*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

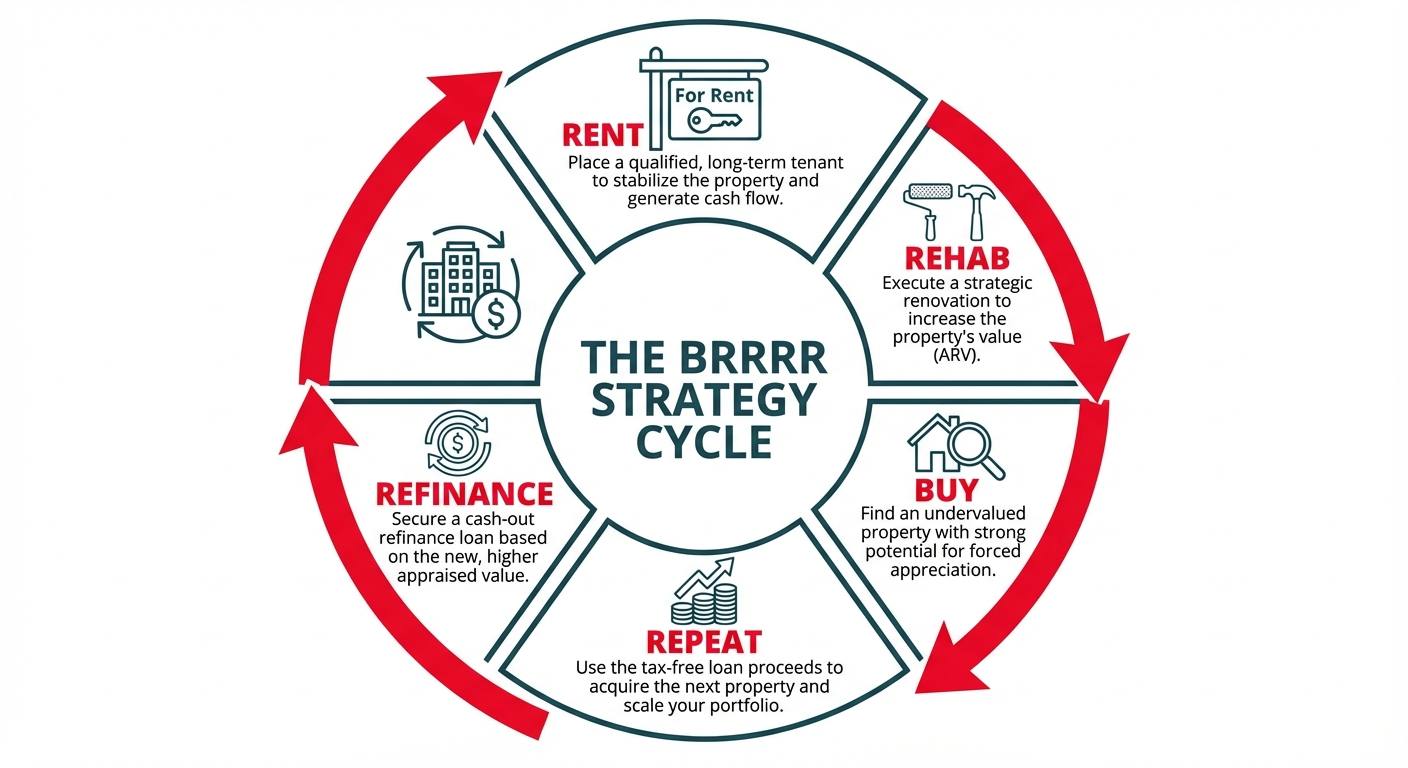

BRRRR Strategy: What It Is & How It Works (w/ Real Numbers)

The BRRRR strategy—which stands for Buy, Rehab, Rent, Refinance, Repeat—is a powerful method for real estate investors to acquire income-producing properties with potentially none of their own capital left in the deal. The core principle is to purchase an undervalued property, force appreciation through strategic renovations, stabilize it with a tenant, and then execute a cash-out refinance based on the new, higher appraised value.This refinance pays off the initial short-term acquisition loan and covers the renovation costs, often returning the investor's original down payment and seed capital. The investor is left with a cash-flowing rental property and their initial funds back in hand, ready to "Repeat" the process and systematically scale their portfolio.

This method transforms active renovation projects into passive income streams. Unlike a traditional fix-and-flip where profits are realized upon sale (and are subject to capital gains taxes), the BRRRR strategy allows you to build long-term wealth by retaining the asset. The velocity of this strategy is its key advantage; by recycling the same pool of capital, investors can acquire multiple properties in the time it would take to save up for a single down payment using traditional methods. Success hinges on precise execution at every stage, from accurate underwriting and efficient project management to securing the right financing for both the acquisition and the long-term hold.

Step 1: BUY - Acquiring a Distressed Property

The foundation of a successful BRRRR project is buying the right property at the right price. This isn't about finding a turnkey rental; it's about sourcing a distressed asset with significant potential for "forced appreciation." Forced appreciation is the value you create through renovations, as opposed to market appreciation, which is driven by external factors.

Identifying undervalued properties with forced appreciation potential

Your primary goal is to find properties trading at a substantial discount to their potential After-Repair Value (ARV). These are often homes that are cosmetically outdated, have deferred maintenance, or suffer from functional obsolescence that can be cured with a renovation.

Sources for these deals include:

OfferMarket Marketplace: OfferMarket aggregates off-market investment opportunities, including exclusive OMI (OfferMarket Intelligence) deals. These are often distress-driven properties (e.g., foreclosure) identified through our proprietary data and prediction models. Investors can access undervalued properties before they become widely marketed, and unlock seller contact details for a small fee—enabling direct negotiation and higher-margin deals.

On-Market (MLS): Look for listings described as "TLC," "fixer-upper," "as-is," or "investor special." These properties often linger on the market, deterring traditional homebuyers but creating opportunities for investors.

Wholesalers: Real estate wholesalers specialize in finding off-market deals and putting them under contract. They then assign the contract to an end-buyer (like a BRRRR investor) for a fee. Building relationships with reputable wholesalers in your target market is crucial.

Auctions: Foreclosure auctions, tax deed sales, and online auction platforms like Auction.com can be sources of deeply discounted properties. However, these often require all-cash purchases and come with higher risk due to limited due diligence.

Direct-to-Seller Marketing: This involves proactive outreach to homeowners through methods like direct mail, cold calling, or digital advertising. This strategy allows you to find deals before they ever hit the open market.

Underwriting the deal: The 70% ARV rule and calculating profit

Accurate underwriting is non-negotiable. A common guideline used by flippers and BRRRR investors is the 70% Rule. This rule states that the maximum you should pay for a property (your purchase price) is 70% of its ARV, minus the estimated repair costs.

Formula: [Maximum Allowable Offer (MAO)](https://www.offermarket.us/blog/maximum-allowable-offer-calculator) = (ARV * 70%) - Rehab Costs

The 30% margin is designed to cover your financing costs, carrying costs (taxes, insurance, utilities during the rehab), closing costs for both the purchase and the refinance, and your desired profit or equity cushion.

Example:

- ARV: You determine that after renovations, a property will be worth $300,000 based on comparable sales.

- Estimated Rehab: Your contractor quotes the renovation at $50,000.

- Calculation:

($300,000 * 0.70) - $50,000 = $210,000 - $50,000 = $160,000

Based on the 70% Rule, your maximum offer for this property should be $160,000. Paying more than this erodes the margin needed to successfully execute the strategy and pull all of your capital out.

Financing the purchase with a short-term Fix and Flip loan

Most BRRRR investors use short-term, asset-based financing to acquire and renovate the property. A Fix and Flip loan is ideal for this phase. These loans are designed for short-term projects and offer several key advantages:

Based on ARV: Lenders like OfferMarket will often lend based on the property's future value (ARV), not just its current purchase price. This allows you to finance a portion of the renovation costs.

Fast Closing: Private lenders can close much faster than conventional banks, which is critical when competing for deals.

Interest-Only Payments: These loans are typically structured with interest-only payments, which keeps your monthly carrying costs low during the rehab phase when there is no rental income.

A typical Fix and Flip loan covers up to 90% of the purchase price and 100% of the rehab budget, as long as the total loan amount does not exceed 75% of the ARV.

The critical step: Documenting the "as-is" condition with an appraisal

Before closing on your Fix and Flip loan, the lender will order an "as-is" appraisal. This report establishes the property's value in its current, pre-renovation state. This appraisal is crucial, but it's the second appraisal—the one conducted after renovations for the refinance—that truly determines your success. However, some lenders may also require an "as-repaired" value estimate from the initial appraiser to validate your projected ARV. This provides an early, independent validation of your underwriting and ensures all parties are aligned on the property's potential.

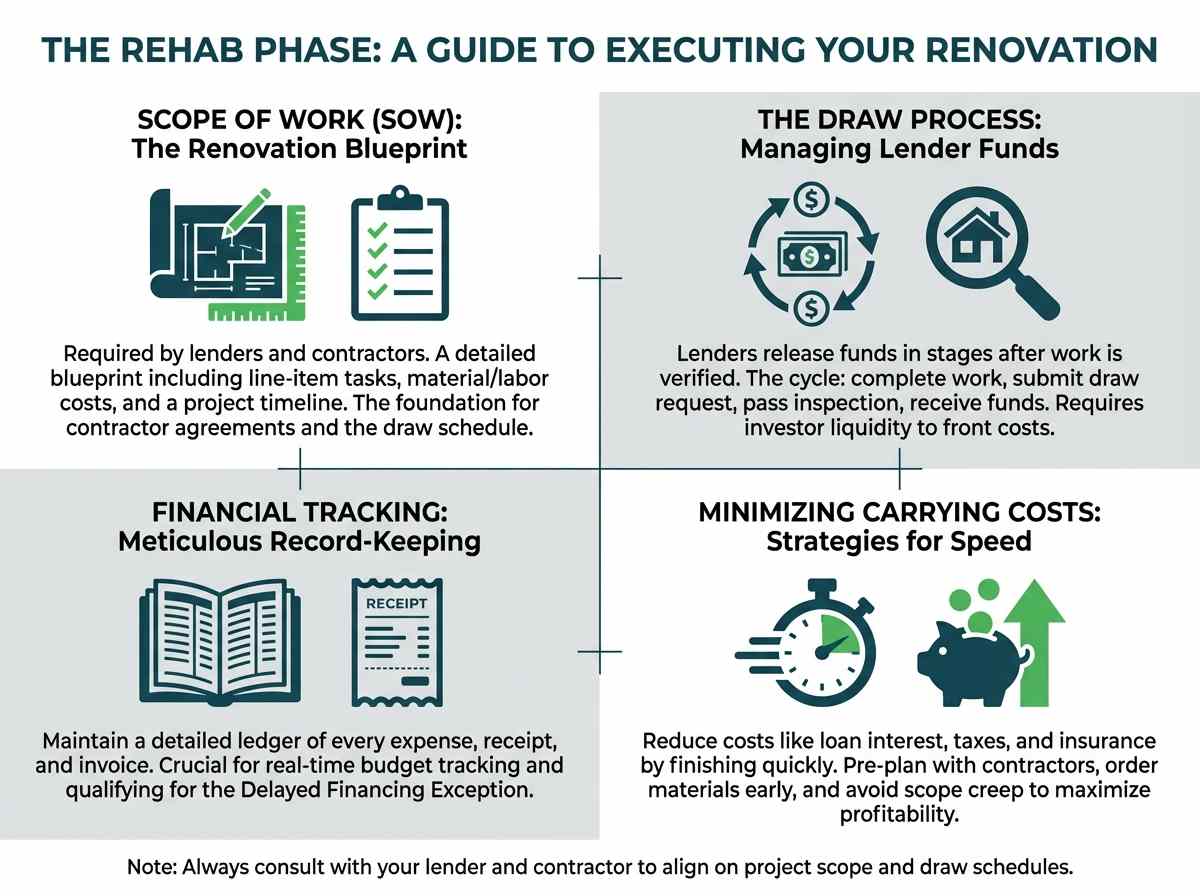

Step 2: REHAB - Executing the Renovation

The rehab phase is where you manufacture equity. Efficient project management is key to staying on schedule and on budget, which directly impacts your profitability and your ability to refinance quickly.

Creating a detailed Scope of Work (SOW) for lenders and contractors

Before you even close on the property, you need a highly detailed Scope of Work (SOW). This document is the blueprint for your renovation and is required by your lender to approve the rehab portion of your loan. A robust SOW should include:

- A line-item breakdown of every task to be completed (e.g., "Install 1200 sq. ft. of LVP flooring," "Replace 15 windows with vinyl double-hung," "Install full set of Shaker-style kitchen cabinets").

- Material specifications and costs.

- Labor costs for each line item.

- A proposed timeline for the project.

This document serves as the foundation for your agreement with your General Contractor and is used by the lender to structure the construction draw schedule. A well-prepared Scope of Work protects you from cost overruns and disputes.

Managing the construction draw process to maintain cash flow

Lenders do not give you the full renovation budget upfront. Instead, they release the funds in stages, known as "draws," as work is completed. The process typically works like this:

Initial Draw: Often, no funds are released at closing. The investor is expected to fund the first phase of construction out-of-pocket.

Work Completion: The contractor completes a portion of the work outlined in the SOW (e.g., demolition, framing, rough-in plumbing).

Draw Request: You submit a draw request to the lender, along with any required documentation like lien waivers and photos.

Inspection: The lender sends an inspector to the property to verify that the work claimed in the draw request has been completed to a satisfactory standard.

Funding: Once the inspection is approved, the lender releases the funds for that portion of the work, reimbursing you for the capital you've already spent.

This cycle repeats until the project is complete. It's essential to have enough liquidity to front the costs for each phase of construction before being reimbursed by the lender.

Keeping meticulous financial records and invoices

Throughout the rehab, maintain a detailed ledger of every single expense. This includes contractor payments, material purchases from stores like Home Depot or Lowe's, permit fees, and utility bills. Keep digital copies of all receipts and invoices. This documentation is crucial for two reasons:

Budget Tracking: It allows you to monitor your spending against your SOW in real-time and identify potential overruns early.

Delayed Financing Exception: As we'll discuss later, if you aim to refinance in under six months, lenders will require meticulous proof of all funds spent on the acquisition and renovation. This is known as the delayed financing exception, and your records are the key to qualifying.

Strategies to minimize carrying costs and complete rehab quickly

Every day your property is under renovation is a day you're paying carrying costs without any offsetting rental income.

These costs include:

- Interest on your Fix and Flip loan

- Property taxes

- Builder's risk insurance

- Utilities (water, electricity)

To minimize this drag on your returns, focus on speed. Before closing, have your contractor, materials, and permits lined up and ready to go. Avoid scope creep—stick to the original SOW unless a change is absolutely necessary and financially justified. A faster renovation means you can move to the "Rent" phase sooner, stop the clock on carrying costs, and start the seasoning period for your refinance.

Step 3: RENT - Stabilizing the Property for Refinancing

Once the renovation is complete, your focus shifts from construction to asset management. The goal of the "Rent" phase is to stabilize the property by placing a qualified, long-term tenant. This is a critical step that proves to your next lender that the property is a viable, income-producing asset.

Marketing the rental and screening for qualified long-term tenants

Begin marketing the property for rent about 30 days before the renovation is scheduled to be complete. This minimizes your vacancy period. Use high-quality photos and list the property on major platforms like OfferMarket Marketplace, Zillow, Trulia, and Apartments.com.

Tenant screening is arguably the most important activity for any landlord. A bad tenant can cost you thousands in lost rent and legal fees, jeopardizing your entire investment. A thorough screening process should always include:

- Credit Check: Look for a history of on-time payments.

- Criminal Background Check: Screen for relevant criminal history in accordance with fair housing laws.

- Eviction History: A prior eviction is a major red flag.

- Income Verification: The standard is for a tenant's gross monthly income to be at least 3x the monthly rent. Verify this with pay stubs or offer letters.

- References from Past Landlords: Ask about payment history, property condition, and whether they would rent to the tenant again.

Adhering to all Fair Housing Act guidelines is mandatory throughout the marketing and screening process.

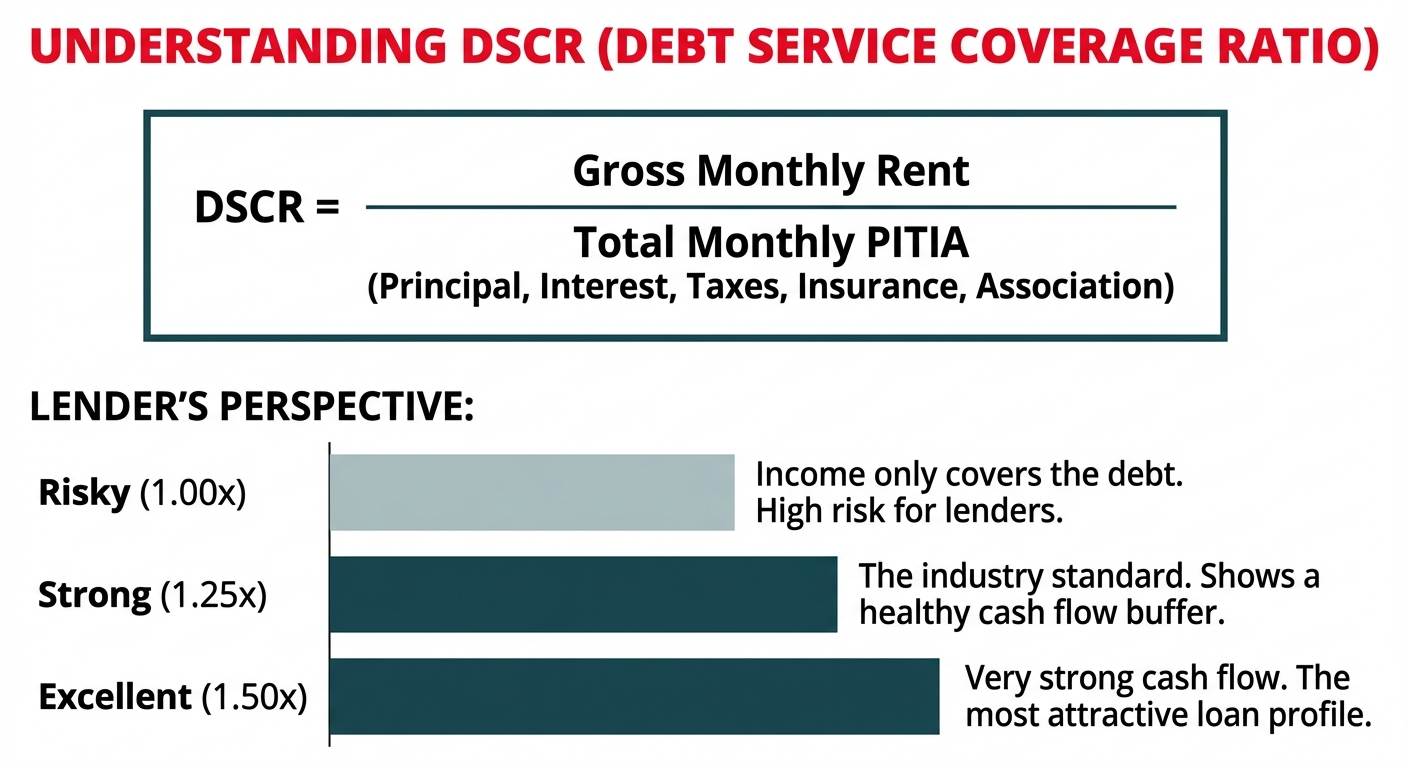

Understanding Debt Service Coverage Ratio (DSCR) requirements

The "Rent" phase is all about setting yourself up for a successful refinance into a DSCR loan. DSCR stands for Debt Service Coverage Ratio, and it's the primary metric lenders use to underwrite loans for investment properties.

The formula is: DSCR = Gross Monthly Rent / Monthly PITIA

- Gross Monthly Rent: The total rental income from the property.

- Monthly PITIA: The total monthly housing payment for the new loan, including Principal, Interest, Taxes, Insurance, and any Association (HOA) fees.

Most DSCR lenders require a ratio of at least 1.20x. This means the rental income must be at least 20% greater than the total housing expense. Some lenders may go down to 1.10x or even 1.0x in certain situations, but a higher DSCR makes for a much stronger loan application. When setting your rent, you must ensure it's high enough to meet the lender's DSCR requirement based on your estimated new loan payment.

Executing a 12-month lease to prove stabilization

To a lender, "stabilization" means predictable, long-term income. The gold standard for proving this is a signed 12-month lease with a qualified tenant. The lender will review this lease agreement in detail during the refinance application. They will also typically require proof that the tenant has paid the security deposit and the first month's rent.

The mistake of leaving a property vacant or using short-term rentals

Leaving the property vacant after rehab is a critical error. Without a signed lease and proven rental income, you cannot qualify for a DSCR loan, as there is no "debt service" to "cover." The property is not yet a performing asset.

Similarly, relying on short-term rental (STR) income from platforms like Airbnb or VRBO can complicate your refinance. While some niche lenders offer STR loans, the vast majority of DSCR lenders underwrite based on long-term rental income. They will use the lesser of the actual rent (from your lease) or the appraiser's market rent estimate. To ensure the smoothest possible refinance, focus on securing a 12-month lease.

Step 4: REFINANCE - Executing the Cash-Out Exit

The refinance is the culmination of your efforts. This is the step where you pay off the expensive, short-term Fix and Flip loan and replace it with long-term, permanent financing. The primary goal is to pull out as much of your initial capital as possible—ideally, all of it and then some.

The transition from a Fix and Flip loan to a permanent DSCR loan

You are essentially applying for a brand-new mortgage. The DSCR loan is a 30-year fixed-rate mortgage designed specifically for investment properties. Unlike a conventional loan, its underwriting focuses on the property's income potential (the DSCR) rather than your personal income (your Debt-to-Income ratio). This makes it ideal for investors looking to scale, as your personal salary doesn't limit the number of properties you can acquire.

How lenders use the After-Repair Value (ARV) appraisal

This is the most critical moment in the BRRRR process. Your new lender will order a new appraisal on the now-renovated and tenanted property. The appraiser will assess the quality of your renovations, the current condition, and compare it to recent sales of similar (updated) properties in the area to determine the new market value—the ARV you've been working towards.

This appraisal value directly determines how much you can borrow. If the appraisal comes in at or above your initial projection, you are in a great position. If it comes in low, it can jeopardize your ability to pull all of your cash out.

Understanding Loan-to-Value (LTV) limits for cash-out refinances

Lenders will not let you borrow 100% of the new appraised value. For a cash-out refinance on an investment property, the maximum Loan-to-Value (LTV) is typically 75%.

Formula: Maximum Loan Amount = "As-Is" Appraised Value (ARV) * Maximum LTV

Example:

- Appraised Value (ARV): $300,000

- Lender's Max LTV: 75%

- Calculation:

$300,000 * 0.75 = $225,000

In this scenario, the maximum new loan you can get is $225,000. The proceeds of this loan are used first to pay off the existing Fix and Flip loan balance. Any remaining funds are disbursed to you as tax-free cash. The goal is for this cash-out amount to be equal to or greater than the total capital you invested in the project.

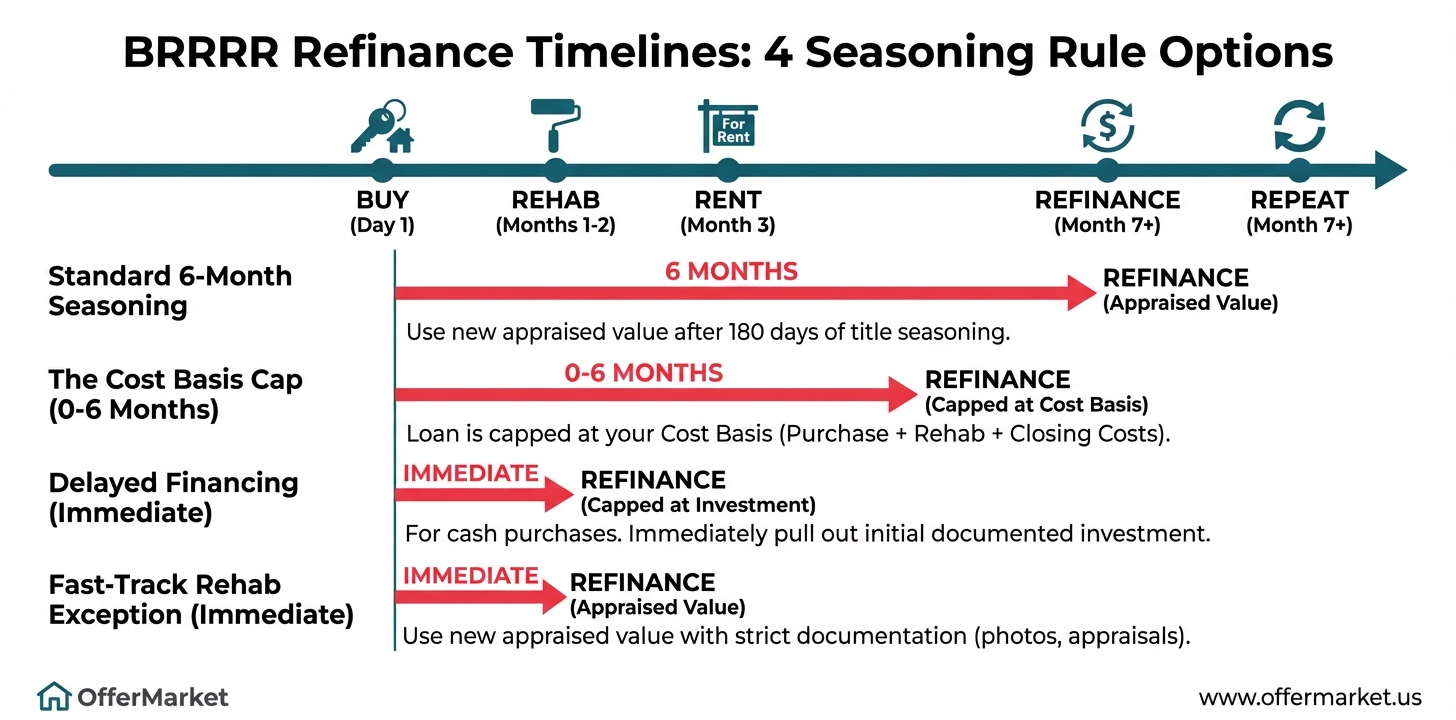

Navigating the standard 6-month seasoning requirement

"Seasoning" refers to the amount of time you have held title to the property. Most lenders have a minimum seasoning requirement of six months before they will allow you to do a cash-out refinance based on the new appraised value.

If you try to refinance before the six-month mark, most lenders will limit your loan amount to be based on your cost basis (purchase price + documented rehab costs), not the new ARV. This prevents you from pulling out the equity you created.

Therefore, you must plan your timeline accordingly. The clock starts on the day you officially take title to the property. A typical BRRRR timeline might look like this:

- Months 1-3: Renovation

- Month 4: Place a tenant

- Months 4-6: Tenant pays rent, property is "seasoning"

- Month 7: Apply for the cash-out refinance

Step 5: REPEAT - Scaling Your Rental Portfolio

The final "R" is what makes this strategy so powerful. By successfully completing a BRRRR, you have not only added a cash-flowing asset to your portfolio but you have also recovered your initial investment capital, allowing you to immediately start looking for the next deal.

Using cash-out proceeds for the next down payment

The cash you received from the refinance is now your seed capital for the next project. You can use it to cover the down payment and initial rehab costs for your next BRRRR property, using another Fix and Flip loan for the primary financing. This creates a "snowball effect," where a single pool of capital is used to acquire an ever-growing portfolio of properties. An investor who starts with $50,000 could theoretically acquire an unlimited number of properties, as the capital is returned and redeployed with each successful cycle.

Leveraging the 3-to-6-month PITIA reserve requirement

When you apply for your DSCR refinance loan, the lender will require you to have cash reserves. These reserves are meant to show that you can cover the mortgage payments during a potential vacancy or unexpected repair. The standard requirement is 3 to 6 months of the full PITIA payment held in a liquid account (like a checking or savings account).

As you acquire more properties, this reserve requirement grows. It's crucial to manage your cash flow to ensure you always have sufficient reserves to qualify for your next loan. The cash-out proceeds from your last deal can often be used to satisfy the reserve requirement for the next one.

Building systems to manage multiple BRRRR projects

Scaling from one project to a portfolio requires moving from an ad-hoc approach to systematized processes. This includes:

- Deal Flow Funnel: Create a consistent system for finding and analyzing deals.

- Team Building: Develop strong relationships with reliable contractors, real estate agents, property managers, and a trusted lending partner like OfferMarket.

- Standardization: Use standardized SOW templates, lease agreements, and financial tracking spreadsheets.

- Project Management: Utilize software or checklists to manage multiple renovation timelines simultaneously.

The goal is to create a repeatable, assembly-line process for acquiring and stabilizing properties.

How each successful cycle builds momentum and borrowing power

With each completed BRRRR project, your position as an investor strengthens. You build a track record of success, which makes you a more attractive borrower to lenders. Your net worth and global cash flow increase, allowing you to qualify for more loans and tackle larger projects. The experience gained from each cycle—from underwriting to managing rehabs—makes you more efficient and profitable on subsequent deals.

Unlock Your Property’s Max Leverage

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →The BRRRR Strategy by the Numbers: A Real-World Example

Let's walk through a hypothetical but realistic example to see how the numbers work at each stage.

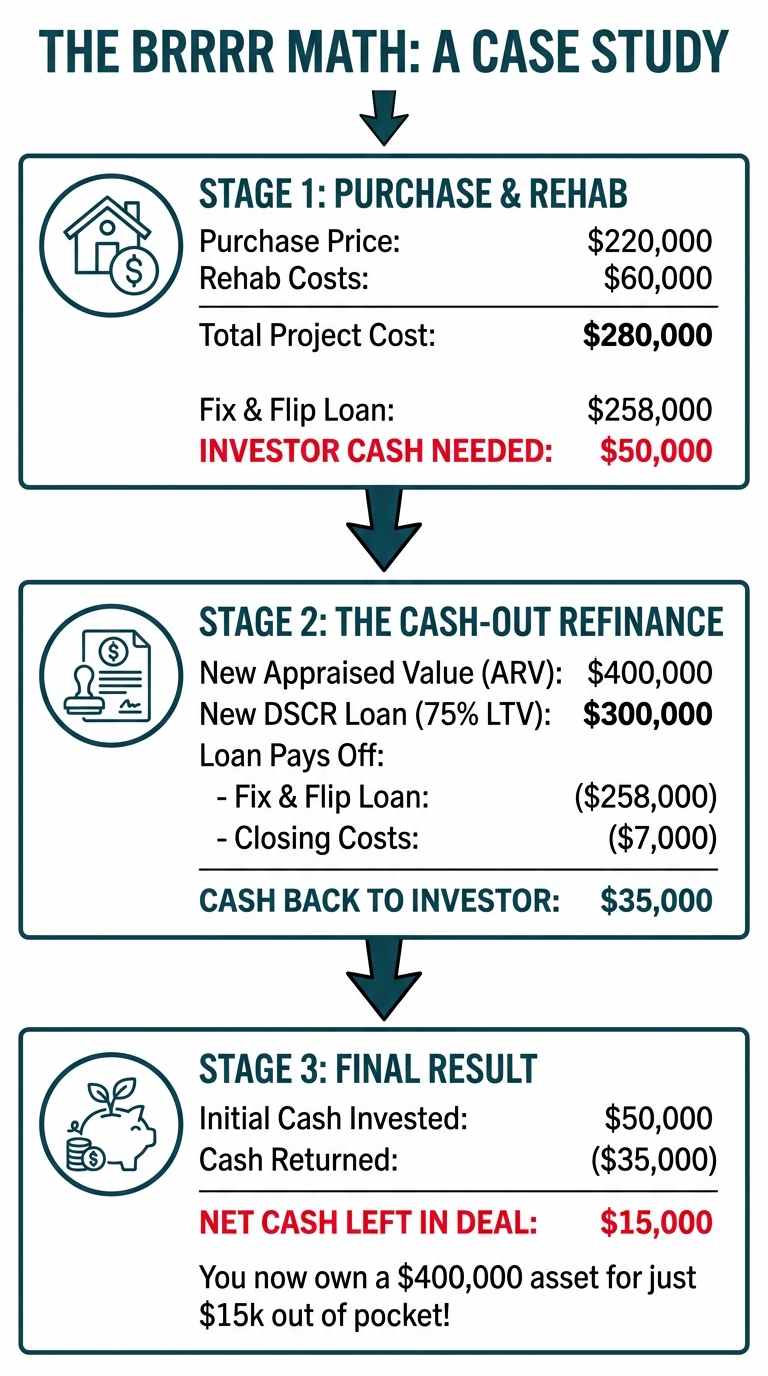

Property: A distressed 3-bedroom, 2-bathroom single-family home. Investor's Initial Capital: $60,000

The Initial Purchase and Rehab Math

- After-Repair Value (ARV): Based on comps, the projected value after renovation is $400,000.

- Purchase Price: You negotiate and buy the property for $220,000.

- Rehab Budget: Your contractor provides a detailed SOW for $60,000.

- Total Project Cost: $220,000 (Purchase) + $60,000 (Rehab) = $280,000.

Financing the Deal with a Fix and Flip Loan

You secure a Fix and Flip loan from OfferMarket with the following terms:

- Loan-to-Cost (LTC): 90% of Purchase Price, 100% of Rehab

- Loan Amount (Purchase): $220,000 * 90% = $198,000

- Loan Amount (Rehab): $60,000 * 100% = $60,000 (held in escrow and released in draws)

- Total Loan Amount: $198,000 + $60,000 = $258,000

- Investor Cash-to-Close:

- Down Payment: $220,000 (Purchase) - $198,000 (Loan) = $22,000

- Closing Costs & Reserves (estimated): $8,000

- Initial Rehab Outlay (to start before first draw): $20,000

- Total Initial Cash Out of Pocket: $22,000 + $8,000 + $20,000 = $50,000

You complete the rehab in 3 months. In month 4, you place a tenant with a 12-month lease for $3,000/month.

The Cash-Out Refinance Calculation

After 6 months of seasoning, you apply for a DSCR loan. The new appraisal confirms the ARV.

- New Appraised Value (ARV): $400,000

- Lender's Max LTV: 75%

- New Maximum Loan Amount: $400,000 * 75% = $300,000

The proceeds of this new loan are used as follows:

- Pay off Fix and Flip Loan: -$258,000

- Pay off Refinance Closing Costs (estimated): -$7,000

- Gross Loan Proceeds: $300,000

- Total Payoffs: $258,000 + $7,000 = $265,000

- Cash-Out to Investor: $300,000 - $265,000 = $35,000

The Final Result: Recovering Capital and Retaining the Asset

Let's review the investor's final position:

- Total Initial Cash Invested: $50,000

- Cash Returned at Refinance: $35,000

- Net Cash Left in the Deal: $50,000 - $35,000 = $15,000

Wait, the goal is to get all your money out. What happened? In this scenario, the investor didn't achieve a "no money down" deal, but it's still a phenomenal outcome. They acquired a $400,000 cash-flowing asset for only $15,000 out of pocket.

To achieve a "zero money down" result, one of three things would need to happen:

- Buy at a Deeper Discount: If the purchase price was $200,000 instead of $220,000.

- Achieve a Higher ARV: If the property appraised for $425,000 instead of $400,000.

- Find a Lender with Higher LTV: A lender offering 80% LTV on the refinance would have yielded a larger loan.

This example illustrates that while the "zero money down" ideal is achievable, the true power of BRRRR is the ability to acquire assets with significantly higher leverage than traditional methods, recycling the vast majority of your capital.

The Fast-Track BRRRR: Bypassing the 6-Month Seasoning Rule

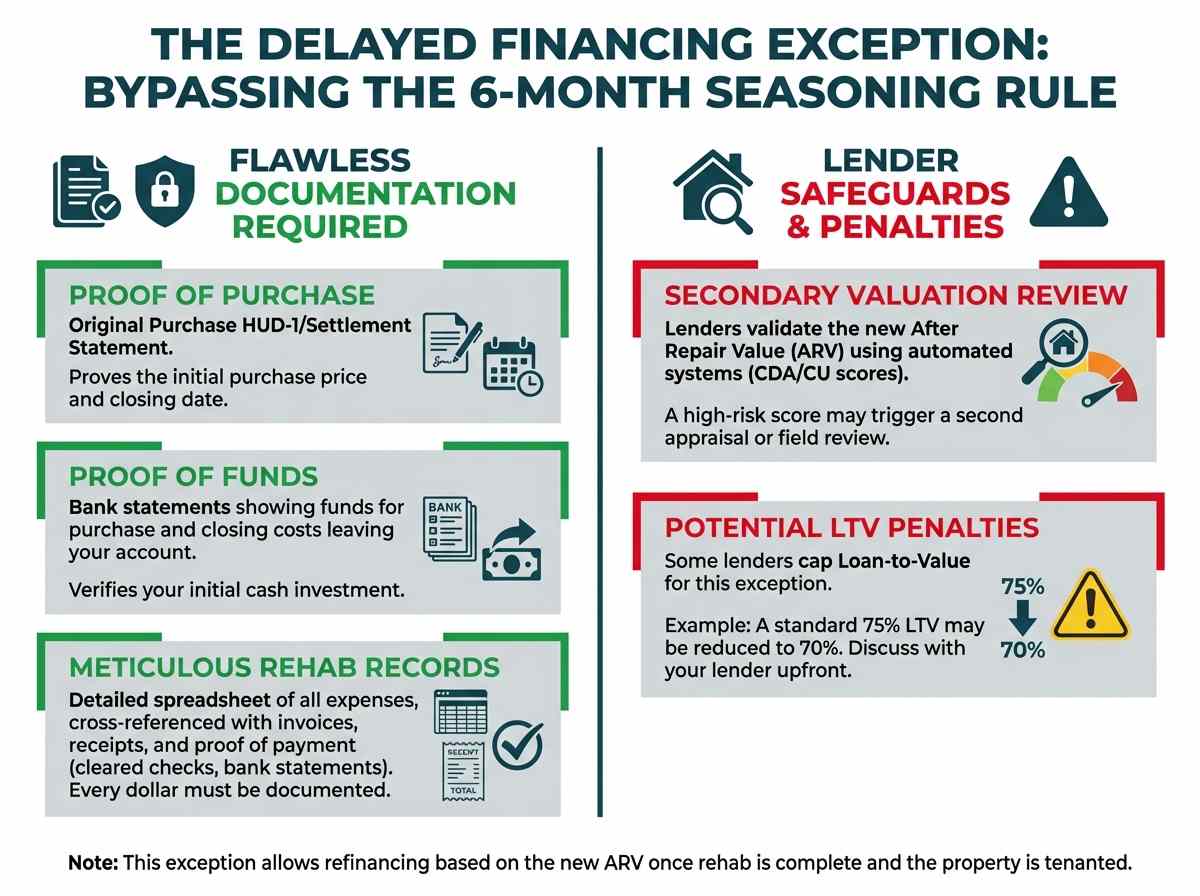

For investors who move quickly, waiting six months to refinance can feel like a drag on momentum. Fortunately, there is a well-established exception to the seasoning rule that allows you to refinance based on the new appraised value in less than six months: the Delayed Financing Exception.

An overview of the delayed financing and rehab exceptions

This exception was originally designed for buyers who purchase a property with cash and want to quickly recoup their investment by getting a mortgage. However, the guidelines from Fannie Mae, which set the standard for many lenders, have been adapted to accommodate investors who also fund renovations.

Under this exception, if you can prove the total funds invested in the project (purchase price + documented renovation costs), a lender can provide a cash-out refinance based on the new ARV, as long as the loan amount doesn't exceed your total documented cost basis. This allows you to execute the "Refinance" step as soon as the rehab is done and a tenant is in place.

The exact documentation required to qualify

To use this exception, you must provide flawless documentation. Lenders are extremely strict about this. You will need:

- Original Purchase HUD-1/Settlement Statement: This proves the original purchase price and closing date.

- Proof of Funds for Purchase: Bank statements showing the funds for the down payment and closing costs leaving your account.

- Meticulous Rehab Records: A detailed spreadsheet of every rehab expense, cross-referenced with:

- Invoices from all contractors.

- Receipts for all materials.

- Cleared checks or bank/credit card statements showing the payments being made for every single invoice and receipt.

Every dollar you want included in your cost basis must be meticulously documented. If you paid a contractor $5,000 in cash and have no invoice or proof of payment, lenders will not include that $5,000 in your cost basis.

The role of the secondary valuation review: CDA and CU scores

Because these loans are based on a rapid and significant increase in value, lenders take extra steps to validate the appraiser's new ARV. They will often run the appraisal through automated underwriting systems that generate a Collateral Underwriter (CU) score or a Collateral Desktop Analysis (CDA). These tools use big data to assess the risk associated with the valuation. If the appraisal comes back with a high-risk score, the lender may require a second appraisal or a field review to confirm the value before approving the loan.

Potential LTV penalties for using the under-6-month exception

While the delayed financing exception is a powerful tool, some lenders may apply a slight LTV penalty for using it. For example, a lender who offers 75% LTV on a seasoned refinance might cap their LTV at 70% for a transaction using the delayed financing exception. This is a risk-mitigation tactic for the lender. It's crucial to discuss this with your loan officer upfront to understand their specific policies and ensure your numbers still work.

Is the BRRRR Strategy Right for You?

The BRRRR method is an advanced investment strategy that, while highly rewarding, is not suitable for everyone. It requires a specific skill set, risk tolerance, and financial position.

The ideal investor profile for the BRRRR method

The BRRRR strategy is best suited for investors who are:

- Value-Add Focused: They are more interested in creating equity through renovations than buying turnkey properties.

- System-Oriented: They enjoy building and refining processes to improve efficiency.

- Growth-Minded: Their primary goal is to scale a rental portfolio as quickly and efficiently as possible.

- Resilient: They can handle the stress and uncertainty that comes with construction projects and complex financing.

Key skills needed: market analysis, project management, and risk tolerance

To succeed with BRRRR, you must be competent in several areas:

- Market Analysis: You need to be able to accurately estimate a property's ARV and prevailing market rents. Getting this wrong can doom the project from the start.

- Deal Underwriting: You must be conservative and disciplined in your calculations, sticking to formulas like the 70% rule.

- Project Management: You need to be able to create a detailed SOW, hire and manage contractors, and keep a renovation project on time and on budget.

- Financial Literacy: You must understand loan products, closing costs, and how to manage cash flow through a multi-stage project.

- Risk Tolerance: BRRRR projects have many moving parts, and things can go wrong. You need the temperament to solve problems without panicking.

Liquidity requirements for down payments and unexpected costs

While the goal is to get your money back out, you need sufficient capital to get in. You'll need cash for:

- Down Payment: Typically 10-25% of the purchase price for a Fix and Flip loan.

- Closing Costs: For both the initial purchase and the final refinance.

- Holding Costs: 3-6 months of interest payments, taxes, and insurance.

- Contingency Reserves: A buffer of 10-15% of your rehab budget is essential to cover unexpected issues that arise during construction.

- PITIA Reserves: The 3-6 months of mortgage payments required by the DSCR lender.

A common mistake is underestimating the total cash required to see a project through to the refinance stage.

Comparing BRRRR to traditional rental acquisition methods

BRRRR vs. Traditional 20% Down:

- Traditional: You save up $60,000 and buy one $300,000 turnkey rental. Your capital is now "stuck" in that property as equity. To buy another, you have to save another $60,000.

- BRRRR: You use $60,000 to execute a BRRRR deal on a $300,000 ARV property. After the refinance, you get most or all of your $60,000 back. You can then immediately use that same capital to buy a second property.

The primary advantage of BRRRR is the velocity of capital. It allows you to do more with less, enabling much faster portfolio growth than traditional methods. The trade-off is significantly more work, complexity, and risk.

Common BRRRR Risks and How to Mitigate Them

Every investment strategy has risks. The key is to understand them upfront and have a plan to mitigate them.

Appraisal Risk: The ARV comes in lower than projected

This is the most common and most dangerous risk in a BRRRR deal. If your refinance appraisal comes in low, your loan amount will be reduced, and you may not be able to pull out all your capital, or worse, you may not be able to borrow enough to pay off the hard money loan.

- Mitigation:

- Conservative Underwriting: Don't push your ARV estimates. Use comps that are truly comparable and make conservative adjustments.

- Know Your Appraisers: Work with lenders who use local, experienced real estate appraisers who understand value-add projects.

- Provide a "Brag Sheet": Give the appraiser a packet with a list of all upgrades, before/after photos, and your list of comparable sales. This helps them understand the scope of the transformation.

- Have a Contingency Plan: Know your numbers. If the appraisal comes in $20,000 low, how much extra cash will you need to bring to closing to complete the refinance? Be prepared for this possibility.

Rehab Risk: Exceeding the renovation budget or timeline

Construction is notoriously unpredictable. Unforeseen issues like mold, foundation problems, or electrical issues can blow your budget. Delays with contractors or permits can extend your timeline, racking up holding costs.

- Mitigation:

- Thorough Inspection: Get a detailed inspection before you buy to uncover as many potential issues as possible.

- Detailed SOW: A line-item SOW prevents scope creep and misunderstandings with your contractor.

- Contingency Fund: Always budget a 10-15% contingency reserve for unexpected repair costs.

- Vet Your Contractor: Hire experienced, licensed, and insured contractors with a proven track record. Check their references thoroughly.

Market Risk: Rents or property values decline unexpectedly

The BRRRR process can take 6-9 months. During that time, the real estate market could shift. A recession could cause property values to fall, or a new apartment complex could be built nearby, causing market rents to soften.

- Mitigation:

- Buy with a Margin of Safety: The 70% rule is designed to provide a buffer against market fluctuations. A deal that is thin on paper will be wiped out by a small market dip.

- Invest in Strong Markets: Focus on areas with strong economic fundamentals like job growth and population growth. These markets are more resilient to downturns. The NAR provides regular updates on housing trends.

- Focus on Cash Flow: Underwrite your deal based on sustainable, long-term cash flow. Even if appreciation stalls, a property with strong cash flow remains a good investment.

Financing Risk: Failing to qualify for the DSCR refinance loan

You could successfully complete the first three steps, only to find you can't get the permanent loan. This could be due to a low appraisal, rents not meeting DSCR requirements, or changes in lending guidelines.

- Mitigation:

- Pre-Qualify for Both Loans: Before you start, talk to a lender who offers both Fix and Flip and DSCR loans. Understand the guidelines for the DSCR loan before you buy the property.

- Maintain Your Credit: Don't do anything to harm your credit score during the project (e.g., miss payments, open lots of new credit). While DSCR loans aren't primarily credit-based, a major drop in your score can still be a problem.

- Work with an Experienced Partner: Choose a lender like OfferMarket that specializes in these types of loans and can guide you through the entire process, from the initial purchase to the final refinance.

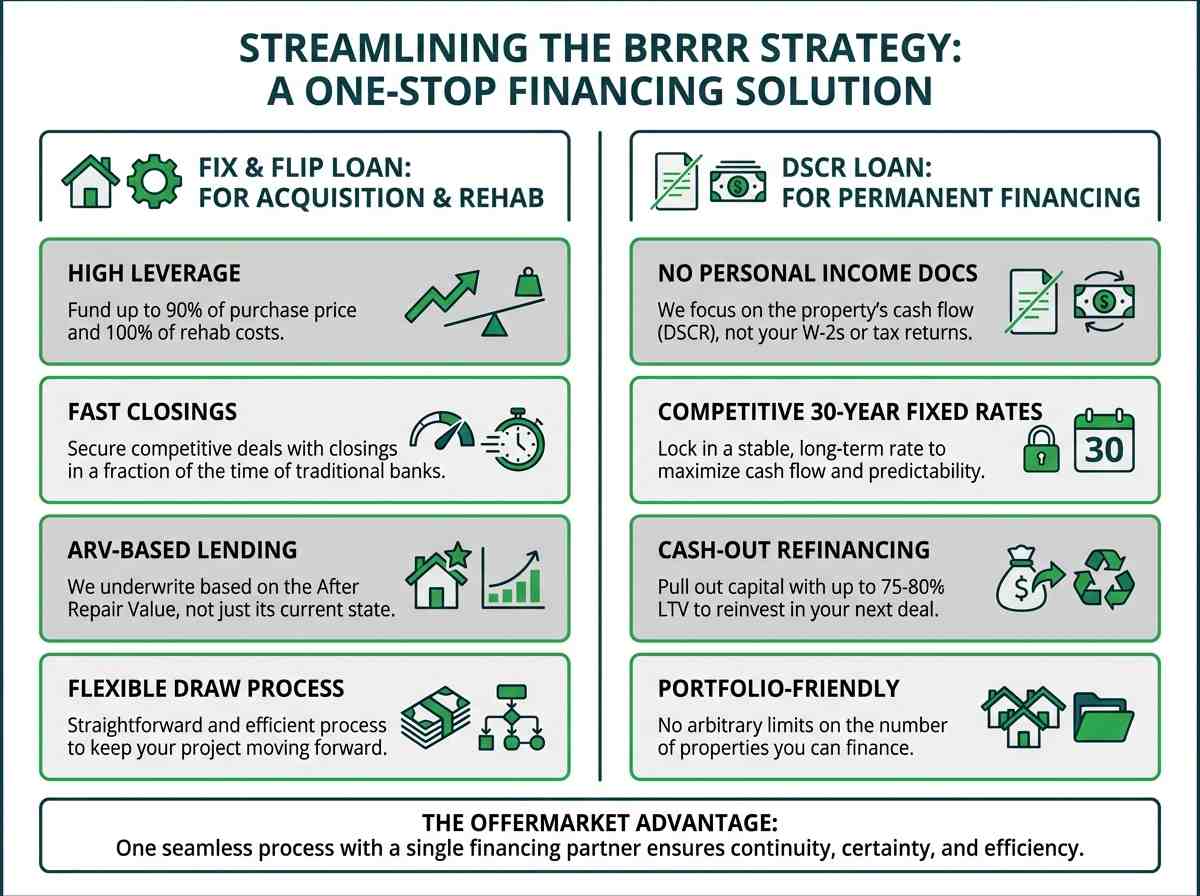

How OfferMarket Streamlines the Entire BRRRR Process

Executing a BRRRR strategy requires two distinct types of loans, and managing relationships with two different lenders can be inefficient and risky. A lender for the acquisition might not understand the needs of a long-term rental investor, and a permanent lender might not understand the fast-paced nature of fix-and-flip deals. OfferMarket bridges this gap by providing a seamless, one-stop financing solution for the entire BRRRR lifecycle.

Our Fix and Flip loan program for the Buy and Rehab phases

Our Fix and Flip loan program is engineered for the speed and flexibility that BRRRR investors need.

- High Leverage: We fund up to 90% of the purchase price and 100% of the rehab costs.

- Fast Closings: We can close in a fraction of the time of traditional banks, helping you secure competitive deals.

- ARV-Based Lending: We underwrite based on the future potential of your project, not just its current state.

- Flexible Draw Process: Our draw process is designed to be straightforward and efficient, helping you keep your project moving.

Our permanent DSCR loan program for the Refinance phase

Once your property is stabilized, our DSCR loan program provides the ideal permanent financing solution.

- No Personal Income Docs: We focus on the property's cash flow (DSCR), not your personal W-2s or tax returns.

- Competitive 30-Year Fixed Rates: Lock in a stable, long-term rate to maximize your cash flow and predictability.

- Cash-Out Refinancing up to 75-80% LTV: We help you pull out the maximum amount of capital to reinvest in your next deal.

- Portfolio-Friendly: Our loans are designed for investors looking to own multiple properties, with no arbitrary limits on the number of properties you can finance.

The benefit of a single financing partner for both transactions

Working with OfferMarket for both loans creates a powerful advantage. We understand your full strategy from day one.

- Continuity: The team that underwrote your Fix and Flip loan already understands the project, leading to a smoother, faster refinance process.

- Certainty of Execution: We can pre-underwrite you for the DSCR loan while you're still in the rehab phase, giving you confidence that your exit financing is secure.

- Efficiency: You only need to build one relationship and go through one onboarding process. We handle the transition from the short-term to the long-term loan seamlessly.

Expert guidance from loan specialists experienced in the BRRRR strategy

Our loan specialists aren't just order-takers; they are experienced advisors who have funded countless BRRRR projects. They understand the nuances of the strategy, from underwriting the initial deal to navigating the seasoning requirements and maximizing your cash-out. They can provide valuable insights and help you avoid common pitfalls throughout the process.

Take the Next Step on Your BRRRR Journey

The BRRRR strategy is a proven method for building wealth and scaling a real estate portfolio with velocity. Success requires careful planning, disciplined execution, and the right financing partner. If you're ready to put this powerful strategy to work, we're here to provide the capital and expertise you need.

- Planning your purchase and rehab? Get an instant quote for a Fix and Flip loan to see your terms in minutes.

- Ready to refinance a stabilized property? Get an instant quote for a DSCR loan to lock in your long-term financing.

- Have questions or a complex deal? Contact an OfferMarket loan specialist for a personalized consultation.

- Want to learn more? Explore our full suite of blogs designed to help you achieve your real estate goals.

Get Your Instant Loan Quote

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →

OfferMarket Loans

Check your rate

60 seconds · no credit pull