*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Level Up Your Financing: Introducing the Portfolio DSCR Loan

A portfolio DSCR loan, often called a blanket loan, is a single mortgage used to finance a group of two or more investment properties. Instead of juggling multiple individual loans—each with its own payment date, interest rate, and servicer—you consolidate them under one streamlined financing vehicle. This approach treats your rental properties as what they are: a unified, income-generating portfolio. The loan's approval isn't based on your personal W-2 income but on the collective cash flow of the properties themselves, measured by the Debt Service Coverage Ratio (DSCR).

This financial tool is specifically designed for seasoned real estate investors who are focused on strategic growth and operational efficiency. By bundling properties, you can unlock significant savings on closing costs, simplify your administrative workload, and free up equity more effectively to accelerate future acquisitions. It's a move from financing properties one by one to managing your entire real estate enterprise with a single, powerful financial instrument.

Defining the Portfolio DSCR Loan (The Blanket Loan)

At its core, a portfolio Debt Service Coverage Ratio (DSCR) loan is a specialized, non-qualified mortgage (non-QM) commercial real estate product designed for real estate investors. While the terms "portfolio loan" and "blanket loan" are often used interchangeably, they both refer to the same concept: a single loan that is secured by multiple properties. This lien is "blanket" in that it covers all the assets in the bundle.

The primary function of this loan is to leverage the combined strength of your properties. Lenders underwrite the loan based on the "blended" or "global" DSCR of the entire portfolio. This means the total net operating income (NOI) from all properties is divided by the total debt service for the proposed new loan. This aggregation allows stronger-performing properties to support weaker ones, enabling you to finance assets that might not qualify for a loan on their own. It's a strategic tool designed for investors who have moved beyond their first few doors and are now managing a true portfolio. The core value isn't just convenience; it's about creating a more robust and scalable financial foundation for your real estate business.

Who is the Ideal Candidate for a Portfolio DSCR Loan?

While a powerful tool, the portfolio DSCR loan isn't for everyone. It's tailored for a specific type of real estate professional who has reached a certain scale and is looking for sophisticated financing solutions.

Experienced Investors with Multiple Properties: The most obvious candidates are investors who already own a collection of rental properties, typically a minimum of two to five, and are feeling the administrative strain of managing individual mortgages. They understand the cash flow dynamics of their assets and are looking for a more efficient way to manage their debt.

Investors Seeking to Refinance and Consolidate: If you have multiple existing loans, perhaps with varying interest rates and maturity dates, a portfolio loan offers a powerful way to consolidate. You can refinance all of them into a single loan with a consistent interest rate and one monthly payment, often pulling cash out in the process to fund new deals.

Investors Acquiring a Property Bundle: This loan is perfect for purchasing a package of properties in a single transaction. Instead of applying for separate loans for each property—a process that would be slow, expensive, and administratively nightmarish—you can secure financing for the entire bundle at once. This is common when buying a portfolio from another investor or a turnkey provider.

Real Estate Professionals Focused on Scaling: The ultimate goal of a portfolio loan is to facilitate growth. By streamlining your existing debt and potentially tapping into collective equity, you create a more efficient financial engine. This frees up both capital and mental bandwidth, allowing you to focus on finding the next deal rather than managing paperwork for the last one. If your strategy involves rapid and repeated acquisitions, establishing a portfolio loan facility with a lender like OfferMarket can be a game-changer.

The Strategic Advantages of Bundling Your Properties

Shifting from a property-by-property financing approach to a portfolio strategy is more than a simple consolidation of debt. It's a fundamental change in how you manage and scale your real estate business. The advantages are tangible, impacting your time, your bottom line, and your capacity for future growth.

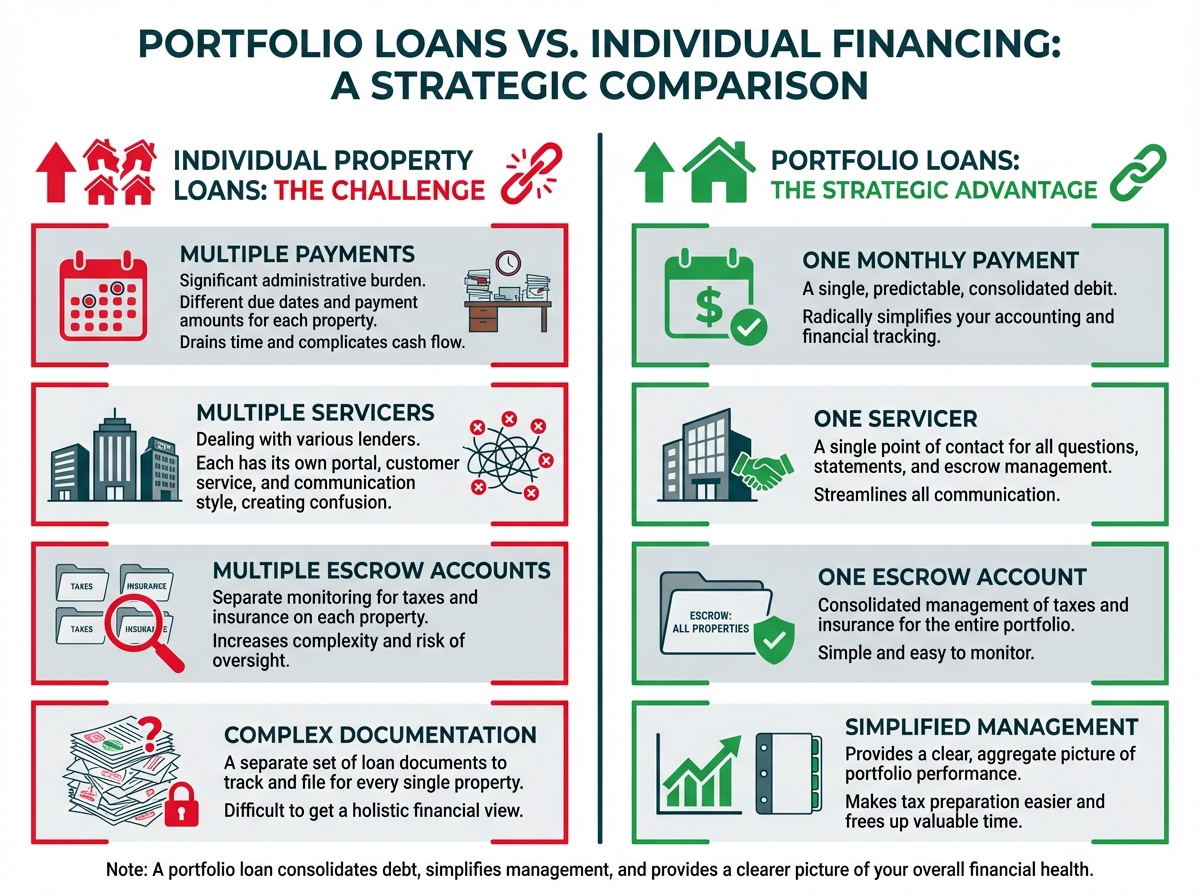

Drastic Simplification and Streamlined Management

The most immediate benefit of a portfolio loan is the radical simplification of your administrative tasks. Consider the complexity of managing five separate rental property loans:

- Five different monthly payments: Each potentially due on a different day of the month.

- Five different loan servicers: Each with its own online portal, customer service number, and communication style.

- Five different escrow accounts: For taxes and insurance, each requiring separate monitoring.

- Five different sets of loan documents: To track and file.

This administrative burden is a significant drain on an investor's most valuable resource: time. A portfolio loan collapses this complexity into a single, manageable structure.

- One Loan: A single set of documents to understand and file.

- One Monthly Payment: A predictable, consolidated debit from your account on the same day each month.

- One Servicer: A single point of contact for all questions, statements, and escrow management.

This streamlined approach simplifies your accounting and makes it significantly easier to track the financial performance of your portfolio as a whole. You can see the aggregate cash flow and debt service in one place, providing a clearer picture of your overall financial health and making tax preparation far less of a headache.

Significant Cost Savings on Financing

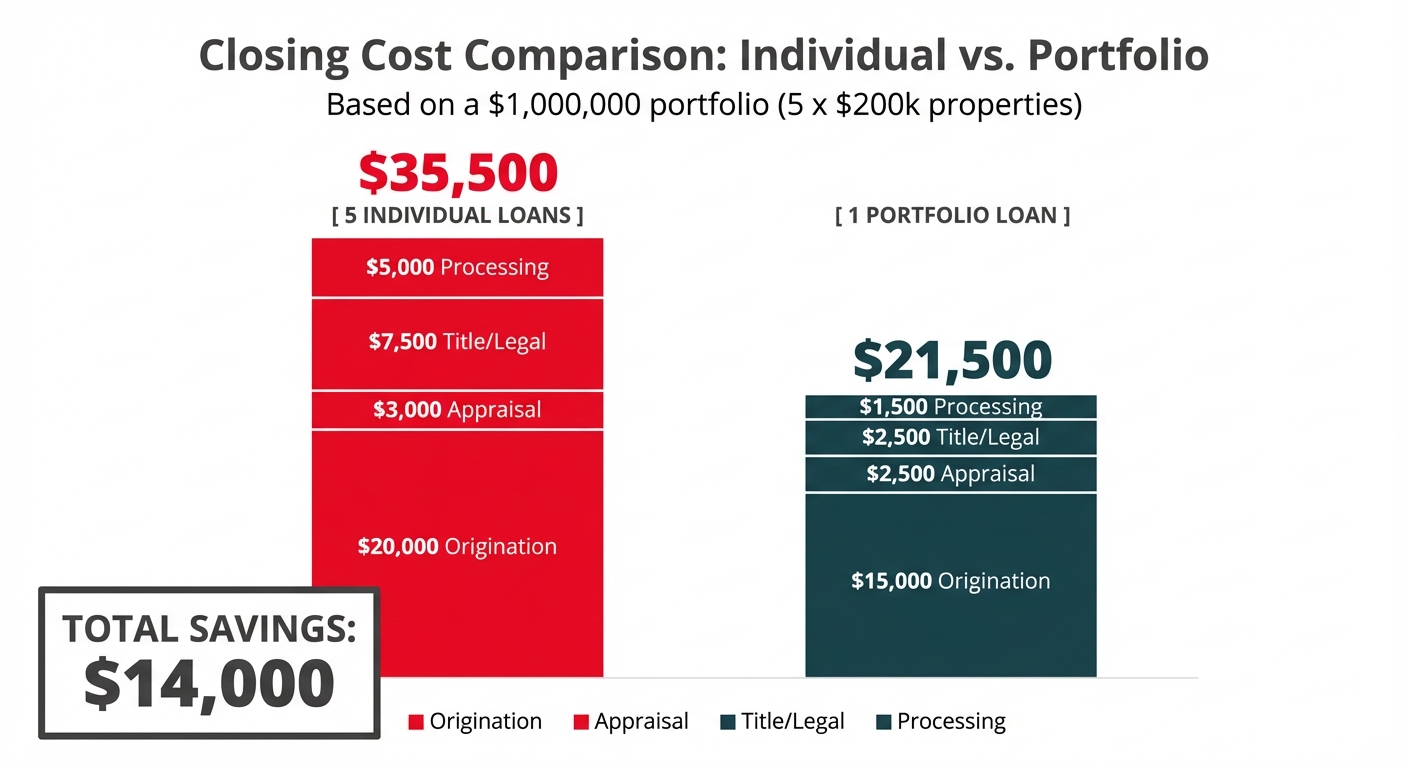

Financing properties individually means incurring a full set of closing costs for every single transaction. These costs can add up quickly and erode your investment returns. A portfolio loan allows you to bundle these expenses, resulting in substantial savings.

Let's imagine you're refinancing five properties, each valued at $200,000, for a total portfolio value of $1,000,000.

Scenario A: Five Individual DSCR Loans

- Origination Fee (2%): $4,000 x 5 = $20,000

- Appraisal Fee: $600 x 5 = $3,000

- Title/Legal Fees: $1,500 x 5 = $7,500

- Processing/Underwriting Fee: $1,000 x 5 = $5,000

- Total Closing Costs: $35,500

Scenario B: One Portfolio DSCR Loan with OfferMarket

- Origination Fee (1.5% portfolio discount): $15,000

- Appraisal Fee (bulk discount): $2,500

- Title/Legal Fees (one closing): $2,500

- Processing/Underwriting Fee (one loan): $1,500

- Total Closing Costs: $21,500

In this conservative example, the investor saves $14,000 simply by choosing a portfolio loan. At OfferMarket, we recognize the efficiencies of underwriting multiple properties at once and pass those savings directly to you. We provide discounts on origination fees and work with appraisal management companies to secure bulk pricing, directly improving your margins and putting more money back into your pocket for your next investment.

Accelerated Portfolio Growth and Velocity

For serious investors, speed and momentum are critical. The faster you can close a deal and recycle your capital, the faster your portfolio grows. Individual financing is inherently slow. A portfolio loan acts as a growth accelerator in several key ways:

Simultaneous Equity Release: Instead of doing a cash-out refinance on one property at a time, a portfolio loan allows you to tap into the combined equity of all your properties in a single transaction. This can provide a substantial lump sum of capital that can be immediately deployed to acquire new assets, including larger multi-family properties or another bundle of single-family rentals.

Establish a Financing Relationship: By closing a portfolio loan, you establish a strong relationship with a lender who now understands your entire portfolio. This makes future financing much faster. When you find your next deal, the lender already has your entity documents, financial history, and a master file. This can shave weeks off the closing timeline for subsequent acquisitions.

Faster Portfolio Acquisitions: When you're buying a package of properties, a portfolio loan is exponentially faster. The due diligence, underwriting, and closing processes are unified. This speed can be a significant competitive advantage in a hot market, making your offer more attractive to sellers who want a quick, clean closing.

Improved Cash Flow Management and Risk Mitigation

A portfolio loan leverages the power of diversification to improve your overall financial stability. By blending the performance of all your properties, you create a more resilient cash flow stream.

The Power of a Blended Portfolio: In any real estate portfolio, some properties will be star performers while others may temporarily underperform due to a vacancy or unexpected repairs. With individual loans, a vacancy in one property could strain your ability to cover its specific mortgage payment. In a portfolio loan, the strong cash flow from your other nine properties easily covers the debt service for the entire bundle, smoothing out the month-to-month volatility. This "global" cash flow provides a crucial safety net.

Predictable Debt Service: With one consolidated payment, your largest monthly expense becomes highly predictable. This simplifies budgeting and financial forecasting. You know exactly what your total debt obligation is each month, allowing for more precise cash flow management and strategic planning for capital expenditures. This stability is essential for mitigating risk and ensuring the long-term health of your investment portfolio.

Under the Hood: How Portfolio DSCR Loans are Underwritten

The underwriting process for a portfolio DSCR loan is more complex than for a single-property loan, but it’s designed to assess the health of your entire real estate enterprise. Lenders look at a combination of blended cash flow, property characteristics, and investor strength. Understanding these key components is crucial for positioning your portfolio for a successful approval.

The Power of Blended DSCR

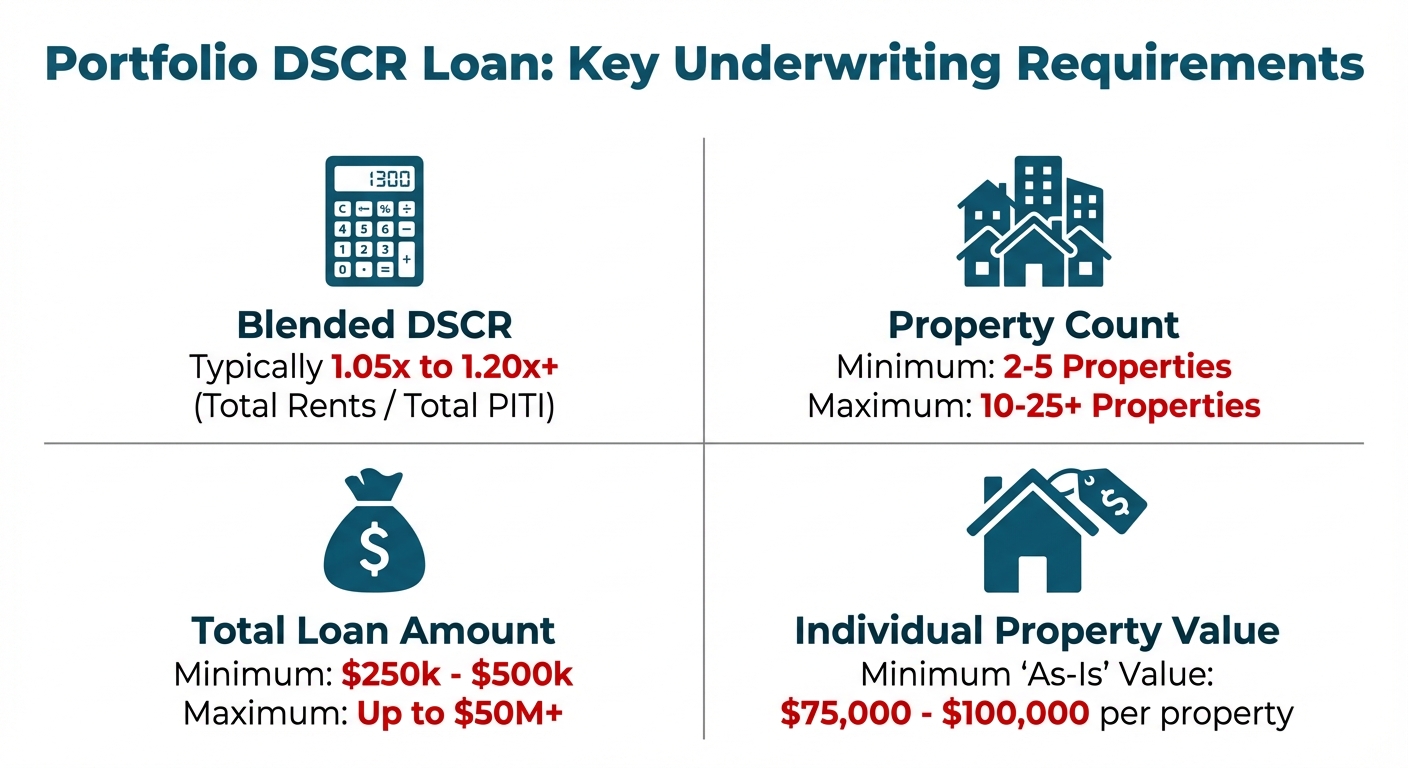

The single most important metric in portfolio loan underwriting is the "blended" or "global" Debt Service Coverage Ratio (DSCR). Instead of evaluating each property on a standalone basis, the lender aggregates the income and expenses for the entire group.

Blended DSCR = Total Gross Rental Income (for all properties) / Total PITIA (for the new single loan)

- Total Gross Rental Income: The sum of the monthly rents from every unit across all properties in the portfolio.

- Total PITIA: The proposed single monthly payment for the new portfolio loan, including Principal, Interest, Taxes, Insurance and HOA for all properties combined.

An Important Underwriting Nuance: While lenders calculate this aggregate "Loan DSCR" to approve the overall blanket loan, many programs also require an individual DSCR calculation for each specific property in the portfolio. They do this to ensure no single property is a severe liability. For example, if more than 25% of the individual properties in a blanket loan have a DSCR below 1.00x, the lender may penalize the entire portfolio with a 10% reduction to the maximum allowable LTV.

The magic of the blended DSCR lies in its ability to balance the portfolio. A high-cash-flowing property can compensate for a property with break-even or slightly negative cash flow.

Example:

An investor has two properties they want to refinance into a portfolio loan.

Property A (Strong Performer):

- Gross Rent: $2,500/mo

- Proposed PITIA: $1,500/mo

- Individual DSCR: $2,500 / $1,500 = 1.67x

Property B (Weaker Performer):

- Gross Rent: $1,800/mo

- Proposed PITIA: $1,700/mo

- Individual DSCR: $1,800 / $1,700 = 1.06x

While Property B has a very low DSCR that might not qualify for a loan on its own, the blended calculation tells a different story:

- Total Gross Rent: $2,500 + $1,800 = $4,300

- Total Proposed PITIA: $1,500 + $1,700 = $3,200

- Blended DSCR: $4,300 / $3,200 = 1.34x

With a strong blended DSCR of 1.34x, the portfolio is easily approved. Most lenders require a minimum blended DSCR between 1.05x and 1.20x, depending on the loan-to-value (LTV), credit score, and number of properties. This blending ability is what allows investors to finance entire portfolios efficiently, without leaving underperforming but otherwise valuable assets behind.

Curious if your portfolio qualifies? Use our free DSCR Calculator to input your properties' rents and estimated expenses to see your blended DSCR in seconds.

Maintaining Flexibility with the Partial Release Clause

The most common concern investors have about blanket loans is the fear of being "trapped." What if you want to sell one of the properties in the portfolio? Are you forced to refinance the entire loan? The answer lies in a critical loan feature: the partial release clause.

A partial release clause is a provision in the loan agreement that allows the borrower to sell an individual property from the portfolio and have the lender release the lien on that specific property, without triggering a due-on-sale clause for the entire loan. This is a non-negotiable feature for any savvy investor.

Here’s how it typically works:

- Sale of a Property: You find a buyer for one of the ten properties in your portfolio loan.

- Paydown Requirement: To release the lien, the lender will require a paydown of the principal loan balance. This amount is usually greater than the allocated loan amount for that specific property. The standard requirement is 120% to 125% of the original loan amount attributed to that asset.

- Lien Release: Once the paydown is made from the sale proceeds, the lender releases their security interest in that one property, and the sale can close. The rest of your portfolio loan remains intact, albeit with a lower principal balance and a recalculated monthly payment.

This clause provides the essential flexibility to manage your portfolio actively—selling off underperforming assets, capitalizing on market appreciation, or executing a 1031 exchange—while still enjoying the benefits of a consolidated portfolio loan. When vetting lenders, always confirm the specifics of their partial release clause.

Understanding Size and Valuation Requirements

Lenders have specific "buy boxes" for the types of portfolios they will finance. These criteria ensure the portfolio is large enough to be efficient to service but not so large that it introduces excessive concentration risk.

Minimum and Maximum Property Count: Most lenders require a minimum of 2 to 5 properties to qualify for a portfolio loan. The maximum number of properties can vary significantly, from 10 to 25, or even more for very large institutional lenders.

Loan Amount Thresholds: There is typically a minimum total loan amount, often starting around $250,000 to $500,000. The maximum loan amount can scale into the tens of millions, with some lenders like OfferMarket capable of handling portfolios up to $50 million.

Individual Property Value Floors: Lenders need to ensure that each property in the portfolio has a certain baseline value to justify the cost of underwriting and servicing. There is almost always a minimum "as-is" appraised value for each individual property, typically ranging from $75,000 to $100,000. Properties below this threshold may not be eligible for inclusion in the portfolio.

Occupancy and Recourse: The Non-Negotiables

Beyond the numbers, lenders have two critical requirements that address the operational stability and security of the loan.

Portfolio Occupancy Floors: Lenders need to see that your portfolio is stabilized and generating income at the time of closing. The industry standard is a 90% occupancy requirement. This means that at least 90% of the total units across all properties in the portfolio must be leased to qualified tenants. A portfolio with high vacancy is seen as a significant risk, as it indicates potential management issues or weak market demand. Lenders want to finance proven, income-producing assets, not speculative turnaround projects.

The Full Recourse Personal Guarantee: This is a crucial point for investors to understand. Unlike some single-asset DSCR loans that can be non-recourse, portfolio loans almost universally require a full recourse personal guarantee from the principals of the borrowing entity. A recourse loan means that if the portfolio defaults and the sale of the properties does not cover the outstanding loan balance, the lender has the right ("recourse") to pursue the personal assets of the guarantor to satisfy the debt.

Why is this required? Because a portfolio loan represents a larger, more concentrated risk for the lender. The personal guarantee ensures the investor has significant "skin in the game" and is fully committed to the success of the portfolio. It's a key component of the security package for the lender. It's worth noting an important market trend: even major capital providers in the space, like ROC Capital, have moved away from non-recourse options for these types of loans, highlighting that full recourse is now the firm industry standard.

What is a DSCR Loan? A Foundation for Investors

Before diving deeper into portfolio strategies, it's essential to have a solid understanding of the underlying loan product: the DSCR loan. This financing tool is the engine that powers modern real estate investment, and its principles are the foundation upon which portfolio loans are built.

Defining the Debt Service Coverage Ratio (DSCR)

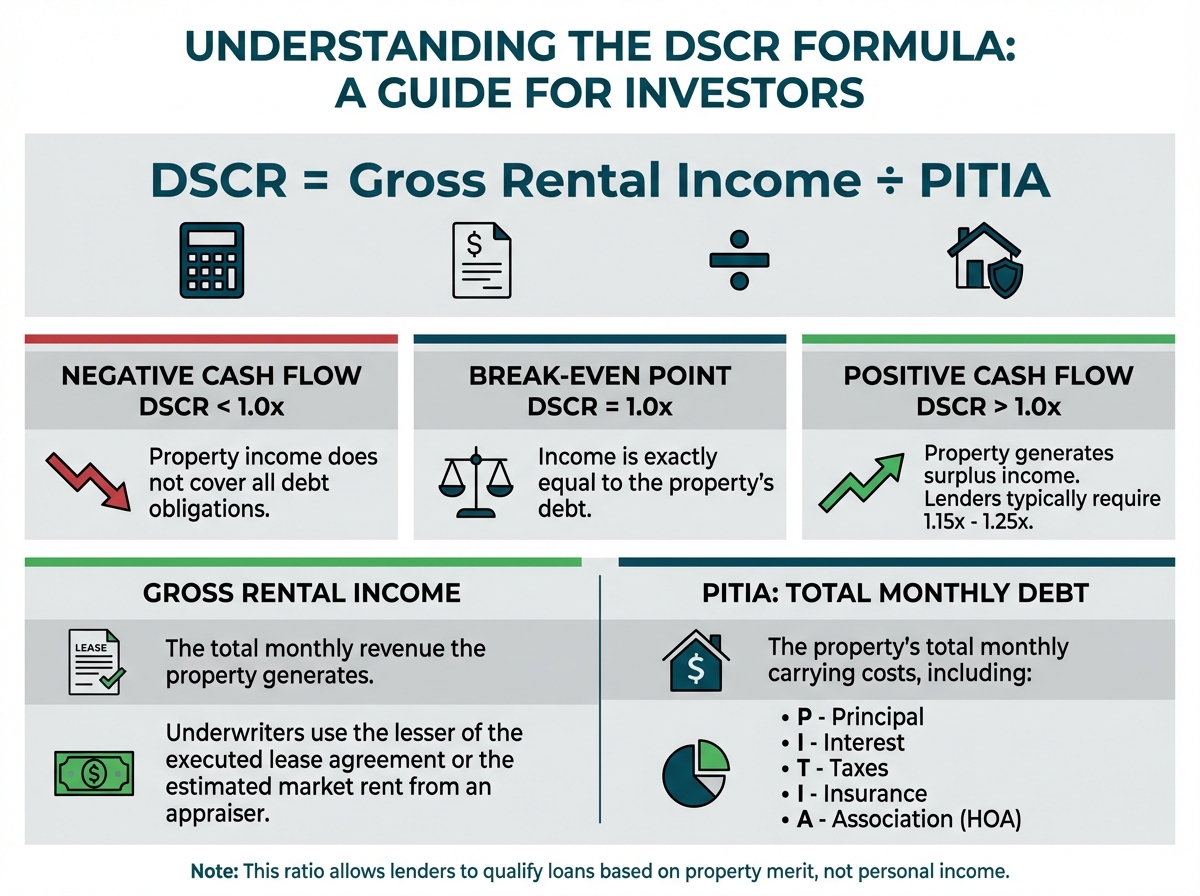

The Debt Service Coverage Ratio is a simple yet powerful calculation used by lenders to determine if a rental property's income is sufficient to cover its mortgage-related debt obligations. It's the primary underwriting metric for these types of loans.

The core formula is:

DSCR = Gross Rental Income ÷ PITIA

Where PITIA = Principal + Interest + Taxes + Insurance + HOA

A DSCR of 1.0x means the property generates exactly enough income to cover the debt—it breaks even. A DSCR below 1.0x means the property has negative cash flow, losing money each month. A DSCR above 1.0x means the property has positive cash flow. Lenders almost always require a DSCR to be above 1.0x, typically in the 1.15x to 1.25x range for a single property, to ensure there is a cash flow buffer for vacancies and unexpected expenses.

Here is the breakdown of the formula:

Gross Rental Income (The Numerator): This is the monthly revenue the property generates. For standard long-term rentals, underwriters typically use the lesser of the actual executed lease agreement or the estimated market rent provided by the appraiser on Form 1007 or 1025.

PITIA (The Denominator): This represents the property's total monthly carrying costs. It stands for Principal, Interest, Taxes, Insurance, and Association (HOA) dues.

By focusing on this ratio, lenders can make a loan decision based purely on the investment merit of the property itself, without needing to verify the borrower's personal salary.

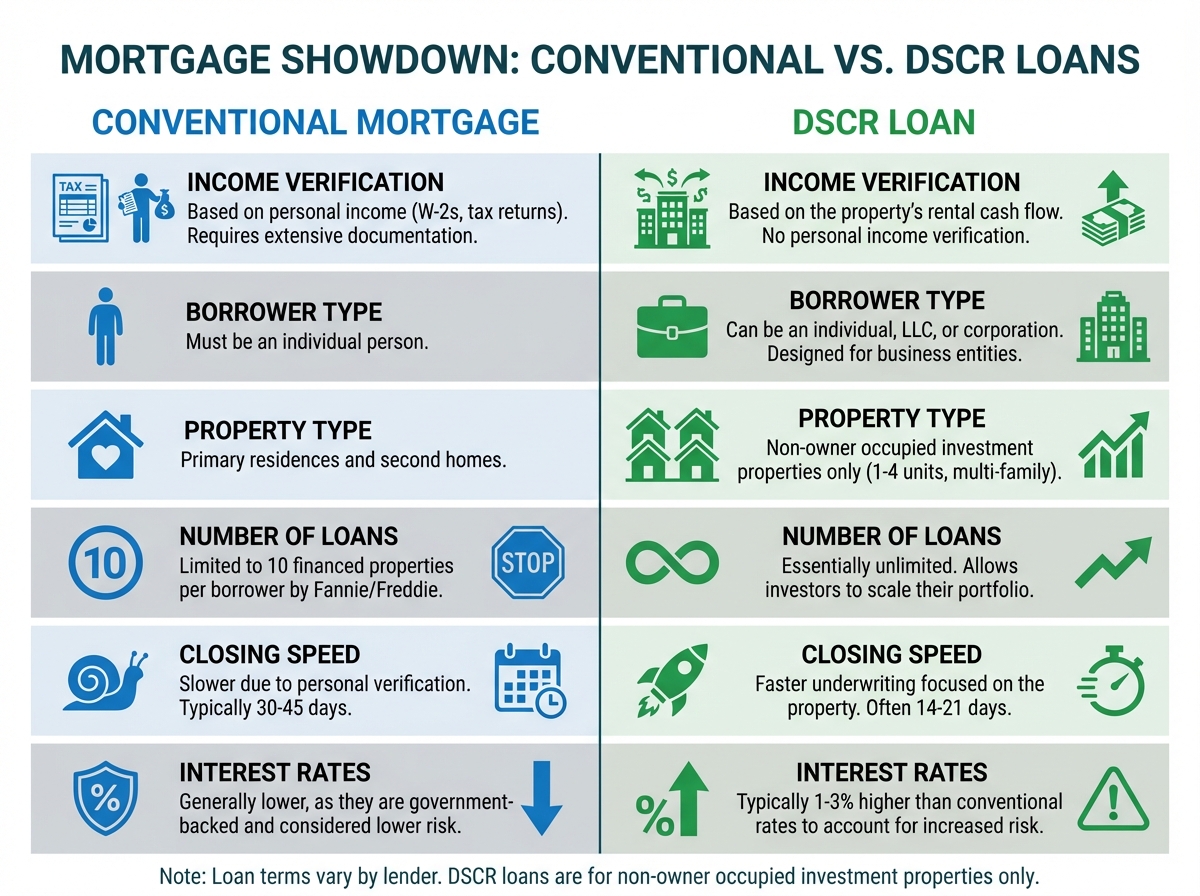

How DSCR Loans Differ from Conventional Mortgages

DSCR loans were created specifically for real estate investors and operate very differently from the conventional (Fannie Mae/Freddie Mac) mortgages you would get for a primary residence.

| Feature | Conventional Mortgage (for Primary Home) | DSCR Loan (for Investment Property) |

|---|---|---|

| Income Verification | Based on personal income (W-2s, tax returns, pay stubs). Requires extensive documentation of borrower's ability to pay. | Based on property's cash flow (DSCR). No personal income verification required. |

| Borrower Type | Must be an individual person. | Can be an individual, but designed for business entities like an LLC or corporation. |

| Property Type | Primary residences, second homes. | Non-owner occupied investment properties only (1-4 units, multi-family, etc.). |

| Number of Loans | Limited by Fannie/Freddie to 10 financed properties per borrower. | Essentially unlimited. Investors can use DSCR loans to finance dozens of properties. |

| Closing Speed | Slower due to extensive personal income and asset verification. Typically 30-45 days. | Faster, as underwriting is focused solely on the property. Often 14-21 days. |

| Interest Rates | Generally lower, as they are government-backed and considered lower risk. | Typically 1-3% higher than conventional rates to account for increased risk. |

The key takeaway is that DSCR loans are a business-purpose loan. They treat real estate investing as a business, where the asset's performance is what matters, not your day job.

Pros and Cons of a Standard (Single Property) DSCR Loan

It's important to understand the strengths and weaknesses of the standard, single-property DSCR loan, as it's the building block for many investors.

Pros:

Unlimited Financed Properties: Overcomes the 10-property limit imposed by conventional lenders, making it the go-to tool for scaling.

No Personal Income Verification: Your ability to scale is tied to your ability to find good deals, not the size of your W-2 salary.

Fast and Efficient: The streamlined documentation and property-focused underwriting lead to quicker closings.

Asset Protection: Allows you to purchase and hold properties in an LLC, which can help shield your personal assets from liability.

Cons:

Higher Interest Rates and Fees: The convenience and flexibility come at a cost. Rates and origination fees are typically higher than conventional loans.

Requires Strong Cash Flow: The property must generate sufficient income to meet the lender's minimum DSCR requirement, which can be challenging in high-price, low-rent areas.

Inefficient at Scale: While you can finance 20 properties with 20 individual DSCR loans, managing them becomes a significant administrative burden, which is precisely the problem that portfolio loans solve. Each closing comes with its own set of costs, and each loan adds another monthly payment to track.

For an investor with more than a handful of properties, the cons of managing individual DSCR loans begin to outweigh the pros, making the transition to a portfolio loan a logical and necessary next step for continued growth.

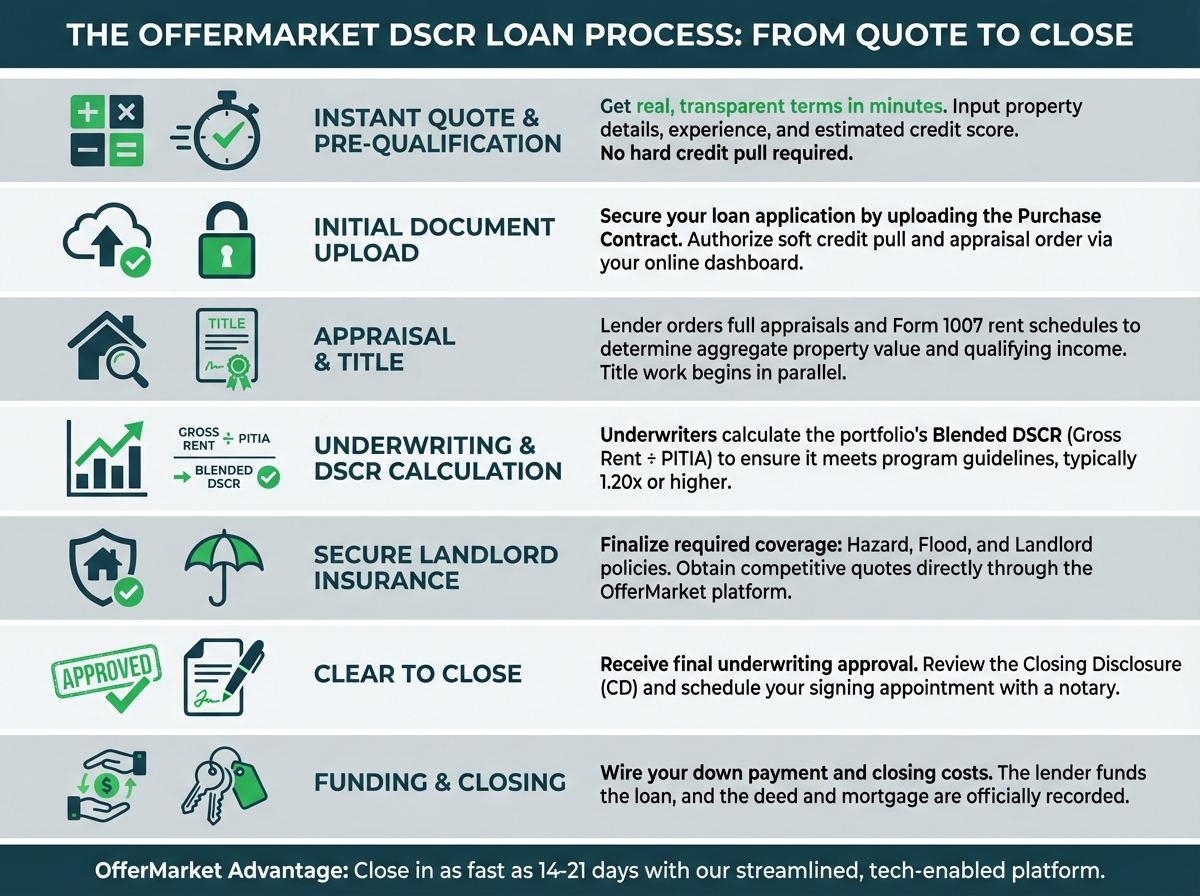

The OfferMarket Application Process: From Instant Quote to Closing Day

Securing a portfolio DSCR loan is a straightforward process, especially when working with a tech-enabled lender like OfferMarket. While there are more moving parts than a single-property loan, the steps are logical and designed to ensure a smooth transaction from initial inquiry to funding. Here’s a breakdown of what you can expect.

Step 1: Pre-qualification and Getting Your Instant Quote

At OfferMarket, we've streamlined this with our Instant Quote tool. Instead of filling out pages of paperwork and waiting days for a response, you can get real, transparent terms in minutes. You'll need to provide:

- Your investment experience (number of flips/rentals in the last 36 months)

- Estimated credit score (no credit pull)

- Borrowing entity (Personal name or LLC)

- Portfolio loan (i.e. for multiple properties)

- Property type

- Unit size

- Subject property address

- Loan Purpose

- Estimated as-is value

- Purchase price

- Tenant type

- Leasing strategy

- Monthly rent

- Annual taxes

- Annual insurance

- Annual HOA

- Citizenship status

OfferMarket Advantage: Our instant quote system lets you run the numbers on potential deals before you even submit a formal application. You can run multiple property scenarios through our calculator to identify which investments offer the best cash flow potential, ensuring you only submit applications for properties that make financial sense.

Step 2: Upload Purchase contract and complete sections marked URGENT

Once you move forward, our streamlined system walks you through the full underwriting checklist inside your dashboard.

First you will need to complete Processing section that are marked URGENT. We like to kick off our process by having you upload a Purchase Contract, authorize a soft credit pull through our website as well as complete a loan application where you enter some additional information.

If your property requires an appraisal we also like you to complete appraisal authorization on the first day so we can order the appraisal on the next business day which should accelerate all the timelines. In some cases for fix and flip loans we allow a desktop appraisal which make things a lot more streamlined.

Step 3: Upload remaining documents

You’ll complete and upload:

- ID Verification

- Bank Statements

- Borrowing Entity Details (LLC/Corp)

- W-9 Form

- ACH Form

- Primary residence verification

- Incumbency certificate

- Insurance information (OfferMarket can help with that since we specialize in insurance for Fix and Flip properties)

Step 4: Property Appraisal and Title

Property appraisals are the most critical piece of a Portfolio DSCR loan because they determine the aggregate property value and the qualifying rental income for the entire pool of assets. The lender orders full appraisals for each property in the portfolio, including Form 1007 (Single-Family Comparable Rent Schedule) for every individual unit.

Portfolio Appraisal Components:

- Aggregate Property Value: Determines the total market value of the portfolio using comparable sales for each asset.

- Form 1007 Rent Schedules: Establishes market rent for every property in the portfolio based on local comparable rentals.

- Property Conditions: Documents the physical state of each asset and identifies any cross-collateralization risks or needed repairs.

- Rental Market Analysis: Provides regional context on rental demand and typical lease terms across the different markets within the portfolio.

Rent Determination Rules:

- The lender uses the lower of the actual lease amount or the appraised market rent for each unit.

- For vacant units within the portfolio, most programs calculate income at 75-90% of market rent.

- For portfolios containing short-term rentals, appraisers may reference AirDNA data or comparable STR properties to justify income.

Once appraisals for all properties are complete, the closing process moves to the title company. OfferMarket’s integrated platform connects directly with title companies across the country, giving everyone involved real-time access to closing documents, wire instructions, and settlement statements for the entire portfolio.

Step 5: Portfolio DSCR Calculation by Underwriting

Once the appraisals are complete, our underwriting team gets to work calculating the portfolio's DSCR to see if it meets program guidelines. This is the moment of truth—where the portfolio either qualifies or needs some adjustments.

Here's How We Calculate It:

Determine Total Qualifying Rent: We aggregate the rental income for all properties in the portfolio, using the lower of the actual lease or Form 1007 market rent for each individual unit.

Calculate Total Monthly PITIA: We calculate the global payment by adding up the new blanket loan's total principal and interest, plus the combined property taxes, insurance, and HOA dues for all properties in the portfolio.

Compute Blended DSCR Ratio: We divide the portfolio's total gross monthly rent by the global monthly PITIA

Check Individual Property Performance: We verify the global ratio meets minimum portfolio requirements (typically 1.05x - 1.20x) and check the "pro-rata" DSCR of each individual property to ensure no single underperforming asset triggers leverage penalties.

Let's Walk Through an Example (4-Property Portfolio):

- Total Portfolio Value: $1,000,000

- Down Payment (25%): $250,000

- Total Loan Amount: $750,000

- Interest Rate: 7.5%

- Monthly P&I (Blanket Loan): $5,244

- Combined Property Taxes: $1,000/month

- Combined Insurance: $400/month

- Combined HOA: $0

- Total PITIA: $6,644

- Combined Qualifying Rent: $8,000

- Blended DSCR: $8,000 ÷ $6,644 = 1.20x

Good news for this portfolio—it qualifies with room to spare. That 1.20x aggregate ratio clears most blanket program minimums and signals solid global cash flow.

OfferMarket Advantage: Want to run these numbers yourself before applying? Our DSCR loan calculator lets you play with variables like down payment amount, estimated rent, and property taxes to see exactly how different scenarios affect your qualification.

Step 6: Landlord Insurance

While underwriting reviews the DSCR calculation, we're also moving forward on insurance and title work. Both need to be buttoned up before closing.

Insurance Requirements:

- *Hazard Insurance* Standard property coverage for fire, wind, and other perils

- Flood Insurance: Required if your property sits in a FEMA flood zone

- Landlord/Dwelling Policy: Specific coverage designed for non-owner-occupied rentals

- Umbrella Policy: Often a smart move for extra liability protection

OfferMarket Advantage: Our integrated insurance services let you secure competitive landlord insurance quotes right through our platform—no need to shop around. This eliminates the need to shop separately and ensures your coverage meets lender requirements from day one. Our relationships with title companies also help keep the title process moving smoothly, cutting down on unnecessary delays.

Step 7: Clear to Close and Loan Document Signing

Once underwriting gives the thumbs up on your DSCR calculation, insurance is in place, and title comes back clear, your loan gets "clear to close" status. Now it's time to sign those final loan documents.

Final Steps:

- Final Closing Disclosure: Your chance to review final loan terms, closing costs, and cash to close

- Wire Instructions: Confirmation of where to send your down payment and closing cost funds

- Signing Appointment: Sit down with a notary or closing attorney to sign your loan documents

- LLC Signature: You'll sign in the name of your LLC, not your personal name

- Funding: The lender wires loan proceeds to the title company

- Recording: Deed and mortgage get recorded with the county

Typical Timeline: Most mortgage closings happen 21-30 days after application, though DSCR loans can sometimes wrap up faster since there's less paperwork involved.

OfferMarket Advantage: Our efficient process and connections with multiple lenders mean we can often get DSCR loans closed in just 14-21 days. We keep you in the loop at every step, so you always know where things stand and what's needed next. Our team handles coordination between all parties—appraiser, insurance provider, title company, and lender—so nothing slips through the cracks.

Conclusion: Your Partner in Scaling and Success

The journey from a novice real estate investor to a seasoned professional is marked by a shift in strategy—from managing individual assets to commanding a cohesive, high-performing portfolio. The portfolio DSCR loan is the financial tool that facilitates this evolution. It is an instrument designed not just for financing, but for strategic growth.

By consolidating your properties under a single, efficient loan, you unlock transformative benefits. You drastically simplify your administrative workload, achieve significant savings on financing costs, and accelerate your ability to acquire new properties. The power of a blended DSCR provides stability, while features like the partial release clause offer the flexibility to actively manage your assets. This is how sophisticated investors build and scale their real estate empires.

At OfferMarket, we are more than just a lender; we are specialists dedicated to providing the financial infrastructure for your success. Our technology-driven platform, deep expertise in portfolio lending, and commitment to competitive, transparent terms are all designed to save you money and time. We understand the unique needs of portfolio owners and have built our entire process around delivering a seamless, superior experience.

Ready to unlock the next level of your real estate investing journey? Stop juggling multiple loans and start managing your portfolio with the power and efficiency it deserves.

OfferMarket Loans

Check your rate

60 seconds · no credit pull