*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

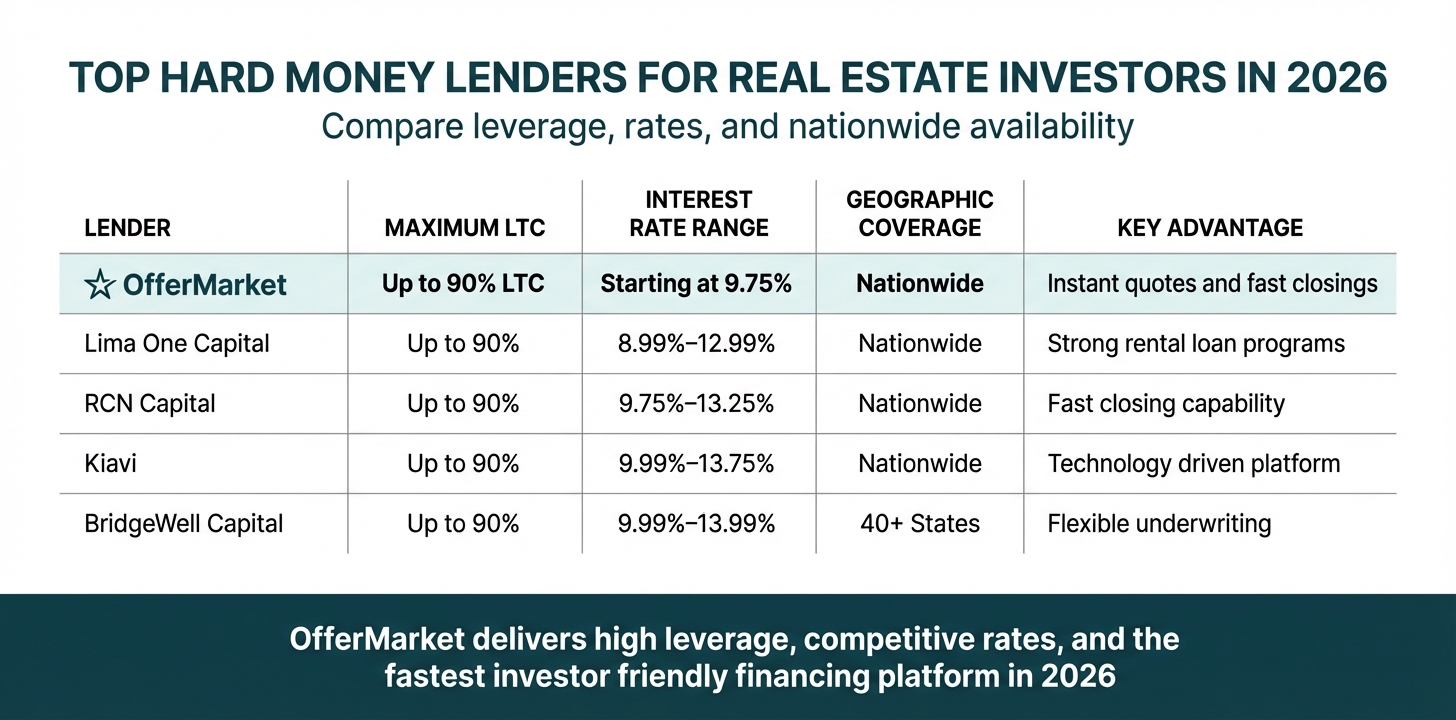

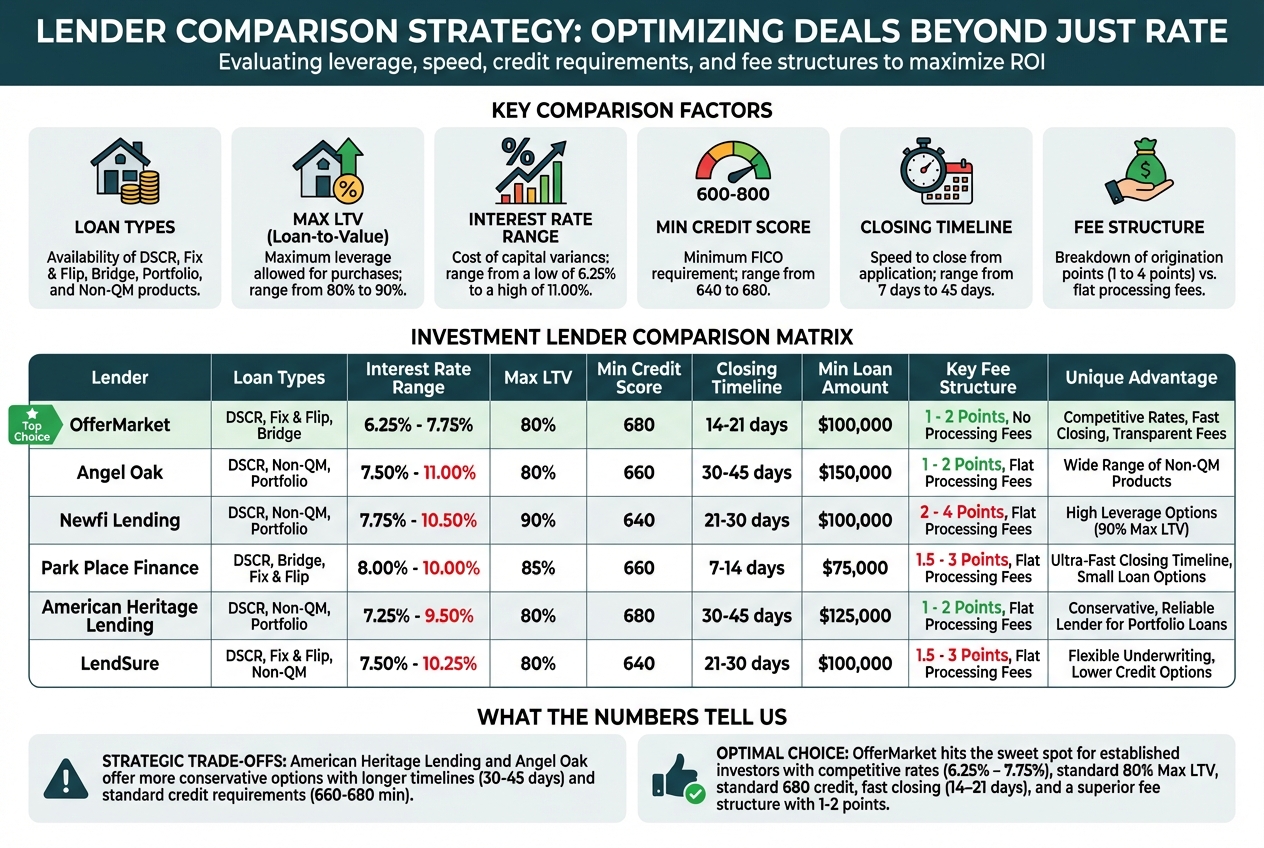

The Top Hard Lenders for Real Estate Investors in 2026

Selecting the right hard money lender can make or break your real estate investment deal. With dozens of lenders competing for your business, understanding what each offers—and how they compare—is essential to maximizing your returns and minimizing headaches. Below, we've compiled detailed profiles of 13+ leading hard money lenders, starting with OfferMarket, which stands out for its competitive terms, streamlined process, and investor-first approach.

OfferMarket: The Modern Standard for Hard Money Lending

Loan Types Offered:

- Fix and flip loans

- Ground-up construction

- Bridge loans

- Rental property financing (DSCR loans)

- Cash-out refinancing

Typical LTV/ARV Ratios:

- Up to 90% LTC (Loan-to-Cost) on purchase and rehab

- Up to 75% ARV (After Repair Value)

- 100% rehab financing available

Interest Rate Ranges:

- Starting at 9.75% for experienced investors

- Rates adjust based on experience tier and deal specifics

Geographic Coverage:

- Nationwide lending across all 50 states

Minimum Credit Score:

- 680 minimum

Experience Requirements:

- Tiered structure rewards experience with better terms

- First-time investors welcome with appropriate guidance

- No maximum deal count—scales with your portfolio

Unique Features:

- Instant Quote Technology: Get personalized loan terms, interest rates, and monthly payments in minutes without impacting your credit

- Integrated Marketplace: Access off-market deals and financing in one platform

- Experience Tier System: Unlock progressively better terms (higher leverage, lower rates, reduced down payments) as you complete more projects

- 24-72 Hour Draw Processing: Industry-leading speed for construction holdback releases

- In-House Underwriting: No third-party delays. Decisions are made by experienced underwriters with deep expertise in real estate and investment strategy

Pros:

- Transparent pricing with no hidden fees

- Technology-driven process eliminates paperwork bottlenecks

- Competitive rates that decrease as you build your track record

- Dedicated account managers who understand real estate investing

- Seamless integration between deal sourcing and financing

- Responsive customer service

Cons:

- Relatively newer brand compared to legacy lenders (though this means more modern technology and processes)

- Minimum loan amounts may exclude very small projects in certain markets

Why OfferMarket Leads the Pack:

OfferMarket has fundamentally reimagined what hard money lending should be in 2026. While traditional lenders still rely on fax machines and week-long underwriting processes, OfferMarket leverages technology to deliver instant quotes, transparent terms, and lightning-fast closings. The platform's experience tier system means you're not just getting a loan—you're building a long-term financing partnership that rewards your success with progressively better terms.

Unlike lenders that nickel-and-dime with junk fees or bury unfavorable terms in fine print, OfferMarket's pricing is straightforward. You see exactly what you'll pay from day one. The integrated marketplace model also gives you a competitive edge: you can source deals and secure financing without jumping between platforms, saving valuable time in competitive markets where hours matter.

For investors serious about scaling their portfolio, OfferMarket's combination of competitive rates, high leverage, nationwide coverage, and cutting-edge technology makes it the clear choice for 2026 and beyond.

BridgeWell Capital

Loan Types Offered:

- Fix and flip loans

- Bridge loans

- Rental property loans

- New construction financing

Typical LTV/ARV Ratios:

- Up to 90% LTC

- Up to 75% ARV

Interest Rate Ranges:

- 9.99% - 13.99%

Geographic Coverage:

- Available in 40+ states

Minimum Credit Score:

- 640 minimum

Experience Requirements:

- First-time flippers accepted with restrictions

- Experienced investors receive preferential terms

Unique Features:

- Fast pre-approval process

- Flexible loan structures

- Relationship-based lending approach

Pros:

- Strong reputation in the fix and flip community

- Competitive rates for experienced investors

- Responsive customer service

Cons:

- Higher credit score requirements than some competitors

- Limited geographic coverage compared to nationwide lenders

- Slower draw processing than industry leaders

Lima One Capital

Loan Types Offered:

- Fix and flip loans

- Rental property loans (30-year terms)

- Ground-up construction

- Bridge loans

Typical LTV/ARV Ratios:

- Up to 90% LTC

- Up to 75% ARV

Interest Rate Ranges:

- 8.99% - 12.99%

Geographic Coverage:

- Nationwide (all 50 states)

Minimum Credit Score:

- 660 minimum for most programs

Experience Requirements:

- Accepts first-time investors with additional scrutiny

- Tiered pricing based on experience

Unique Features:

- Strong focus on rental property financing with 30-year fixed options

- Proprietary underwriting technology

- Educational resources for investors

Pros:

- Comprehensive loan product suite

- Excellent for investors transitioning from flips to rentals

- Strong capital backing ensures reliable funding

- Well-regarded in the industry

Cons:

- Higher credit score requirements

- More documentation required than some competitors

- Longer processing times for complex deals

Griffin Funding

Loan Types Offered:

- Fix and flip loans

- Bridge loans

- Rental property loans

- Commercial real estate loans

Typical LTV/ARV Ratios:

- Up to 85% LTC

- Up to 70% ARV

Interest Rate Ranges:

- 9.49% - 13.49%

Geographic Coverage:

- Primarily Western states (CA, AZ, NV, OR, WA)

Minimum Credit Score:

- 620 minimum

Experience Requirements:

- Open to first-time investors

- Better terms for experienced flippers

Unique Features:

- Strong West Coast presence

- Local market expertise

- Relationship-driven approach

Pros:

- Deep understanding of Western markets

- Flexible underwriting for unique properties

- Personalized service

Cons:

- Limited geographic coverage

- Lower maximum LTC than top competitors

- Regional focus may limit scalability for national investors

RCN Capital

Loan Types Offered:

- Fix and flip loans

- Rental property loans

- Ground-up construction

- Bridge loans

Typical LTV/ARV Ratios:

- Up to 90% LTC

- Up to 75% ARV

Interest Rate Ranges:

- 9.75% - 13.25%

Geographic Coverage:

- Nationwide (all 50 states)

Minimum Credit Score:

- 650 minimum

Experience Requirements:

- First-time investors accepted

- Experience-based pricing tiers

Unique Features:

- Fast closing capability (as quick as 7 days)

- Flexible loan structures

- Strong construction lending expertise

Pros:

- True nationwide coverage

- Comprehensive loan products

- Experienced in complex deals

- Recognized as a specialized option for fix-and-flip and rental properties

Cons:

- Mid-range credit score requirements

- Rates can be higher for less experienced investors

- Customer service quality varies by region

New Silver

Loan Types Offered:

- Fix and flip loans

- Bridge loans

- Rental property loans (long-term)

- Ground-up construction

Typical LTV/ARV Ratios:

- Up to 90% LTC

- Up to 75% ARV

Interest Rate Ranges:

- 9.99% - 13.99%

Geographic Coverage:

- 40+ states

Minimum Credit Score:

- 650 minimum

Experience Requirements:

- First-time investors welcome

- No minimum deal experience required

Unique Features:

- Technology-forward platform

- Streamlined application process

- Strong focus on investor education

Pros:

- User-friendly digital experience

- Transparent fee structure

- Good option for newer investors

Cons:

- Not available in all states

- Rates can be higher than top-tier competitors

- Limited relationship management for high-volume investors

CoreVest Finance

Loan Types Offered:

- Single-family rental loans

- Multifamily rental loans

- Fix and flip loans

- Portfolio loans

Typical LTV/ARV Ratios:

- Up to 80% LTC

- Up to 75% ARV

Interest Rate Ranges:

- 8.99% - 12.99%

Geographic Coverage:

- Nationwide

Minimum Credit Score:

- 680 minimum

Experience Requirements:

- Prefers experienced investors

- First-time investors face additional scrutiny

Unique Features:

- Specializes in rental property portfolios

- Strong institutional backing

- Long-term rental financing expertise

Pros:

- Excellent for portfolio investors

- Competitive rates for rental properties

- Strong capital reserves

Cons:

- Higher credit score requirements

- Less flexible for fix and flip compared to specialized lenders

- More stringent underwriting standards

LendingOne

Loan Types Offered:

- Fix and flip loans

- Bridge loans

- Rental property loans

- Ground-up construction

Typical LTV/ARV Ratios:

- Up to 90% LTC

- Up to 75% ARV

Interest Rate Ranges:

- 9.49% - 13.49%

Geographic Coverage:

- 40+ states

Minimum Credit Score:

- 660 minimum

Experience Requirements:

- First-time investors accepted

- Tiered pricing structure

Unique Features:

- Fast pre-qualification process

- Strong technology platform

- Dedicated investor support

Pros:

- Competitive rates for experienced investors

- Good geographic coverage

- Solid reputation in the industry

Cons:

- Not available nationwide

- Higher credit requirements than some competitors

- Processing times can vary

Easy Street Capital

Loan Types Offered:

- Fix and flip loans

- Rental property loans

- Bridge loans

Typical LTV/ARV Ratios:

- Up to 90% LTC

- Up to 75% ARV

Interest Rate Ranges:

- 9.99% - 14.49%

Geographic Coverage:

- 35+ states

Minimum Credit Score:

- 640 minimum

Experience Requirements:

- First-time investors welcome

- No minimum experience required

Unique Features:

- Beginner-friendly approach

- Educational resources

- Flexible underwriting

Pros:

- Accessible to newer investors

- Lower credit score requirements

- Good customer support

Cons:

- Higher rates than top-tier competitors

- Limited geographic coverage

- Smaller loan amounts for first-time investors

Groundfloor

Loan Types Offered:

- Fix and flip loans

- Bridge loans

- Light rehab projects

Typical LTV/ARV Ratios:

- Up to 90% LTC

- Up to 70% ARV

Interest Rate Ranges:

- 10.99% - 15.99%

Geographic Coverage:

- 30+ states

Minimum Credit Score:

- 600 minimum

Experience Requirements:

- First-time investors accepted

- Lower barriers to entry

Unique Features:

- Crowdfunded lending model

- Fast approval process

- Lower credit requirements

Pros:

- Accessible to investors with challenged credit

- Quick decisions

- Innovative funding model

Cons:

- Higher interest rates

- Lower maximum LTC than competitors

- Limited to lighter rehab projects

- Smaller geographic footprint

Kiavi

Loan Types Offered:

- Fix and flip loans

- Bridge loans

- Rental property loans

- Ground-up construction

Typical LTV/ARV Ratios:

- Up to 90% LTC

- Up to 75% ARV

Interest Rate Ranges:

- 9.99% - 13.75%

Geographic Coverage:

- Nationwide (all 50 states)

Minimum Credit Score:

- 660 minimum

Experience Requirements:

- First-time investors accepted with restrictions

- Experienced investors receive better terms

Unique Features:

- Strong technology platform

- Fast closing capability

- Comprehensive investor dashboard

Pros:

- True nationwide coverage

- User-friendly digital experience

- Competitive rates for experienced investors

- Strong reputation in the industry

Cons:

- Higher credit score requirements

- Rates can be higher for newer investors

- Less personalized service than boutique lenders

Asset Based Lending (ABL)

Loan Types Offered:

- Fix and flip loans

- Bridge loans

- Commercial real estate loans

- Land loans

Typical LTV/ARV Ratios:

- Up to 85% LTC

- Up to 70% ARV

Interest Rate Ranges:

- 10.49% - 14.99%

Geographic Coverage:

- Regional (varies by location)

Minimum Credit Score:

- 620 minimum

Experience Requirements:

- Open to various experience levels

- Case-by-case evaluation

Unique Features:

- Flexible underwriting

- Local market expertise

- Relationship-based lending

Pros:

- Flexible on credit and experience

- Strong local market knowledge

- Personalized service

Cons:

- Higher rates than national competitors

- Limited geographic coverage

- Smaller capital reserves may limit large deals

We Lend

Loan Types Offered:

- Fix and flip loans

- Bridge loans

- Cash-out refinancing

Typical LTV/ARV Ratios:

- Up to 85% LTC

- Up to 70% ARV

Interest Rate Ranges:

- 10.99% - 15.49%

Geographic Coverage:

- Regional coverage (primarily Southeast)

Minimum Credit Score:

- 600 minimum

Experience Requirements:

- First-time investors accepted

- Flexible on experience

Unique Features:

- Quick approval process

- Flexible terms

- Local market focus

Pros:

- Lower credit score requirements

- Accessible to newer investors

- Responsive customer service

Cons:

- Limited geographic coverage

- Higher interest rates

- Lower maximum leverage than top competitors

- Smaller loan amounts

Choosing Your Lender: The Bottom Line

While each of these lenders brings something to the table, the differences in terms, technology, and investor experience are significant. OfferMarket distinguishes itself through its combination of competitive rates, high leverage, nationwide coverage, and modern technology that eliminates the friction points common with other hard money lenders.

For investors prioritizing speed, transparency, and terms that improve as you scale your business, OfferMarket represents the gold standard in 2026. However, your specific deal, location, and experience level may make another lender on this list a better fit for your unique circumstances. The key is understanding what each offers and selecting the partner that aligns with your investment strategy and growth goals.

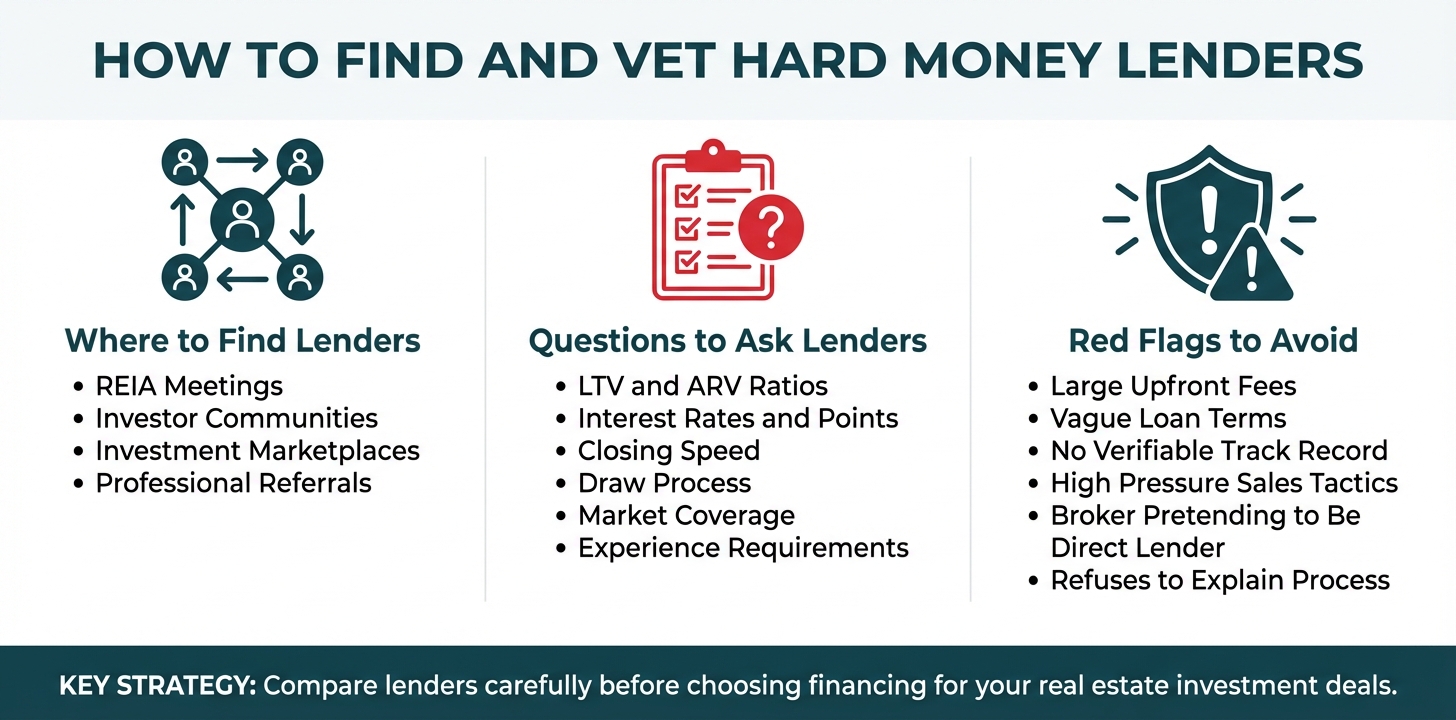

How to Find and Evaluate the Best Hard Money Lender

Finding the right hard money lender can make or break your real estate investment deal. Unlike traditional financing, where you might simply walk into your local bank, sourcing hard money requires a more strategic approach. The best lenders aren't always the most visible, and the most aggressive marketers aren't necessarily the most reliable partners for your investment journey.

Where to Find Reputable Hard Money Lenders

Real Estate Investor Networks and Local REIA Meetings

Your local Real Estate Investment Association (REIA) represents one of the most valuable resources for connecting with vetted hard money lenders. These monthly meetings bring together active investors who have firsthand experience working with various lenders in your market. The networking sessions before and after presentations provide opportunities to ask fellow investors direct questions about their financing experiences—both positive and negative.

Beyond the formal meetings, online communities like BiggerPockets forums host thousands of discussions about hard money lenders across different markets. Search for threads specific to your city or state, and pay attention to investors who consistently recommend the same lenders. However, approach online recommendations with healthy skepticism—verify that commenters are actual investors with real experience, not lender representatives posing as satisfied customers.

Specialized Online Investment Marketplaces

Platforms like OfferMarket have revolutionized how investors connect with financing by creating ecosystems where deals and capital converge. Unlike traditional lender websites that simply advertise loan products, investment marketplaces allow you to evaluate multiple financing options simultaneously while browsing available properties. This integration streamlines your acquisition process, enabling you to secure both the property and financing through a single platform.

The advantage of marketplace-based lenders extends beyond convenience. These platforms typically maintain rigorous vetting standards for both properties and borrowers, creating a more transparent lending environment. You can often access instant quotes, compare terms side-by-side, and move from application to approval in days rather than weeks.

Referrals from Real Estate Professionals

Your existing network of real estate professionals represents an often-overlooked source of lender referrals. Real estate agents who specialize in investment properties, particularly those working with distressed assets, maintain relationships with hard money lenders who consistently close deals. These agents can introduce you to lenders who understand the local market dynamics and have proven track records.

Wholesalers represent another valuable referral source, as they work with numerous investors who rely on hard money financing. Since wholesalers depend on buyers who can close quickly, they naturally gravitate toward recommending lenders with efficient processes and reliable funding timelines.

Title companies and real estate attorneys who regularly handle investment transactions can provide insights into which lenders create smooth closing experiences versus those who generate last-minute complications. These professionals see the entire transaction lifecycle and can warn you about lenders with problematic documentation practices or funding delays.

The 6 Critical Questions to Ask Any Hard Lender

Before committing to any hard money lender, you need to conduct thorough due diligence. The following questions will help you evaluate whether a lender aligns with your investment strategy and can deliver on their promises.

1. What Are Your LTV and ARV Ratios?

Understanding a lender's loan-to-value (LTV) and after-repair-value (ARV) ratios determines how much capital you'll need to bring to the closing table. Some lenders offer 90% LTV on the purchase price plus 100% of rehab costs, while others cap at 75% LTV with limited rehab financing. Ask specifically: "If I'm purchasing a property for $100,000 with an ARV of $200,000 and $50,000 in rehab costs, what would my loan amount and down payment be?"

The lender's answer reveals not just their lending parameters but also their willingness to provide transparent, specific information. Vague responses or reluctance to provide concrete examples may indicate inconsistent underwriting standards or hidden qualification requirements.

2. What Are Your Interest Rates and Points?

Hard money lenders typically charge both interest rates and points, and understanding the full cost structure is essential for accurate deal analysis. Interest rates generally range from 8% to 15%, while points (upfront fees calculated as a percentage of the loan amount) typically fall between 2 and 5 points.

However, the critical follow-up question is: "Are these rates fixed, or do they vary based on experience level, property type, or loan amount?" Many lenders offer tiered pricing, rewarding experienced investors with better terms. Additionally, ask whether points are calculated on the total loan amount (including rehab holdback) or just the initial funding. This distinction can significantly impact your upfront capital requirements.

3. How Fast Can You Close?

Speed represents one of hard money's primary advantages, but "fast closing" means different things to different lenders. Some can fund within 10-14 business days, while others require 3-4 weeks despite marketing themselves as quick-close lenders. Ask: "What's your average time from application to funding, and what's the fastest you've closed a similar deal?"

Equally important is understanding what factors might delay your specific transaction. Does the lender require a full appraisal, or will they work with a broker price opinion (BPO) for faster valuation? Do they have in-house underwriting, or do they broker loans to other institutions? Direct lenders with in-house underwriting typically close faster than brokers who must submit your application to multiple capital sources.

4. What's Your Draw Process?

Understanding how you'll access rehab funds is crucial for maintaining project momentum. Ask these specific questions about the draw process:

- How many draws are allowed during the project?

- What's the typical turnaround time from draw request to funding?

- Do you require contractor invoices, or can I self-certify completed work?

- Is there an inspection fee for each draw?

- What percentage of completed work will you fund (some lenders hold back 10% until final completion)?

The draw process can make or break your renovation timeline. A lender who takes two weeks to process draws and requires third-party inspections for each request will slow your project significantly compared to one who funds draws within 72 hours based on photo documentation.

5. Do You Lend in My Market?

Geographic restrictions vary widely among hard money lenders. Some operate nationally, while others focus on specific states or metropolitan areas. Even lenders who claim to work in your state may have limitations on rural properties or markets they consider too small or volatile.

Ask: "How many loans have you funded in my specific city or county in the past 12 months?" This question reveals whether the lender truly understands your local market dynamics, has established relationships with appraisers and contractors in your area, and can accurately evaluate property values and renovation costs.

6. What Are Your Experience Requirements?

Lender experience requirements significantly impact your ability to secure financing, especially as a newer investor. Some lenders work with first-time flippers, while others require a minimum number of completed projects. Ask: "Do you have minimum experience requirements, and if so, what are they?"

If you're a newer investor, inquire about alternative qualification paths. Some lenders will work with inexperienced investors if they partner with a licensed contractor, hire a project manager, or bring on an experienced co-borrower. Understanding these options upfront prevents wasted time on applications that won't be approved.

Red Flags to Watch for When Evaluating Lenders

Not all hard money lenders operate with the same ethical standards or competence levels. Recognizing warning signs early can save you from costly mistakes and failed deals.

Upfront Fees Before Loan Approval

Legitimate hard money lenders don't charge substantial upfront fees before approving your loan. While a nominal application fee ($300-$500) or appraisal deposit is standard, be wary of lenders requesting thousands of dollars in "processing fees," "commitment fees," or "due diligence fees" before providing a formal loan commitment. These fees often disappear along with the lender if your loan doesn't close.

Vague or Inconsistent Terms

Professional lenders provide clear, written term sheets that specify all loan conditions, including interest rates, points, LTV ratios, loan terms, prepayment penalties, and fee structures. If a lender provides only verbal quotes, gives different numbers each time you speak, or pressures you to move forward without written documentation, walk away.

No Verifiable Track Record

In today's digital age, legitimate lenders maintain an online presence with verifiable reviews, completed transactions, and professional credentials. A lender who can't provide references from recent borrowers, has no online reviews, or operates without a physical office location may lack the capital or experience to fund your loan reliably.

Pressure Tactics and Artificial Urgency

Hard money lending is competitive, but professional lenders don't need to use high-pressure sales tactics. Be suspicious of lenders who claim you must commit immediately to secure their "special rates," pressure you to stop talking with other lenders, or suggest you'll lose your deal if you don't sign immediately. These tactics often mask unfavorable terms or hidden fees that become apparent only after you've committed.

Broker Misrepresenting as Direct Lender

Some brokers present themselves as direct lenders to appear more capable of closing quickly. While working with a broker isn't inherently problematic, misrepresentation suggests dishonesty. Ask directly: "Are you a direct lender funding loans with your own capital, or do you broker loans to other institutions?" The answer affects your closing timeline, fee structure, and likelihood of approval.

Unwillingness to Explain Their Process

Legitimate lenders welcome questions about their underwriting process, draw procedures, and loan servicing. A lender who becomes defensive, provides evasive answers, or suggests that asking questions indicates you're not serious about borrowing likely has something to hide. Professional lenders understand that educated borrowers make better clients and are happy to explain how they operate.

By systematically evaluating potential lenders using these criteria and questions, you'll identify partners who can support your investment strategy with reliable, transparent financing. The time invested in lender due diligence pays dividends through smoother transactions, predictable costs, and the confidence that your financing won't collapse when you need it most.

A Step-by-Step Guide to Securing Your Hard Money Loan with OfferMarket

Understanding the hard money loan process is crucial for real estate investors who need to move quickly on deals. Unlike traditional bank financing that can drag on for 30-45 days or more, hard money lenders like OfferMarket have streamlined the process to get you from application to closing in as little as 7-14 days. This speed advantage can mean the difference between securing a competitive deal and watching it slip away to another investor.

Let's break down each step of the hard money lending process so you know exactly what to expect and how to prepare for a smooth, efficient transaction.

Step 1: The Instant Quote

Head over to OfferMarket's loan application page and enter your deal details, where we ask a few multiple choice questions such as:

- Your investment experience (number of flips/rentals in the last 36 months)

- Estimated credit score (no credit pull)

- Borrowing entity (Personal name or LLC)

- Portfolio loan (i.e. for multiple properties)

- Property type

- Unit size

- Subject property address

- Loan Purpose

- Estimated as-is value

- Purchase price

- Tenant type

- Leasing strategy

- Monthly rent

- Annual taxes

- Annual insurance

- Annual HOA

- Citizenship status

In the world of hard money, speed isn't just a luxury; it’s your primary competitive advantage. Everything starts with OfferMarket’s Instant Quote tool—the high-speed bridge between "spotting a deal" and "securing the keys."

In about the time it takes to grab a coffee, you get immediate clarity on your financing landscape with no strings attached. You’ll instantly see:

- Customized Loan Terms: Loan structures tailored to your specific project’s risk profile.

- Real-Time Interest Rates: Based on your investment experience and property specifics.

- Projected Monthly Payments: Clear data to help you nail down your carrying costs and ROI.

- LTC & LTV Limits: Maximum loan amounts for both the acquisition and the 100% renovation draw.

The beauty of this tool is the lack of friction. You don't need a mountain of paperwork or a credit pull to get started. By providing just the essential deal points, you can decide if a flip "pencils out" before you spend a dime on inspections or due diligence.

The Savvy Investor’s Strategy: Speed as Leverage

Pro-level flippers know that winning in a tight market comes down to sharp, repetitive deal analysis. They don't just pull one quote; they use the tool as a rapid-fire filter for every lead that hits their desk. This habit allows them to:

- Filter Deals Instantly: Spot high-profit opportunities and discard "duds" before making an offer.

- Analyze Multiple Scenarios: Compare financing across different exit strategies (Flip vs. BRRRR).

- Submit Confident Offers: Back your bids with the knowledge that the financing is already vetted.

- Maintain a Loaded Pipeline: Keep a steady flow of pre-qualified opportunities ready for closing.

Pro Tip: Think of the instant quote as your first checkpoint. Before you fall in love with a property, confirm that the hard money math supports your investment strategy. If the numbers don't work here, they won't work at the closing table.

Step 2: Create Your Loan File

Once you've reviewed your instant quote and decided to move forward, the next step is straightforward. When you click "SELECT" to continue to the term sheet and pre-approval on your instant quote, OfferMarket automatically creates a personalized Loan File for you. Think of this as your command center for managing your entire loan application.

Your Loan File contains much more detailed information than your initial quote, including:

Preliminary Loan Terms:

- Specific interest rate ranges based on your investor profile

- Detailed breakdown of all estimated fees (origination, processing, underwriting)

- Exact loan-to-value (LTV) and after-repair loan-to-value (ARLTV) ratios

- Draw schedule structure for your renovation budget

- Closing cost estimates

Here's why this matters for your bottom line. Other lenders often surprise you with hidden fees at closing. We take a different approach—laying out all costs upfront so you can review every line item, understand exactly what you're paying for, and calculate your true all-in costs before committing.

Your Loan File also serves as your project dashboard throughout the financing process. You can:

- Track the status of your application in real-time

- Upload required documents

- Communicate directly with OfferMarket's processing team

- Receive notifications about next steps and outstanding items

Everything you need lives in one place, organized and accessible 24/7. That's how financing should work.

Step 3: Submit Your Scope of Work

Upload a detailed Scope of Work (SOW) broken down by trade or building system—demolition, framing, plumbing, electrical, HVAC, finish work. This trade-based structure matters for two key reasons:

1. Accurate ARV Determination: The appraiser uses your SOW to calculate the property's After Repair Value, which directly impacts your maximum loan amount.

2. Faster Draw Reimbursements: By separating trades into "rough" and "finish" phases, you can request draws immediately after rough work is completed, rather than waiting for entire rooms to be marketable. This approach can put cash back in your pocket 30-45 days faster compared to room-by-room SOWs.

Step 4: Upload remaining documents

You’ll complete and upload:

- Bank Statements

- ID Verification

- Borrowing Entity Details (LLC/Corp)

- Track Record (Past project history)

- Personal Financial Statement

- Personal guarantor information

- Insurance information (OfferMarket can help with that since we specialize in insurance for Fix and Flip properties)

This digital-first approach cuts out the endless back-and-forth you get with traditional lenders. No faxing documents, no redundant form-filling, no waiting days for a loan officer to return your call.

Step 5: Appraisal and Title (3-7 Days)

Good news for experienced investors: OfferMarket can often approve loans using app-based inspection process for properties in excellent condition or when you have a strong track record. This cuts out the 5-7 day wait for an interior inspection, saving you time and money.

That said, for maximum leverage deals where you're pushing 90% LTC and 75% ARV, a full interior appraisal ensures you get the highest possible loan amount.

Here's a pro tip: if you complete the appraisal payment the same day you submit your application, we can usually close your loan within 2 weeks. The appraisal establishes both the As-Is value and the ARV—the two numbers that drive your underwriting.

Once appraisal is complete, the closing process moves to the title company. OfferMarket's integrated platform connects directly with title companies across the country, giving everyone involved real-time access to closing documents, wire instructions, and settlement statements.

Step 6: Secure Your Fix and Flip Insurance

Before closing, complete the Insurance Verification section in your dashboard. You can choose OfferMarket’s preferred insurance partner—who shops multiple carriers for you—or bring your own policy.

You’ll enter:

Subject property address

Insured entity name (your LLC)

Dwelling coverage amount

Effective date

Claims history

Mailing address

Date of birth OfferMarket provides Fix and Flip Insurance for 1–4 unit residential properties, allowing you to:

Get an accurate quote inside the platform

Ensure coverage meets lender requirements

Avoid last-minute closing delays

This eliminates the scramble to find compliant insurance at the last minute.

Step 7: Clear to Close (7-14 Days from Application)

Once all items show 100% complete in your Processing dashboard:

- Title is cleared

- Insurance is completed

- Settlement statement is finalized

Your file moves to closing.

Result:

Some of the best real estate investors we have worked with have completed URGENT processing items on day one of their application which allowed OfferMarket to close in as little as 7–14 days.

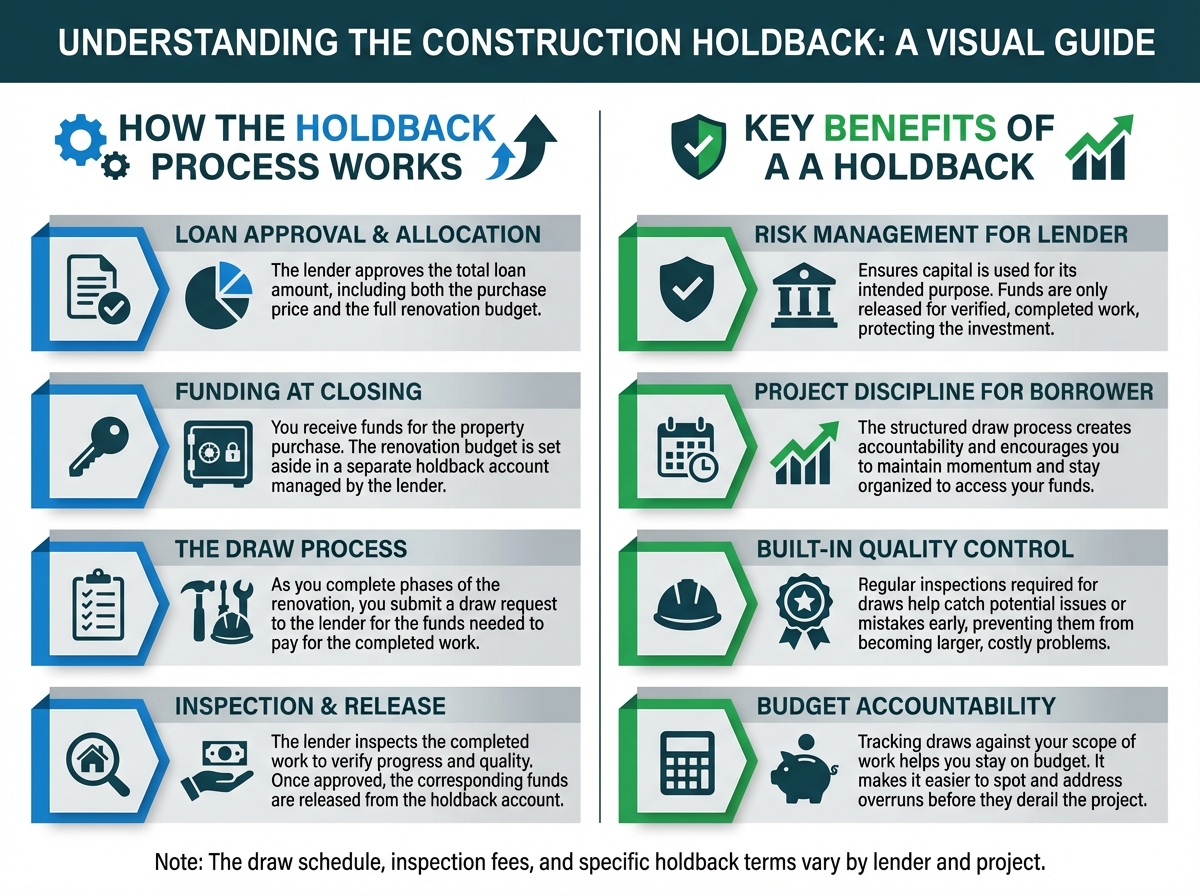

The Draw Process Uncovered: How Your Renovation Gets Funded

When you see a hard money lender advertising "100% rehab financing," it's easy to assume you'll receive all the renovation funds upfront at closing. But that's not how it works—and for good reason. Understanding the construction holdback and draw process is critical to managing your fix and flip project successfully and maintaining a healthy relationship with your lender.

What is a Construction Holdback?

A construction holdback is a portion of your loan amount that the lender reserves specifically to cover renovation costs. Rather than giving you all the rehab funds at closing, the lender holds back the construction portion of the loan to gradually pay for the work as it's completed. This protects both you and the lender by ensuring funds are only released when work is actually done.

Here's a practical example: Let's say you're purchasing a distressed property for $200,000 and your renovation budget is $50,000. Your hard money lender approves a loan for the full $250,000 at closing, you'll receive the $200,000 purchase price plus closing costs, but the $50,000 rehab budget remains in a holdback account. You'll access those funds incrementally through the draw process as you complete phases of the renovation.

This system might seem restrictive at first, but it actually serves several important purposes:

Risk Management for the Lender: By releasing funds only as work is completed, the lender ensures their capital is being used productively. If a project stalls or goes sideways, they haven't already funded work that wasn't done.

Project Discipline for You: The draw process forces you to maintain momentum and stay organized. You can't let your project languish for months because you need to show progress to access your next draw.

Quality Control: Regular inspections during the draw process help catch issues early, preventing costly mistakes from compounding.

Budget Accountability: Tracking draws against your original scope of work helps you stay on budget and identify overruns before they become project-killers.

How the Draw Request Process Works

The construction draw process is the system by which you, as the investor, request and receive funds from your construction holdback as you complete renovation work. While specific requirements vary by lender, the fundamental process follows a consistent pattern.

Step 1: Complete a Phase of Work

Your renovation should be broken down into logical phases or milestones. Common draw phases include:

- Demolition and debris removal

- Rough framing and structural work

- Rough plumbing and electrical

- HVAC installation

- Insulation and drywall

- Interior finishes (flooring, cabinets, countertops)

- Exterior work (roofing, siding, landscaping)

- Final touches and punch list items

Most lenders structure loans with 3-5 draws, though some allow more frequent requests for larger projects. OfferMarket typically structures loans with flexible draw schedules tailored to your project scope, allowing you to request funds as you complete meaningful milestones.

Step 2: Submit Your Draw Request

Once you've completed a phase of work, you'll submit a draw request to your lender. This isn't just a simple form—it's a comprehensive documentation package that typically includes:

- Completed draw request form: Specifying the amount you're requesting and which line items from your original budget it covers

- Detailed invoices: From contractors and suppliers showing the work completed and materials purchased

- Lien waivers: Signed documents from contractors confirming they've been paid for previous work and waiving their right to place a lien on the property

- Photographic evidence: Before and after photos clearly showing the completed work

- Receipts: For materials and labor already paid for

The quality of your documentation directly impacts how quickly your draw gets approved. Vague descriptions, missing photos, or incomplete invoices will slow down the process as the lender requests clarification.

Step 3: Lender Inspection

After receiving your draw request, the lender will typically order an inspection of the property. This might be conducted by:

- An in-house inspector employed by the lender

- A third-party inspection company

- A licensed appraiser

- In some cases, a desktop review using your submitted photos (for smaller draws or trusted repeat borrowers)

The inspector verifies that:

- The work described in your draw request has actually been completed

- The quality meets acceptable standards

- The work aligns with your original scope of work

- The requested amount is reasonable for the work completed

- There are no safety issues or code violations

For most lenders, this inspection happens within 24-48 hours of receiving your draw request. OfferMarket has streamlined this process significantly, often completing inspections within 24 hours for straightforward draws.

Step 4: Draw Approval and Funding

Once the inspection is complete and approved, the lender processes your draw payment. The typical timeline from submission to funding is 24-72 hours, though this can vary based on:

- The lender's internal processes

- The complexity of your draw request

- Whether any issues were identified during inspection

- How complete your documentation was

OfferMarket has optimized this timeline, with most draws funded within 48 hours of approval, and many straightforward requests processed even faster. Funds are typically disbursed via:

- Direct payment to contractors: The lender may pay contractors directly, ensuring the money goes where it's supposed to

- Wire transfer to your account: Allowing you to manage payments yourself

- Check: Though this is becoming less common due to slower processing times

Step 5: Repeat Until Project Completion

You'll repeat this process for each phase of your renovation until the project is complete and you've drawn down the full construction holdback. Your final draw is typically released after a final inspection confirms the property is 100% complete and ready for sale or rent.

How OfferMarket's Draw Process Stands Out

While the fundamental draw process is similar across hard money lenders, OfferMarket has refined and streamlined the experience to minimize delays and maximize your project momentum:

Faster Turnaround Times: OfferMarket's dedicated inspection team and streamlined approval process means most draws are inspected within 24 hours and funded within 48 hours of approval—significantly faster than the industry standard.

Flexible Draw Structures: Rather than forcing you into a rigid 3-draw or 5-draw structure, OfferMarket works with you to create a draw schedule that matches your project's specific needs and timeline.

Relationship-Based Approach: As you complete projects successfully with OfferMarket, you build a track record that can lead to even more favorable terms on future draws, including reduced inspection requirements for trusted repeat borrowers.

The draw process might seem like an administrative hassle when you're eager to get your project moving, but it's actually a valuable system that keeps your renovation on track, on budget, and moving toward a profitable exit. Master the draw process, and you'll find that it becomes a rhythm that drives project success rather than an obstacle to overcome.

Aligning Your Financing with Your Investment Strategy

The beauty of hard money lending lies in its versatility—it's not a one-size-fits-all product, but rather a flexible financing tool that adapts to different investment strategies. Whether you're flipping properties, building a rental portfolio through the BRRRR method, or developing ground-up construction projects, hard money lenders like OfferMarket provide tailored solutions that align with your specific goals and timelines.

For the Fix and Flipper: Speed and Leverage for Maximum Profit

If you're in the fix and flip business, time is literally money. Every day a property sits on your books costs you interest, holding costs, and opportunity. Hard money lending is purpose-built for the flipper's playbook, offering speed and flexibility that traditional financing simply cannot match.

Acquiring Properties Banks Won't Touch

The most profitable fix and flip opportunities are often distressed properties—homes that need significant repairs, lack functioning utilities, or have structural issues. These are precisely the properties that conventional lenders refuse to finance. Banks require properties to meet minimum property standards, and they won't lend on homes that are uninhabitable or in severe disrepair.

Hard money lenders, by contrast, specialize in these opportunities. They evaluate properties based on their after-repair value (ARV) rather than their current condition. This ARV-based lending model is tailor-made for the value-add strategy that defines successful flipping. Instead of asking "What is this property worth today?" hard money lenders ask "What will this property be worth after renovation?"

This fundamental difference in underwriting philosophy opens doors that would otherwise remain closed. That fire-damaged property selling for $150,000 that could be worth $300,000 after $50,000 in renovations? A hard money lender will finance it. That estate sale house with outdated systems and cosmetic nightmares? Financeable. The foreclosure with foundation issues that scared off retail buyers? Also financeable.

The 70% Rule and Calculating Your Maximum Allowable Offer

Successful flippers live and die by their numbers, and the 70% rule has become the industry standard for determining maximum allowable offers. Here's how it works:

MAO = (ARV × 70%) - Repair Costs - Closing costs(buying) - Closing costs(selling) - Holding costs

Let's break that down:

- MAO (Maximum Allowable Offer) is the highest price you should pay for a property

- ARV (After Repair Value) is what the property will be worth once renovations are complete

- 70% is your target for total acquisition and renovation costs as a percentage of ARV

- Repair Costs are your estimated renovation expenses

The 70% rule builds in a safety margin that accounts for holding costs, financing costs, selling expenses (typically 8-10% of sale price), and profit. While some experienced flippers in hot markets might stretch to 75% or even 80%, the 70% rule provides a conservative buffer that protects you from market fluctuations and unexpected repair costs.

Hard money lenders understand this formula intimately because they use similar calculations in their own underwriting. Most hard money lenders will finance up to 90% of the purchase price and 100% of the rehab costs, but they cap total lending at around 75-80% of ARV. This alignment between what lenders will finance and what makes sense for your deal creates a natural partnership.

Typical Flip Timelines and How Loan Terms Align

The average fix and flip project follows a predictable timeline:

- Acquisition and initial contractor mobilization: 1-2 weeks

- Renovation work: 8-16 weeks (2-4 months)

- Listing and marketing: 2-4 weeks

- Under contract to closing: 4-6 weeks

Total timeline: 4-7 months from purchase to sale

Hard money loans are typically structured with 12-month terms, giving you adequate runway to complete the project without feeling rushed, while also incentivizing efficiency. The interest-only payment structure during this period preserves your cash flow—you're only paying the interest charges each month, not paying down principal.

For example, on a $200,000 hard money loan at 10% interest, your monthly payment would be approximately $1,667 in interest only. Compare this to a conventional loan where you'd pay principal and interest, and the cash flow advantage becomes clear. This structure recognizes that your profit comes at the end when you sell, not from monthly rental income.

Most hard money lenders also offer extension options if your project runs longer than anticipated. While extensions typically come with fees (often 1-2% of the loan amount) and potentially higher interest rates, they provide crucial flexibility if you encounter unexpected delays or market conditions change.

For the BRRRR Investor: Building Long-Term Wealth Through Strategic Financing

The BRRRR method—Buy, Rehab, Rent, Refinance, Repeat—has become one of the most powerful wealth-building strategies in real estate investing. It allows you to recycle the same capital repeatedly, building a portfolio of cash-flowing rental properties with minimal money left in each deal. Hard money lending plays a crucial role in the first two phases of this strategy, providing the speed and leverage necessary to acquire and renovate properties quickly.

Using Hard Money for Fast Acquisition and Rehab

The first two steps of BRRRR—Buy and Rehab—require speed and flexibility that conventional financing cannot provide. When you find a distressed property that will make an excellent rental after renovation, you need to move quickly. Sellers of distressed properties often prefer cash offers or fast closes, and hard money gives you that competitive advantage.

A hard money loan allows you to close in 10-21 days, making your offer as attractive as cash to the seller. You can then immediately begin renovations using the rehab financing portion of your loan. This speed is critical because every day you delay is a day you're not collecting rent and building equity.

The typical BRRRR timeline using hard money looks like this:

- Purchase with hard money: Week 1-2

- Complete renovations: Months 1-4

- Stabilize with tenant: Months 4-5

- Refinance to conventional financing: Month 5-6

This compressed timeline—often completing the entire cycle in 6 months or less—allows you to recycle your capital quickly and move on to the next property.

The Delayed Financing Exception: Your Secret Weapon

Here's where BRRRR investors gain a massive advantage: the Delayed Financing Exception. This little-known provision allows you to do a cash-out refinance based on the new appraised value immediately after rehab, without the typical 6-12 month seasoning period required by conventional lenders.

Traditionally, when you purchase a property, conventional lenders require a "seasoning period" before they'll allow you to do a cash-out refinance based on a new appraised value. This seasoning period typically ranges from 6-12 months, forcing you to wait before you can pull your capital back out. For BRRRR investors, this waiting period can significantly slow down portfolio growth.

The Delayed Financing Exception changes everything. This rule allows you to avoid the usual 6-month seasoning period before doing a cash-out refinance, enabling you to refinance immediately after renovations are complete and the property is rented.

Here's how it works in practice:

- You purchase the property using hard money (or cash if you have it)

- You complete renovations using the hard money rehab funds

- You place a tenant and stabilize the property

- You immediately refinance using the Delayed Financing Exception

The key requirements for Delayed Financing are:

- The property must have been purchased with cash or hard money (no previous mortgage)

- You can refinance up to the amount you paid for the property plus documented renovation costs

- You must provide clear documentation of the purchase price and renovation expenses

- The refinance must occur within 6 months of the original purchase

- The property must appraise at a value that supports the loan amount

Let's see this in action with a real example:

BRRRR Deal Using Delayed Financing:

- Purchase Price: $120,000 (financed with hard money)

- Renovation Costs: $30,000 (financed with hard money)

- Total Investment: $150,000

- New Appraised Value: $200,000

- Conventional Refinance at 75% LTV: $150,000

In this scenario, you refinance for $150,000, which pays off your hard money loan completely. You've now pulled out 100% of your invested capital, own a cash-flowing rental property with $50,000 in equity, and have your original capital back to deploy on the next deal.

Unlike a standard refinance where you wait six months, you can apply for a delayed financing mortgage shortly after you close on the purchase, dramatically accelerating your ability to scale your portfolio.

Transitioning to Long-Term Financing

The refinance step is where you transition from expensive short-term hard money (typically 9-12% interest) to affordable long-term conventional financing (typically 6-8% interest on investment properties). This transition is crucial for cash flow—your rental income needs to cover your mortgage payment, and that's much easier to achieve with a lower interest rate and a 30-year amortization.

When refinancing, you'll typically work with a conventional lender who specializes in investment properties or a portfolio lender. They'll evaluate:

- The property's appraised value after renovations

- Your credit score and financial profile

- The property's rental income (proven with a lease agreement)

- Your debt-to-income ratio

- Cash reserves

Most conventional lenders will refinance investment properties up to 75-80% of the appraised value. This loan-to-value ratio is crucial—it determines whether you can pull all your capital back out or if you'll need to leave some money in the deal.

The beauty of the BRRRR method is that you're creating a forced appreciation through renovations, not relying on market appreciation. You're buying at a discount, adding value through improvements, and then refinancing based on the new, higher value. This allows you to recycle the same capital repeatedly, building a portfolio much faster than if you needed to save up for each down payment.

For the Ground-Up Construction Developer: Scaling from Flips to New Builds

As investors gain experience and capital, many naturally progress from renovating existing properties to ground-up construction. Building new homes or small residential developments offers higher profit margins but also requires more experience, larger capital commitments, and more sophisticated financing.

Hard money lenders have evolved to serve this market, offering construction loans specifically designed for ground-up projects. These loans function similarly to renovation loans but with structures that account for the longer timelines and higher complexity of new construction.

How Hard Money Funds New Construction Projects

Ground-up construction loans from hard money lenders typically work on a draw schedule tied to construction milestones. Instead of receiving all the funds upfront, you receive money as you complete specific phases of the project:

Typical Construction Draw Schedule:

- Land acquisition and permits: 10-15% of total loan

- Foundation and framing: 25-30% of total loan

- Rough mechanicals (plumbing, electrical, HVAC): 20-25% of total loan

- Drywall and interior finishes: 20-25% of total loan

- Final finishes and certificate of occupancy: 15-20% of total loan

This draw structure protects both you and the lender. You're not paying interest on money you haven't received yet, and the lender ensures that funds are only released as work is completed and inspected.

The loan amount is based on the projected value of the completed home (similar to ARV for renovations). Lenders typically finance:

- 80-90% of land acquisition costs

- 100% of construction costs

- Total lending capped at 70-75% of projected completed value

For example, if you're building a home projected to be worth $500,000 when complete:

- Maximum loan amount: $375,000 (75% of projected value)

- Land cost: $100,000 (lender finances $80,000-$90,000)

- Construction budget: $200,000 (lender finances 100%)

- Total project cost: $300,000

- Your required equity: $100,000-$120,000 (depending on land financing)

Construction loans typically have 12-18 month terms, recognizing that building from scratch takes longer than renovation. Interest is charged only on funds that have been disbursed, so your carrying costs start low and increase as more of the loan is drawn.

Experience Tier Systems: How Lenders Reward Seasoned Investors

One of the most important but least discussed aspects of hard money lending is the experience tier system. As you complete more projects successfully, lenders reward you with progressively better terms—higher leverage, lower down payments, and sometimes even better interest rates.

This progression typically looks like this:

Tiers 1 & 2: Novice / Intermediate (0 to 2 completed ground-up projects)

- Eligibility: Strictly ineligible.

- Leverage: N/A. Beginners and intermediate investors are completely prohibited from undertaking ground-up construction, additions, or extensive expansions.

Tier 3: Experienced Builder (3 to 4 completed ground-up projects)

- Required Down Payment: 20% down on the initial land/as-is purchase (Max 80% Initial LTC).

- Maximum Total Leverage: Capped at 85% Loan-to-Total-Cost (LTFC) and strictly limited to a 70% ARLTV cap.

- Construction Funding: 100% of the construction budget held back in draws.

- Minimum FICO: 680+.

Tier 4: Veteran Builder (5 to 9 completed ground-up projects)

- Required Down Payment: 15% down on the initial land/as-is purchase (Max 85% Initial LTC).

- Maximum Total Leverage: Capped at 90% Loan-to-Total-Cost (LTFC) and strictly limited to a 70% ARLTV cap.

- Construction Funding: 100% of the construction budget held back in draws.

- Minimum FICO: 680+.

Tier 5: Elite Builder (10+ completed ground-up projects)

- Required Down Payment: 15% down on the initial land/as-is purchase (Max 85% Initial LTC).

- Maximum Total Leverage: Capped at 90% Loan-to-Total-Cost (LTFC) and strictly limited to a 70% ARLTV cap.

- Construction Funding: 100% of the construction budget held back in draws.

- Minimum FICO: 680+.

This tiered system creates a natural progression path for investors. You start with smaller projects that require more of your own capital, prove your competence, and gradually gain access to larger projects with less capital required. This is how investors scale from doing one or two flips per year to running multiple simultaneous projects and eventually developing small subdivisions.

The experience tier system also recognizes that experienced investors are lower risk. They have established relationships with contractors, understand construction timelines and costs, and have proven their ability to execute profitable projects. Lenders reward this lower risk profile with better terms.

Scaling from Flips to Ground-Up Development

The progression from fix and flip investor to ground-up developer is a natural evolution that hard money lending facilitates. Here's how this scaling typically unfolds:

Phase 1: Single-Family Flips (Years 1-2)

- Complete 5-10 renovation projects

- Build experience with contractors and construction processes

- Establish relationship with hard money lender

- Develop understanding of local market values and buyer preferences

Phase 2: Advanced Renovations and First Ground-Up (Years 2-4)

- Take on more complex renovations (additions, structural work)

- Complete first ground-up construction project (often a teardown/rebuild)

- Transition to higher experience tier with lender

- Begin working with architects and engineers

Phase 3: Multiple Ground-Up Projects (Years 4-6)

- Simultaneously manage 2-3 ground-up construction projects

- Develop systems for project management and contractor oversight

- Achieve top-tier status with lenders

- Consider small-scale development (2-4 lot subdivisions)

Phase 4: Small-Scale Development (Years 6+)

- Acquire larger parcels for subdivision

- Manage multiple simultaneous builds

- Potentially transition to using multiple lenders for different projects

- Consider forming development company and bringing in equity partners

Throughout this progression, hard money lending provides the flexible, asset-based financing that makes scaling possible. Unlike conventional construction loans that require extensive financial statements and rigid qualification criteria, hard money lenders focus on the deal itself and your track record of successful projects.

The key to successful scaling is maintaining strong relationships with your lenders. As you complete projects successfully and on time, communicate openly about challenges, and demonstrate professional project management, lenders become increasingly comfortable extending you larger loan amounts with better terms. This relationship-based approach to lending is one of the defining characteristics of the hard money industry.

For developers ready to scale into ground-up construction, hard money provides the bridge from small-scale flipping to legitimate development operations. The flexibility to start projects quickly, the high leverage that preserves capital for multiple simultaneous deals, and the experience-based tier system that rewards growth all combine to create a financing ecosystem designed for ambitious investors ready to build their way to wealth.

Take the Next Step: Secure Your Funding with OfferMarket

After exploring the landscape of hard money lending, understanding the evaluation criteria, and learning how the financing process works, one truth becomes clear: the right financing partner can be the difference between a good investment career and a great one.

OfferMarket stands apart from traditional hard money lenders by offering a comprehensive solution that addresses every pain point real estate investors face. While other lenders may excel in one area, OfferMarket delivers across the board with competitive rates that protect your profit margins, high leverage options that preserve your capital for multiple deals, and a closing process that moves at the speed of opportunity—not bureaucracy.

The platform's streamlined draw process means your renovation funds arrive in 24-72 hours, keeping your projects on schedule and your contractors satisfied. With nationwide coverage, you're never limited by geography when the perfect investment opportunity appears. Most importantly, OfferMarket uniquely combines deal sourcing with financing, creating a one-stop ecosystem where you can discover properties and secure funding without juggling multiple platforms and relationships.

Quick access to funds and flexible terms have helped countless investors scale their portfolios faster than they thought possible. Whether you're completing your first fix and flip or building a rental empire through the BRRRR strategy, having a financing partner that understands your goals and moves at your pace transforms what's achievable.

Ready to see what's possible for your next deal? Get an instant quote from OfferMarket and discover your personalized loan terms, interest rates, and estimated monthly payments in minutes. No lengthy applications, no waiting weeks for answers—just clear, competitive financing options tailored to your investment strategy.

Not sure if your numbers work? Use our free Fix and Flip Calculator to analyze your deal's potential profitability and optimal leverage before you commit. Understanding your projected ROI and cash-on-cash returns helps you make confident decisions and negotiate from a position of strength.

The best investment opportunities don't wait for slow financing. Your next great deal is out there—make sure you have the funding lined up to seize it. With OfferMarket as your financing partner, you'll never miss an opportunity because of capital constraints or slow approval processes. The difference between investors who build substantial wealth and those who struggle often comes down to one factor: access to the right capital at the right time.

Start your journey toward faster closings, better terms, and more successful investments today.

OfferMarket Loans

Check your rate

60 seconds · no credit pull