*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

The 5 Best Loans For Rental Property Investors

Securing the right financing is the cornerstone of a successful real estate investment strategy. The type of loan you choose can directly impact your cash flow, scalability, and overall return on investment. For investors, the landscape of loans for rental property extends far beyond the conventional mortgages used for primary residences. Specialized products are designed to evaluate the property's income potential rather than just your personal financial picture.

The five most effective loans for rental property investors are the DSCR Loan, Fix and Flip Loan, Ground Up Construction Loan, Home Equity Loan (HELOAN), and the Slow Flip Loan. Each serves a distinct purpose, from acquiring a turnkey rental with no income verification to funding a complete new build. The most popular and versatile option for long-term hold investors is the Debt Service Coverage Ratio (DSCR) loan, which qualifies the loan based on the property's rental income covering the mortgage payment, making it ideal for scaling a portfolio.

Comparison Table of Rental Property Loans

To help you visualize which loan best fits your needs, here is a side-by-side comparison of the five main types of loans for rental properties.

| Loan Type | Typical LTV/LTC | Credit Score Range | Loan Term | Best For | Key Feature |

|---|---|---|---|---|---|

| DSCR Loan | Up to 80% LTV | 680+ | 30 Years | Long-term buy-and-hold investors scaling a portfolio. | Qualifies on property income, not personal DTI. |

| Fix and Flip Loan | Up to 90% LTV, 100% LTC | 680+ | 12-24 Months | Investors executing the BRRRR strategy. | Funds purchase and 100% of renovation costs. |

| Ground Up Loan | Up to 85% LTC | 680+ | 12-24 Months | Experienced developers building new rental units. | Funds are disbursed in draws based on progress. |

| Home Equity Loan | Up to 75% CLTV | 680+ | 30 Years | Accessing equity without refinancing a low-rate 1st mortgage. | DSCR-based qualification on a second lien. |

| Slow Flip Loan | Varies | 720+ | 5 Years | Experienced investors with small, extended projects. | Medium-term hold with a step-down prepay penalty. |

The 5 Best Loans For Rental Property Investors

Choosing the right loan is critical for maximizing your investment's potential. While a conventional mortgage is an option, it often comes with stringent personal income requirements that can limit your ability to scale. Specialized investor loans are designed to overcome this hurdle. Here are the top five financing options tailored for real estate investors.

DSCR Loan for cash-flow based qualification

The DSCR loan is a game-changer for investors. It qualifies you based on the rental property's ability to generate enough income to cover its mortgage debt, rather than on your personal debt-to-income ratio. This is the premier product for building a portfolio of long-term rentals.

Fix and Flip Loan for BRRRR strategy execution

A Fix and Flip Loan is a short-term, interest-only loan that funds the purchase and renovation of a property. For investors using the BRRRR (Buy, Renovate, Rent, Refinance, Repeat) method, this loan is the engine that powers the first two steps, providing the capital needed to acquire and improve the asset before placing a tenant and refinancing into a long-term DSCR loan.

Ground Up Construction Loan for building new rental units

For investors looking to build new rental properties from the ground up, a Ground Up Construction Loan provides the necessary financing. This loan covers project costs from land acquisition to vertical construction, disbursed in draws as you complete predefined milestones.

Home Equity Loan to leverage existing property equity

If you already own investment properties with significant equity, a Home Equity Loan allows you to tap into that value. This is a second-position lien that lets you pull cash out without disturbing a favorable first mortgage, providing funds for a down payment on a new property or for renovations.

Slow Flip Loan for smaller projects with extended timelines

The Slow Flip Loan is a niche product for experienced investors undertaking smaller renovations that may take longer than a typical hard money loan term. It offers a 5-year term, giving you ample time to complete the work and sell or refinance the property.

DSCR (Debt Service Coverage Ratio) Loan

The DSCR loan is arguably the most powerful tool for long-term rental property investors. Its entire structure is designed to facilitate portfolio growth by focusing on the asset's performance, not the borrower's personal balance sheet.

What It Is: A long-term loan qualified by property income, not personal DTI

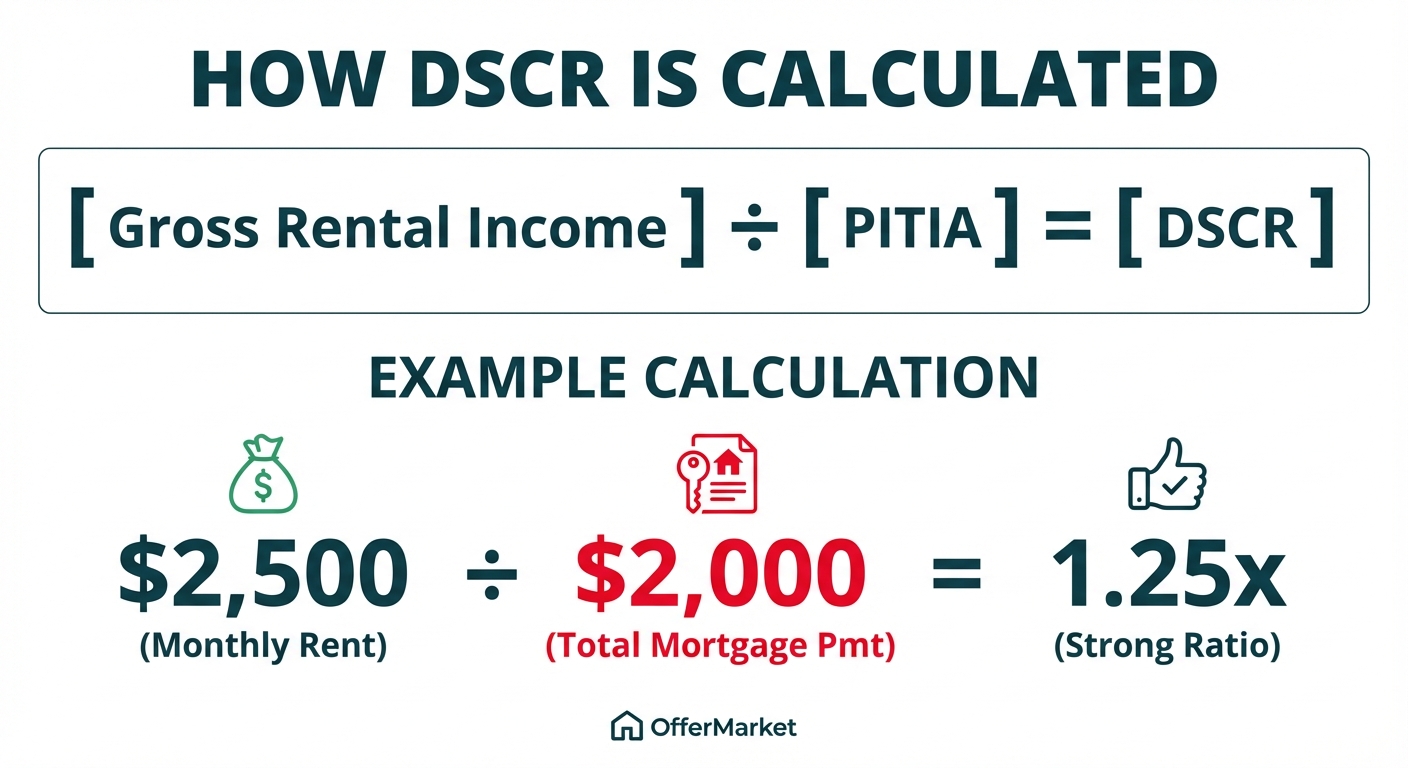

A DSCR loan is a type of non-qualified mortgage (Non-QM) where the lender primarily assesses the property's cash flow. The key metric is the Debt Service Coverage Ratio, which compares the property's gross rental income to its proposed monthly mortgage payment (including principal, interest, taxes, insurance, and association dues, or PITIA). If the rent covers the payment, the loan is likely to be approved, regardless of your personal DTI.

How It Works: Underwriting focuses on the ratio of gross rent to the mortgage payment (PITIA)

The DSCR calculation is simple:

DSCR = Gross Rental Income / PITIA

A DSCR of 1.0x means the rent exactly covers the mortgage payment. Most lenders, including OfferMarket, look for a DSCR of 1.25x or higher for the best terms, but programs are available for properties with a DSCR as low as 0.75x in some cases. For example, if a property rents for $2,500 per month and the total proposed PITIA is $2,000, the DSCR would be 1.25x ($2,500 / $2,000), which is a strong ratio.

Who It Is For: Investors scaling portfolios who want to avoid personal income verification

This loan is perfect for:

- Self-employed investors: No need for tax returns or W-2s.

- Investors with multiple properties: Avoid hitting the limit on the number of financed properties set by conventional lenders like Fannie Mae.

- Investors who want to close quickly: The streamlined documentation process leads to faster closings.

- Foreign nationals: Many DSCR programs are open to non-U.S. citizens.

Key Features: 30-year fixed, ARM, and Interest-Only (IO) options available

DSCR loans offer the same flexibility as traditional mortgages, allowing you to tailor the financing to your investment strategy.

- 30-Year Fixed: Provides stability and predictable payments, ideal for long-term buy-and-hold.

- Adjustable-Rate Mortgage (ARM): Often starts with a lower rate for a fixed period (e.g., 5, 7, or 10 years), which can improve initial cash flow.

- Interest-Only (IO): Requires you to pay only the interest for a set period (typically the first 10 years), which dramatically increases cash flow. This is an advanced strategy for maximizing returns in the short term.

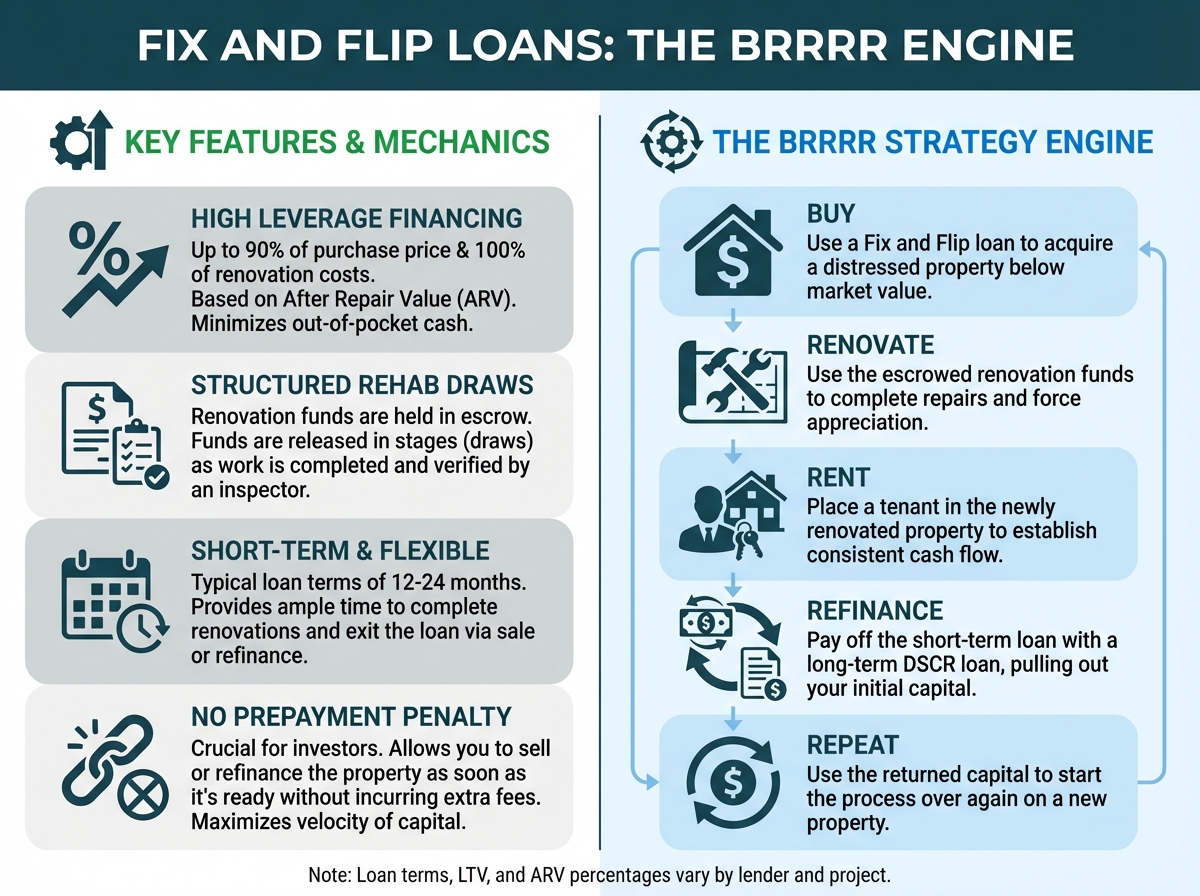

Fix and Flip Loan: The BRRRR Engine

The Fix and Flip loan is the quintessential tool for value-add investors. It's short-term financing designed specifically to cover the acquisition and renovation of a property you intend to improve and then either sell or refinance.

What It Is: Short-term bridge financing for acquiring and renovating properties

Also known as a bridge loan or hard money loan, this product provides the capital to buy a distressed property and fund the necessary repairs. Unlike a traditional mortgage, the loan amount is based on the property's After Repair Value (ARV), which is the estimated value of the property after all renovations are complete.

How It Works: Lenders finance purchase and rehab costs, with renovation funds in escrow

The process is straightforward. The lender approves a total loan amount that covers a percentage of the purchase price and 100% of the renovation budget.

- Closing: You receive the funds to purchase the property.

- Rehab Draws: The renovation funds are held in an escrow account. As you complete phases of the project (e.g., demolition, framing, plumbing), you submit a draw request. An inspector verifies the work, and the lender releases the funds for that portion of the project.

This structure protects both the borrower and the lender by ensuring the renovation funds are used as intended.

Who It Is For: Investors using the Buy, Renovate, Rent, Refinance, Repeat (BRRRR) strategy

This loan is the lifeblood of the BRRRR method, a popular strategy for rapidly building a rental portfolio.

- Buy: Use a Fix and Flip loan to purchase a property below market value.

- Renovate: Use the escrowed funds to force appreciation.

- Rent: Place a tenant in the newly renovated property to establish cash flow.

- Refinance: Pay off the short-term Fix and Flip loan with a long-term DSCR loan, often pulling out your initial capital and sometimes more.

- Repeat: Use the returned capital to start the process over on a new property.

Key Features: Up to 90% LTV and 100% LTC, typically 12-month terms, no prepayment penalty

- High Leverage: OfferMarket provides up to 90% of the purchase price and 100% of the renovation costs, not to exceed 75% of the ARV. This high leverage minimizes your out-of-pocket cash requirement.

- Short Term: Loan terms are typically 12-24 months, giving you enough time to complete the renovation and exit the loan.

- No Prepayment Penalty: This is a crucial feature. It allows you to refinance or sell the property as soon as it's ready without incurring extra fees, maximizing your velocity of capital.

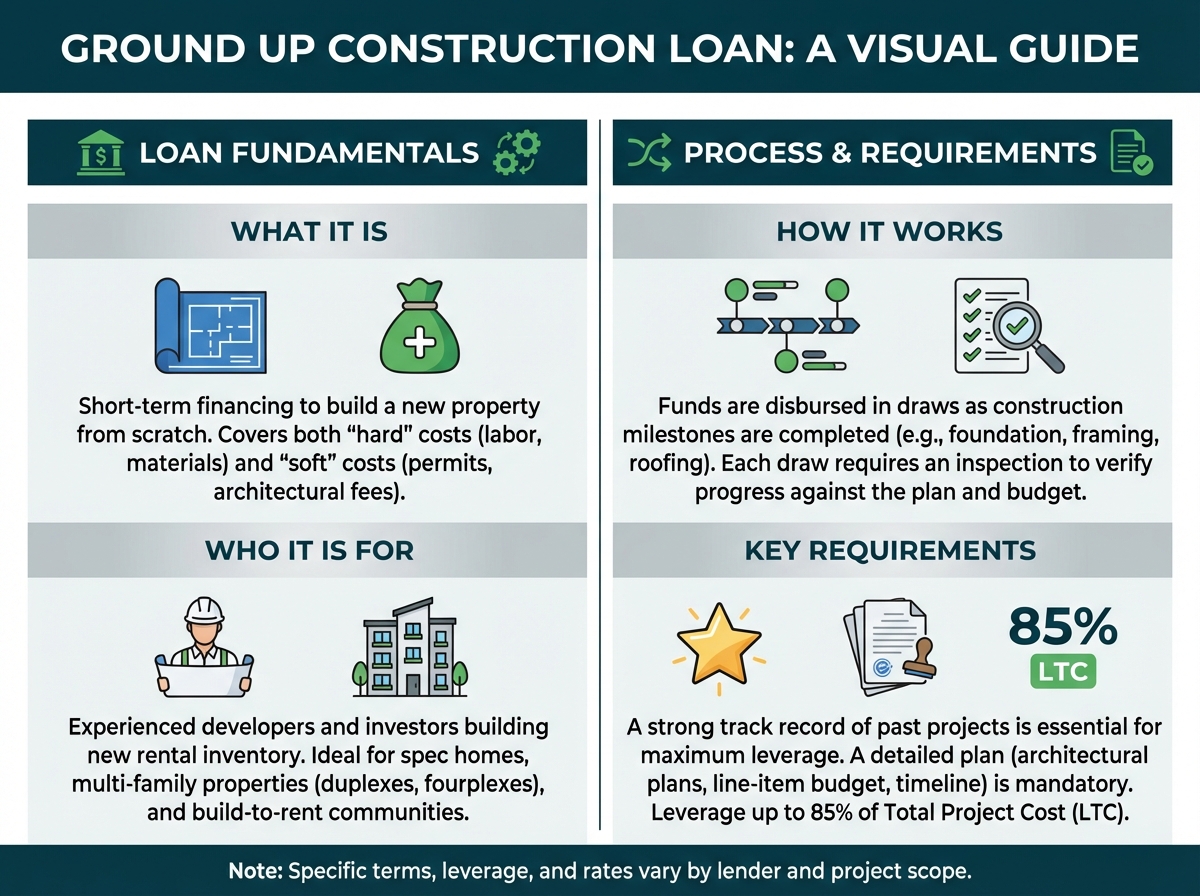

Ground Up Construction Loan

For ambitious investors who want to create their own rental inventory, a ground up construction loan is the essential financing vehicle. This loan funds the entire construction process, from a vacant lot to a certificate of occupancy.

What It Is: Short-term financing for building a new property from scratch

This loan covers the "hard" costs (labor, materials) and "soft" costs (permits, architectural fees) associated with new construction. It's a specialized product that requires a higher level of experience and planning than a standard purchase loan.

How It Works: Funds are disbursed in draws as construction milestones are completed

Similar to a fix and flip rehab budget, construction funds are not disbursed as a lump sum. They are held by the lender and released in stages based on a pre-approved draw schedule.

- Initial Draw: May cover land acquisition and initial site work.

- Milestone Draws: Subsequent draws are funded upon completion of major phases like foundation, framing, roofing, and mechanical systems.

- Final Draw: The last portion is released once the project is complete and has received its Certificate of Occupancy. Each draw requires an inspection to verify that the work has been completed according to the plan and budget.

Who It Is For: Experienced developers and investors building new rental inventory

Lenders require a strong track record for ground up construction loans. You'll need to demonstrate that you have successfully completed similar projects in the past. This loan is ideal for:

- Builders constructing spec homes to be rented out.

- Investors building multi-family properties like duplexes or fourplexes.

- Developers creating build-to-rent communities.

Key Features: Requires a strong track record of past projects for maximum leverage

- Experience is Key: The more successful projects you have on your resume, the better the terms (higher leverage, lower rates) you can secure.

- Detailed Plan Required: You must submit a comprehensive package including architectural plans, a detailed budget (line-item), and a construction timeline.

- Leverage: Loan amounts are typically based on a percentage of the Total Project Cost (LTC) or the final "as-completed" value of the property. Experienced borrowers can often secure financing for up to 85% of the project cost.

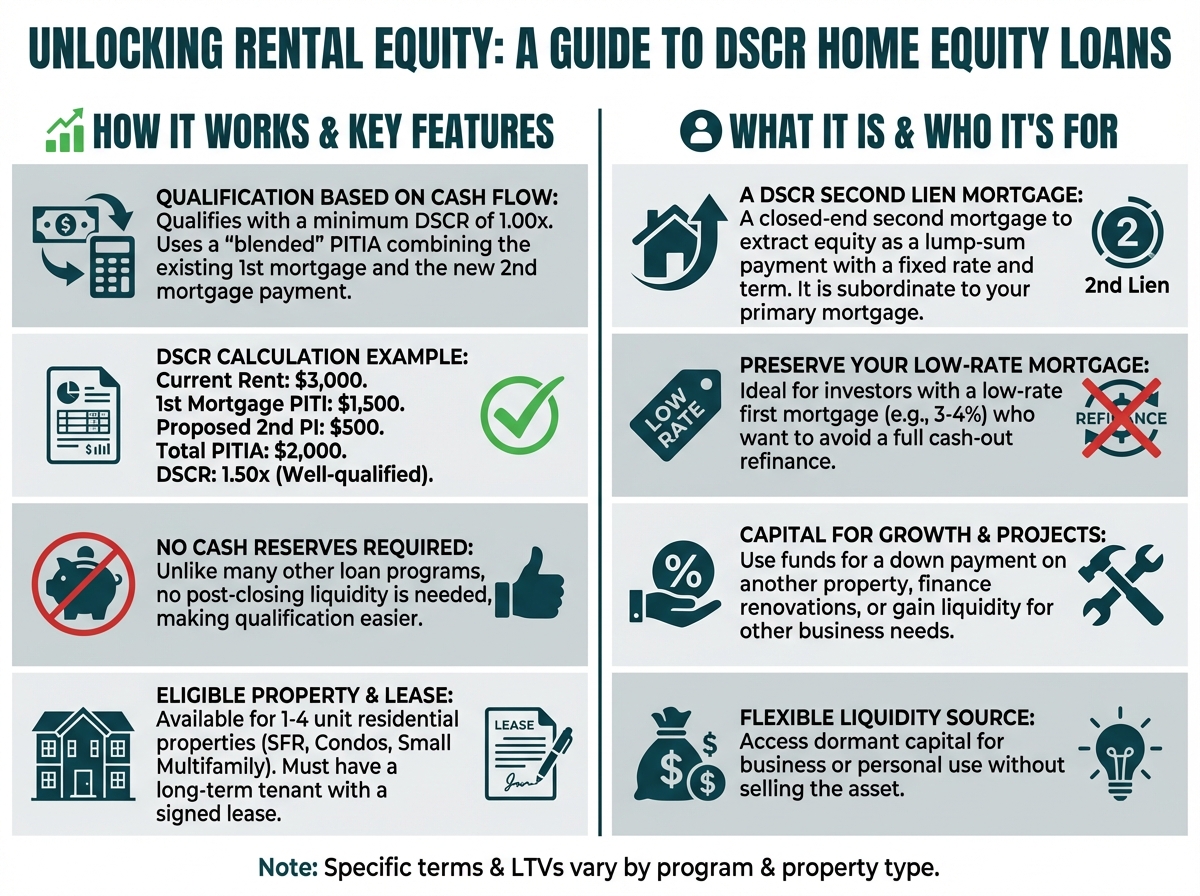

Home Equity Loan for Rental Properties

A home equity loan on an investment property is a powerful way to unlock dormant capital and put it to work. It allows you to access the equity you've built without having to sell or do a cash-out refinance on the entire property.

What It Is: A closed-end second mortgage (DSCR second lien) to extract equity

This is a loan taken out against your property that is subordinate to your primary mortgage. It’s a "second lien," meaning if you default, the primary mortgage holder gets paid back first. Unlike a Home Equity Line of Credit (HELOC), a home equity loan provides a lump-sum disbursement of cash with a fixed interest rate and a fixed repayment term.

How It Works: Qualifies based on a minimum DSCR of 1.00x on the property's cash flow

OfferMarket's Home Equity Loan for rental properties uses the DSCR methodology for qualification. The underwriting team will look at the property's current rental income and calculate a "blended" PITIA that includes the payment on your existing first mortgage and the proposed payment on the new second mortgage. The combined payment must be covered by the rent (DSCR must be 1.00x or greater).

Example:

- Current Rent: $3,000

- 1st Mortgage PITI: $1,500

- Proposed 2nd Mortgage PI: $500

- Total PITIA: $2,000

- DSCR: $3,000 / $2,000 = 1.50x (Well-qualified)

Who It Is For: Investors wanting to tap into equity without refinancing a low-rate first mortgage

This product is perfect for investors who:

- Secured a primary mortgage with an ultra-low interest rate (e.g., 3-4%) and don't want to lose it by refinancing.

- Need capital for a down payment on another investment property.

- Want to fund renovations on the subject property or another property in their portfolio.

- Need liquidity for business or personal use.

Key Features: No cash reserves required, available for 1-4 unit properties with long-term leases

- No Cash Reserves: Unlike many other loan programs, this one does not require you to have post-closing liquidity, making it easier to qualify.

- Property Types: Eligible for 1-4 unit residential properties, including single-family homes, condos, and small multi-family buildings.

- Lease Requirement: The property must have a long-term tenant in place with a signed lease to verify the rental income used in the DSCR calculation.

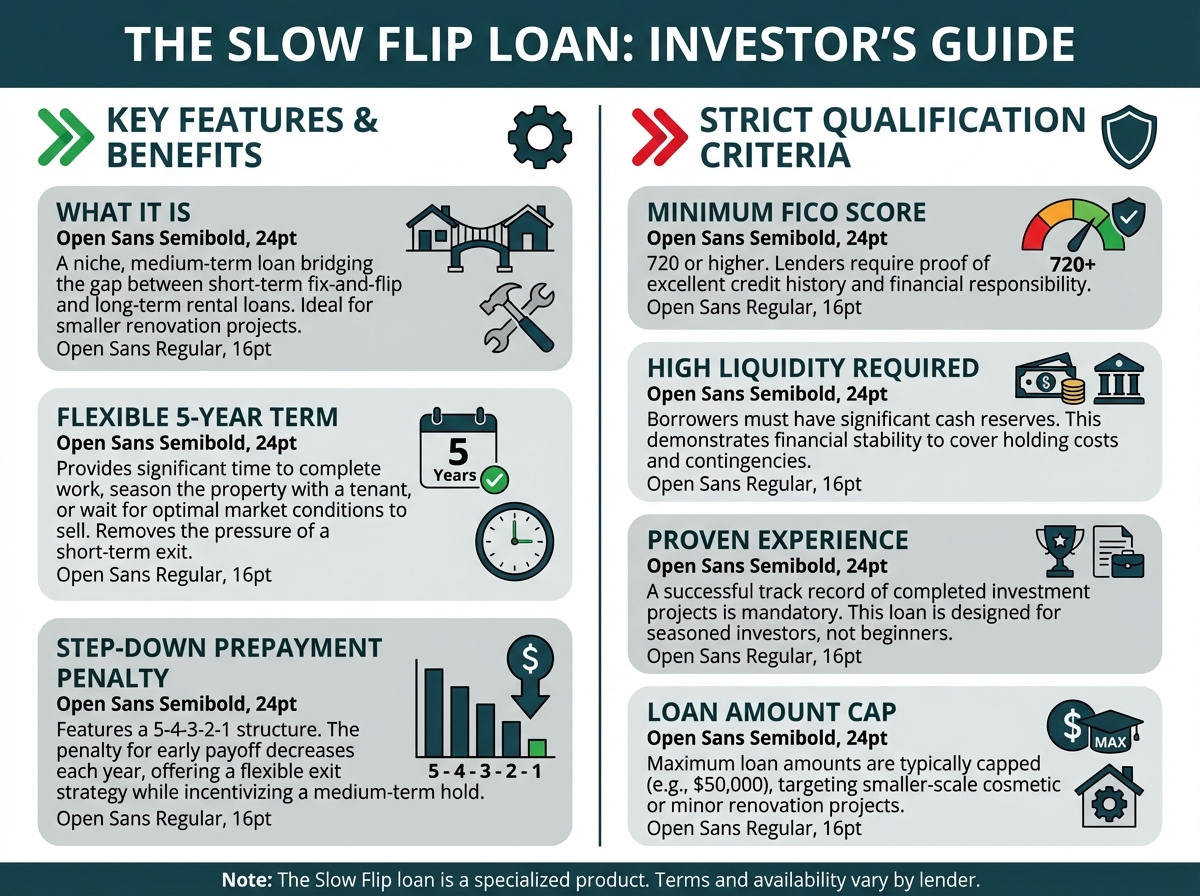

Slow Flip Loan

The Slow Flip loan is a specialized product that bridges the gap between a short-term fix and flip loan and a long-term rental loan. It's designed for experienced investors who have smaller projects that may not fit the timeline of a hard money loan.

What It Is: A niche, medium-term loan for smaller renovation projects

This loan provides financing for projects that might involve cosmetic updates or minor renovations where the investor needs more time to complete the work, season the property with a tenant, or wait for optimal market conditions to sell.

How It Works: Strict qualification criteria including a 720 FICO and high liquidity

Due to its unique structure, the Slow Flip loan has more stringent qualification requirements than a standard fix and flip loan. Lenders need to see that you are a highly qualified and experienced borrower. This typically includes:

- Minimum FICO Score: 720 or higher.

- Liquidity: Significant cash reserves are required.

- Experience: A proven track record of successful projects.

- Loan Amount Cap: The maximum loan amount is typically capped, for example, at $50,000.

Who It Is For: Experienced investors with smaller projects capped at a $50,000 loan amount

This loan is not for beginners. It's tailored for seasoned investors who have a specific need for a longer term on a smaller-scale project. For example, an investor who wants to gradually update a rental property between tenants without the pressure of a 12-month balloon payment.

Key Features: 5-year term with a step-down prepayment penalty

- 5-Year Term: This extended term provides significant flexibility, removing the pressure to complete a project and exit the loan quickly.

- Step-Down Prepayment Penalty: This is a key feature. The penalty for paying off the loan early decreases over time. The standard program uses 5-4-3-2-1 step-down structure (5% in year one, 4% in year two, 3% in year three, 2% in year four, and 1% in year five). This structure incentivizes holding the loan for a reasonable period but still allows for an early exit.

Get Your Instant Loan Quote

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →Key Requirements for Rental Property Loan Approval

While specialized investor loans are more flexible than conventional mortgages, they still have rigorous underwriting standards. Meeting these key requirements will significantly increase your chances of approval and help you secure the best possible terms.

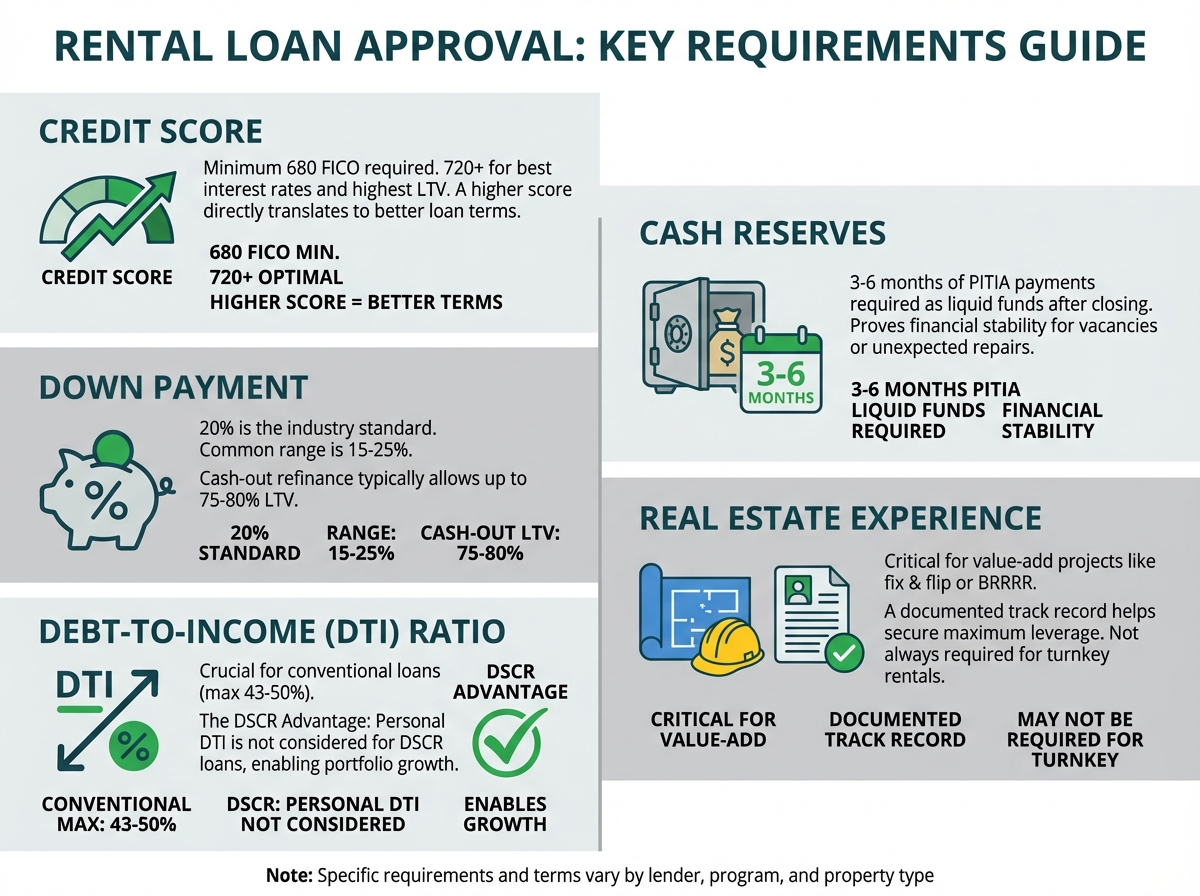

Credit Score: Minimum scores and impact on interest rates

Your credit score is a reflection of your financial responsibility and is a critical factor for any lender. While DSCR loans don't focus on your income, they absolutely focus on your credit history.

- Minimum Score: Most investor loan programs require a minimum FICO score of 680. For the best interest rates and highest leverage (LTV), lenders prefer to see a score of 720 or higher.

- Impact on Terms: A higher credit score directly translates to a lower perceived risk for the lender. An investor with a 760 FICO will receive a lower interest rate and may be offered a higher LTV than an investor with a 680 FICO, even for the same property. For more information on how scores are calculated, you can visit official sources like myFICO.

Down Payment: Standard requirements and sourcing options

The down payment, or your "skin in the game," is another crucial component. For investment properties, expect to put down more than you would for a primary residence.

Standard Requirement: A 20% down payment is the industry standard for a rental property purchase. For some programs, like a DSCR loan, you may find options with 15% down, but 20-25% is more common and will get you better terms. For a cash-out refinance, lenders typically allow you to borrow up to 75-80% of the property's appraised value.

Sourcing Options: Your down payment must come from a legitimate source. This can include personal savings, funds from a business account, a gift from a family member (which requires a formal gift letter), or capital pulled from another property via a home equity loan. Creative strategies like seller financing can sometimes be used to cover a portion of the down payment, but this must be disclosed to and approved by your primary lender.

Debt-to-Income (DTI) Ratio: Relevance for non-DSCR loans versus DSCR loan advantages

Your DTI ratio compares your total monthly debt payments to your gross monthly income.

Relevance for Conventional Loans: For any conventional or government-backed loan, DTI is a paramount metric. Lenders typically want to see a DTI of 43% or lower, though some programs go up to 50%. As defined by the CFPB, this is a major limiting factor for investors with multiple mortgages.

The DSCR Advantage: This is where DSCR loans shine. Because qualification is based on the property's income, your personal DTI is not considered. This allows you to acquire more properties than would be possible with conventional financing, as each new conventional mortgage adds to your personal DTI calculation.

Cash Reserves: Post-closing liquidity requirements

Lenders need to know you have the financial stability to handle unexpected vacancies or repairs. This is verified by checking your post-closing cash reserves.

What They Are: Cash reserves are liquid funds you have remaining after paying the down payment and all closing costs. This can be in checking/savings accounts, brokerage accounts, or retirement accounts (usually counted at a percentage, like 60-70%).

How They're Measured: Reserves are measured in months of the subject property's PITIA payment. Most lenders require 3-6 months of reserves. For example, if the PITIA on your new rental is $2,000, you would need to show proof of $6,000 to $12,000 in liquid assets after closing. For investors with larger portfolios, the reserve requirement may be calculated based on a percentage of the total unpaid principal balance of all financed properties.

Real Estate Experience: Its role in securing favorable terms for value-add projects

For a straightforward purchase of a turnkey rental with a DSCR loan, experience is not always required. However, for any value-add project (fix and flip, BRRRR, ground up construction), your track record is critical.

Why It Matters: Lenders are investing in your ability to successfully execute the business plan. A history of completed projects shows you can manage a budget, timeline, and contractors, significantly reducing the lender's risk.

What Lenders Look For: A "real estate resume" showing the addresses of properties you've bought, renovated, and sold or refinanced in the last 2-3 years. The more experience you can document, the more likely you are to be approved for maximum leverage (e.g., 90% LTV and 100% of rehab costs) on a fix and flip loan.

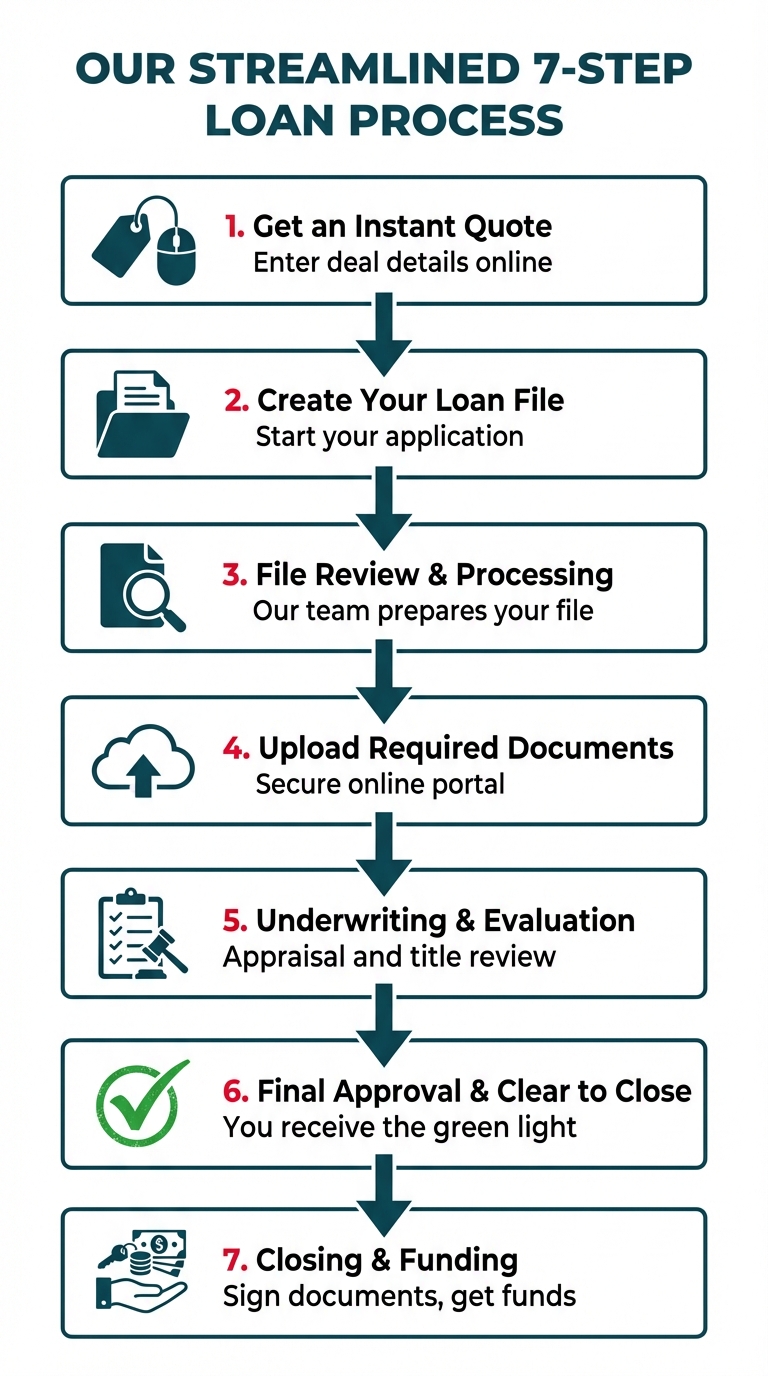

The OfferMarket Loan Process: Step-by-Step

We've engineered our loan process for speed, transparency, and efficiency, allowing you to go from application to closing faster than traditional lenders.

Step 1: Get an Instant Quote

Start by entering your property address and project details into our instant quote tool. In less than two minutes, you'll receive a real-time term sheet outlining your estimated loan amount, interest rate, leverage, and key terms—without a credit pull.

Step 2: Create Your Loan File

If the terms look good, proceed by creating your loan file. You'll provide basic information about yourself and your borrowing entity (typically an LLC or corporation), along with a few high-level details about the project.

Step 3: File Review and Processing

Once submitted, your file enters our processing queue and is assigned to a dedicated loan analyst. This person becomes your primary point of contact and helps guide you through the rest of the process.

Step 4: Upload Required Documents

Using our secure online portal, you’ll upload the required documents—typically including your entity formation documents, government ID, purchase contract, and renovation scope of work. Keeping these documents organized helps speed up approval.

Step 5: Underwriting and Property Evaluation

While documents are being uploaded, our team begins the underwriting process. This includes ordering a valuation (often a desktop appraisal to save time and cost) and running title and background checks. The underwriter reviews the deal to ensure it meets lending guidelines.

Step 6: Final Approval and Clear to Close

Once underwriting is complete and all conditions are satisfied, your loan receives final approval and a “clear to close.” We issue the loan commitment and send closing instructions and documents to the title company or closing attorney.

Step 7: Closing and Funding

You’ll sign the closing documents, and funds are wired to the title company to complete the transaction. From application to funding, the process typically takes 10 to 21 days, allowing investors to move quickly on opportunities.

Advanced Financing Strategies

As you grow your portfolio, you can employ more sophisticated strategies to optimize your financing and accelerate your growth.

Financing Multiple Rental Properties: Using portfolio loans

A portfolio loan is a single loan that is secured by multiple properties. Instead of having five separate mortgages for five properties, you have one loan and one monthly payment.

Benefits: This can simplify your bookkeeping and potentially lower your overall borrowing costs. It also allows you to "blanket" properties together, using the equity in well-performing assets to help you acquire new ones.

When to Use It: This is a great strategy once you have 5-10+ properties and want to streamline your debt management or pull a large amount of cash out from your portfolio's combined equity.

Second Home vs. Investment Property Loan: Understanding the critical underwriting differences

The way a property is classified has a massive impact on the loan terms.

Second Home: A property you intend to occupy for part of the year and do not rent out. These loans have more favorable terms, including lower down payment requirements (as little as 10%) and lower interest rates, because they are considered less risky. You must have exclusive control over the property and cannot have a rental management agreement in place.

Investment Property: A property you intend to rent out for income. The underwriting is stricter, requiring higher down payments (20%+) and slightly higher interest rates. Declaring a property as a second home when you intend to use it as a full-time rental is mortgage fraud, which has severe consequences. Lenders will scrutinize properties in vacation areas to ensure they meet the second home criteria.

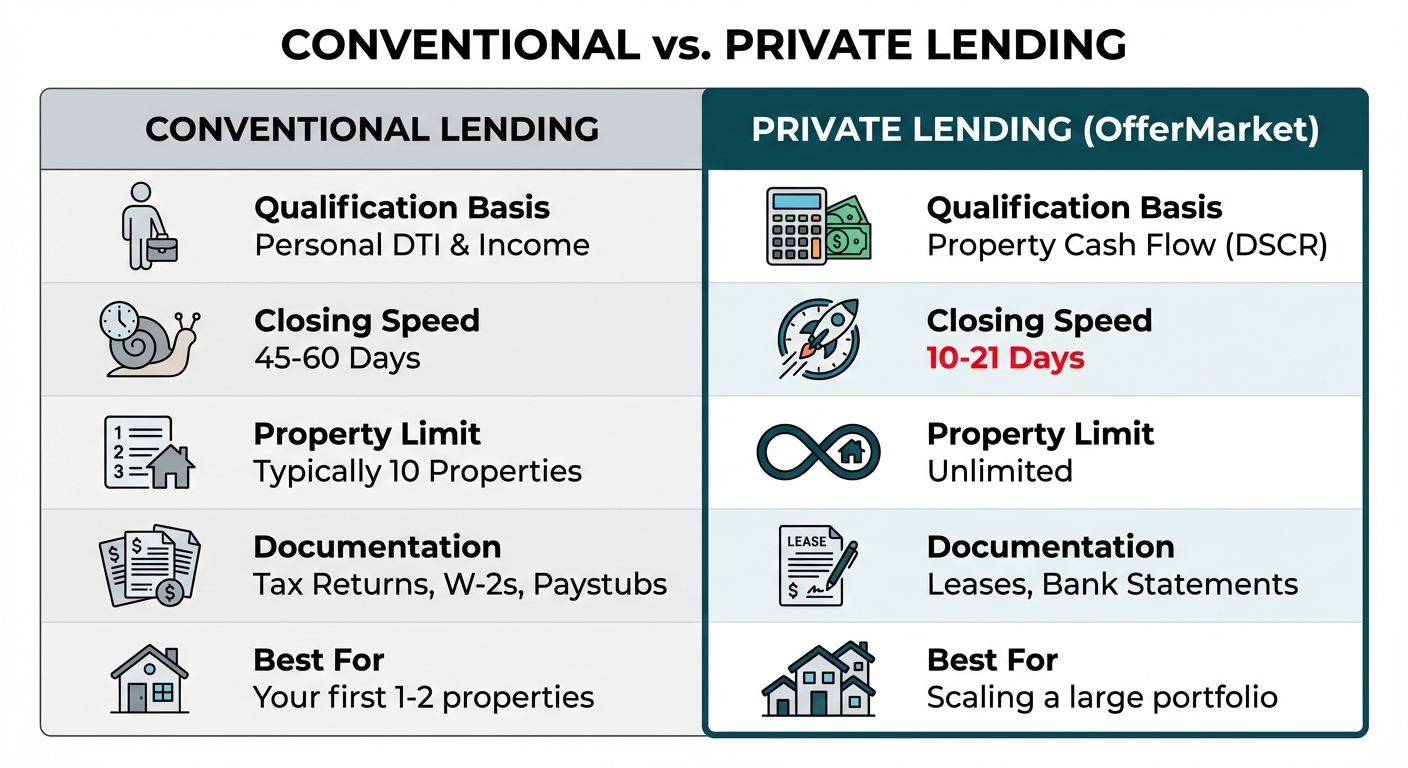

Conventional vs. Private Lending: Comparing the benefits of speed and flexibility

While conventional loans from a bank or credit union can offer low rates, they come with significant drawbacks for investors.

Conventional Loans: Strict DTI limits, caps on the number of financed properties (typically 10), slow closing times (45-60 days), and extensive personal income documentation.

Private Lending (like OfferMarket): Focus on asset performance (DSCR), no limit on financed properties, fast closing times (10-21 days), and streamlined documentation. While interest rates may be slightly higher, the speed and flexibility offered by a private lender are invaluable for investors who need to move quickly on deals and scale their portfolios without being constrained by personal income.

Conclusion: Your Partner in Rental Property Investing

Navigating the world of investment property financing can be complex, but understanding your options is the first step toward building a powerful and profitable real estate portfolio. The five primary loan types—DSCR, Fix and Flip, Ground Up Construction, Home Equity, and Slow Flip—each offer a unique solution tailored to a specific investment strategy. Whether you're buying a turnkey rental, executing a full BRRRR, or building from scratch, the right financing vehicle is available.

At OfferMarket, we specialize in providing these investor-focused loan products. Our value proposition is built on speed, flexibility, and competitive terms designed to help you close more deals and scale your business efficiently. By leveraging technology and focusing on the metrics that matter for investors, we've streamlined the process from application to funding. Stop letting slow, restrictive bank lending hold you back. Fund your next deal with a partner who understands your goals.

Take the first step today and get an instant, transparent quote for your next rental property loan.

OfferMarket Loans

Check your rate

60 seconds · no credit pull