*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Rural DSCR Loan

Last updated: June 12, 2026

For most real estate investors, a rural property is a quietly disqualifying detail they never see coming. You find a promising rental, run your numbers, line up a DSCR loan, and only deep into the process discover that the property is designated rural and your lender will not fund it. Rural designation is one of the most common and least understood reasons a DSCR loan falls apart. The good news is that the designation is knowable in advance, and a new option now exists for investors whose properties have long been shut out. Here is how rural designation works, why most lenders avoid it, and where the new program fits.

Rural DSCR Loan Guidelines

| Criteria: Rural DSCR Loan | Guidelines |

|---|---|

| Minimum loan amount | $75,000 |

| Maximum loan amount | $1,000,000 |

| Minimum property value | $25,000 |

| Maximum LTV | 100% (low balance) or 75% |

| Rural | Allowed |

| Maximum lot size | less than 10 acres |

| Appraisal | Desktop appraisal (less than $75,000 loan amount), or full appraisal (interior inspection) |

| Ineligible states | AK, AZ, CA, HI, MN, ND, NV, OR, SD, VT |

| Credit Pull | Hard |

| Minimum credit score | 680 |

| Minimum liquidity reserve | 3 months (single unit), 6 months (2-4 units) |

| Minimum DSCR | 1.0 |

| Experience | -5% LTV for less than 1 year of landlord experience |

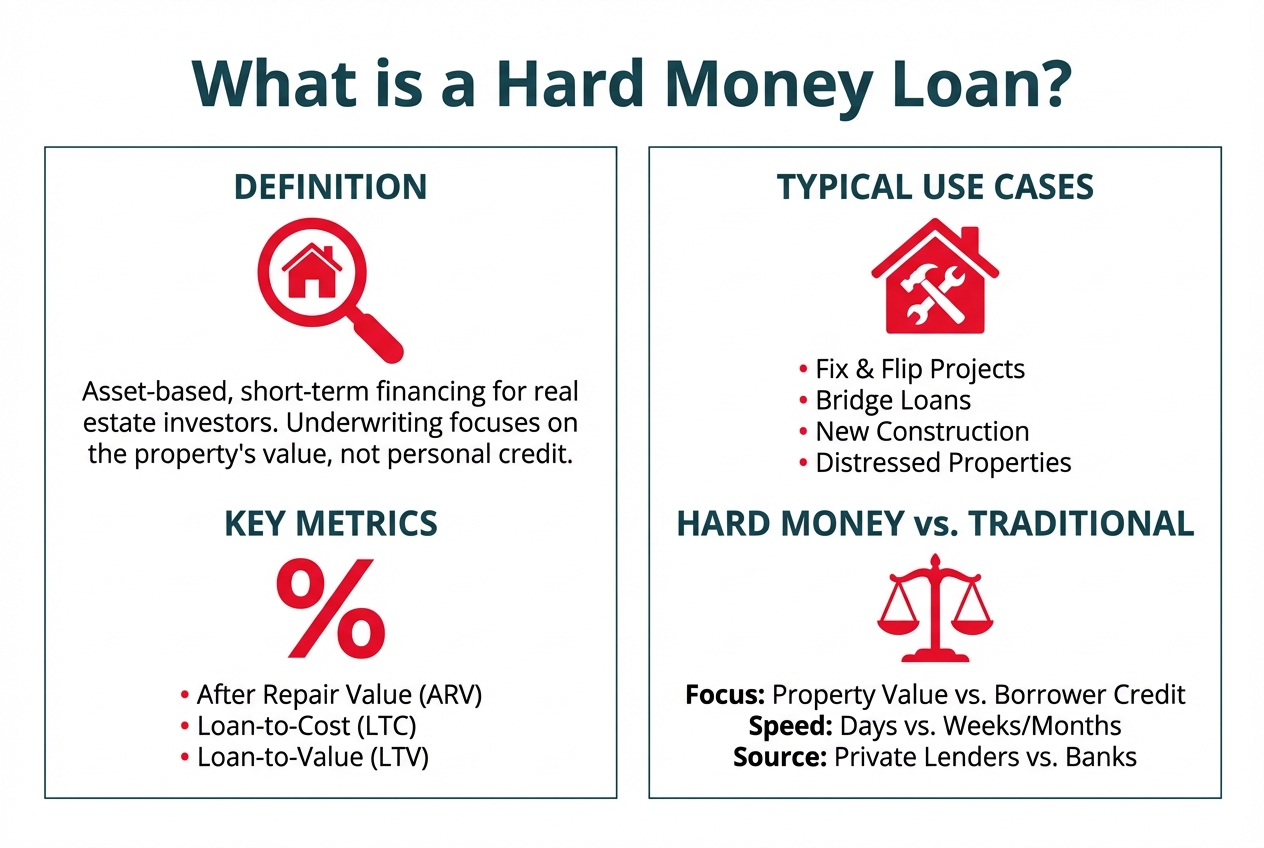

A Quick Refresher on DSCR Loans

A DSCR loan, short for Debt Service Coverage Ratio loan, is a financing product built specifically for real estate investors. Rather than qualifying the borrower based on personal income, tax returns, and employment, a DSCR loan qualifies the deal based on the property's ability to cover its own debt. The debt service coverage ratio compares the property's rental income to its debt obligations. When the income sufficiently covers the payment, the deal qualifies.

This focus on the property rather than the borrower is what makes DSCR loans so popular for one to four unit residential rental properties. But because these loans are frequently sold to fixed income investors through securitization, they must conform to guidelines that govern what kind of collateral is acceptable. Rural property is one of the most common exclusions in those guidelines, which is why so many investors run into a wall when the property sits outside a populated market.

How Lenders Decide a Property Is Rural

Most DSCR loan programs for one to four unit properties require an appraisal where the property is not flagged as rural, and lenders typically lean on three independent checks to make that determination. If any one of them indicates rural, the deal is usually dead at a standard lender. Investors should run these same checks themselves before committing to a property, because each is free and takes only a minute.

The Appraisal Neighborhood Characteristics Section

The first and most decisive check is the appraisal itself. Every residential appraisal includes a Neighborhood Characteristics section where the appraiser classifies the area as urban, suburban, or rural. Most DSCR loan programs require that the rural box is not checked. If the appraiser marks the property rural, the standard program cannot fund it, regardless of how strong the rest of the deal looks.

The CFPB Rural and Underserved Areas Tool

The second check is the Consumer Financial Protection Bureau's Rural and Underserved Areas Tool, available at https://www.consumerfinance.gov/rural-or-underserved-tool/. Most DSCR loan programs do not allow this tool to indicate that the property address is rural. If the result returns a Yes in the rural or underserved column, the property is considered rural.

If the result returns a No in that column, the property is not considered rural.

The USDA Property Eligibility Map

The third check is the USDA Property Eligibility map, available at https://eligibility.sc.egov.usda.gov/eligibility/welcomeAction.do?pageAction=sfp. Most DSCR loan programs do not allow the USDA map to indicate that the property is eligible for USDA funding, because USDA eligibility is itself a signal that the property is rural. The logic is straightforward: the USDA program exists specifically to support rural housing, so if a property qualifies for it, the property is rural by that program's definition.

If your search result shows the property as eligible, it is considered rural.

If your search result shows the property as ineligible, it is not considered rural.

Why Most Lenders Avoid Rural Properties

It helps to understand why rural designation is such a consistent dealbreaker, because the reasons are structural rather than arbitrary.

The first reason is liquidation risk. If a rural property goes into foreclosure, the lender faces a thinner market of potential buyers than it would in a dense metro area. Fewer buyers means a longer time to sell and a greater chance of having to accept a price below market value. Lenders price for that risk, and many simply choose to avoid it.

The second reason is securitization guidelines. Many private lenders do not hold their loans. They group loans together and sell portions as securities to fixed income investors. For a loan to be eligible for inclusion in one of these pools, both the property and the borrower must meet the pool's guidelines, and most investment property securitizations specifically exclude properties considered rural. A lender that funds a rural loan may find it cannot sell that loan, which defeats its business model. This is why the exclusion is so widespread even among lenders who would otherwise like the deal.

The New Rural DSCR Option

OfferMarket Capital LLC now offers DSCR loan funding for rural properties, opening a path for investors whose deals have traditionally been turned away. This addresses a real gap in the market, since a great deal of cash-flowing rental property sits in areas that the standard checks flag as rural, leaving otherwise creditworthy investors without conventional DSCR financing.

It is important to set expectations clearly. Not all rural properties are eligible. Property eligibility may vary, and this is not a guarantee of eligibility or funding. Rural lending carries the real risks described above, so each property is evaluated on its own merits rather than approved automatically. The point is that a rural designation is no longer an automatic dead end, which is a meaningful change for investors operating in these markets.

How Rural Designation Affects a Standard DSCR Loan

The table below distills how the three rural checks typically affect a standard DSCR loan and what the new rural option changes.

| Rural Indicator | How to Check | Effect on Standard DSCR Loan |

|---|---|---|

| Appraisal Neighborhood Characteristics | Rural box checked on the appraisal report | Typically disqualifies the deal |

| CFPB Rural and Underserved Tool | Returns Yes in the rural or underserved column | Typically disqualifies the deal |

| USDA Property Eligibility Map | Property shown as eligible for USDA funding | Typically disqualifies the deal |

| Rural DSCR option | Evaluated case by case | May be eligible for funding, subject to review |

Who Benefits Most

This program is best suited to investors who own or want to acquire one to four unit rental property in areas that the standard rural checks flag, yet which still produce solid rental income. If your appraisal is marked rural, or the CFPB or USDA tools point to a rural designation, a conventional DSCR program will likely turn you away, and the rural option may be the difference between financing the deal and walking away from it.

Before counting on it, run all three checks yourself so you understand exactly how the property is likely to be classified. If any of them indicate rural, the rural program may apply, but remember that eligibility is assessed property by property and is not guaranteed. As with any specialized program, it is worth confirming current availability and terms before building a deal around it.

Rural DSCR Loan Guidelines

| Criteria: Rural DSCR Loan | Guidelines |

|---|---|

| Minimum loan amount | $75,000 |

| Maximum loan amount | $400,000 |

| Minimum property value | $100,000 |

| Maximum LTV | 75% |

| Rural | Allowed |

| Maximum lot size | less than 10 acres |

| Appraisal | Drive-by (no interior inspection) or full appraisal (interior inspection) |

| Ineligible states | AK, AZ, CA, HI, MN, ND, NV, OR, SD, VT |

| Credit Pull | Hard |

| Minimum credit score | 680 |

| Minimum liquidity reserve | 3 months (single unit), 6 months (2-4 units) |

| Minimum DSCR | 1.0 |

| Experience | -5% LTV for less than 1 year of landlord experience |

Closing Thoughts

Most DSCR loan programs for one to four unit properties require an appraisal where rural is not checked in the Neighborhood Characteristics section, and they do not allow either the CFPB Rural and Underserved Areas Tool or the USDA Property Eligibility map to indicate that a property is rural. Those checks exist because rural property carries greater liquidation risk and is generally excluded from the securitizations that fund most DSCR loans. OfferMarket Capital LLC now offers DSCR loan funding for rural properties, though not all rural properties are eligible, property eligibility may vary, and this is not a guarantee of eligibility or funding.

For investors with cash-flowing rentals in rural markets, it is a practical path to financing that the standard programs have long left out.

Join 25,000+ Real Estate Investors

Sign up for your free OfferMarket account and join 25,000+ residential real estate investors. Membership is free and includes the following benefits:

- Low cost private lending

- Off market deal flow

- Insurance rate shopping

- Weekly market insights

OfferMarket Loans

Check your rate

60 seconds · no credit pull