DSCR Loan Indianapolis

OfferMarket Loans

Check your rate

60 seconds · no credit pull

DSCR Loan Example Deal

DSCR Loan calculation

DSCR Loan Requirements

DSCR Loan Common Questions

Last updated: February 22, 2025

Investing in rental properties can be both exciting and challenging, no matter where you are in your journey. Whether you're just starting to build your portfolio or you're a seasoned investor looking to scale, finding the right financing options is crucial to your success. That's where DSCR loans in Indianapolis come into play.

A DSCR (Debt Service Coverage Ratio) loan is designed to help you secure funding based on your property's income potential rather than your personal financials. It's a game-changer for investors aiming to grow their portfolios while managing risk effectively. In this article, you'll find actionable insights to navigate DSCR loans and leverage them to optimize your investments in the thriving Indianapolis market.

What Is A DSCR Loan?

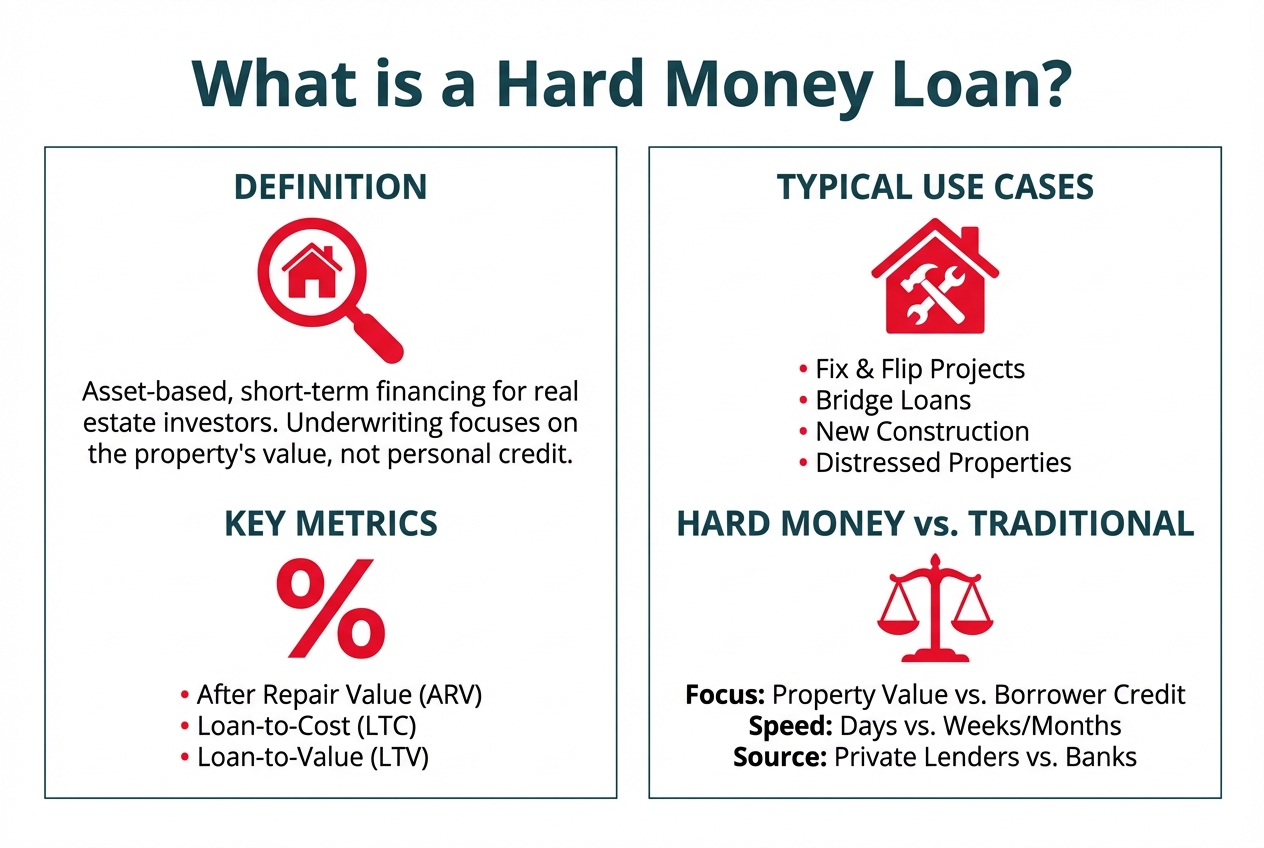

A DSCR loan is a type of financing based on your property's income generation rather than your personal income or credit profile. It's designed to assist real estate investors in securing funding for rental properties.

Understanding Debt Service Coverage Ratio (DSCR)

DSCR measures your property's ability to cover its debt obligations using its income. Lenders calculate DSCR by dividing the property’s net operating income (NOI) by its total debt service. For example, if a property generates $10,000 in NOI annually and has $8,000 in yearly debt payments, its DSCR is 1.25. A DSCR above 1.0 typically indicates that the property generates sufficient income to cover loan payments, making it more favorable to lenders.

How DSCR Loans Work

DSCR loans assess the viability of your rental property by focusing on its income potential rather than your personal financials. Lenders evaluate the property's DSCR to determine how much funding you qualify for. These loans are commonly used for fix and rent loan strategies, helping you grow your real estate portfolio. Adequate coverage, such as landlord insurance, can enhance your eligibility, as it demonstrates risk mitigation to lenders. The emphasis remains on your property’s cash flow performance.

Top Neighborhoods for Rental Properties in Indianapolis

When considering rental property investments in Indianapolis, three notable areas stand out: Carmel, Greenwood, and Anderson. Each of these neighborhoods offers unique advantages for investors looking to capitalize on the growing rental market.

Carmel

Carmel is known for its affluent community and high-quality schools, making it a desirable location for families. The city boasts a vibrant arts scene, numerous parks, and a strong local economy. With a median home price significantly higher than the national average, rental properties here tend to attract higher rents, ensuring a solid return on investment. The ongoing development projects and a focus on maintaining a high standard of living contribute to the area's appeal.

Greenwood

Greenwood offers a more affordable alternative while still providing access to the amenities of Indianapolis. The city has seen substantial growth in recent years, with new businesses and residential developments emerging. Its proximity to major highways makes it an attractive option for commuters. The rental market in Greenwood is robust, with a mix of single-family homes and multi-family units, catering to a diverse tenant base.

Anderson

Anderson, located northeast of Indianapolis, presents a unique opportunity for investors. While it may not have the same level of demand as Carmel or Greenwood, it offers lower property prices and higher potential yields. The city is undergoing revitalization efforts, which could lead to increased property values and rental rates in the future. Investors looking for affordable entry points into the market may find Anderson appealing.

Economic Drivers for Home Price and Rent Appreciation

The economic landscape of Indianapolis is a significant factor in the appreciation of home prices and rents. Key drivers include:

- Job Growth: Indianapolis has a diverse economy with strong sectors in healthcare, education, and technology. The presence of major employers contributes to job stability and attracts new residents, driving demand for rental properties.

- Population Growth: The Indianapolis metro area has experienced steady population growth, leading to increased housing demand. As more people move to the area for job opportunities, the rental market continues to thrive.

- Infrastructure Development: Ongoing investments in infrastructure, including transportation and public services, enhance the livability of the area. Improved access to amenities and services makes neighborhoods more attractive to potential renters.

Major Counties in the Indianapolis Metro Area

The Indianapolis metro area encompasses several key counties, each contributing to the region's overall growth and rental market dynamics:

- Marion County: Home to the city of Indianapolis, Marion County is the economic and cultural hub of the region. It offers a wide range of rental options, from urban apartments to suburban homes.

- Hamilton County: This affluent county includes cities like Carmel and Fishers, known for their high-quality schools and family-friendly environments. The demand for rental properties is strong here, driven by the area's reputation.

- Hancock County: Located to the east of Marion County, Hancock County is experiencing growth as more residents seek affordable housing options while still being close to Indianapolis.

- Johnson County: This county includes Greenwood and offers a mix of suburban and rural living. The rental market is diverse, catering to various demographics.

- Shelby County: While more rural, Shelby County provides opportunities for investors looking for lower property prices and potential for appreciation as the metro area expands.

In conclusion, Indianapolis and its surrounding neighborhoods present a wealth of opportunities for rental property investors. By focusing on areas like Carmel, Greenwood, and Anderson, and understanding the economic drivers and county dynamics, investors can make informed decisions to maximize their returns.

Benefits Of DSCR Loans In Indianapolis

DSCR loans offer significant advantages for real estate investors in Indianapolis. Designed to prioritize property income over personal financials, these loans simplify the process of securing investment capital.

Flexible Financing Options

DSCR loans provide flexibility by focusing on your property's rental income rather than your personal financial history. Lenders evaluate the property's DSCR to determine its ability to cover debt obligations. This approach works well for diverse investment strategies like the fix and rent loan, which allows you to renovate and lease properties. Additionally, incorporating landlord insurance can strengthen your application by showcasing risk management. Coverage options like dwelling coverage and loss of rent coverage further secure your investment assets.

Suitable For Real Estate Investments

Designed specifically for real estate investors, DSCR loans are ideal for acquiring, renovating, or renting out properties in Indianapolis. Unlike traditional loans, this lending option supports investors aiming to expand rental portfolios or execute fix and rent strategies. The DSCR calculation directly relates to the property's income potential, ensuring investment viability. Including general liability coverage in your insurance plan demonstrates proactive risk mitigation, which could improve lender confidence.

No Personal Income Documentation Required

DSCR loans eliminate the need for personal income verification, streamlining the application process. Lenders focus exclusively on the property's cash flow and your credit score and bank statement liquidity. This is especially useful for self-employed rental investors or those with non-traditional income sources. With proper risk coverage, such as landlord insurance, you enhance your eligibility, as policies like loss of rent coverage indicate preparedness for potential revenue interruptions.

Who Qualifies For A DSCR Loan In Indianapolis?

Understanding qualification criteria for a DSCR loan is crucial for real estate investors. These loans focus on property income, streamlining eligibility for borrowers looking to expand their rental portfolios.

DSCR Requirements For Borrowers

Lenders assess your property’s net operating income (NOI) in relation to its debt obligations. A DSCR of 1.0 or higher typically qualifies for approval, as it shows the property generates enough income to cover loan payments. Personal income documentation isn't required, making this loan suitable for self-employed investors or those with non-traditional earnings.

A stable rental income stream is essential. Demonstrating effective risk management using landlord insurance or related policies, such as dwelling coverage or general liability coverage, strengthens your application. Lenders may also review your credit score for additional assurance, though the primary focus remains on property performance.

Property Types Eligible For DSCR Loans

DSCR loans apply to residential properties and some commercial units generating rental income. Eligible property types include single-family homes, multi-family units, condominiums, and townhomes. Fix and rent investments, where properties are renovated before leasing, are also viable options as long as the property does not have too much deferred maintenance and has an appraisal condition rating of C4 condition or better.

Vacant properties are typically allowed. Lenders expect your property to meet certain occupancy and rental potential standards, ensuring its ability to generate sufficient cash flow. Aligning property-specific policies, like dwelling coverage and loss of rent coverage, can help mitigate associated risks and enhance eligibility.

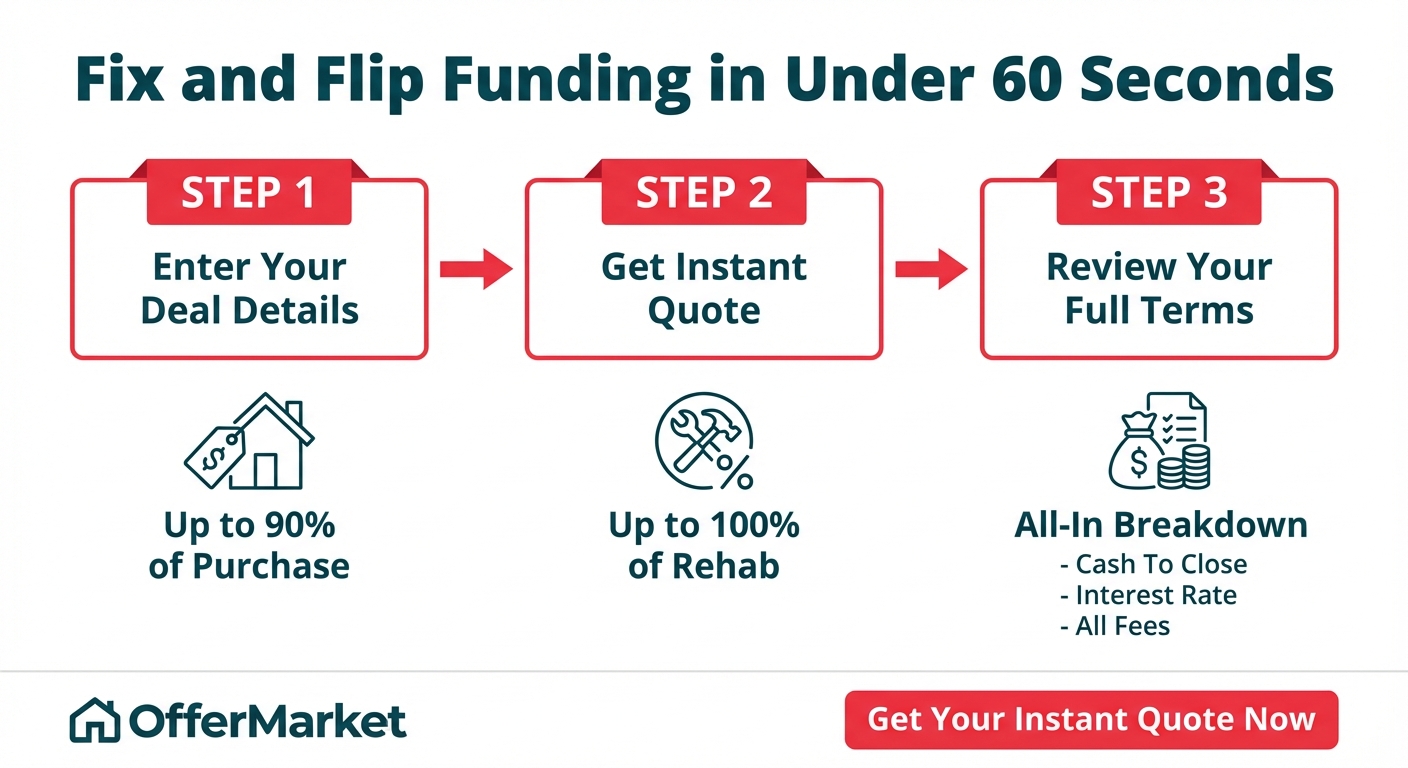

How To Apply For A DSCR Loan In Indianapolis

Applying for a DSCR loan in Indianapolis involves understanding the key steps and preparing the necessary documents to ensure a smooth process.

Key Steps In The Application Process

Start by identifying a reliable lender specializing in DSCR loans. Research and compare their terms, rates, and requirements. Next, evaluate your rental property’s income potential. Calculate the DSCR by dividing the property’s net operating income by its total debt obligations. A DSCR of 1.0 or higher often meets approval criteria.

Submit a loan application providing property details and a clear income strategy, such as a fix and rent plan, to demonstrate viability. Enhance your application with landlord insurance, including loss of rent coverage, for added financial security. Complete the lender’s underwriting process to validate the property’s cash flow and risk profile.

Documents Needed For Approval

Prepare rental property income records, such as lease agreements or income projections, to support your application. Provide the property’s net operating income (NOI) calculations to confirm debt coverage capacity.

Ensure landlord insurance documents, including proof of dwelling coverage and general liability coverage, are included to address liability concerns. Submit property appraisals and inspection reports, as these validate the property’s market value and occupancy potential. Prepare a detailed business plan, especially for fix and rent loans, to outline your investment strategy.

Choosing The Right Lender In Indianapolis

Selecting the right lender is critical for securing a DSCR loan that fits your investment strategy. Different lenders offer varying terms, rates, and requirements, so choosing the optimal one ensures a smoother financing process.

Factors To Consider When Selecting A Lender

Evaluate the lender’s experience in DSCR loans by reviewing their track record with investors in Indianapolis. Lenders familiar with the local market understand property values and rental demand, which strengthens their loan assessments. Check the lender's loan terms, including DSCR requirements, interest rates, and prepayment penalties, to ensure they align with your financial goals. Assess their ability to offer additional benefits, such as flexible terms for fix and rent loans or support for securing landlord insurance. Strong customer service, quick approval timelines, and clear communication are crucial to avoid delays during the loan application process.

Top DSCR Loan Providers In Indianapolis

Several reputable lenders in Indianapolis specialize in DSCR loans. National mortgage companies and local credit unions often offer competitive rates and terms for investment properties like single-family homes or multi-family units. Research lenders with previous experience in facilitating fix and rent loans, as they often tailor packages for property renovations. Some lenders collaborate with insurers to help integrate landlord insurance costs, covering dwelling coverage or loss of rent coverage, into loan structures. Contact multiple lenders, compare their offerings, and look for recommendations from other real estate investors for a well-informed decision.

Key Takeaways

- DSCR Loans Prioritize Property Income: Unlike traditional loans, DSCR loans in Indianapolis focus on a property's income potential rather than personal financials, making them ideal for real estate investors.

- Flexible Financing for Investors: DSCR loans offer flexibility, supporting strategies like fix-and-rent and enabling self-employed individuals or those with non-traditional incomes to qualify without personal income verification.

- Key Qualification Criteria: A DSCR of 1.0 or higher, stable rental income, and effective risk management (e.g., landlord insurance) are crucial for loan approval. Eligible properties include single-family homes, multi-family units, and vacant properties with future rental potential.

- Streamlined Application Process: To apply, calculate your property’s DSCR, prepare income records, and include proof of insurance. Partnering with a reliable DSCR lender ensures a smoother approval process.

- Choosing the Right Lender Matters: Evaluate lenders based on their experience, loan terms, and local market knowledge to find the best fit for your investment strategy in Indianapolis.

- Insurance Enhances Loan Eligibility: Policies like landlord insurance, dwelling coverage, and loss of rent coverage can improve your application by demonstrating proactive risk mitigation.

Conclusion

DSCR loans offer a powerful financing solution for real estate investors in Indianapolis, focusing on property income rather than personal financial history. By streamlining the application process and accommodating diverse investment strategies, these loans provide the flexibility you need to grow your portfolio.

Partnering with the right lender is key to securing favorable terms and maximizing your investment potential. With careful planning and a strong understanding of DSCR loans, you can confidently navigate the Indianapolis market and achieve long-term financial success.

Frequently Asked Questions

What is a DSCR loan?

A DSCR (Debt Service Coverage Ratio) loan is a type of financing where lenders assess a rental property's income potential to determine loan eligibility, rather than relying on the borrower’s personal income or credit history.

How do lenders calculate DSCR?

Lenders calculate DSCR by dividing a property's net operating income (NOI) by its total debt service (loan payments). A DSCR greater than 1.0 indicates that the property generates sufficient income to cover loan obligations.

Why are DSCR loans ideal for rental property investors in Indianapolis?

DSCR loans are flexible for investors as they focus on rental property income rather than personal finances. This is particularly helpful for self-employed individuals and those using diverse investment strategies like fix-and-rent.

What are the key benefits of DSCR loans?

DSCR loans streamline the application process by eliminating personal income documentation and prioritizing rental income potential. They are ideal for acquiring, renovating, or renting properties without traditional financial restrictions.

What property types qualify for DSCR loans?

Eligible property types for DSCR loans include single-family homes, multi-family units, condominiums, and some commercial properties, provided they generate sufficient rental income to meet loan requirements.

What is the minimum DSCR required to qualify for a loan?

Most lenders require a minimum DSCR of 1.0 or higher, as it indicates the property generates enough income to cover the loan’s monthly payments and expenses.

Do I need personal income documentation for a DSCR loan?

No, DSCR loans do not require personal income documentation. They are based entirely on a property’s ability to generate rental income sufficient to cover debt obligations along with your credit score and liquidity.

How can landlord insurance enhance my DSCR loan application?

Landlord insurance showcases risk management by protecting the property and potential rental income, enhancing your reliability as an investor and strengthening your loan application.

What is the application process for a DSCR loan in Indianapolis?

The process involves selecting a reliable lender, assessing the rental property’s income potential, calculating DSCR, and submitting documents such as income records, NOI calculations, landlord insurance, and property appraisals.

How do I choose the right lender for a DSCR loan in Indianapolis?

Look for lenders experienced with DSCR loans, familiar with Indianapolis' market, and offering loan terms that align with your goals. Evaluate their customer service, approval timelines, and compare rates.

Can a DSCR loan be used for property renovations?

Yes, DSCR loans are an excellent option for the fix-and-rent model, allowing investors to renovate properties and lease them to generate rental income for loan coverage.

Are DSCR loans suitable for self-employed real estate investors?

Absolutely. DSCR loans do not rely on personal income, making them ideal for self-employed investors or those with non-traditional income sources.

What documents are required when applying for a DSCR loan?

The following documents are crucial for your DSCR loan application:

- Personal Identification: Provide a valid government-issued ID, such as a driver's license or passport.

- Property Information: Gather details about the property, including purchase agreement or rental income statements.

- Bank Statements: Submit recent bank statements, typically covering the most recent 2 months, to demonstrate financial health.

- Rental Income Verification: Include lease agreements or rent rolls to validate expected rental income from the property.

How do DSCR loans support long-term investment strategies?

By focusing on rental income potential, DSCR loans allow investors to expand their portfolios and manage financial risk without being reliant on their personal income for financing approvals.

What loan structure options are available for DSCR loans?

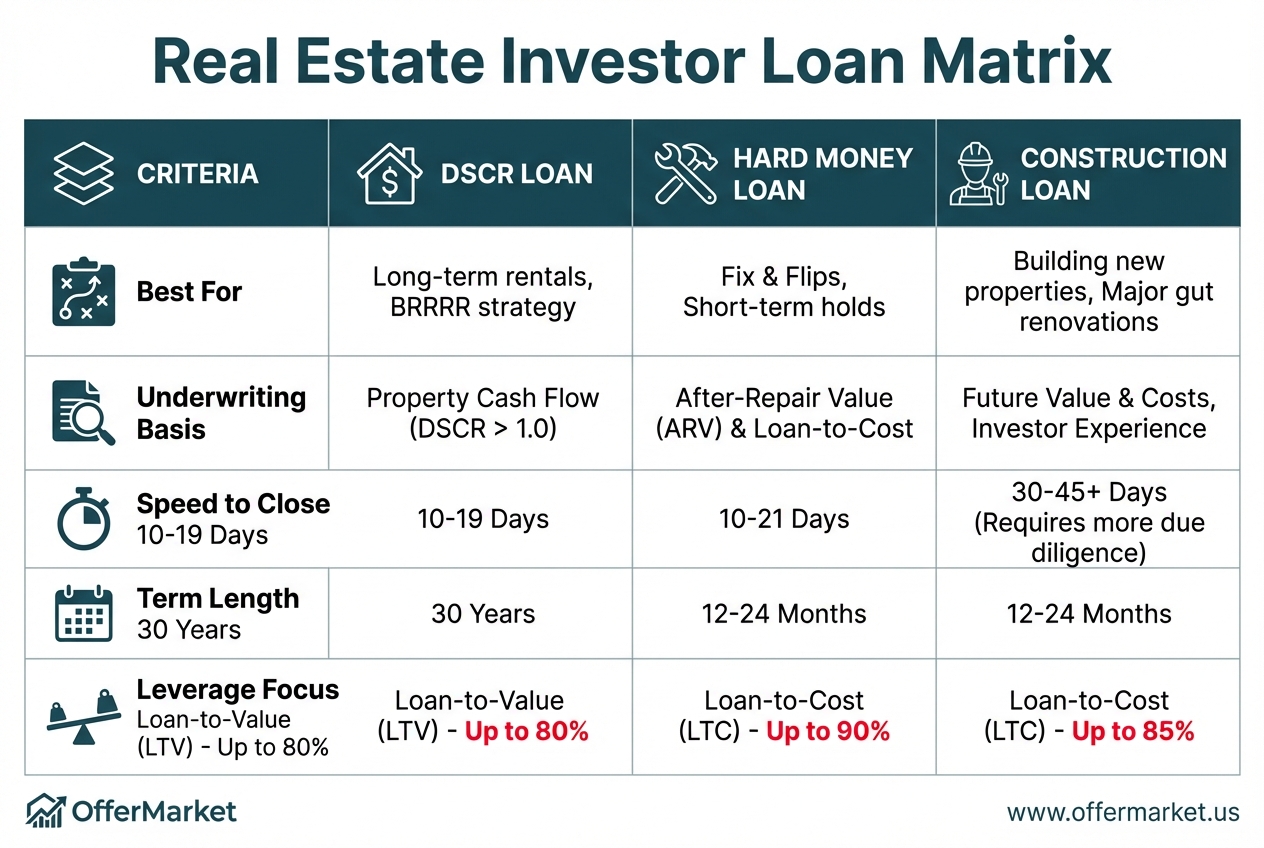

While the most commonly selected and competitive terms will be for 30 year year term, fully amortizing, fixed rate structure, there are also partial interest-only and adjustable rate options available for your consideration. It's important to work with an expert DSCR lender to match you with the best structure to properly manage risk and accomplish your goals.

| Loan Product | Term | Amortization Type | Notes |

|---|---|---|---|

| 30-Year Fixed | 30 Years | Fully Amortizing | Stable monthly payments |

| Partial Interest Only | 5 or 10 Years | Interest Only (initial period) | Improved cash flow initially |

| Adjustable Rate Mortgage (ARM) | Varies | Variable | Higher risk due to rate fluctuations |

How to Apply for a DSCR Loan in Indianapolis

Applying for a DSCR loan in Akron involves gathering necessary documents and completing the application process efficiently. Understanding these steps ensures a smoother experience.

Grow your Indy portfolio with OfferMarket

If you've found this helpful and would like access to more rental property investing resources, sign up for OfferMarket. Membership is free and comes with the following benefits:

🏠 Off market properties 💰 Private lending ☂️ Landlord insurance rate shopping 💡 Community & insights

If you are not already a member, we hope you will accept our invitation to join us!

OfferMarket Loans

Check your rate

60 seconds · no credit pull