*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Utah Landlord Insurance

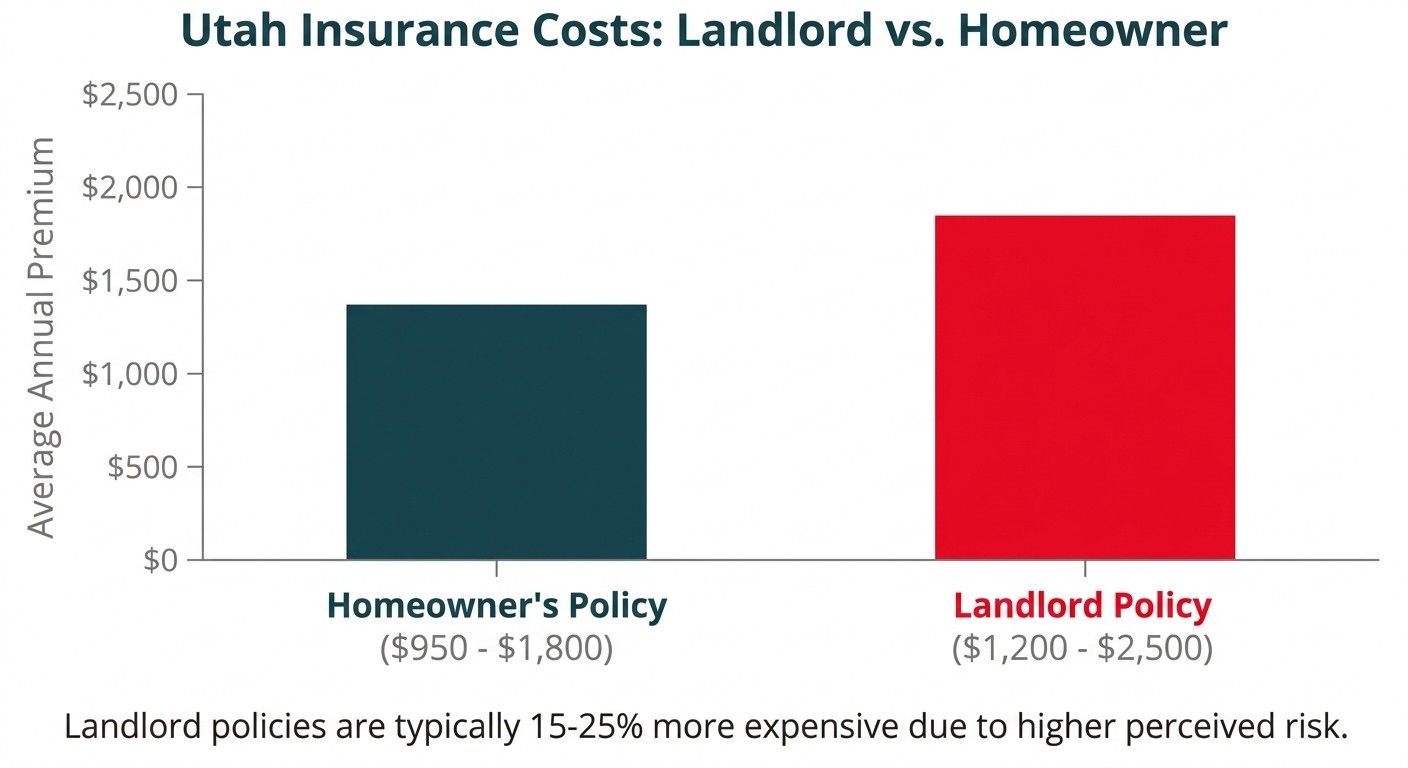

In Utah, the average cost of landlord insurance typically ranges from $1,200 to $2,500 per year, which is generally 15-25% more than a standard homeowners policy. This essential coverage, often called a Dwelling Fire policy (DP-3), is designed specifically for rental properties. It protects your financial investment by covering the physical structure of the building (dwelling protection), provides liability coverage in case a tenant or visitor is injured on the property, and reimburses you for lost rental income if the property becomes uninhabitable due to a covered event like a fire or major storm.

This coverage is not just a recommendation; it's a fundamental requirement for any serious real estate investor. A standard homeowner's policy (HO-3) will not cover claims on a property that you do not occupy as your primary residence. Relying on the wrong policy can lead to claim denial, leaving you responsible for catastrophic repair costs and legal fees. Understanding the specific components of a Utah landlord policy ensures your asset is properly protected against the state's unique risks, from winter storms to seismic activity.

Understanding Your Core Coverage

A landlord insurance policy, known as a DP-3 policy in the industry, is a package of different coverages. While policies can be customized, nearly all standard Utah landlord policies are built on four essential pillars of protection.

Dwelling Protection

This is the bedrock of your policy. Dwelling protection covers the physical structure of your rental property, including the foundation, walls, roof, and windows. It also covers systems that are permanently installed, such as the electrical, plumbing, and HVAC systems. If a fire damages the kitchen, for example, this coverage pays to repair the cabinets, drywall, wiring, and any other part of the structure that was affected. The amount of dwelling coverage should be based on the property's Replacement Cost Value (RCV), not its market value.

Liability Insurance

Liability coverage protects you from financial loss if you are found legally responsible for bodily injury or property damage to a third party. The most common scenario is a tenant or their guest slipping on an icy walkway and suing you for medical expenses. This coverage can pay for their medical bills, your legal defense costs, and any settlement or judgment, up to your policy's limit. Standard liability limits often start at $100,000, but many investors opt for $500,000 or $1,000,000 for greater protection, especially if they own multiple properties.

Loss of Rental Income

Also known as "Fair Rental Value" coverage, this is a critical component for any investor. If your rental property becomes uninhabitable due to a covered peril (like a major water pipe burst or a fire), you will lose the rental income you rely on. Loss of Rental Income coverage reimburses you for this lost rent while the property is being repaired. This helps you continue to meet your mortgage obligations and other expenses even when the property is vacant, preventing a covered disaster from turning into a financial crisis.

Other Structures

This coverage protects structures on the rental property that are not attached to the main dwelling. Common examples include a detached garage, a shed, a fence, or a gazebo. Coverage for other structures is typically calculated as a percentage of your total dwelling coverage, often around 10%. If a windstorm knocks down a fence or a tree falls on the detached garage, this is the part of your policy that would cover the repair costs.

Get an Instant Insurance Quote

Protect your investment property with competitive rates — quote in minutes.

Get Insurance Quote →Average Cost of Landlord Insurance in Utah for 2026

The average annual premium for a landlord insurance policy in Utah falls between $1,200 and $2,500 for a typical single-family rental property. This represents an average cost of roughly $100 to $210 per month. This is generally about 15-25% higher than a standard homeowner's insurance policy because rental properties are considered to have a higher risk profile. Tenants may not be as diligent about property maintenance as an owner-occupant, and the increased foot traffic of guests and visitors raises the potential for liability claims.

The cost can vary significantly based on location within the state.

Salt Lake City: Premiums in metro areas like Salt Lake City may be higher due to higher property values and potentially higher crime rates. However, better access to fire departments can sometimes offset these costs.

St. George: Properties in Southern Utah face different risks, such as flash flooding (which requires a separate policy) and higher summer temperatures that can strain HVAC systems.

Rural Areas: Landlords in more rural parts of Utah might see different rates based on their proximity to fire hydrants and emergency services, as well as their exposure to wildfire risk.

Ultimately, the premium is directly tied to the property's value and the amount of coverage needed. A $700,000 rental in Park City will have a much higher premium than a $350,000 rental in Ogden because the cost to rebuild it (the replacement cost) is significantly higher.

Factors That Directly Influence Your Premium

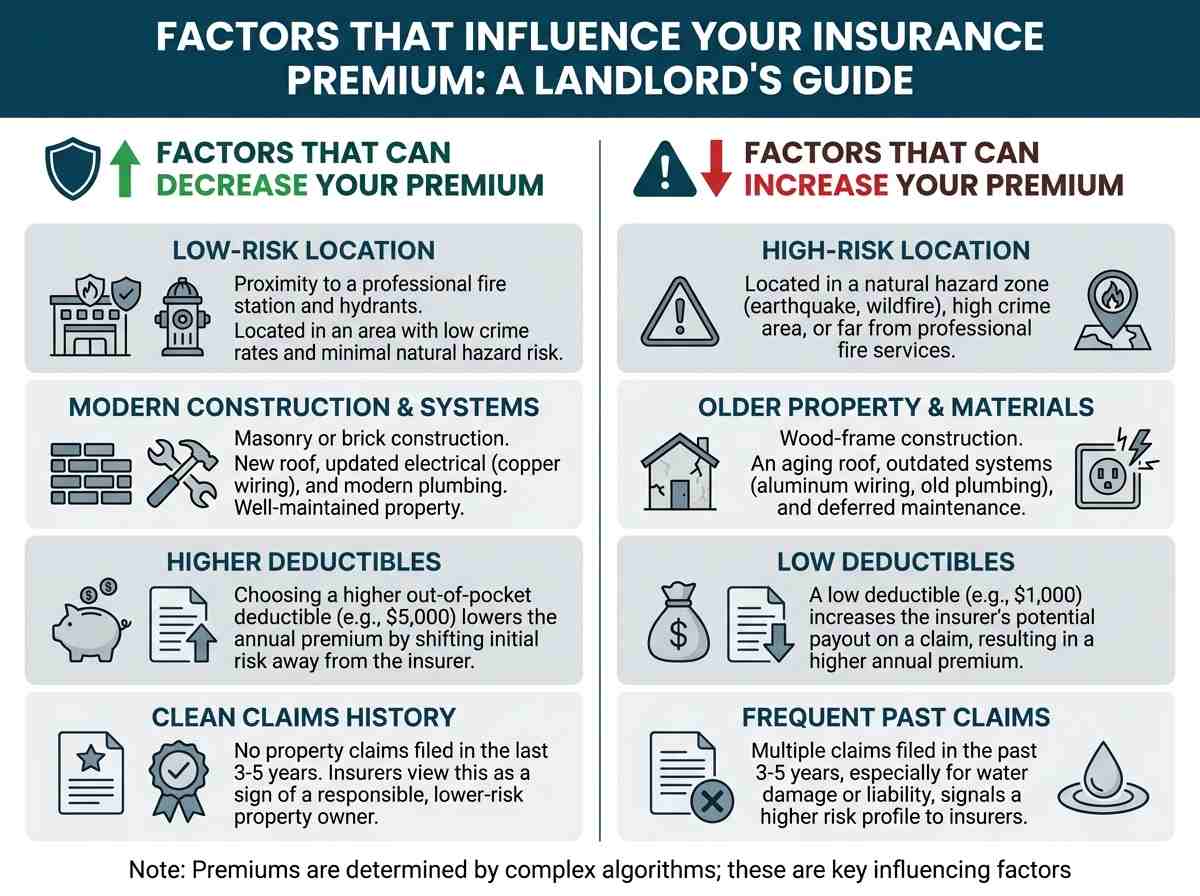

Insurance carriers use sophisticated algorithms to determine your premium, weighing dozens of data points to assess the risk of a potential claim. While you can't control every factor, understanding them helps you anticipate costs and identify areas where you can make improvements.

Property Location

Where your property is located is one of the most significant rating factors. Insurers analyze:

Proximity to Fire Services: The distance to the nearest fire station and fire hydrant directly impacts risk. Properties in areas with a fully-staffed, professional fire department (a lower Protection Class rating) will have lower premiums than those in rural areas served by volunteers.

Crime Rates: Insurers use local crime statistics to assess the risk of theft, vandalism, and malicious mischief. Higher crime rates can lead to higher premiums.

Natural Hazard Zones: Utah has specific geographic risks. Properties located near the Wasatch Fault zone have a higher earthquake risk. Those in canyons or near forested areas have an elevated wildfire risk. These factors will be reflected in your base premium or the cost of necessary endorsements.

Property Age and Construction

The physical characteristics of your rental property play a major role in pricing.

Building Materials: Masonry or brick construction is often cheaper to insure than wood-frame construction because it is more resistant to fire.

Age of Key Systems: The age and condition of the roof, electrical system, plumbing, and HVAC are critical. A brand new roof and updated copper plumbing with modern circuit breakers present a much lower risk of claims than a 25-year-old roof and outdated aluminum wiring. Many insurers offer significant discounts for newer systems.

Overall Condition: A well-maintained property is less likely to have claims. Insurers will consider the general upkeep of the property when underwriting the policy.

Coverage Selections

The coverage limits and deductibles you choose have a direct, linear impact on your premium.

Liability Limits: Increasing your liability coverage from $300,000 to $1,000,000 will increase your premium, but it often provides significant peace of mind for a relatively small additional cost.

Property Deductibles: Your deductible is the amount you pay out-of-pocket on a claim before the insurance company pays. A higher deductible (e.g., $5000 vs. $2500) will lower your annual premium because you are agreeing to take on more of the initial risk.

Claims History

Your personal claims history as a property owner follows you. If you have filed multiple property claims in the past three to five years, even on different properties, insurers will view you as a higher risk. A history of frequent claims, especially those related to water damage or liability, can lead to substantially higher premiums or even make it difficult to find coverage from standard carriers.

Meeting Mortgage Lender Insurance Requirements

If you are using a mortgage to finance your Utah rental property, your lender will have specific insurance requirements that you must meet before closing. Lenders do this to protect their financial interest in the property. Failure to secure the correct type and amount of coverage can delay or even derail your purchase.

Check your rate

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Check my rate →Mandated Hazard Insurance

Lenders will require you to obtain a "hazard insurance" policy. For a rental property, this almost always means a Special Form (DP-3) policy. A DP-3 policy provides "all-risk" coverage on the dwelling, meaning it is covered against all perils except those specifically listed as exclusions in the policy.

This is far more comprehensive than a Basic Form (DP-1) or Broad Form (DP-2) policy, which only cover a list of named perils. You can learn more about the differences in our comprehensive guide to landlord insurance.

Replacement Cost Value

This is a non-negotiable requirement for nearly all lenders. Your dwelling coverage limit must be equal to or greater than 100% of the property's Replacement Cost Value (RCV). RCV is the estimated cost to rebuild the property from the ground up with similar materials and quality at today's labor and material prices.

It is not the market value, which includes the land, or the purchase price. Lenders insist on RCV to ensure there are enough funds to completely restore their collateral in the event of a total loss.

Required Extended Perils

The lender will provide a list of perils that must be covered. A standard DP-3 policy typically includes all of these, such as:

- Fire and lightning

- Windstorm and hail

- Explosion

- Riot or civil commotion

- Smoke

- Vandalism and malicious mischief

Proof of Insurance

Before your loan can close, you must provide your lender with proof of insurance. This is typically done by sending them the Declarations Page of your new policy. This one-page summary lists the property address, the named insured, the policy period, the coverage types and limits, the deductibles, and, most importantly, lists the lender as the "mortgagee".

This mortgagee clause ensures the lender is notified if the policy lapses or is canceled and gives them an interest in any claim payments made for dwelling damage.

Additional Details for Utah Landlord Insurance

If your project involves financing, lender require their mortgagee clause on your policy, such as:

| Detail | Information |

|---|---|

| Mortgagee Clause | OfferMarket Capital LLC ISAOA/ATIMA 627 S Hanover St Baltimore, MD 21230 |

| Condos and PUDs in Utah | Blanket policies permitted if individual units are covered. Associations must maintain all-risk coverage for common areas and equipment at 100% replacement cost. |

| Instructions | Use ACORD forms for compliance. Submit insurance certificates, invoices, or paid receipts at least 24 hours prior to closing. Final policy documents due within 60 days post-closing. Notify your carrier if the property becomes vacant, and obtain a vacancy permit if needed. |

Utah-Specific Risks and Endorsements

Standard insurance policies are designed to cover common risks, but Utah landlords face unique perils that often require special attention and additional coverage through endorsements.

Earthquake Coverage

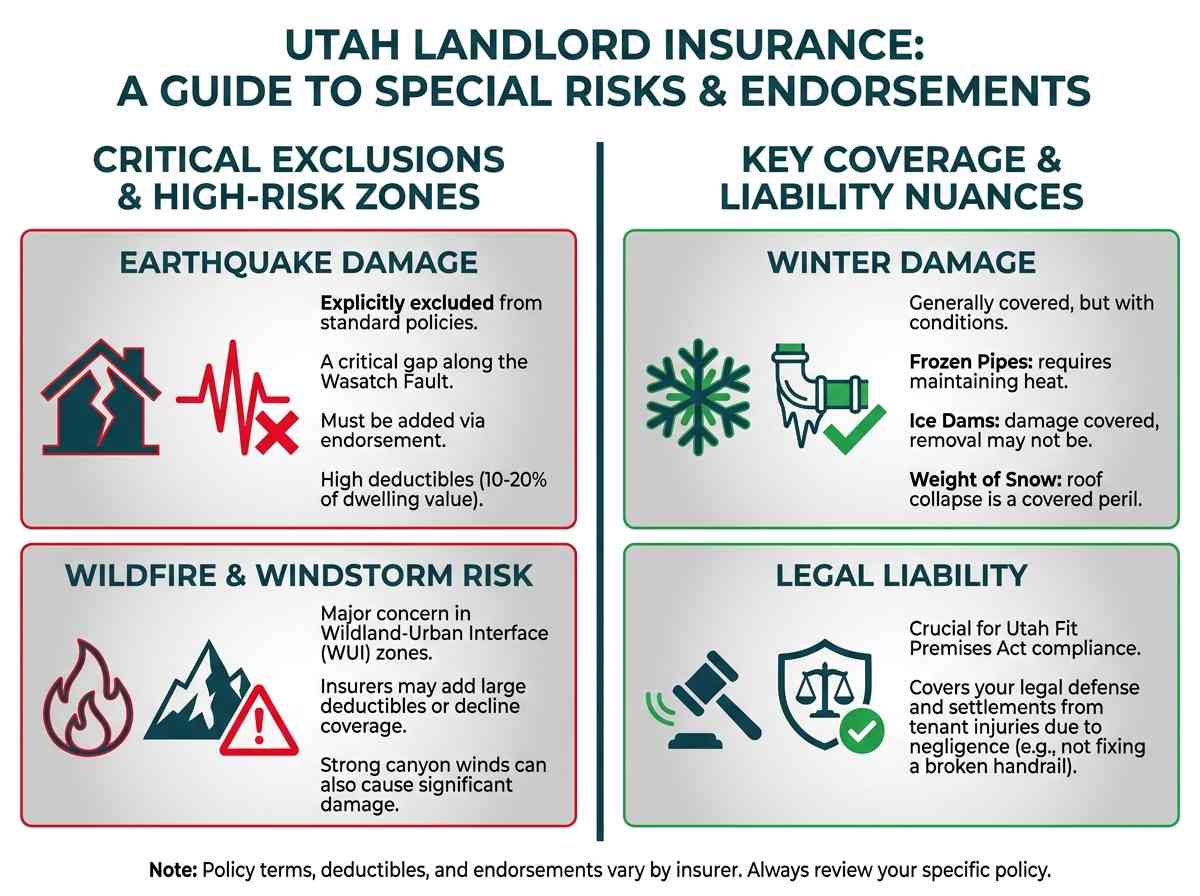

This is the most significant coverage gap for Utah property owners. Standard DP-3 policies explicitly exclude damage from earthquakes. Given that much of Utah's population and real estate value lies along the seismically active Wasatch Fault, this is a critical risk to address. Earthquake coverage must be added as an endorsement or purchased as a separate policy. It typically comes with a high deductible, often 10-20% of the dwelling's value, but it is the only way to protect your asset from catastrophic damage in a seismic event. For more information on Utah's earthquake risk, the Utah Geological Survey is an excellent resource.

Wildfire and Windstorm Risk

As development pushes further into the Wildland-Urban Interface (WUI), wildfire risk has become a major concern for insurers and property owners, particularly in the foothills and canyon communities. While fire is a covered peril, some insurers may add specific wildfire deductibles or even decline to cover properties in extremely high-risk zones. Similarly, strong canyon winds and microbursts can cause significant damage. It's crucial to review your policy to ensure there are no specific sub-limits or exclusions for wind and hail damage.

Winter Damage

Utah's cold winters bring a host of risks. A standard policy will generally cover sudden and accidental damage from winter weather, but there are important nuances:

Frozen Pipes: Coverage typically applies if a pipe bursts and causes water damage, but only if you have taken reasonable steps to maintain heat in the building.

Ice Dams: Damage to the dwelling caused by ice dams (ridges of ice at the edge of a roof that prevent melting snow from draining) is usually covered, but the cost to remove the ice dam itself may not be.

Weight of Ice and Snow: If heavy snow accumulation causes a roof to collapse, this is generally a covered peril.

Legal Liability

Your liability coverage should align with your responsibilities under the Utah Fit Premises Act. This state law requires landlords to provide safe and habitable living conditions. If you fail to maintain the property (e.g., not fixing a broken handrail) and a tenant is injured as a result, you could be found negligent. Your liability insurance is your financial backstop in these situations, covering legal defense and potential settlements.

Common Exclusions in a Standard Policy

Understanding what your landlord policy doesn't cover is just as important as knowing what it does. Misunderstanding these exclusions can lead to major financial shocks when a claim is denied.

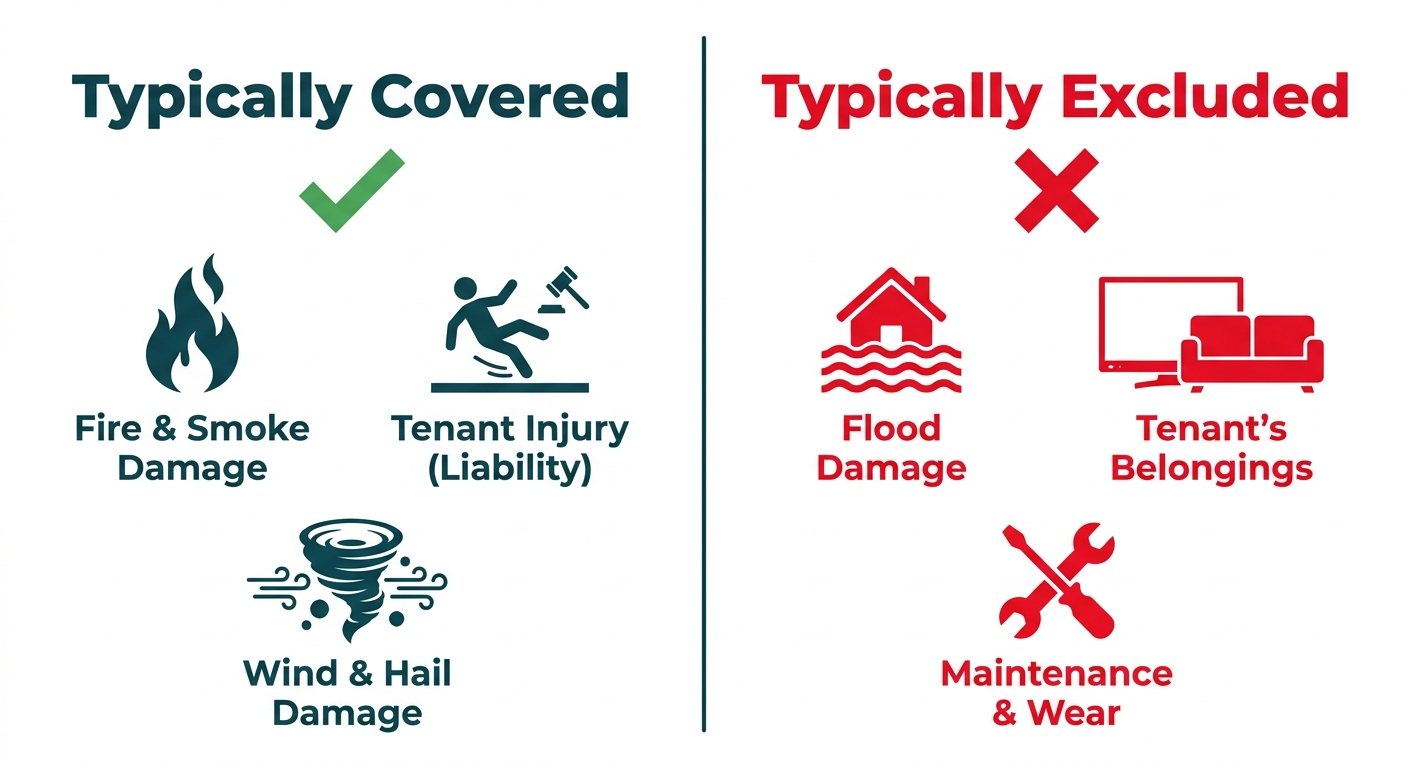

Tenant Personal Property

This is the most common point of confusion. Your landlord policy does not cover your tenant's personal belongings.

If a fire destroys the building, your policy will pay to rebuild the structure, but it will not pay to replace your tenant's furniture, clothes, or electronics. For this reason, it is a best practice for landlords to require their tenants to carry their own renters insurance policy. This not only protects the tenant but also reduces the likelihood of them trying to file a liability claim against you for their lost property.

Routine Maintenance and Wear

Insurance is designed to cover sudden and accidental losses, not predictable, gradual deterioration. Your policy will not pay to fix a leaky faucet, repair worn-out carpeting, or replace an appliance that has reached the end of its useful life. These are considered costs of doing business and are the landlord's responsibility. The line is crossed when a maintenance issue causes sudden damage; for example, if the old, leaky water heater suddenly bursts and floods the basement, the policy would cover the water damage, but likely not the cost of the new water heater itself.

Flood Damage

Similar to earthquakes, damage from flooding is excluded from all standard landlord insurance policies. Flooding is specifically defined as rising surface water from an outside source, like an overflowing river or heavy rainfall. To protect your property from this risk, you must purchase a separate flood insurance policy, which is typically administered through the National Flood Insurance Program (NFIP).

Vandalism by Tenant

While standard policies often include coverage for vandalism by third parties, damage done by a current tenant is frequently excluded. If a tenant maliciously damages the property before moving out, you may find yourself without coverage under a basic policy. Some carriers offer a specific endorsement to add coverage for this scenario, which is highly recommended.

Optional Coverages for Enhanced Protection

Beyond the standard package, you can add endorsements to your policy to close coverage gaps and tailor the protection to your specific needs.

Building Code Upgrade

Also known as "Ordinance or Law" coverage, this is crucial for older properties. If your rental is significantly damaged, current building codes may require you to make expensive upgrades during the repair process (e.g., installing a modern sprinkler system or updated wiring). A standard policy only pays to replace what was there before. This endorsement provides funds to cover the additional cost of bringing the property up to current code.

Vandalism and Malicious Mischief

While often included for third-party vandalism, it's important to confirm this coverage is on your policy. It protects you if your property is intentionally damaged, such as having windows broken or graffiti sprayed on the walls, especially during periods of vacancy between tenants.

Personal Injury Liability

Standard liability insurance covers bodily injury and property damage. Personal injury liability is a different category of risk. It provides coverage if you are sued for offenses such as:

- Wrongful eviction

- Wrongful entry

- Invasion of privacy

- Libel or slander

In an increasingly litigious environment, this coverage offers an essential layer of protection against tenant lawsuits that don't involve physical injury.

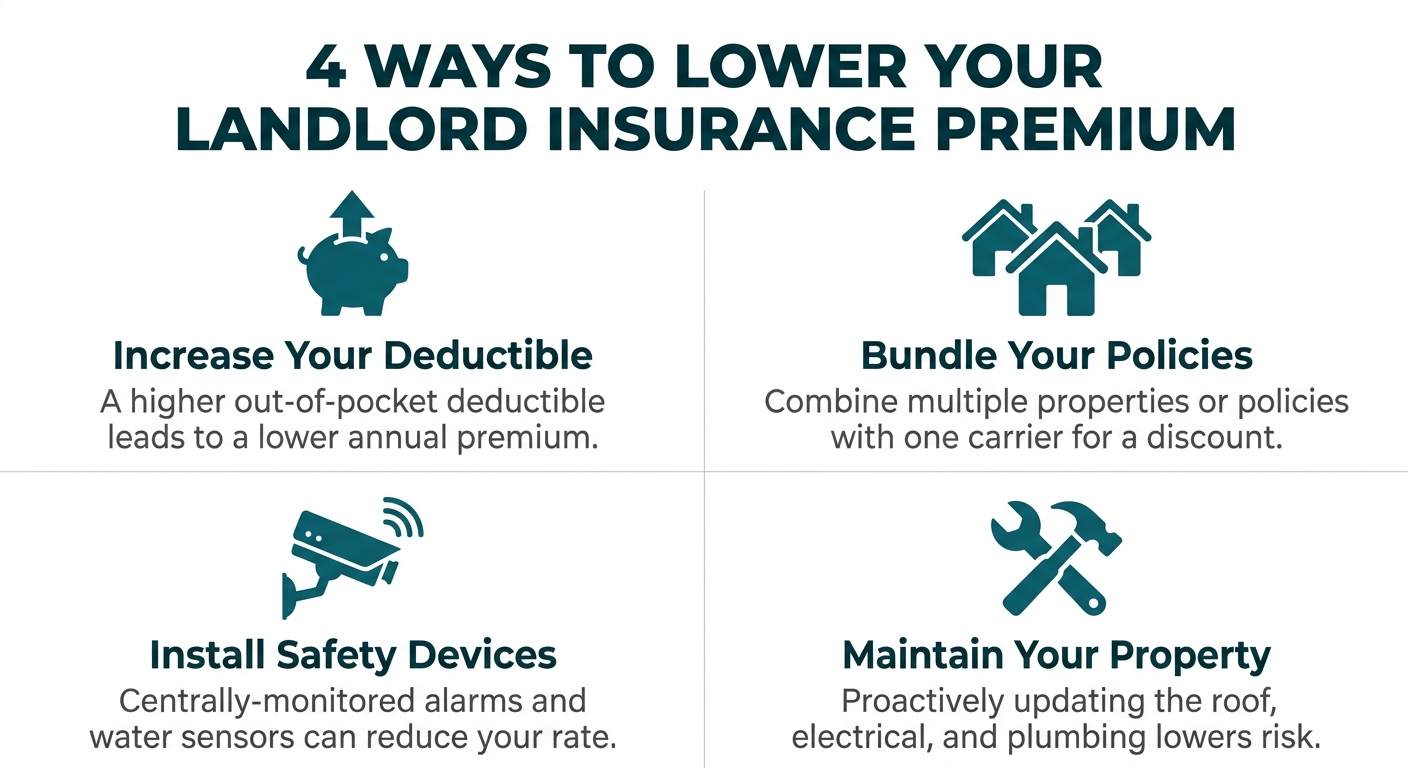

Actionable Steps to Lower Your Annual Insurance Premium

While you can't change your property's location, you can take several proactive steps to reduce your insurance costs:

Increase Your Deductible: Raising your deductible from $1,000 to $2,500 or even $5,000 can result in significant premium savings.

Bundle Your Policies: If you have multiple rental properties or need other insurance (like a primary home or auto policy), placing them with the same carrier can often unlock multi-policy discounts.

Install Safety and Security Devices: Insurers offer discounts for centrally-monitored fire and burglar alarms, automatic water shut-off valves, and smart home security systems.

Maintain Your Property: Proactively replacing an old roof, updating the electrical panel, or installing a new HVAC system can lower your risk profile and lead to a better rate.

Review Your Coverage Annually: Don't just "set it and forget it." Your needs and property values change over time. An annual review ensures you are not over- or under-insured and allows you to take advantage of new discounts or more competitive rates.

Securing Your Utah Landlord Insurance Policy

Finding the right balance of coverage and cost is key to protecting your investment effectively. OfferMarket's insurance platform shops 40+ carriers in a single submission, so you can compare rates and coverage without chasing individual agents or filling out multiple applications. The entire process takes under a minute.

How to Get an Instant Landlord Insurance Quote from OfferMarket

Go to OfferMarket and walk through a short form. Here is exactly what you will be asked and why each field matters.

Step 1: Select Your Coverage Type

Choose between Landlord or Fix and Flip. If the property is tenant-occupied or you are purchasing a rental, select Landlord. If you are actively rehabbing the property and it is not yet occupied, select Fix and Flip. This determines which carrier programs and policy structures apply to your quote.

Step 2: Enter the Subject Property Address

Input the address of the rental property you need insured in Utah. From the address, OfferMarket surfaces key coverage details for your property, including the comparison between DP-3 (Special Form) and DP-1 (Basic Form) policies. This is where you will see what each coverage type actually includes for your specific situation: open perils vs. named perils, whether water damage and burst pipes are covered or excluded, theft of materials and contents during vacancy or renovation, replacement cost vs. actual cash value settlement, loss of rent coverage, and vandalism protection.

DP-3 is the recommended coverage for rental property investors because it covers anything that happens to your property unless it is specifically excluded, while DP-1 only covers the short list of disasters explicitly written into the policy. Most of the coverage gaps landlords run into trace back to that one difference.

Step 3: Enter Monthly Rent

Input the current or projected monthly rent for the property. This helps determine your loss of rent (business interruption) coverage, which protects your rental income if the property becomes uninhabitable due to a covered event like a fire or storm.

Step 4: Enter Your Insured Entity Name

If the property is held in an LLC or trust, enter the entity name here. If you hold the property in your personal name, you can leave this blank. For investors financing with a DSCR loan, many lenders require the entity name on the insurance policy to match the borrowing entity exactly.

Step 5: Set Your Dwelling Coverage Amount

This is the estimated replacement cost to rebuild the property, not the purchase price or market value. If the property would cost $180,000 to rebuild from the ground up, that is your dwelling coverage number. We always recommend insuring at full replacement cost value to avoid coinsurance penalties. If you are unsure, start with your best estimate. OfferMarket's team will review the replacement cost estimate as part of the quote review process.

Step 6: Set Your Effective Date

This is when you want the policy to go into effect. If you are purchasing the property, use your closing or settlement date. If you already own the property and are switching carriers, you can set the effective date to today or your current policy's expiration date. If you are still in due diligence and your closing date is not finalized, a rough estimate works. You can adjust it later.

Step 7: Enter Your Claims History

How many insurance claims have you filed in the last five years? This applies to claims across all properties you own, not just the subject property. Carriers use claims history as a rating factor. Fewer claims generally means better rates. If you have zero claims in the last five years, that works in your favor.

Step 8: Enter Your Mailing Address

This is your personal or business mailing address, not the property address. Carriers use this for correspondence, billing, and in some cases as an additional underwriting data point.

Step 9: Enter Your Date of Birth

Standard identity verification that carriers require. This does not affect your premium.

Step 10: Submit and Get Your Instant Quote

Once you hit submit, OfferMarket shops your details across 40+ carriers and returns competitive quotes. From there, the in-house insurance team reviews every quote to close coverage gaps, flag any issues like inflated dwelling coverage or percentage-based wind/hail deductibles, and make sure the policy meets your lender's requirements if you are financing with a DSCR loan or fix and flip loan.

Why This Process Matters for Utah Landlords

Most insurance agents run a single carrier or a small handful. If that carrier's appetite does not match your property's risk profile, you are stuck with a higher premium or a coverage gap you did not know existed. OfferMarket removes that bottleneck by shopping the full market in one submission.

The in-house team then reviews what comes back, so you are not just getting the cheapest quote. You are getting the right coverage at the best price, with a team that understands what landlord insurance actually needs to include: replacement cost dwelling coverage, flat deductibles across all perils, adequate liability, loss of rent, and ordinance and law endorsements.

Get your instant landlord insurance quote and see how top-rated carriers compare for your Utah rental property.

Shop 40+ Carriers for Your Utah Rental Property

Enter your property address, coverage preferences, and get an instant landlord insurance quote. OfferMarket's team reviews every quote to make sure your coverage meets lender guidelines and protects your investment.

Get Insurance Quote →

OfferMarket Loans

Check your rate

60 seconds · no credit pull