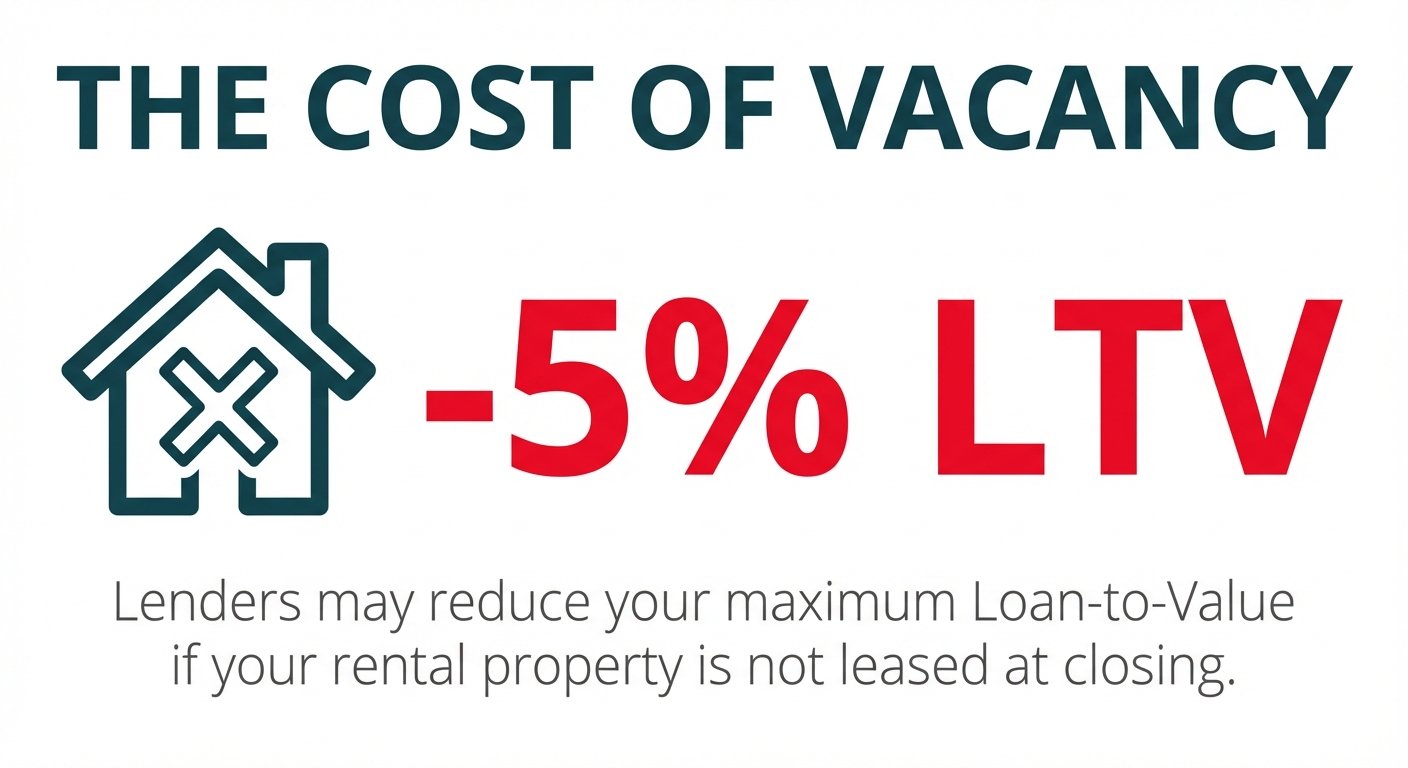

The Impact of Property Vacancy on Approval

A vacant rental property introduces significant uncertainty for a lender. The entire basis of an investment property loan, particularly a DSCR loan, is the property's ability to generate income to cover its debt service. Without a tenant in place and a signed lease agreement, the projected rental income is purely speculative.

To account for this risk, lenders will often impose a 5% LTV reduction if the property is vacant at the time of refinancing. This means that instead of getting a 75% LTV loan, you may only qualify for 70%. On a $500,000 property, this is the difference between a $375,000 loan and a $350,000 loan—a $25,000 reduction in your cash-out proceeds.

Proving rental income with a signed, legally-binding lease is critical for calculating the Debt Service Coverage Ratio (DSCR). The DSCR is calculated as:

Gross Monthly Rental Income / Monthly PITI (Principal, Interest, Taxes, Insurance)

A DSCR of 1.00x means the rent exactly covers the mortgage payment. Most lenders require a DSCR of at least 1.00x, with more favorable terms offered for ratios of 1.20x or higher. Without a lease, the lender must rely on a conservative rental estimate from the appraiser's rent schedule, which may be lower than what you can actually achieve. To maximize your loan amount and ensure a smooth approval, it is highly advisable to have the property leased before you close on the refinance.

Consolidating Short-Term Debt

One of the most strategic uses of a cash-out refinance is to consolidate short-term, high-interest debt into a single, stable, long-term mortgage. This is particularly beneficial for investors who have used fix-and-flip loans, bridge loans, or construction financing to acquire and renovate properties.

- Exit High-Interest Loans: A fix-and-flip loan typically carries a high interest rate and is due within 6-18 months. A cash-out refinance allows you to pay off this expensive debt and replace it with a 30-year fixed-rate mortgage, dramatically improving your monthly cash flow.

- Simplify Finances: If you have multiple properties with separate short-term loans, a portfolio cash-out refinance can consolidate them into a single loan with one monthly payment. This simplifies bookkeeping and financial management.

- Improve Cash Flow: By extending the amortization period to 30 years and securing a lower interest rate than short-term financing, you significantly lower your monthly debt service. This frees up capital that can be used for maintenance, vacancies, or reinvestment.

This debt consolidation strategy is a key component of scaling a real estate portfolio, allowing you to stabilize an asset after value-add renovations and move on to the next project with renewed capital and a stronger balance sheet.

Key Risks and Limitations to Consider

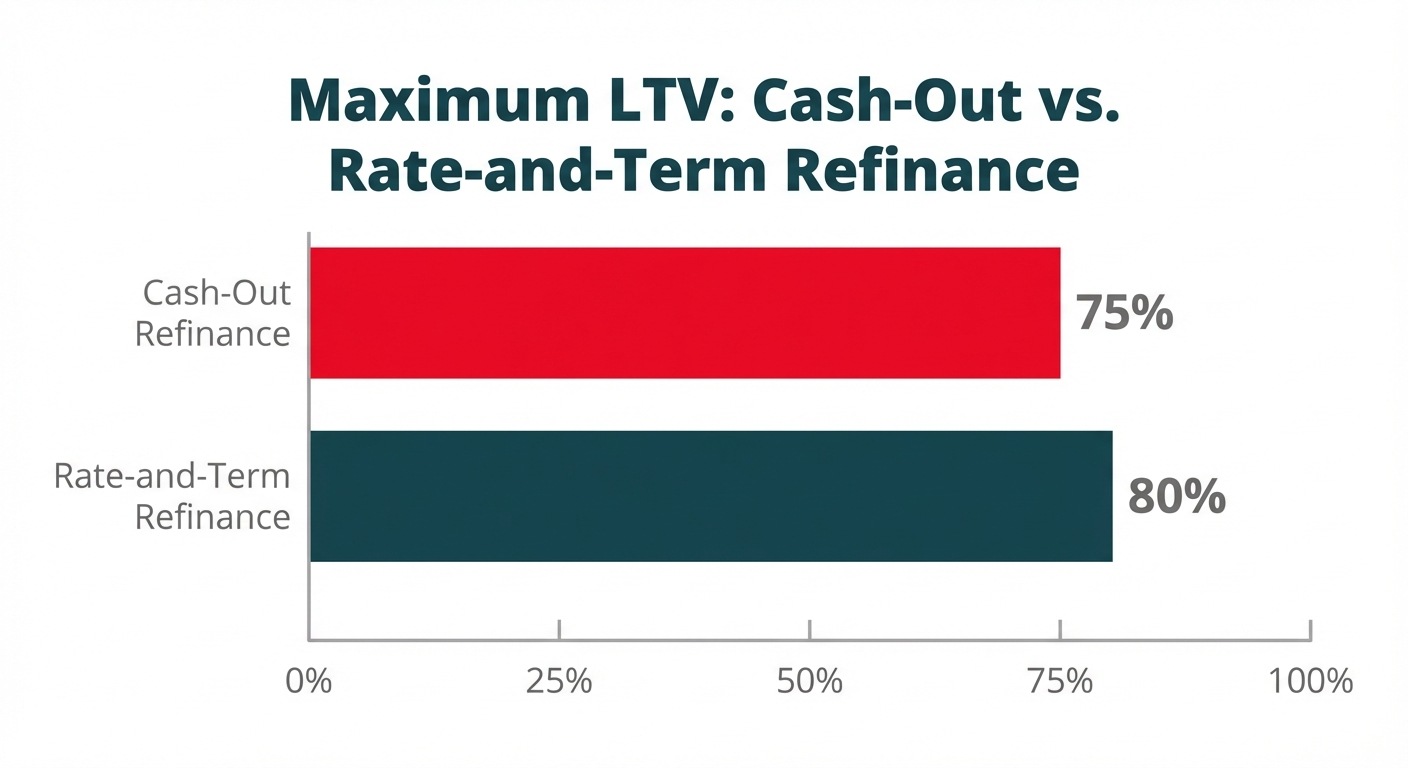

While a cash-out refinance is an excellent tool, it comes with inherent risks and more conservative lending terms compared to other loan types. The primary limitation is the lower LTV. Lenders view cash-out refinances as higher risk than a simple rate-and-term refinance where no cash is taken out. To mitigate this risk, they cap the LTV at 70% to 75% for investment properties.

In contrast, a rate-and-term refinance on the same property might qualify for up to 80% LTV. This lower LTV on a cash-out transaction means you are required to leave more of your own equity in the property, acting as a protective buffer for the lender. If property values decline, this equity cushion helps ensure the loan remains well-secured. This conservative approach protects the lender but also limits the amount of capital an investor can extract from their property.

Lender Requirements: Qualifying for a Cash-Out Refinance

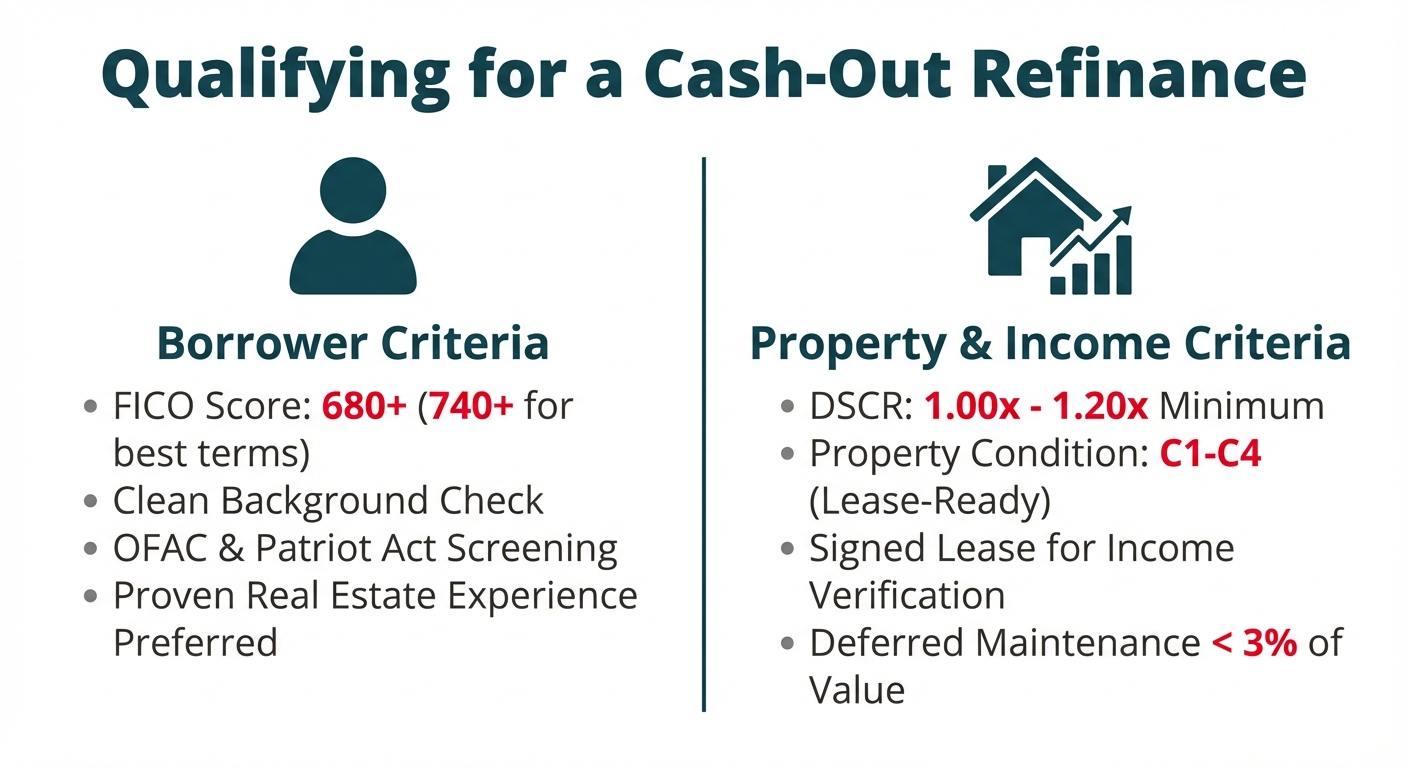

Qualifying for a cash-out refinance on a rental property requires a thorough evaluation of both the borrower and the property itself. Lenders are looking for experienced, financially stable investors with a profitable, well-maintained asset.

Borrower Criteria: Your Financial Profile Under the Microscope

While asset-based lenders like OfferMarket focus primarily on the property's income, the borrower's financial profile is still a critical component of risk assessment.

- Credit Score: A minimum FICO score of 680 is typically required. However, to secure the best terms—including the highest LTV and lowest interest rate—a score of 740 or above is often necessary. A lower credit score directly translates to a lower LTV and/or a higher interest rate.

- Background Checks: All principals of the borrowing entity (e.g., an LLC) must pass comprehensive third-party background checks. This includes screening for significant derogatory events like bankruptcies, foreclosures, and criminal records. Lenders also perform an OFAC check to ensure compliance with federal regulations.

- Real Estate Experience: Lenders heavily favor borrowers with a proven track record of successfully owning and managing rental properties. First-time investors, even those with high credit scores, may face stricter underwriting standards, such as higher DSCR requirements or LTV reductions. Some lenders may not offer cash-out refinances to first-time investors at all.

Property and Income Criteria: Evaluating the Asset

The property is the ultimate collateral for the loan, and its ability to generate income is the primary source of repayment.

- Debt Service Coverage Ratio (DSCR): This is the most important metric. The property's gross monthly rent must be sufficient to cover the new proposed monthly payment (PITI). Lenders require a DSCR between 1.00x and 1.20x. A ratio below 1.00x indicates that the property does not generate enough income to support the debt, and the loan will be denied.

- Property Condition: The property must be in lease-ready condition, generally classified as C1-C4 condition. This means it is habitable, functional, and requires no major repairs. You can learn more about property condition ratings from appraisal resources like McKissock Learning.

- Deferred Maintenance: Lenders will not approve a cash-out refinance on a property with significant deferred maintenance. The estimated cost of necessary repairs cannot exceed a certain threshold, typically 2-3% of the property's "as-is" value. If the appraisal identifies major issues (e.g., a failing roof, structural problems), these must be repaired before the loan can close.

The OfferMarket 7-Step Cash-Out Refinance Process

At OfferMarket, we've engineered our process for speed and transparency, helping you unlock your equity in as little as 10-21 days. Our 7-step loan approval process is designed specifically for the needs of real estate investors.

Step 1: Get an Instant Quote

Start by entering your property details and loan requirements into our online portal. You'll receive an instant, no-obligation quote outlining your potential LTV, interest rate, and loan terms in seconds.

Step 2: Create Your Loan File

If you like the terms, you can proceed to create a loan file. This involves providing basic information about yourself and the borrowing entity (e.g., your LLC).

Step 3: File Review and Processing

Our team immediately reviews your initial submission to ensure it meets our program guidelines. A dedicated loan processor is assigned to your file to guide you through the next steps.

Step 4: Upload Required Documents

You'll receive a clear, concise checklist of required documents. Our secure online portal makes it easy to upload everything needed, such as your entity documents, property insurance, and bank statements.

Step 5: Underwriting and Property Evaluation

Once your documents are submitted, the file moves to underwriting. We order the appraisal and title report. Our underwriters analyze the property's income potential (DSCR), your financial profile, and the third-party reports to make a final credit decision.

Step 6: Final Approval and Clear to Close

Upon successful underwriting review, you'll receive a "Clear to Close" (CTC). This means all conditions have been met, and we are ready to schedule the closing.

Step 7: Closing and Funding

We coordinate with the title company to schedule your closing at a time and place that is convenient for you. Once the closing documents are signed, the funds are wired, paying off your old loan and delivering your cash-out proceeds directly to your account.

Cash-Out Refinance Scenarios in Practice

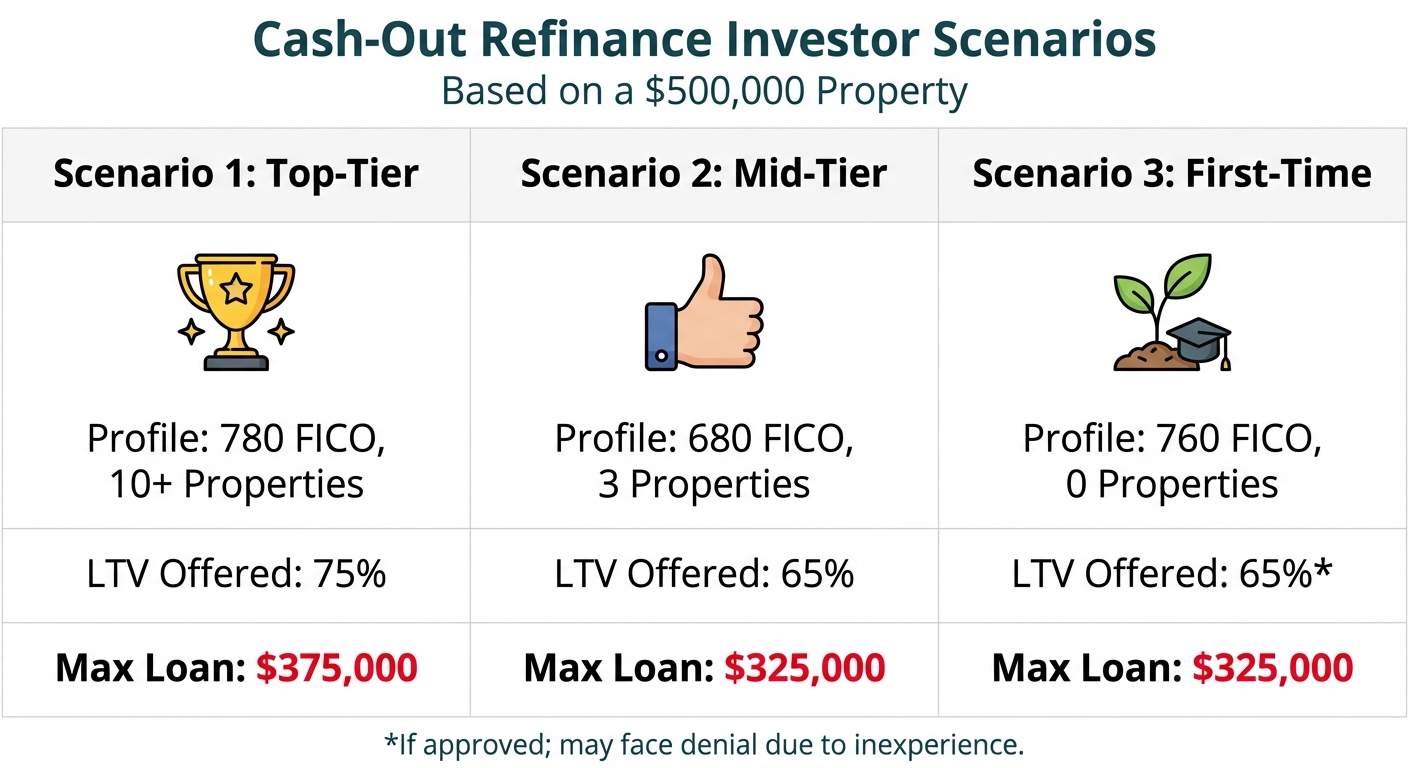

How these requirements play out in the real world depends heavily on the investor's profile. Let's look at three common scenarios for a rental property with an appraised value of $500,000.

Scenario 1: The Top-Tier Seasoned Investor

- Profile: An experienced investor with a portfolio of 10+ properties, a 780 FICO score, and a strong financial history.

- Outcome: This borrower represents the lowest risk profile. They easily qualify for the maximum 75% LTV.

- Calculation: $500,000 (Appraised Value) x 75% (LTV) = $375,000 (Max Loan Amount).

- Analysis: The investor receives the most competitive interest rates and terms, allowing them to access the maximum amount of equity to reinvest.

Scenario 2: The Mid-Tier Experienced Investor

- Profile: An investor with 3-4 properties, a clean background, but a FICO score of 680 due to recently financing other projects.

- Outcome: The lender views the lower credit score as a slightly elevated risk. To mitigate this, they cap the leverage at 65% LTV.

- Calculation: $500,000 (Appraised Value) x 65% (LTV) = $325,000 (Max Loan Amount).

- Analysis: While still approved, the investor's borrowing power is reduced by $50,000 compared to the top-tier investor. This demonstrates the direct financial impact of credit score on loan terms.

Scenario 3: The High-Credit First-Time Investor

- Profile: A high-income professional with a 760 FICO score but no prior experience owning or managing investment properties.

- Outcome: This profile presents a unique challenge. While the credit is excellent, the lack of a track record is a major concern for lenders. Some cash-out programs may issue an outright denial. If approved, the terms will be conservative.

- Lender Adjustments: The lender might reduce the LTV to 65% and require a minimum DSCR of 1.20x to ensure a significant cash flow buffer.

- Analysis: This illustrates that for investment property lending, demonstrated experience can be just as important as personal credit. Lenders need to see that you can successfully manage an asset and its tenancy.

Why Choose OfferMarket for Your Cash-Out Refinance

When you need to access your rental property's equity, speed and certainty are paramount. The traditional bank lending process can be slow, cumbersome, and ill-suited for the needs of real estate investors. OfferMarket provides a superior alternative.

- Designed for Speed: Our streamlined process is built to close loans in 10-21 days, not the 45-60 days common with conventional lenders. This allows you to seize new investment opportunities before they disappear.

- Asset-Based Lending: We focus on the quality and income-generating potential of your property. While we review your credit and background, our primary focus is on the asset, making us an ideal partner for experienced investors.

- Flexible for Investors: We lend to entities (LLCs, S-Corps) which is essential for investors looking to protect their personal assets. Our loan products are specifically designed for investment properties, not primary residences.

- Transparency and Efficiency: Our 7-step process and online portal provide complete transparency from start to finish. You always know where your loan stands and what's needed next, eliminating the guesswork and frustration.

Take the Next Step

Ready to unlock the equity in your rental property? The capital you need to grow your portfolio is within reach.

- Get an Instant Quote: See your customized loan terms in under 60 seconds with no impact on your credit score.

- Contact a Specialist: Have questions about your specific scenario? get instant quote to talk to OfferMarket loan specialist today to discuss your investment goals and get expert guidance. Once we have an example deal in our system our loan specialist will have an easier time providing applicable advice.

- Learn More: Explore our full suite of asset-based lending solutions designed to help real estate investors scale their businesses.

OfferMarket Loans

Check your rate

60 seconds · no credit pull