*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Loans For Real Estate Investors: Financing Options Guide

Selecting the right financing is the cornerstone of a successful real estate investment. The loan you choose impacts everything from your cash flow and potential return on investment to your ability to scale your portfolio. For investors, financing options extend far beyond conventional mortgages, with specialized products designed for specific strategies like long-term rentals, short-term flips, and new construction. Understanding the core differences in their purpose, terms, and qualification criteria is the first step toward securing the optimal loan for your project.

Loans for Real Estate Investors

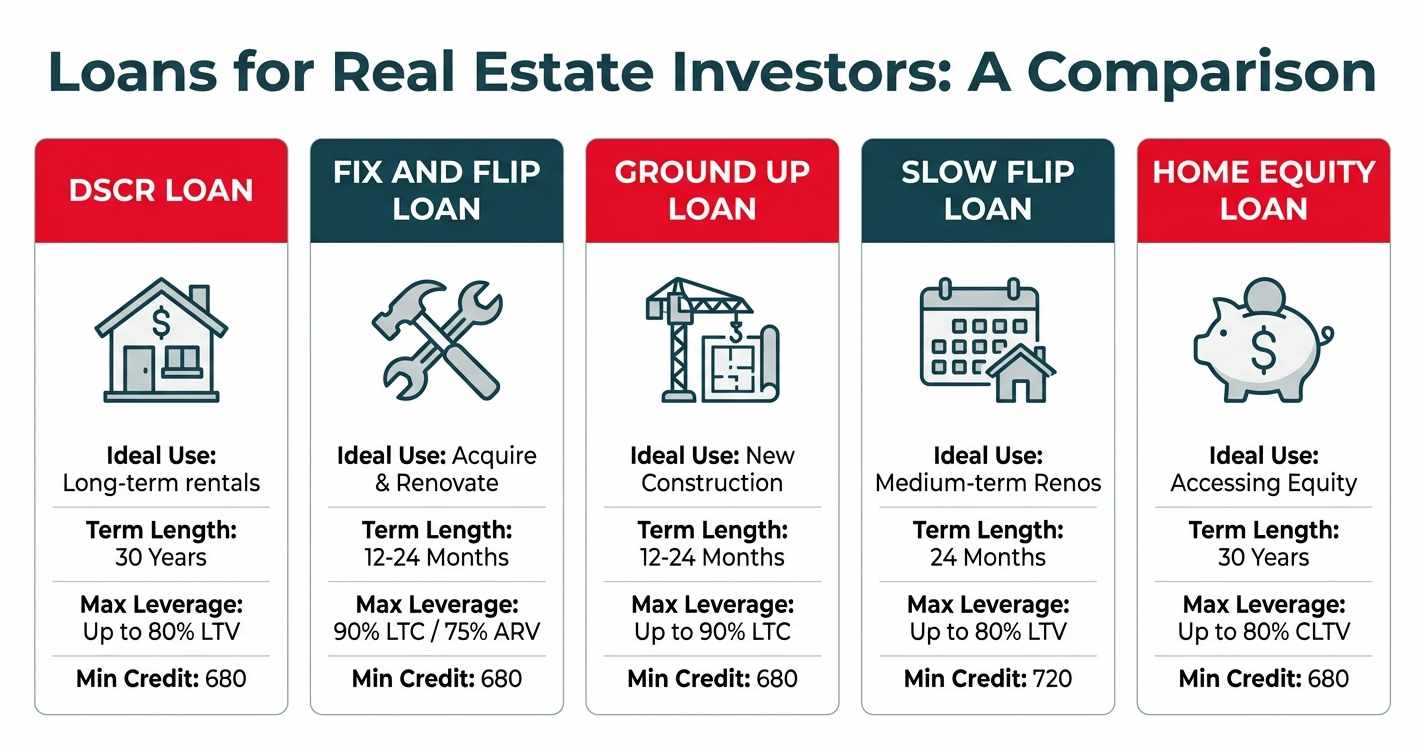

Below is a comprehensive comparison of the most common loans for real estate investors, highlighting their key features to help you quickly identify which products align with your goals.

| Loan Type | Ideal Use Case | Typical Term Length | Max Leverage (LTV/LTC) | Min Credit Score |

|---|---|---|---|---|

| DSCR Loan | Long-term (30-year) financing for stabilized, cash-flowing rental properties. | 30 Years | Up to 80% LTV | 680 |

| Fix and Flip Loan | Short-term financing to acquire and renovate a property for quick resale. | 12-24 Months | Up to 90% LTC / 75% ARV | 680 |

| Ground Up Construction | Financing the construction of a new residential property from the ground up. | 12-24 Months | Up to 90% LTC | 680 |

| Slow Flip Loan | Medium-term financing for renovations on properties that may take longer to sell. | 24 Months | Up to 80% LTV | 720 |

| Home Equity Loan | Accessing equity in an existing rental property as a second lien mortgage. | 30 Years | Up to 80% CLTV | 680 |

DSCR Long-Term Rental Property Loans

A DSCR loan is a powerful financing tool designed specifically for real estate investors purchasing or refinancing long-term rental properties. Unlike conventional mortgages that heavily scrutinize a borrower's personal income and debt-to-income (DTI) ratio, a DSCR loan qualifies the property itself. The lender's primary focus is on the property's ability to generate enough rental income to cover its mortgage expenses. This makes it an ideal solution for self-employed investors or those with multiple properties, as it streamlines the application process by removing the need for personal tax returns and W-2s.

What is a DSCR Loan?

DSCR stands for Debt Service Coverage Ratio. It's a simple calculation lenders use to determine if a property's cash flow is sufficient to cover its debt obligations. This single metric is the heart of the DSCR loan underwriting process. If the property's income can "service" the debt, the loan is likely to be approved, provided other criteria like credit score and LTV are met. This asset-based lending approach allows investors to scale their portfolios based on the performance of their investments, not the limitations of their personal income documentation.

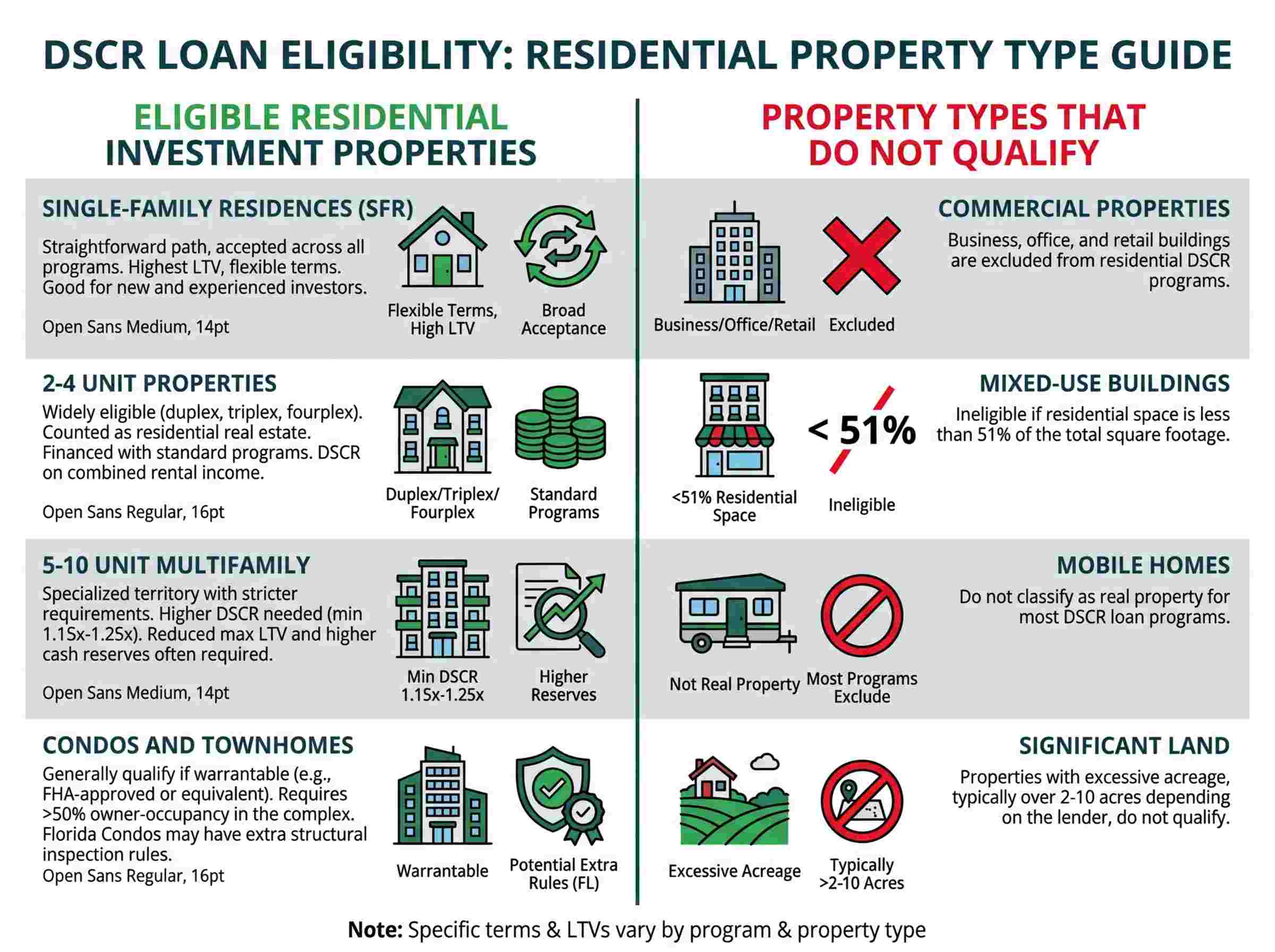

Ideal Investor Profile and Property Type

The ideal candidate for a DSCR loan is a real estate investor—new or experienced—who wants to acquire a "rent-ready" or stabilized rental property. This includes:

Portfolio Builders: Investors looking to acquire multiple properties without having their personal DTI ratio affect their borrowing capacity.

Self-Employed Investors: Entrepreneurs, self employed, or business owners whose income may be complex to document through traditional means.

Investors in High-Cost Areas: In markets where property prices are high, DSCR loans provide a pathway to financing that isn't capped by personal salary.

The property itself should be in good condition and capable of generating immediate rental income. This includes single-family homes (SFRs), 2-4 unit multi-family properties, townhomes, and condos. The key is that the property can be leased quickly to a long-term tenant, establishing the cash flow needed for the DSCR calculation.

How DSCR is Calculated: Gross Monthly Rent / PITI

The formula for DSCR is straightforward:

DSCR = Gross Monthly Rent / PITIA

Where:

Gross Monthly Rent is the total rental income the property generates each month. For a new purchase, this is typically determined by the appraiser's market rent analysis. For a refinance, it's based on the current lease agreement.

PITIA stands for Principal, Interest, Taxes, Insurance and HOA fees. It represents the total monthly mortgage payment.

Example Calculation:

- Gross Monthly Rent: $2,500

- Monthly Principal & Interest: $1,600

- Monthly Property Taxes: $300

- Monthly Homeowner's Insurance: $100

- HOA Fee: $0

- Total PITIA = $2,000

DSCR = $2,500 / $2,000 = 1.25

Most lenders, including OfferMarket, look for a DSCR of 1.20 or higher. A ratio of 1.0 means the income exactly covers the expenses (a "break-even" scenario). A ratio above 1.0 indicates positive cash flow. Some programs may allow for a DSCR as low as 1.0, but this often comes with stricter requirements, such as a larger down payment or higher credit score.

Key Qualification Metrics

While DSCR is the main metric, lenders still consider other factors to assess risk:

Credit Score: A minimum credit score of 680 is typically required. However, a higher score (720+) will unlock the best interest rates and most favorable terms, such as higher LTVs.

Down Payment (LTV): The maximum Loan-to-Value (LTV) is generally 80%, meaning a minimum down payment of 20% is required for a purchase. For a cash-out refinance, the max LTV is often lower, around 75%. A larger down payment reduces the lender's risk and can lead to better terms.

Cash Reserves: Lenders want to see that you have sufficient liquidity to cover several months of PITIA payments in case of a vacancy or unexpected repairs. The standard requirement is 3-6 months of PITIA held in a verifiable account.

The OfferMarket Advantage for DSCR Loans

At OfferMarket, we specialize in financing for real estate investors and have streamlined the DSCR loan process. Our advantages include:

Competitive Rates: We leverage technology and a vast network of capital partners to offer some of the most competitive rates in the industry.

Flexible Underwriting: We understand the investor mindset. Our underwriting focuses on the property's performance, allowing for a common-sense approach to lending.

Speed and Efficiency: Our digital platform allows you to get an instant DSCR loan quote online, upload documents electronically, and close faster than traditional banks.

No Personal Income Verification: True to the nature of DSCR loans, we don't require personal tax returns or W-2s, making the process faster and less intrusive for investors.

Fix and Flip Short-Term Renovation Bridge Loans

For real estate investors whose strategy is to buy, renovate, and quickly sell a property for profit, a Fix and Flip loan is the essential financing tool. These are short-term, interest-only bridge loans designed to cover the acquisition and renovation costs of a project. Unlike long-term mortgages, the focus is not on rental income but on the property's potential value after improvements—the After Repair Value (ARV). This allows investors to leverage the future value of a property to finance its transformation.

How Fix and Flip Loans Work for Rapid Resale

Fix and Flip loans provide the capital needed to both purchase a distressed property and fund the necessary renovations. The loan is structured to be paid back in a short period, typically 12 to 24 months, which aligns with the typical project timeline for a flip.

The funding is often disbursed in two parts:

- Acquisition Funds: A portion of the loan is used to purchase the property at closing.

- Renovation Funds: The money allocated for repairs is held in an escrow account by the lender. The investor funds repairs out-of-pocket and then submits draw requests to the lender for reimbursement as work is completed and inspected.

This structure protects both the lender and the borrower, ensuring that the renovation funds are used as intended to increase the property's value.

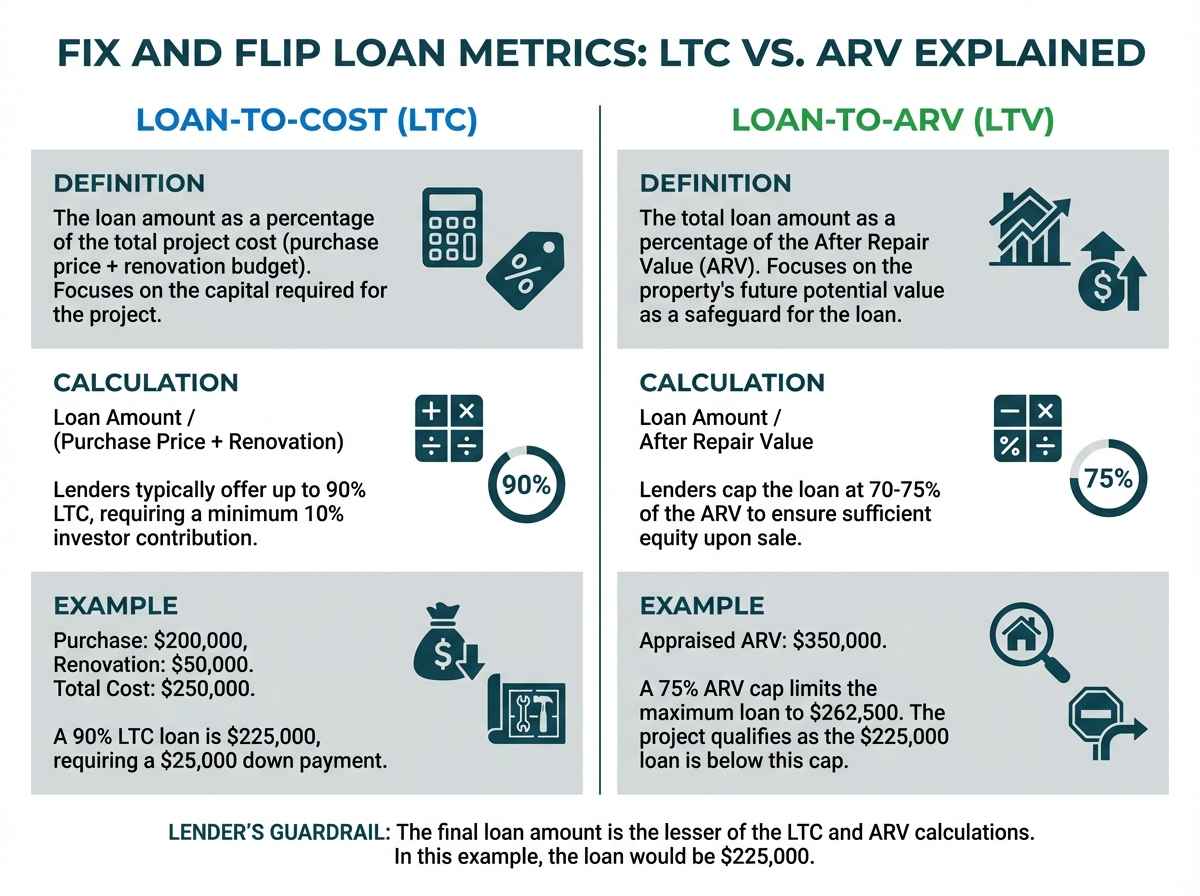

Understanding Leverage: Loan-to-Cost and Loan-to-ARV

Leverage is critical in the fix and flip business, as it allows investors to do more projects with less of their own capital. Two key metrics define the leverage on these loans:

Loan-to-Cost (LTC): This is the loan amount as a percentage of the total project cost (purchase price + renovation budget). Lenders typically offer up to 90% LTC, meaning the investor needs to contribute at least 10% of the total costs as a down payment.

- Example: Purchase Price: $200,000; Renovation Budget: $50,000. Total Cost: $250,000. A 90% LTC loan would be $225,000, requiring a $25,000 down payment from the investor.

Loan-to-ARV (LTV): This is the total loan amount as a percentage of the After Repair Value. Lenders cap the loan amount at a certain percentage of the ARV, typically 70-75%, to ensure there is enough equity in the project to cover costs and generate a profit upon sale. The ARV is determined by an independent appraiser who assesses the property and the investor's scope of work.

- Example: Using the project above, if the appraiser determines the ARV is $350,000, a 75% ARV cap would limit the total loan amount to $262,500. Since the 90% LTC calculation resulted in a $225,000 loan, the project qualifies as it is below the ARV cap.

Lenders will fund the lesser of the two calculations (LTC vs. ARV), which creates a crucial guardrail for the investment.

The Importance of Experience and Track Record

While some lenders offer fix and flip loans to first-time investors, having a proven track record is a significant advantage. Lenders view experienced flippers as lower risk. An investor who can show a portfolio of successfully completed and sold projects will typically qualify for:

- Higher Leverage: More experienced investors may be offered 90% LTC, while a first-timer might be capped at 80-85%.

- Lower Interest Rates and Fees: A strong track record demonstrates competence and reduces the lender's perceived risk, which is rewarded with better pricing.

- Larger Loan Amounts: Lenders are more comfortable extending larger loans to investors who have managed projects of a similar scale before.

For new investors, it's crucial to present a well-researched project, including a detailed scope of work, a realistic budget, and comparable sales (comps) that support the projected ARV. Partnering with an experienced contractor can also strengthen an application. For more information, you can explore resources on how to build a real estate portfolio.

Typical Loan Structure

Fix and Flip loans have a unique structure tailored to the short-term nature of the investment:

Interest-Only Payments: During the loan term, the borrower only pays interest on the outstanding balance. This keeps monthly payments low, preserving cash flow for the renovation. The full principal balance is due at the end of the term.

Short-Term: The loan term is typically 12 months, with options to extend for an additional 6-12 months if needed (often for a fee).

No Prepayment Penalty: These loans are designed to be paid off early. Once the property is renovated and sold, the investor uses the proceeds to pay off the loan balance without incurring any penalty, which is a critical feature for a flipping strategy.

Why OfferMarket is a Top Choice for Flippers

OfferMarket is built by investors, for investors. We understand the speed and flexibility required to succeed in the competitive flipping market.

Fast Funding: We can close loans in a fraction of the time of traditional lenders, ensuring you don't lose a deal waiting for financing.

High Leverage: We offer competitive leverage, up to 90% of the purchase and renovation costs, allowing you to keep more of your capital free for the next opportunity.

Transparent Process: Get an instant fix and flip loan quote online. Our platform provides a clear, step-by-step process from application to funding, with a dedicated team to support you.

Experience-Focused: We value your track record and reward experienced investors with our best terms, but we also have programs designed to help newer investors get started and build their portfolios.

Ground Up Construction Loans

For investors and developers aiming to build a new residential property from scratch, a Ground Up Construction loan provides the necessary capital. This type of financing covers the costs associated with the entire construction process, from site work and foundations to framing and finishes. Unlike other investor loans, construction loans are more complex due to the inherent risks of building a new structure. As a result, they come with stricter qualification requirements, particularly regarding the borrower's experience.

Financing New Residential Builds for Rent or Sale

A ground up construction loan can be used to build various types of residential properties, including:

- Single-family homes

- 2-4 unit multi-family properties

- Townhomes

The investor's exit strategy determines the loan's structure. If the plan is to sell the property upon completion (a "spec build"), the loan is a short-term bridge loan, similar to a fix and flip loan, that is paid off with the proceeds from the sale. If the plan is to hold the property as a long-term rental, the construction loan is a short-term solution that will need to be refinanced into a permanent, long-term mortgage (like a DSCR loan) once the project is complete and a certificate of occupancy is issued.

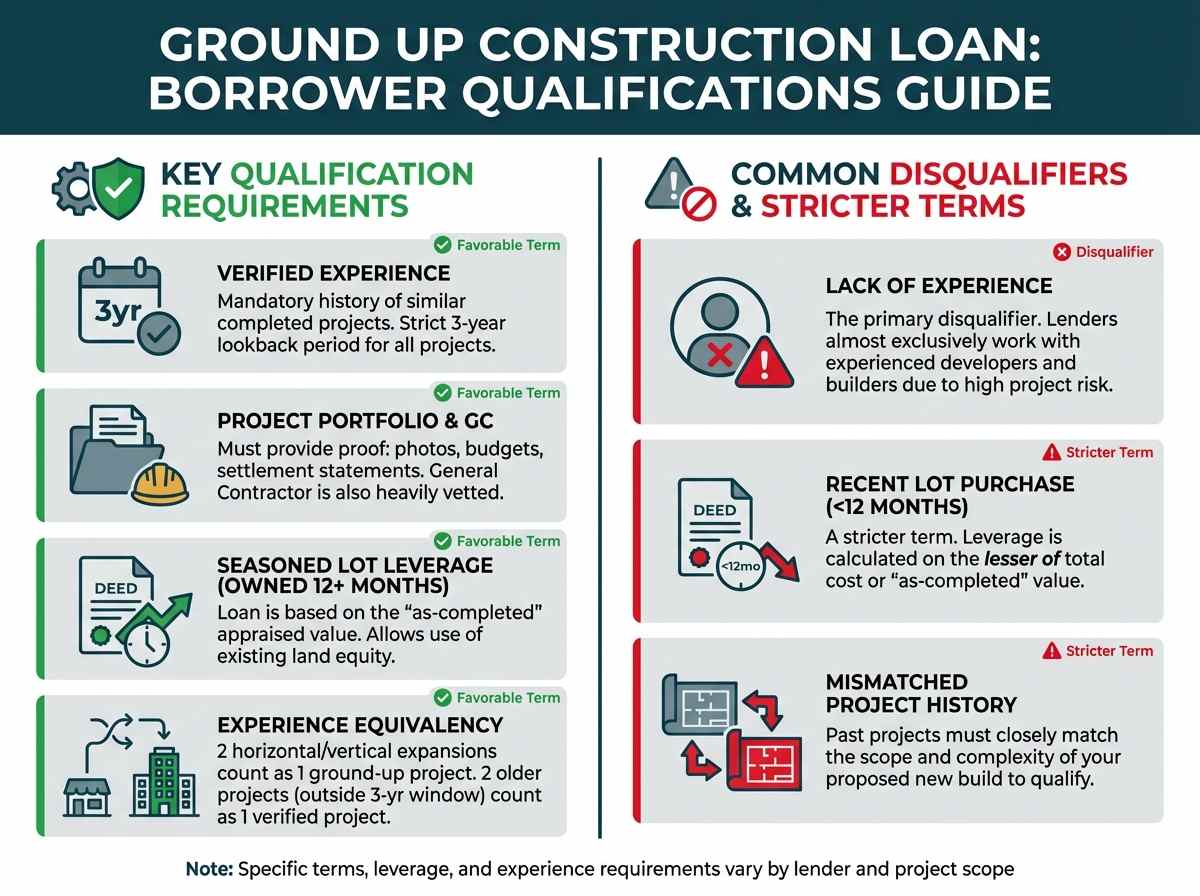

Strict Experience Requirements for Developers

Lenders consider ground up construction to be one of the riskiest forms of real estate lending. A project can face delays, cost overruns, and issues with contractors. To mitigate this risk, lenders almost exclusively work with experienced developers and builders.

The typical minimum experience requirement is:

- Verified history of similar completed projects (sold or rented) within a strict 3-year lookback period.

The borrower must be able to provide a portfolio of past projects, including photos, budgets, and settlement statements, to prove their ability to manage a construction project from start to finish successfully. Lenders also heavily vet the general contractor (GC) chosen for the project, reviewing their license, insurance, and track record.

Past projects must closely match the scope and complexity of your proposed build. If you lack direct ground-up experience, every two completed horizontal or vertical expansion projects will count as one ground-up project. Projects completed outside the 3-year window are heavily discounted, with every two older projects counting as only one verified project.

Loan Amount Restrictions Based on Lot Ownership Duration

The amount of leverage a lender will offer on a construction loan often depends on how long the borrower has owned the lot.

Recent Purchase (Owned Less Than 12 Months): Lenders apply a strict 12-month cutoff rather than a 6-12 month range. If the lot was acquired less than 12 months prior to the application date, underwriters will calculate your leverage using the lesser of the total acquisition costs (the lot's original purchase price plus construction costs) or the new "as-completed" appraised value. Furthermore, highly experienced investors can actually qualify for up to 90% Loan-to-Total-Cost (LTFC), rather than being capped at 85%.

Seasoned Ownership (Owned 12 Months or More): If you have held title to the lot for 12 months or longer, the loan is based entirely on the "as-completed" appraised value, ignoring the original purchase price. Your statement is entirely correct that owning the lot free and clear allows you to use your existing land equity towards the transaction, significantly reducing your required cash-to-close.

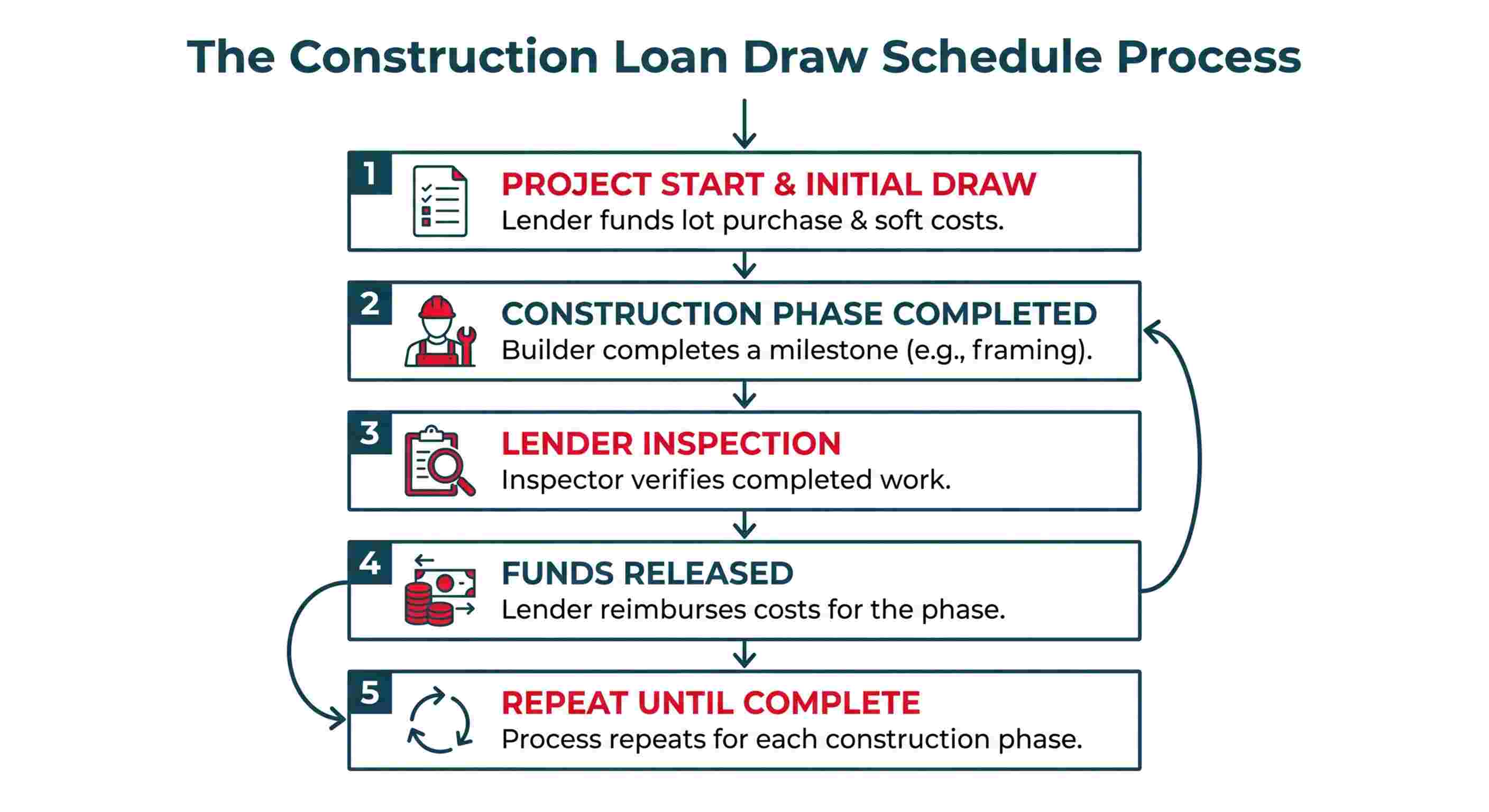

Draw Schedules and Construction Budget Management

Construction loan funds are not disbursed as a lump sum at closing. Instead, they are paid out in stages, known as draws, as the project reaches specific milestones.

- Initial Draw: The first draw at closing typically covers the lot acquisition (if applicable) and initial soft costs.

- Construction Draws: The investor or their builder completes a phase of construction (e.g., foundation, framing, rough-in plumbing). They then submit a draw request to the lender.

- Inspection: The lender sends an inspector to the site to verify that the work has been completed according to the plans and budget.

- Reimbursement: Once the inspection is approved, the lender releases the funds for that phase of work.

This process repeats until the project is complete. The investor must have enough liquidity to front the costs for each stage before being reimbursed by the lender. A detailed construction budget (often in a format like the AIA G702/703) is required upfront and is meticulously tracked throughout the loan term.

OfferMarket’s Streamlined Process for New Construction

Navigating a construction loan can be daunting, but OfferMarket simplifies the process for experienced developers.

- Expert Guidance: Our loan officers have deep experience in construction financing and can guide you through the complexities of budgeting, draw schedules, and underwriting.

- Competitive Terms: We offer competitive leverage (up to 90% LTC) and pricing to ensure your project is profitable.

- Efficient Draw Processing: Our streamlined draw request and inspection process ensures that you get your reimbursements quickly, keeping your project on schedule and your contractors paid on time.

- One-Stop Shop: We offer both the initial construction loan and the permanent take-out financing (like a DSCR loan) once the project is complete, providing a seamless transition from construction to long-term hold.

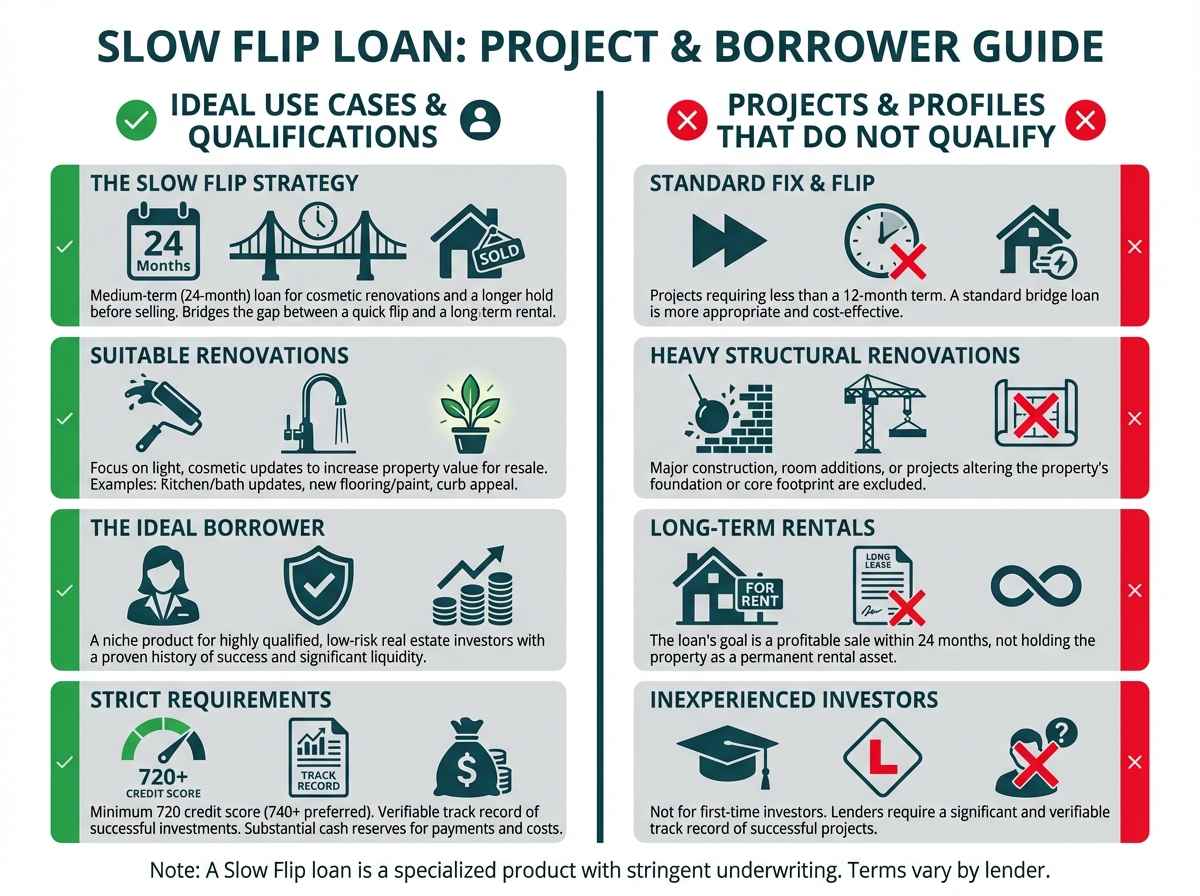

Slow Flip Loans

The Slow Flip loan is a niche financing product designed for a very specific type of real estate investor and project. It bridges the gap between a fast-paced fix and flip and a long-term rental. This medium-term loan, typically with a 24-month term, is ideal for investors who are undertaking minor renovations on a property they intend to sell, but who anticipate a longer holding period than a standard flip. This could be due to market conditions, the scale of the cosmetic updates, or a desire to season the property before sale.

Flexible Medium-Term Financing for Smaller Projects

A Slow Flip loan is best suited for projects that involve light, cosmetic renovations rather than heavy structural changes.

Think of projects like:

- Updating a kitchen with new countertops and appliances.

- Replacing flooring and painting.

- Modernizing bathrooms.

- Improving curb appeal with landscaping.

The goal is to increase the property's value for a future sale without the time pressure of a 12-month bridge loan. The 24-month term provides a comfortable buffer to complete the work, stage the property, and wait for the optimal time to list it on the market.

Stringent Qualification Criteria

Because of its unique structure and longer term, the Slow Flip loan comes with some of the most stringent qualification requirements among investor loan products. Lenders are looking for highly qualified, low-risk borrowers.

- High Credit Score: A minimum credit score of 720 is typically required, with the best terms reserved for borrowers with scores of 740 or higher.

- Proven Experience: This is not a product for first-time investors. Lenders require a significant and verifiable track record of successful real estate investments, often similar in scope to the proposed project.

- Substantial Liquidity: Borrowers must demonstrate significant cash reserves. This not only covers the down payment and closing costs but also proves they can comfortably handle the mortgage payments for the 24-month term and any unexpected project costs.

Loan Amount Caps and Out-of-Pocket Closing Costs

Slow Flip loans generally have more conservative leverage and loan amount parameters compared to other products.

- Loan Amount Caps: The maximum loan amount is strictly capped at $50,000, focusing the product on small-balance projects.

- Leverage: The maximum allowable leverage typically allows you to borrow up to 100% of the purchase price.

- Out-of-Pocket Costs: A Slow Flip loan does not finance renovation costs, so 100% of repairs must be funded out-of-pocket. However, you can roll closing costs into the loan (exceeding 100% of the purchase price) if your "as-is" LTV is less than 80% and you meet strict high-tier criteria, such as an 800+ FICO score and at least $50,000 in verified liquidity.

Use Cases for the Slow Flip Strategy

An investor might choose a Slow Flip loan in several scenarios:

Market Timing: An investor believes the real estate market will be stronger in 18-24 months and wants to buy a property now, make light improvements, and wait for appreciation before selling.

"Wholetailing": An investor buys a property that is in relatively good condition but could use some cosmetic updates to appeal to a retail buyer. They perform the updates over time without the pressure of a short-term loan.

Personal Project Management: An investor who manages their own renovations on the side may need a longer timeline to complete the work around their primary professional obligations.

Understanding This Niche Product at OfferMarket

The Slow Flip loan is a specialized tool in our comprehensive suite of financing solutions. At OfferMarket, we recognize that not every investment fits neatly into a "quick flip" or "long-term hold" box. For the highly qualified investor with the right project, our Slow Flip loan offers the flexibility needed to execute a medium-term strategy. Because of the strict requirements, we encourage investors to get an instant quote to see if this product is the right fit for their specific circumstances and qualifications.

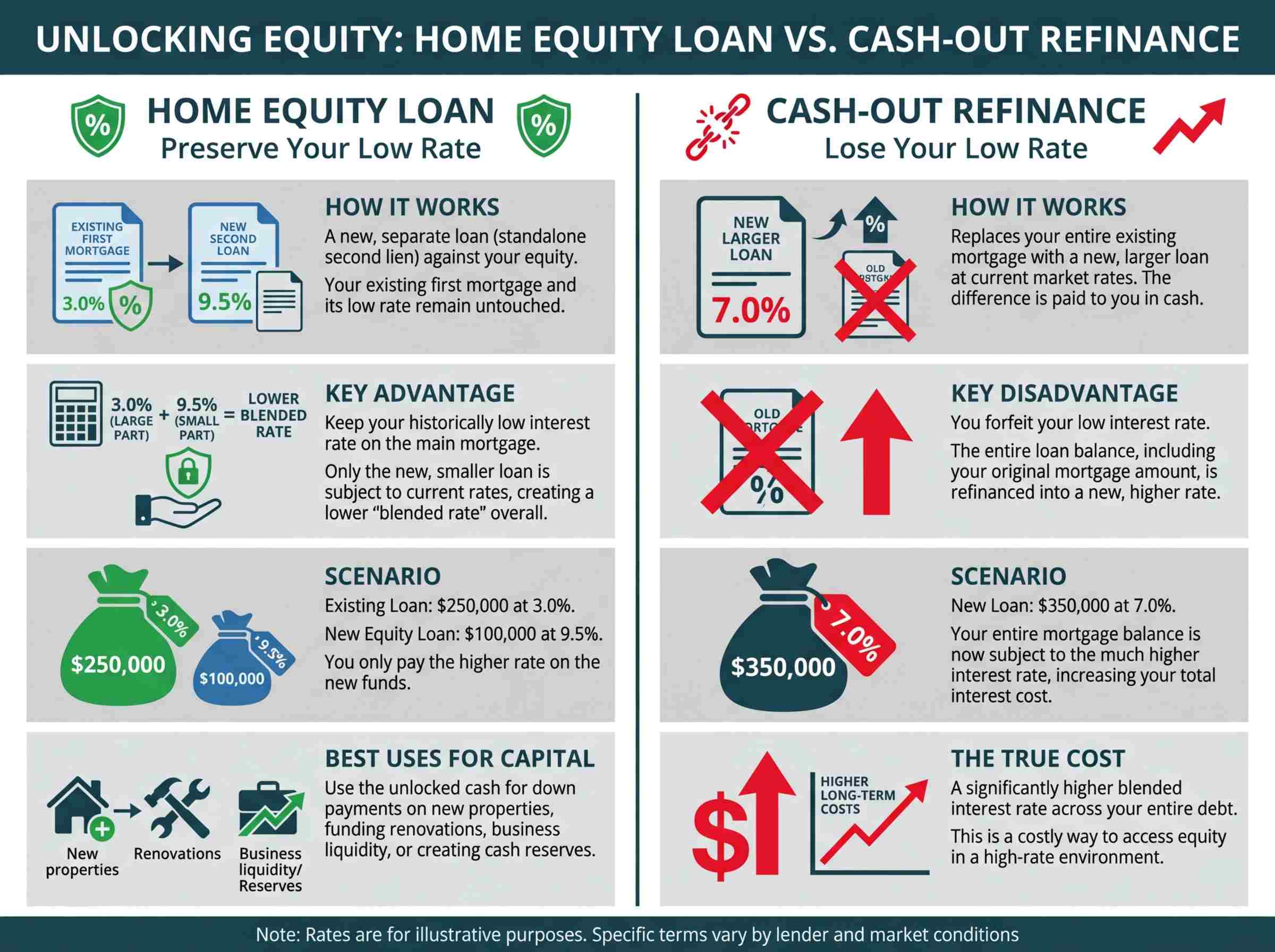

Home Equity Loan or Standalone Second Liens

For investors who already own rental properties with significant equity, a Home Equity Loan, also known as a Standalone Second Lien, is a strategic tool for unlocking capital. This type of loan allows you to borrow against the equity in your investment property without touching the existing first mortgage. This is particularly valuable for investors who secured a historically low interest rate on their primary loan and do not want to lose it by doing a cash-out refinance in a higher-rate environment.

Accessing Trapped Equity in an Existing Rental Property

Equity is the difference between your property's current market value and the outstanding balance on your mortgage. As you pay down your mortgage and/or the property appreciates in value, your equity grows. A Home Equity Loan places a second, subordinate lien on the property, allowing you to convert a portion of this equity into cash.

This cash can be used for a variety of investment purposes, such as:

- A down payment on another rental property.

- Funding renovations on other properties in your portfolio.

- Providing liquidity for business opportunities.

- Creating a cash reserve fund.

Preserving a Low Interest Rate on Your First Mortgage

The primary advantage of a standalone second lien over a cash-out refinance is the preservation of your existing first mortgage.

Scenario:

You own a rental property valued at $500,000.

You have an existing first mortgage of $250,000 with a 3.0% interest rate.

You want to access $100,000 in equity.

Option 1: Cash-Out Refinance. You would refinance the entire mortgage into a new $350,000 loan. If current rates are 7.0%, your entire loan balance is now at that much higher rate.

Option 2: Home Equity Loan. You keep your $250,000 first mortgage at 3.0%. You take out a new, separate $100,000 Home Equity Loan. While the rate on the second loan might be higher (e.g., 9-10%), you are only paying that rate on the $100,000 you borrowed, not the full $350,000. This "blended rate" is often significantly lower than the rate on a new cash-out refinance.

This strategy is a cornerstone of savvy portfolio management.

Combined Loan-to-Value (CLTV) Caps

When underwriting a second lien, lenders look at the Combined Loan-to-Value (CLTV). This is calculated by adding the balance of the first mortgage and the new proposed second mortgage, and dividing that by the property's value.

CLTV = (First Mortgage Balance + New Second Mortgage Amount) / Property Value

Example:

- Property Value: $500,000

- First Mortgage Balance: $250,000

- Desired Home Equity Loan: $100,000

- Total Loan Amount = $350,000

CLTV = $350,000 / $500,000 = 70%

Lenders typically cap the CLTV on investment properties at 75-80%. This ensures a protective equity cushion of at least 20-25% remains in the property.

Property Requirements

To qualify for a home equity loan on an investment property, the property must be stabilized and generating income. Lenders will require:

- A Long-Term Lease in Place: The property must be occupied by a tenant with an executed lease agreement, typically with at least 6 months remaining on the term. This proves the property is a viable, income-producing asset.

- Property Type: The loan is generally available for single-family residences (SFRs), 2-4 unit properties, condos, and townhomes.

The Benefit of No Cash Reserve Requirements with OfferMarket

One of the standout features of OfferMarket's Home Equity Loan program is the lack of a cash reserve requirement. While most lenders require investors to have 3-6 months of PITIA in reserves for each property, our program for standalone second liens does not. This allows you to deploy more of your capital towards your next investment rather than having it sit idle in a bank account. This flexibility, combined with competitive terms and a streamlined process, makes our Home Equity Loan a powerful tool for scaling your real estate portfolio efficiently.

Unlock Your Investment Quote

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →Matching Your Strategy to the Right Investor Loan

With a clear understanding of the different loan types available, the next step is to match your specific investment plan to the most suitable financing. Every real estate strategy has a unique timeline, capital requirement, and risk profile, and there is a loan product designed to align with each one. Choosing correctly from the outset can be the difference between a profitable venture and a struggling project.

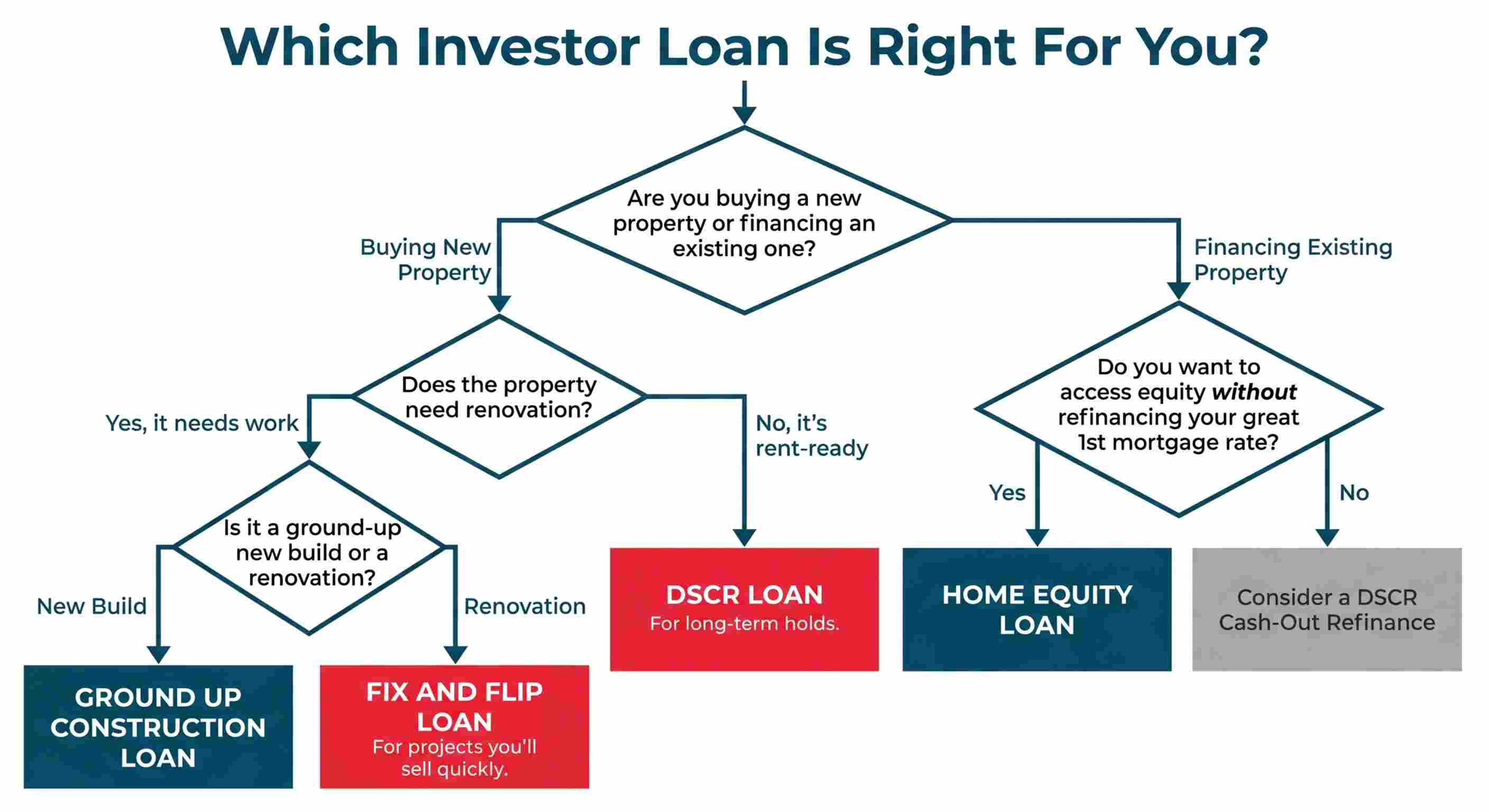

Buy and Hold Stabilized Rental: DSCR Long-Term Rental Loan

If your strategy is to acquire a rent-ready property and hold it for long-term cash flow and appreciation, the DSCR Loan is the perfect fit.

- Why it works: It qualifies the property on its own income, not your personal DTI. The 30-year fixed term provides stability and predictable payments, which is ideal for a buy-and-hold model. It allows you to build a portfolio of cash-flowing assets without the paperwork burden of conventional loans.

Renovate and Sell Quickly: Fix and Flip Short-Term Bridge Loan

If your business model is to buy distressed properties, add value through renovations, and sell for a profit within a year, the Fix and Flip Loan is your go-to tool.

- Why it works: It finances both the purchase and the renovation costs, maximizing your leverage. The interest-only structure keeps holding costs low during the project. The short-term nature and lack of prepayment penalties are designed specifically for a quick exit upon sale.

Build a New Property: Ground Up Construction Loan

For experienced developers building a new residential property from the ground up, whether to sell or to rent, the Ground Up Construction Loan is the only option.

- Why it works: This loan is structured to fund a project in stages, from lot acquisition to final completion. The draw schedule ensures funds are managed responsibly. It provides the significant capital required to take a project from a vacant lot to a completed, valuable asset.

Access Equity Without Refinancing: Home Equity Loan or Standalone Second Lien

If you are a current property owner with substantial equity and a great interest rate on your first mortgage, the Home Equity Loan is the most strategic way to tap into your capital.

- Why it works: It allows you to pull cash out of your property for other investments without sacrificing the low interest rate on your primary mortgage. It is a targeted way to access liquidity while keeping your existing, favorable financing in place.

Medium-Term Financing for Small Projects: Slow Flip Loan

For the highly qualified investor working on a cosmetic renovation with a longer timeline (up to 24 months), the Slow Flip Loan provides a unique solution.

- Why it works: It offers a longer term than a standard flip loan, providing flexibility for projects that don't fit a rapid timeline. It's designed for seasoned investors who want to time the market or manage a less intensive renovation over a longer period.

The OfferMarket Loan Application and Underwriting Process

We believe that securing financing for your real estate investments should be as streamlined and efficient as possible. Our technology-driven platform is designed to provide transparency and speed at every stage, from getting an instant quote to closing your loan. Here is a step-by-step overview of our process.

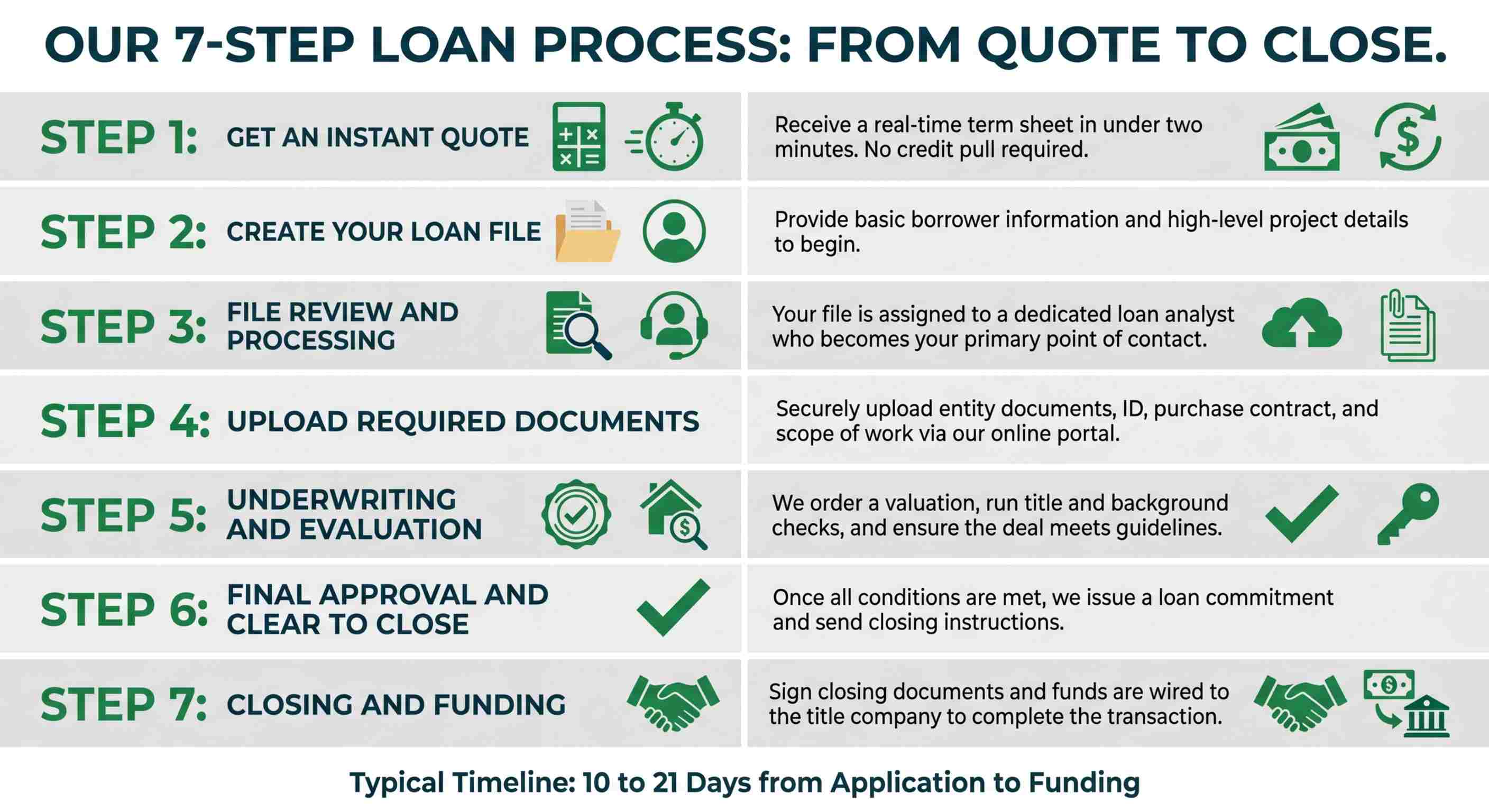

Step 1: Get an Instant Quote

Start by entering your property address and project details into our instant quote tool. In less than two minutes, you'll receive a real-time term sheet outlining your estimated loan amount, interest rate, leverage, and key terms—without a credit pull.

Step 2: Create Your Loan File

If the terms look good, proceed by creating your loan file. You'll provide basic information about yourself and your borrowing entity (typically an LLC or corporation), along with a few high-level details about the project.

Step 3: File Review and Processing

Once submitted, your file enters our processing queue and is assigned to a dedicated loan analyst. This person becomes your primary point of contact and helps guide you through the rest of the process.

Step 4: Upload Required Documents

Using our secure online portal, you’ll upload the required documents—typically including your entity formation documents, government ID, purchase contract, and renovation scope of work. Keeping these documents organized helps speed up approval.

Step 5: Underwriting and Property Evaluation

While documents are being uploaded, our team begins the underwriting process. This includes ordering a valuation (often a desktop appraisal to save time and cost) and running title and background checks. The underwriter reviews the deal to ensure it meets lending guidelines.

Step 6: Final Approval and Clear to Close

Once underwriting is complete and all conditions are satisfied, your loan receives final approval and a “clear to close.” We issue the loan commitment and send closing instructions and documents to the title company or closing attorney.

Step 7: Closing and Funding

You’ll sign the closing documents, and funds are wired to the title company to complete the transaction. From application to funding, the process typically takes 10 to 21 days, allowing investors to move quickly on opportunities.

Key Financial Metrics All Real Estate Investors Must Know

To speak the language of lending and make informed investment decisions, you need to be fluent in the key financial metrics that underpin every real estate deal. Understanding these concepts will help you analyze properties, communicate effectively with lenders, and maximize your returns.

Debt Service Coverage Ratio (DSCR)

As discussed earlier, DSCR is the lifeblood of long-term rental financing. It measures a property's ability to pay its own mortgage.

- Formula: DSCR = Gross Monthly Rent / Monthly PITIA

- Why it matters: A DSCR above 1.0 indicates positive cash flow. Most lenders require a DSCR of at least 1.20, meaning the property's income is 20% greater than its expenses, providing a healthy buffer.

Loan-to-Value (LTV) and Loan-to-Cost (LTC)

These two metrics measure leverage but are used in different contexts.

- *Loan-to-Value (LTV):* Used for stabilized properties. It's the loan amount as a percentage of the property's current appraised value.

- Formula: LTV = Loan Amount / Appraised Value

- Why it matters: It determines your down payment. An 80% LTV loan requires a 20% down payment.

- Loan-to-Cost (LTC): Used for renovation and construction projects. It's the loan amount as a percentage of the total project cost (purchase + repairs).

- Formula: LTC = Loan Amount / Invested Cost (Purchase price of the property + Estimated rehabilitation budget + Sunk capital)

- Why it matters: It determines how much of the total project a lender will finance. 90% LTC is common for experienced flippers.

After Repair Value (ARV)

ARV is a forward-looking valuation used for fix and flip projects. It is an appraiser's opinion of what a property will be worth after all proposed renovations are completed.

How it's determined: An appraiser analyzes your scope of work and compares your project to recent sales of similar, fully renovated properties in the area (known as "comps").

Why it matters: Lenders use ARV to set the maximum loan amount on a flip (e.g., "up to 75% of ARV"). It acts as a safety measure to ensure the project is viable and there will be enough value upon completion to repay the loan and generate a profit. Our ARV calculator can help you estimate this value.

Why Finance Your Next Investment with OfferMarket

Choosing a lending partner is as important as choosing the right property. At OfferMarket, we are more than just a lender; we are a strategic partner dedicated to helping you achieve your real estate investment goals.

Comprehensive Suite of Loan Products for Any Strategy

We offer a full spectrum of financing solutions under one roof. Whether you're a buy-and-hold investor needing a DSCR loan, a flipper in search of high-leverage bridge financing, or a developer planning a new build, we have a product tailored to your specific needs. This means you can grow and diversify your strategies without having to find a new lender for every deal.

Competitive Rates and Flexible Terms

Our technology-driven platform and diverse capital sources allow us to operate efficiently and pass those savings on to you. We provide highly competitive interest rates, origination fees, and flexible terms across all our loan programs. We empower you to structure financing that maximizes your profitability.

Fast, Streamlined Digital Application and Closing Process

Time is money in real estate. Our online application process is designed for speed and convenience. You can get an instant quote in minutes, upload documents securely from any device, and track your loan's progress in real-time. This efficiency means we can close loans in days, not weeks, so you can seize opportunities as they arise.

Dedicated Support for Investors of All Experience Levels

Whether you're closing your first deal or your hundredth, our team of experienced loan officers is here to support you. We provide expert guidance, answer your questions, and work with you to overcome challenges. We value relationships and are committed to being your long-term financing partner as you scale your portfolio.

Tools and Resources to Help You Succeed

We believe in empowering our clients with knowledge. Our website features a wealth of free resources, including investment property calculators, in-depth guides on real estate strategies, and market insights. We provide the tools you need to analyze deals, make informed decisions, and grow your business.

Get Your Instant Loan Quote

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →

OfferMarket Loans

Check your rate

60 seconds · no credit pull