*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

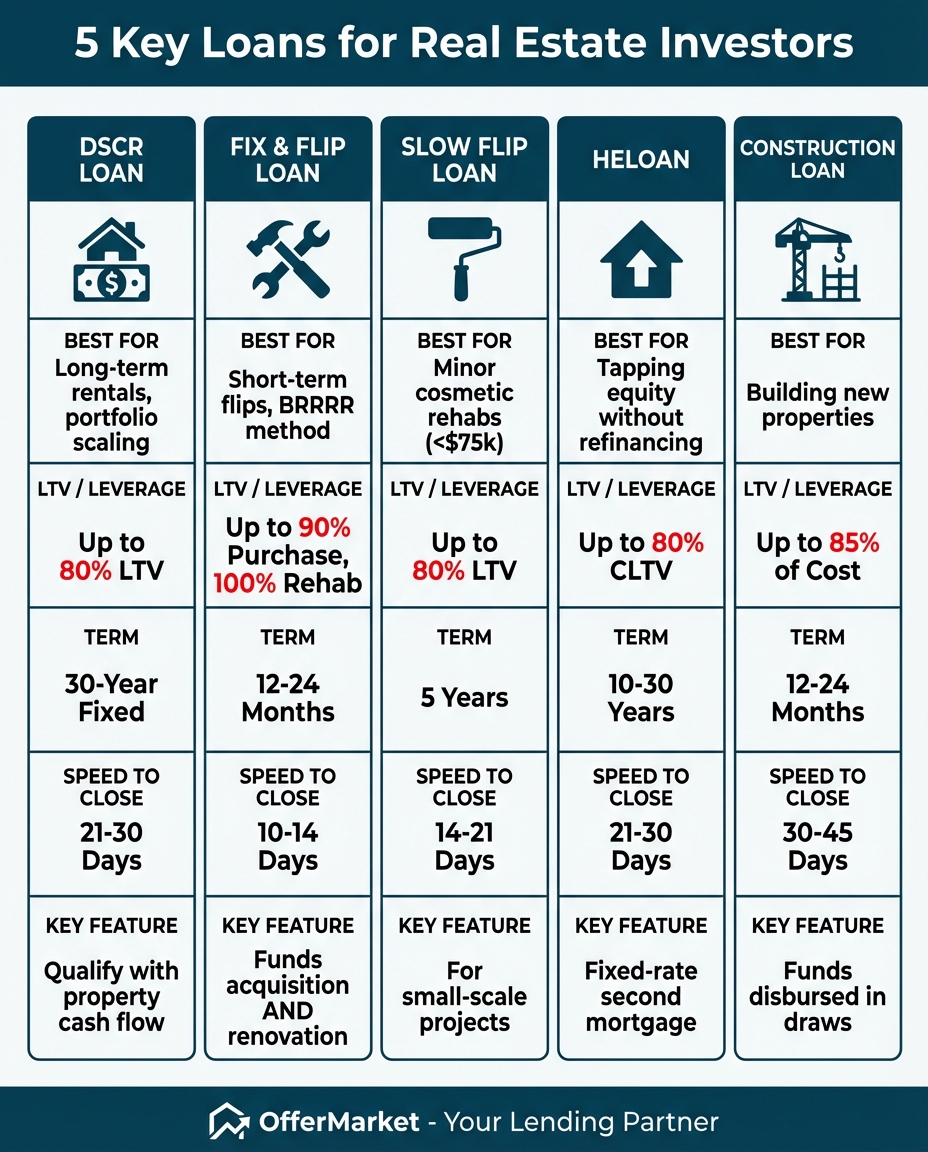

Navigating Investment Property Loans: A Direct Comparison

Lending for investment property operates on a fundamentally different principle than traditional home mortgages. Instead of primarily scrutinizing your personal income and debt-to-income (DTI) ratio, investor-focused lenders prioritize the property's ability to generate income. This is the core of asset-based lending, where the loan is underwritten based on the investment's financial performance and value, not just your W-2. For real estate investors, this shift is critical. It means your deal's strength, measured by metrics like Debt Service Coverage Ratio (DSCR) or After Repair Value (ARV), becomes the key to unlocking capital.

This guide dives deep into the five most powerful types of investment property loans: DSCR, Fix & Flip, Slow Flip, HELOAN, and Ground-Up Construction. We'll dissect how each works, who they're for, and how they stack up on the key metrics that matter to investors: Loan-to-Value (LTV) for leverage, speed to close, overall cost, and loan term. Understanding these differences is the first step to choosing the right financing vehicle to scale your portfolio, maximize your returns, and avoid the common roadblocks of conventional lending.

Understanding Asset-Based vs. Income-Based Lending

The single most significant hurdle for real estate investors seeking traditional financing is the reliance on personal income verification. Conventional mortgages, underwritten to guidelines set by Fannie Mae and Freddie Mac, are designed for owner-occupants. They meticulously analyze your pay stubs, tax returns, and existing debts to calculate your DTI ratio. For many successful investors—especially those who are self-employed, have variable income, or reinvest heavily in their business—this model is restrictive and often results in denials, even for profitable deals.

Asset-based lending flips the script. Lenders in this space, like OfferMarket, are more concerned with two questions:

- Does the property generate enough income to cover the proposed mortgage payment and expenses?

- Is there sufficient equity or value in the property to secure the loan?

This approach opens doors for investors who can't fit into the rigid box of traditional underwriting. Your ability to find a great deal becomes more important than your personal balance sheet.

Key Metrics for Comparison: LTV, Speed, Cost, and Term

When evaluating loans for investment property, you must look beyond the interest rate. Four core metrics will determine a loan's suitability for your specific project:

- Loan-to-Value (LTV) / Loan-to-Cost (LTC): This ratio represents the amount of leverage you can achieve. A higher LTV means less cash required out of pocket. For acquisition, LTV is the loan amount divided by the property's purchase price or appraised value (whichever is lower). For renovation loans, Loan-to-Cost (LTC) is often used, representing the loan amount as a percentage of the total project cost (purchase price plus rehab budget).

- Speed (Time to Close): In competitive real estate markets, the ability to close quickly is a massive advantage. While a conventional loan can take 45-60 days, many investor loans can close in as little as 10-21 days, allowing you to compete with cash buyers.

- Cost (Points, Interest Rate, Fees): The cost of capital is more than just the interest rate. You must account for origination fees (often called "points," where one point equals 1% of the loan amount), processing fees, and potential prepayment penalties. Short-term loans may have higher rates and points but offer flexibility, while long-term loans have lower rates but may include penalties for early payoff.

- Term: The loan term should align with your strategy. A 12-month, interest-only loan is perfect for a quick flip, while a 30-year, fixed-rate amortizing loan is ideal for a long-term rental property.

Matching Loan Types to Specific Real Estate Strategies

There is no "one-size-fits-all" loan in real estate investing. The optimal financing depends entirely on your goal:

- Buy-and-Hold Rentals: The goal is long-term, stable cash flow. A 30-year fixed-rate DSCR loan is often the perfect fit.

- House Flipping: Speed and high leverage on the purchase and renovation are paramount. A short-term Fix & Flip loan (hard money) is the industry standard.

- BRRRR Method (Buy, Rehab, Rent, Refinance, Repeat): This strategy requires a two-step financing process: a short-term Fix & Flip loan for the acquisition and rehab, followed by a long-term DSCR loan for the refinance to pull cash out and hold as a rental.

- New Construction: Building from the ground up requires specialized financing that funds the project in stages. A ground-up construction loan is designed for this purpose.

Why Traditional Mortgages Often Fail for Investors

Beyond the strict DTI requirements, conventional loans present other significant obstacles for serious investors:

- Property Limits: Fannie Mae and Freddie Mac generally limit an individual to a maximum of 10 financed properties. This creates a hard ceiling for investors looking to scale a large portfolio.

- Slow Underwriting: The extensive documentation required (tax returns, pay stubs, letters of explanation) and multi-layered approval process make closing in under 30 days nearly impossible.

- Seasoning Requirements: Conventional lenders often require a "seasoning" period after a purchase or renovation before they will allow a cash-out refinance based on the new, higher appraised value. This can tie up your capital for six months to a year, slowing down the "Repeat" phase of the BRRRR strategy.

- Inability to Lend to Entities: For liability protection and tax purposes, most serious investors hold properties in an LLC. Many conventional lenders will only lend to individuals, not business entities.

These limitations are precisely why the private lending market for investors exists. It provides the speed, flexibility, and leverage necessary to execute professional real-estate strategies effectively.

1. DSCR (Debt Service Coverage Ratio) Loans

A DSCR loan is a long-term financing solution for income-generating investment properties, underwritten primarily based on the property's cash flow rather than the borrower's personal income. It is the quintessential asset-based loan for buy-and-hold investors.

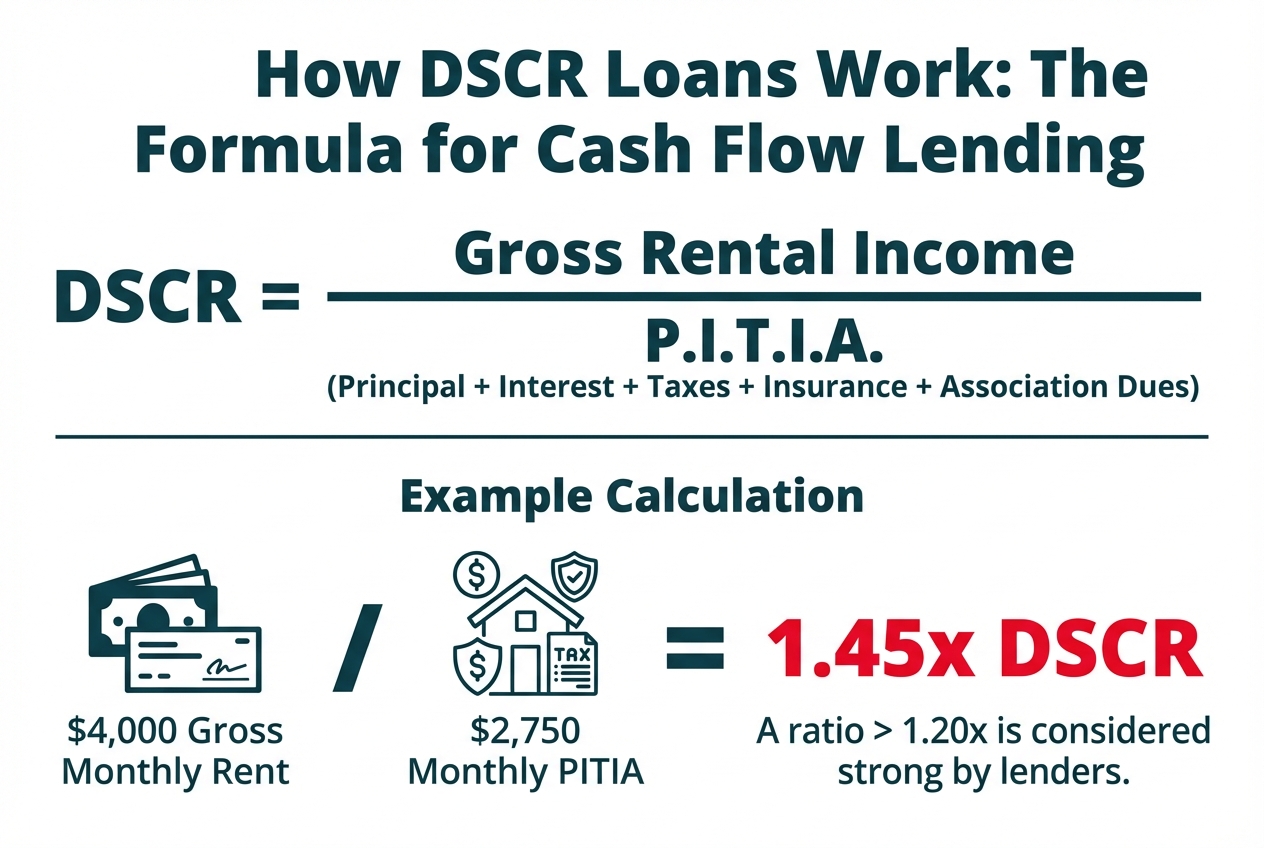

Core Concept: Property Cash Flow Qualifies the Loan

The "Debt Service Coverage Ratio" is a simple calculation that lenders use to determine if a property's income is sufficient to cover its debt obligations.

The Formula:

DSCR = Gross Rental Income / PITIA

- Gross Rental Income: The total monthly rent collected from the property.

- PITIA: The total monthly housing expense, which stands for Principal, Interest, Taxes, Insurance, and Association (HOA) fees.

Lenders require the DSCR to be above a certain threshold, typically 1.0x, with most preferring 1.20x or higher. A ratio of 1.20x means the property generates 20% more income than is needed to cover the mortgage and related expenses, providing a healthy cash flow buffer.

Example DSCR Calculation: Let's say you're buying a duplex that rents for a total of $4,000 per month. The proposed new mortgage payment (P&I) is $2,200, property taxes are $400/month, insurance is $150/month, and there are no HOA fees.

- Gross Rental Income: $4,000

- PITIA: $2,200 (P&I) + $400 (Taxes) + $150 (Insurance) = $2,750

- DSCR: $4,000 / $2,750 = 1.45x

With a DSCR of 1.45x, this property easily qualifies for a DSCR loan, as it demonstrates strong cash flow well above the typical 1.20x requirement. You can use an online DSCR calculator to quickly analyze the viability of your own deals.

Ideal Investor Profile

DSCR loans are perfect for:

- Buy-and-Hold Investors: This is the primary audience. The long-term, fixed-rate nature of the loan provides stability for rental income.

- Self-Employed Individuals: Entrepreneurs, freelancers, and business owners whose tax returns don't reflect their true cash flow can qualify easily.

- Investors Scaling a Portfolio: Without the 10-property limit of conventional loans, investors can use DSCR loans to acquire dozens of properties.

- Investors Using the BRRRR Method: After rehabbing and renting a property, a DSCR loan is the ideal tool for the "Refinance" step, allowing you to pull cash out based on the new appraised value.

Key Terms and Conditions

While terms vary by lender, here's what you can typically expect with a DSCR loan from a provider like OfferMarket:

- Loan-to-Value (LTV): Up to 80% for purchases and rate/term refinances. Up to 75% for cash-out refinances.

- Loan Term: Most commonly a 30-year fixed term, providing predictable payments. Interest-only options are also available, often for the first 10 years of a 40-year term.

- DSCR Requirement: Minimum of 1.0x, but a ratio of 1.20x or higher will secure the best rates and terms. Some lenders may go lower, but the rate will be higher.

- Credit Score: Minimum FICO score is typically around 660, with the best pricing reserved for borrowers with 720+.

- Prepayment Penalties: This is a key feature. Most DSCR loans have a prepayment penalty, often structured as "3-2-1" or "5-4-3-2-1". A "3-2-1" penalty means if you pay off the loan in the first year, you owe a penalty of 3% of the outstanding balance. In the second year, it's 2%, and 1% in the third. After three years, there is no penalty. This structure allows lenders to offer lower long-term rates.

When to Use a DSCR Loan

- Purchasing a turnkey rental property: When a property is already cash-flowing, a DSCR loan is the most straightforward way to finance it without touching your personal income documents.

- Refinancing out of a hard money loan: This is the final step in the BRRRR strategy. After you've renovated and tenanted the property, a DSCR loan provides the permanent, long-term financing.

- Scaling your rental portfolio: When you've hit the conventional loan limit or want to acquire properties more quickly and efficiently, DSCR loans are the path forward.

- Cash-out refinancing: If you have significant equity in an existing investment property, a DSCR cash-out refinance lets you pull that capital out to use for down payments on future acquisitions.

2. Fix & Flip, Hard Money, and Bridge Loans

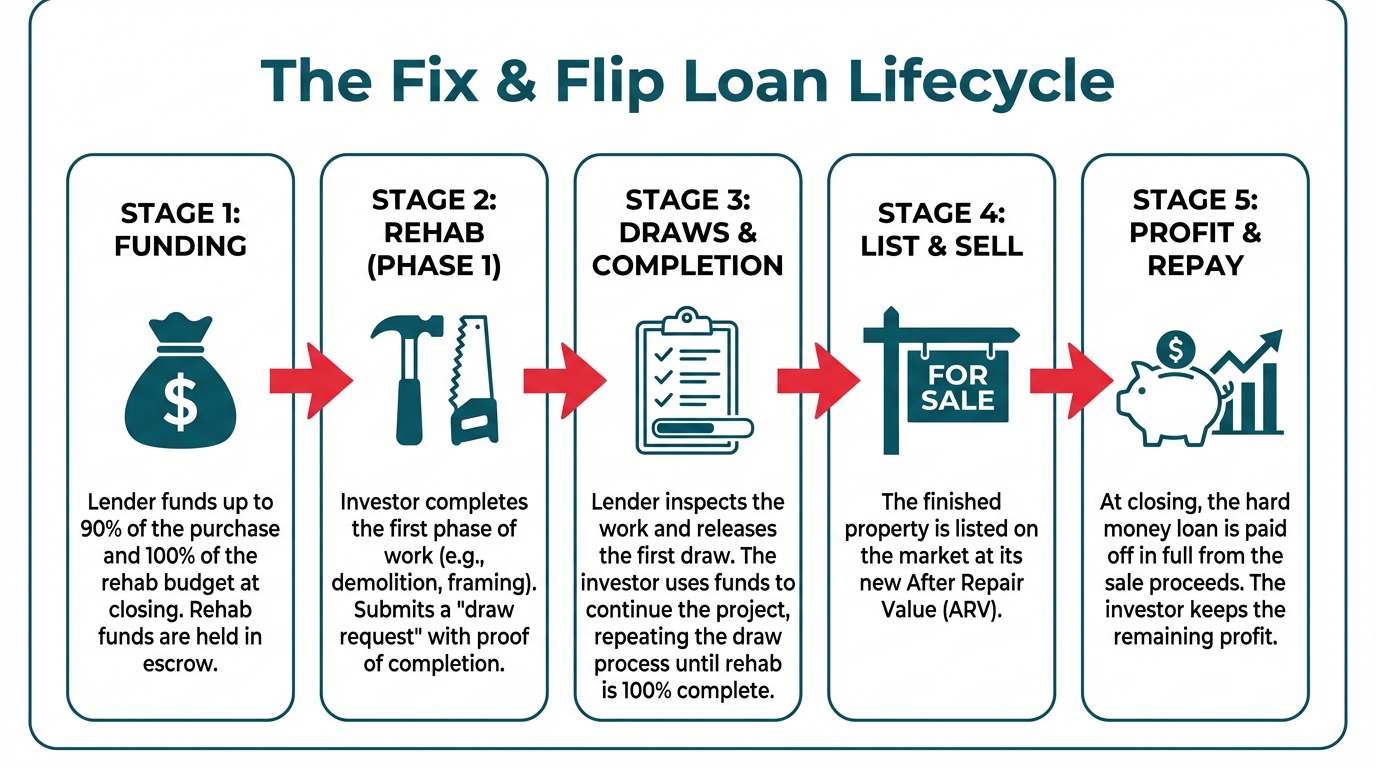

Fix & flip loans, often referred to as hard money or bridge loans, are short-term, asset-based financing tools designed for the acquisition and renovation of properties that you intend to sell quickly. Their primary advantages are speed and leverage, allowing investors to secure a property and fund its transformation with minimal cash out of pocket.

Core Concept: Short-Term Financing for Acquisition and Renovation

Unlike long-term loans, fix & flip financing is focused on a property's potential value, or After Repair Value (ARV). The lender underwrites the deal based on your renovation plan and the projected market value of the property once the work is complete. The loan is structured to cover a significant portion of both the purchase price and the renovation budget.

This type of financing serves as a "bridge" to get you from the purchase of a distressed asset to the sale of a stabilized, market-ready home. Because the timeline is short (typically 12 months), the costs are structured differently, with an emphasis on interest-only payments and origination points rather than long-term amortization.

Ideal Investor Profile

These loans are tailored for active, hands-on investors:

- Experienced House Flippers: Investors who have a proven system for finding, renovating, and selling properties rely on the speed and leverage of hard money to execute their business model.

- BRRRR Method Investors: For the "Buy" and "Rehab" phases of the BRRRR strategy, a fix & flip loan is the perfect tool. It provides the capital needed to acquire and improve the property before refinancing into a long-term DSCR loan.

- Wholesalers and Wholetailers: Investors who get a property under contract and may do a light cosmetic renovation before reselling it to another investor or a homeowner can use bridge financing to close the deal quickly.

Key Terms and Structure

Fix & flip loans have a unique structure designed to accommodate a renovation project:

- Leverage: Lenders typically offer up to 90% of the purchase price and 100% of the renovation budget. The total loan amount is usually capped at 70-75% of the property's ARV.

- Term: The standard term is 12 months. Some lenders may offer extensions for a fee or provide slightly longer terms (18-24 months) for larger projects.

- Interest: Payments are almost always interest-only. This keeps the monthly carrying costs low during the renovation phase when the property is not generating income.

- Rehab Funds Disbursement (The Draw Process): The portion of the loan allocated for renovations is not given to you as a lump sum at closing. Instead, it's held in escrow and disbursed in "draws" as you complete phases of the project. You'll submit a draw request with proof of completed work (photos, receipts, inspection report), and the lender will release the funds for that portion of the budget.

- No Prepayment Penalty: Since the entire business model is based on a quick sale, these loans do not have prepayment penalties. You are encouraged to pay them off as soon as the project is complete.

Cost Structure: Understanding Points and Interest

The cost of a hard money loan is typically higher than a long-term mortgage, which is a trade-off for the speed, leverage, and flexibility it provides.

- Origination Points: Lenders charge upfront fees called points. One point is equal to 1% of the total loan amount. It's common to see 1 to 2 points on a fix & flip loan. For a $300,000 loan, 2 points would equal a $6,000 fee, which is often rolled into the loan itself.

- Interest Rates: Rates are higher than conventional or DSCR loans, often ranging from 9% to 12% APR. However, since you only hold the loan for a few months, the total interest paid is manageable. For example, on a $300,000 loan at 10% interest, your interest-only payment would be $2,500 per month. If you complete the project in 6 months, you'd pay a total of $15,000 in interest.

When analyzing a flip, you must factor these costs into your budget. A good rental property calculator can be adapted to model the holding costs for a flip, including loan interest, points, insurance, and taxes.

3. Slow Flip Low Balance Loans

The Slow Flip loan is a specialized, niche product designed to fill a gap in the market between large-scale renovation loans and small, unsecured personal loans. It's tailored for investors undertaking minor, cosmetic rehab projects on lower-value properties.

Core Concept: Micro-Loans for Cosmetic Renovations

Traditional hard money lenders often have minimum loan amounts (e.g., $75,000 or $100,000) because the administrative work to underwrite a small loan is the same as a large one. This leaves a financing void for investors who find a great deal on a property that only needs $20,000 in cosmetic updates like paint, flooring, and new fixtures.

The Slow Flip loan addresses this by providing small-balance financing specifically for these types of projects. It offers a simplified underwriting process but comes with a different term structure compared to a standard fix & flip loan.

Ideal Investor Profile

This loan is best suited for:

- Investors doing light cosmetic rehabs: Think paint, carpet, kitchen cabinet refinishing, and landscaping—not tearing down walls or reconfiguring layouts.

- Wholetailers: Investors who want to do a quick cleanup to maximize the resale value to another landlord or first-time homebuyer.

- Landlords refreshing a vacant rental: An owner who needs to update a dated rental unit between tenants to attract a higher rent can use this loan instead of paying for the work out of pocket.

Key Terms and Conditions

The Slow Flip loan has a very distinct set of terms that differentiate it from other products:

- Maximum Loan Amount: The defining feature is the low balance, typically capped at $50,000.

- Term: Instead of a 12-month term, these loans often have a 5-year term. This provides a longer runway for the investor to complete the work and sell or rent the property without the pressure of a looming balloon payment.

- Fees: The fee structure is often simplified, with fixed fees instead of points calculated as a percentage of the loan.

- Prepayment Penalty: This is the most crucial and unique feature. To compensate for the small loan balance and longer term, these loans carry a strict 5-year step-down prepayment penalty. For example:

- Year 1: 5% penalty

- Year 2: 4% penalty

- Year 3: 3% penalty

- Year 4: 2% penalty

- Year 5: 1% penalty

This penalty structure means the loan is not ideal for a traditional 3-6 month flip. An investor using this product must be prepared to hold the property for a longer period or factor the prepayment penalty into their profit calculations if they plan to sell early.

4. HELOAN (Closed-End Second Lien)

A HELOAN, or Home Equity Loan, is a type of second mortgage that allows property owners to borrow against their equity in the form of a lump-sum payment. Unlike a Home Equity Line of Credit (HELOC), which is a revolving line of credit, a HELOAN provides the full loan amount upfront and has a fixed interest rate and a fixed repayment schedule.

Core Concept: Access Equity as a Lump Sum Without Refinancing

The primary benefit of a HELOAN on an investment property is the ability to tap into your equity without disturbing your existing first mortgage. This is incredibly valuable for investors who locked in a historically low interest rate (e.g., 3-4%) on their primary loan. Refinancing that entire loan to pull out cash would mean replacing that great rate with a much higher one on the entire balance.

A HELOAN sits in a second lien position behind your primary mortgage. You receive a lump sum of cash at closing, and you now have two separate mortgage payments each month: one for your original loan and one for the new HELOAN.

Ideal Investor Profile

- Investors with Significant Equity: Property owners who have seen substantial appreciation or have paid down their mortgage over time are prime candidates.

- Owners with a Low-Rate First Mortgage: Anyone who wants to preserve their low-interest primary loan while still accessing capital.

- Investors Needing Capital for a Down Payment: A common strategy is to use a HELOAN on an existing property to fund the down payment for the next acquisition.

Key Terms and Conditions

- Combined Loan-to-Value (CLTV): Lenders will typically go up to 80% CLTV. This is calculated by adding the balance of your first mortgage and the new HELOAN amount, then dividing by the property's current value.

- Example:

- Property Value: $500,000

- First Mortgage Balance: $250,000

- Maximum CLTV (80%): $400,000

- Maximum Equity Available: $400,000 (Max CLTV) - $250,000 (1st Lien) = $150,000 (Max HELOAN amount)

- Example:

- Rates and Term: Interest rates are fixed, which provides a predictable payment. They are higher than first mortgage rates but often lower than unsecured personal loans or credit cards. Terms typically range from 10 to 30 years.

Qualification Methods for Investment Properties

A key innovation in this space is the ability to qualify for a HELOAN on an investment property using DSCR principles. Instead of verifying your personal DTI, a lender like OfferMarket can underwrite the HELOAN based on the property's cash flow. The calculation is slightly different, as it must account for both mortgage payments.

DSCR for a HELOAN:

DSCR = Gross Rental Income / (First Mortgage PITIA + New HELOAN P&I)

The property's rent must be sufficient to cover the debt service of both loans combined. This asset-based approach makes it much easier for real estate investors to unlock the equity in their portfolios.

5. Ground-Up Construction Loans

Ground-up construction loans are a specialized form of financing for investors and builders who are developing a property from scratch. This can include building on a vacant lot or tearing down an existing structure to rebuild. These loans are more complex than standard acquisition or refinance loans due to the inherent risks of the construction process.

Core Concept: Phased Financing for New Builds

A construction loan covers the total cost of the project, including the land acquisition (if not already owned) and the entire construction budget. The fundamental difference is how the funds are disbursed. Instead of a lump sum at closing, the loan is paid out in stages, or draws, tied to specific construction milestones. This protects the lender by ensuring their capital is being used as intended and that the project is progressing on schedule and on budget.

The loan is short-term, typically 12-24 months, designed to last only for the duration of the construction phase. Once the project is complete and a certificate of occupancy is issued, the investor will need to either sell the property or refinance the construction loan into a permanent long-term mortgage, such as a DSCR loan.

Ideal Investor Profile

- Experienced Builders and Developers: Lenders for these projects require a proven track record. Borrowers need to demonstrate they have successfully completed similar projects in the past. This is not a loan for first-time investors.

- Investors with a Strong Team: A successful application requires a full team, including a licensed general contractor, architect, and surveyor.

- BRRRR Investors on an Advanced Scale: Some investors use this for the "build-to-rent" strategy, where they build a new property (e.g., a duplex or fourplex) with the intention of holding it as a long-term rental.

Key Terms and Conditions

- Loan-to-Cost (LTC): This is the primary metric. Lenders will typically finance up to 85% of the total project cost. The investor is responsible for contributing the remaining 15% as equity.

- Term: 12 to 24 months, interest-only.

- The Draw Schedule: This is the heart of the loan agreement. Before closing, the borrower and lender agree on a detailed draw schedule based on the construction budget. Milestones might include:

- Foundation poured

- Framing complete

- Rough-in plumbing and electrical finished

- Drywall and interior finishes

- Final inspection and Certificate of Occupancy

- Inspections: Before each draw is released, the lender will send an inspector to the site to verify that the work for that milestone has been completed satisfactorily.

Critical Requirements for Approval

Securing a construction loan requires extensive documentation to mitigate the lender's risk. Be prepared to provide:

- Detailed Construction Budget: A line-item budget detailing all hard and soft costs, from lumber and labor to permits and architectural fees.

- Architectural Plans and Specs: Complete, permit-ready blueprints and a detailed scope of work.

- Builder/General Contractor Vetting: The lender will need to approve your general contractor, reviewing their license, insurance, and past project portfolio.

- Verified Experience: You, the borrower, will need to provide a portfolio of previously completed projects to demonstrate your experience.

The complexity and stringent requirements of ground-up construction loans make them suitable only for seasoned professionals in the real estate development space.

Comparing Your Financing Options at a Glance

Choosing the right loan requires a clear, side-by-side comparison of how each option performs against the metrics that matter most to your specific investment strategy.

Loan Type vs. Best Use Case

| Loan Type | Best For | Key Differentiator |

|---|---|---|

| DSCR Loan | Long-term buy-and-hold rentals | Qualifies on property cash flow, not personal DTI. 30-year term. |

| Fix & Flip Loan | Short-term (3-9 month) flips, BRRRR projects | Speed and high leverage (up to 100% of rehab). Funds purchase & reno. |

| Slow Flip Loan | Minor cosmetic rehabs on lower-value assets | Small loan amounts (under $50k) with a 5-year term and prepayment penalty. |

| HELOAN | Tapping equity without refinancing | Fixed-rate second mortgage that preserves a low-rate first lien. |

| Construction Loan | Building new properties from the ground up | Funds disbursed in draws based on construction milestones. |

Side-by-Side LTV and Leverage Comparison

Leverage is a measure of how much of the lender's money you can use versus your own. Higher leverage means less cash out of your pocket.

- Highest Leverage for Renovation: Fix & Flip loans are the clear winner, offering up to 90% of the purchase price and 100% of the renovation budget.

- Highest Leverage for Acquisition (Rent-Ready): DSCR loans and Slow Flip loans are comparable, offering up to 80% LTV on a purchase.

- Highest Leverage for New Builds: Construction loans provide up to 85% of the total project cost (LTC).

- Leverage for Existing Assets: HELOANs allow you to access equity up to 80% of your property's combined loan-to-value (CLTV).

Comparing Speed: Time to Close

In a competitive market, speed wins deals. Here's how the options stack up:

- Fastest: Fix & Flip / Hard Money Loans (10-14 Days). These lenders are built for speed and can often close as fast as a cash buyer.

- Moderate: DSCR, Slow Flip, and HELOANs (14-30 Days). These require an appraisal and more detailed underwriting than a hard money loan but are still significantly faster than a conventional mortgage.

- Slowest: Construction Loans (30-45+ Days). The extensive documentation, budget review, and builder vetting process make this the longest closing timeline.

Cost Breakdown: Interest Rates, Points, and Penalties

The cost of capital is a critical part of your ROI calculation.

| Loan Type | Typical Interest Rate | Origination Points | Prepayment Penalty |

|---|---|---|---|

| DSCR Loan | 6.5% - 9.0% | 1 - 2 points | Yes (Typically 3 or 5-year step-down) |

| Fix & Flip Loan | 9.0% - 12.0% | 1 - 2 points | No |

| Slow Flip Loan | 8.0% - 10.0% | Fixed Fees | Yes (Strict 5-year step-down) |

| HELOAN | 7.5% - 10.5% | 0 - 1 point | Varies, often none |

| Construction Loan | 9.5% - 12.5% | 2 - 3 points | No |

Note: Interest rates are subject to market conditions and can change. These are illustrative ranges.

Matching the Right Loan to Your Investment Strategy

Theory is great, but let's apply this knowledge to the most common real estate investment strategies.

For the BRRRR Method: Combining Fix & Flip with a DSCR Refinance

The BRRRR (Buy, Rehab, Rent, Refinance, Repeat) method is a powerful strategy for building a rental portfolio with minimal capital. It relies on a precise two-step financing process:

- Buy & Rehab: You start by acquiring a distressed property using a Fix & Flip loan. This gives you the high leverage needed to cover the purchase and the 100% financing for the renovation. The short-term, interest-only nature of the loan keeps your holding costs low during the 3-6 month rehab period.

- Rent & Refinance: Once the renovation is complete and you've placed a tenant in the property, it is now a stabilized, cash-flowing asset. The property's value has been "forced" up through the renovation. You then apply for a DSCR cash-out refinance. The new appraisal will reflect the higher ARV. The DSCR loan pays off the entire hard money loan, and if you've executed the strategy correctly (buying right and managing your budget), the new loan will be large enough to return most, if not all, of your original cash investment.

- Repeat: You now have a cash-flowing rental with little to no money left in the deal, and you've recycled your capital to go find the next property.

For House Flipping: Hard Money for Speed and Leverage

For a pure house flipper, the goal is to turn capital over as quickly as possible. The business model depends on maximizing the number of projects completed per year. For this, the Fix & Flip (Hard Money) loan is the undisputed champion.

- Speed: It allows you to compete with cash offers, which is essential for acquiring the best off-market deals from wholesalers or at auctions.

- Leverage: By financing the purchase and the entire renovation, it allows you to spread your capital across multiple projects simultaneously instead of tying it all up in one deal.

- Flexibility: The lack of a prepayment penalty means you can sell the property and pay off the loan the moment the project is finished without incurring extra costs.

For Long-Term Rentals: DSCR or Conventional Loans

When buying a rent-ready property for long-term hold, your priorities shift to securing the lowest possible long-term cost of capital.

- DSCR Loans: This is the preferred tool for most active investors. It allows you to scale beyond 10 properties, close in an LLC, and qualify without your personal tax returns. The rates are competitive, and the 30-year fixed term provides stability.

- Conventional Investment Property Loans: For investors with fewer than 10 properties and strong, easily documented W-2 income, a conventional loan from a bank or mortgage broker can sometimes offer a slightly lower interest rate. However, you must be prepared for a slower, more document-intensive process and the limitations mentioned earlier. For many, the operational ease of a DSCR loan outweighs a marginal difference in rate.

For Scaling Your Portfolio: Portfolio Loans and Strategic Use of DSCR

As you grow, managing dozens of individual loans can become cumbersome. This is where portfolio loans and strategic financing come into play.

- DSCR Loans: The primary engine for scaling remains the DSCR loan, used to acquire properties one by one.

- Portfolio Loans: A portfolio loan is a single, larger loan that is secured by multiple properties at once. This is a refinancing tool, not an acquisition tool. An investor with 5, 10, or 20+ free-and-clear properties (or properties with significant equity) can consolidate them under one blanket mortgage. This simplifies payments and can be used to pull out a large amount of cash at once to fund many future acquisitions.

- Strategic Equity Access: Using HELOANs on stabilized properties within your portfolio can provide quick, efficient access to down payment capital without the need to do a full cash-out refinance on any single property.

The OfferMarket Advantage: Modern Lending for Modern Investors

The real estate investing landscape has evolved, but traditional banking has not kept pace. Investors need a lending partner that understands their business and provides tools built for speed, scale, and efficiency. This is where OfferMarket stands apart.

Technology-Driven Platform for Instant Quotes and Seamless Applications

Our platform is designed to eliminate the friction and delays of old-school lending. You can get a free, instant loan quote in minutes, not days. By providing a few key details about your deal, our system can instantly generate accurate terms for multiple loan products, allowing you to compare your options and make informed decisions on the spot. The entire application and document submission process is handled online through a secure, intuitive portal.

Bypassing Traditional Bank Hurdles

We've built our lending programs from the ground up for investors. That means:

- No Tax Returns Needed for DSCR and Fix & Flip loans.

- No DTI Calculations on asset-based loans.

- No Arbitrary Property Limits. We are a partner for your growth, whether you're buying your second property or your fiftieth.

- LLC and Corporate Vesting is standard practice. We help you protect your assets.

Focus on Asset Performance

Our underwriting philosophy is simple: a great deal deserves a great loan. We focus on the merits of the property—its cash flow, its value, its potential. This aligns our interests with yours and empowers you to get financing based on your skill as an investor, not the structure of your personal income.

Diverse Product Suite for Every Strategy

As this guide has shown, there is a specialized tool for every job in real estate. OfferMarket provides a comprehensive suite of investor-focused loans under one roof. Whether you're executing a BRRRR, a flip, a new build, or simply expanding your rental portfolio, we have the specific financing product you need to execute your strategy efficiently and profitably.

Get Your Instant Investment Property Loan Quote

The best way to understand your financing options is to see real numbers for your specific deal. It takes less than two minutes, requires no hard credit pull, and will give you a clear picture of the rates and terms you qualify for.

- Primary CTA: Get a free, instant quote for your next deal and see how OfferMarket can fund your growth.

- Secondary CTA: Analyze your deals like a pro. Use our free online tools:

- DSCR Calculator to instantly check a rental property's cash flow viability.

- Rental Property Calculator for a full analysis of ROI, cash-on-cash return, and long-term performance.

Have questions about your specific scenario or want to talk through a complex deal? Our lending experts are investors themselves and are ready to help you craft the perfect financing strategy.

Frequently Asked Questions About Investment Property Lending

What is a prepayment penalty and how does it work?

A prepayment penalty is a fee charged by a lender if you pay off your loan before a specified period. It is most common on long-term loans like DSCR loans. The purpose is to ensure the lender earns a certain amount of interest to compensate for the risk and cost of originating the loan. The most common structure is a "step-down" penalty. For example, a "5-4-3-2-1" penalty on a 30-year loan means:

- Pay off in Year 1: 5% of the principal balance is due as a fee.

- Pay off in Year 2: 4% fee.

- Pay off in Year 3: 3% fee.

- Pay off in Year 4: 2% fee.

- Pay off in Year 5: 1% fee.

- After Year 5, there is no penalty.

Short-term loans, like fix & flip loans, do not have prepayment penalties.

Can I get an investment property loan in an LLC?

Yes. In fact, it is highly recommended. Lending to a Limited Liability Company (LLC) or other business entity is a standard practice for private and asset-based lenders like OfferMarket. This is a key advantage over conventional loans, which typically must be made to an individual. Holding property in an LLC provides critical liability protection, separating your personal assets from your business assets.

What is the minimum credit score for investor loans?

The minimum credit score typically starts around 620-660, depending on the loan product and lender. However, the best pricing and highest leverage (LTV) are reserved for borrowers with higher credit scores, usually 720 and above. While the loan is asset-based, the borrower's credit history is still a factor in assessing risk and determining the interest rate.

How are points and origination fees calculated?

Points, also known as origination fees, are an upfront cost for securing the loan. One point is equal to one percent (1%) of the total loan amount. The calculation is straightforward:

Origination Fee = Loan Amount x (Points / 100)

Example:

- Loan Amount: $400,000

- Points Charged: 2 points

- Calculation: $400,000 x (2 / 100) = $8,000

This fee is typically paid at closing and can often be rolled into the total loan balance rather than being paid out of pocket. It's a common cost on both short-term hard money loans and long-term DSCR loans.

OfferMarket Loans

Check your rate

60 seconds · no credit pull