*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

The Fast-Track BRRRR Method Explained

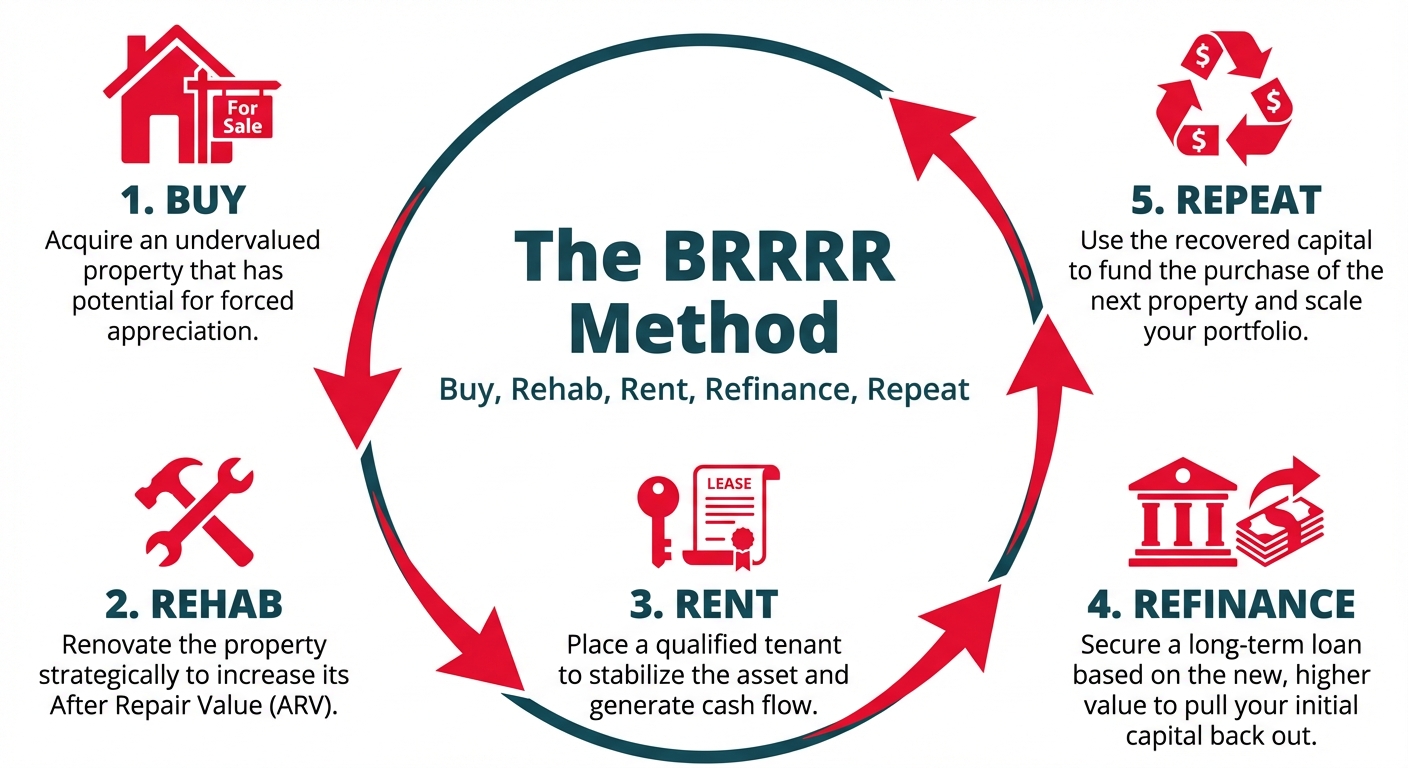

The BRRRR method is a real estate investment strategy that stands for Buy, Rehab, Rent, Refinance, Repeat. It allows investors to acquire a property, increase its value through renovations (forced appreciation), stabilize it with a tenant, and then pull their initial investment capital back out through a cash-out refinance. This capital is then used to acquire the next property, creating a repeatable system for scaling a rental portfolio. The ultimate goal is to recover 100% of the initial capital, allowing an investor to acquire a cash-flowing asset with little to no money left in the deal, achieving an infinite cash-on-cash return.

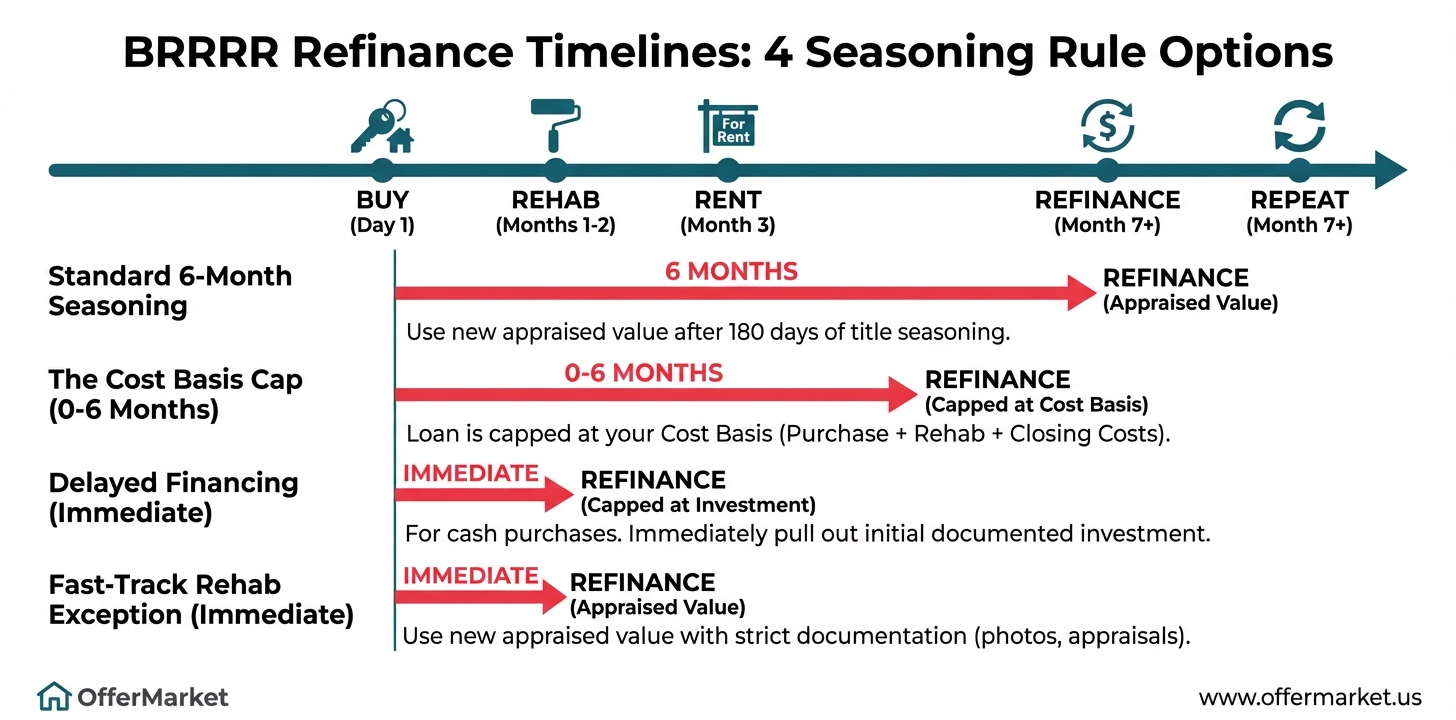

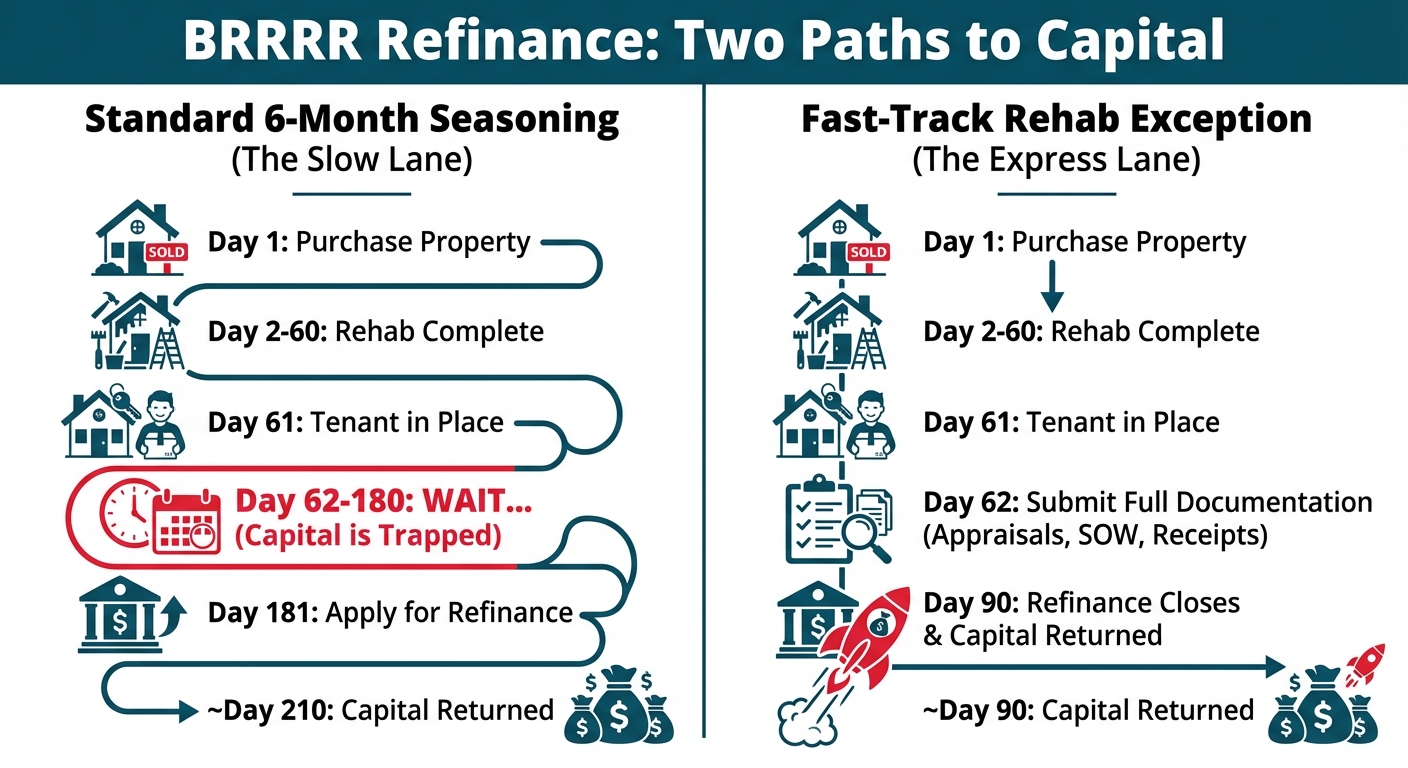

A key challenge for investors is the traditional lender requirement of a "seasoning period," typically six months, before they will allow a cash-out refinance based on the new, higher appraised value. However, a modern approach known as the Fast-Track BRRRR method utilizes a specific lending guideline—the "Delayed Financing Exception" or "Rehab Exception"—to bypass this waiting period. This exception allows investors to refinance immediately after the renovation and tenant placement are complete, drastically accelerating the velocity of their capital and the speed at which they can repeat the process and grow their portfolio. This strategy hinges on meticulous documentation and partnering with a lender that specializes in this type of financing.

The standard BRRRR strategy is powerful, but the traditional six-month seasoning requirement acts as a significant brake on an investor's growth. The Fast-Track BRRRR method is an evolution of this strategy designed to maximize capital velocity. Instead of waiting half a year for your cash to be released from a completed project, you can pull it out in as little as 60-90 days from the initial purchase, ready to be deployed into the next deal.

Bypassing the 6-month seasoning requirement to accelerate capital velocity

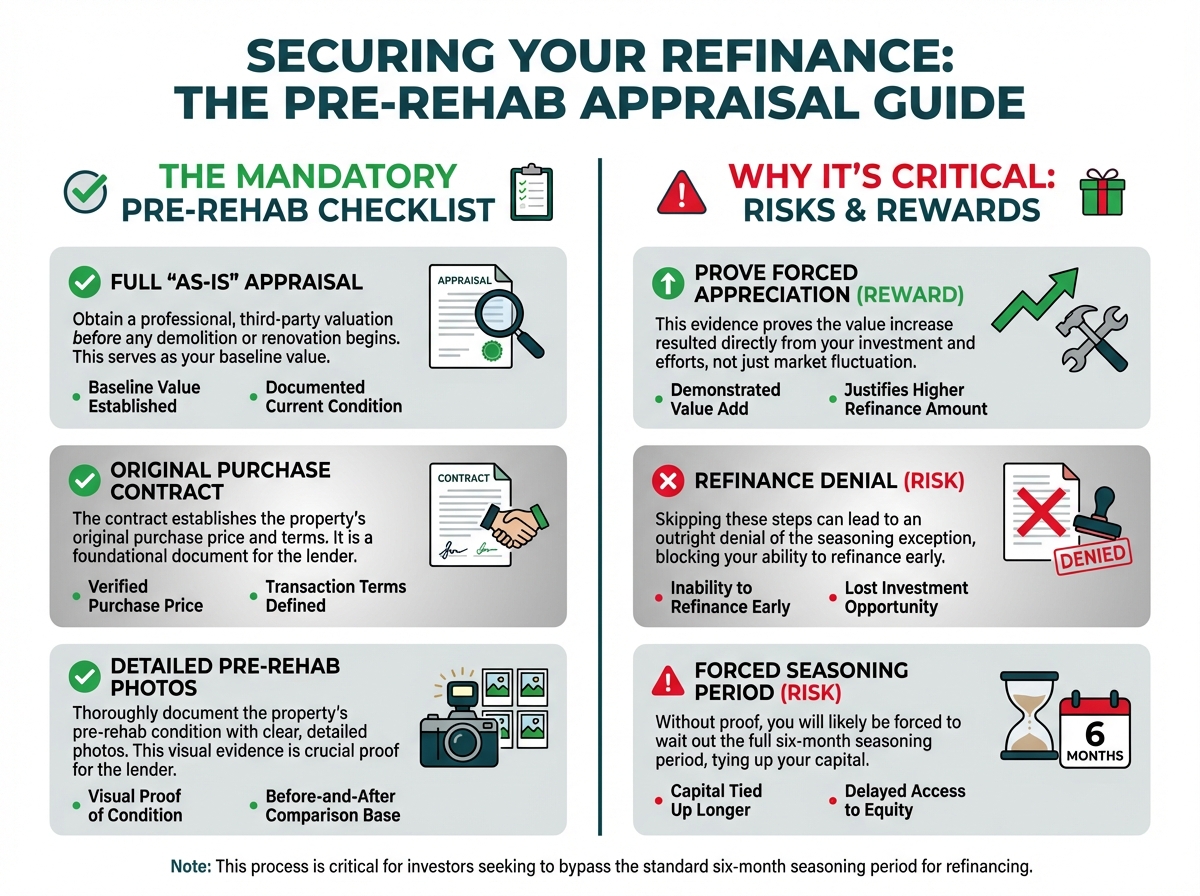

The cornerstone of the Fast-Track method is leveraging the Delayed Financing Exception, a provision within conventional lending guidelines established by Fannie Mae. While many lenders are either unaware of this rule or unwilling to implement it, specialized lenders have built processes around it. This exception allows a borrower to execute a cash-out refinance immediately after purchasing a property with cash or a short-term loan (like a hard money loan), provided certain conditions are met. The key is proving that substantial renovations were completed, which justifies the new, higher appraised value. This turns a six-month cycle into a two- or three-month cycle, potentially tripling the number of deals an investor can complete in a year with the same pool of capital.

The core principle of forcing appreciation through strategic renovations

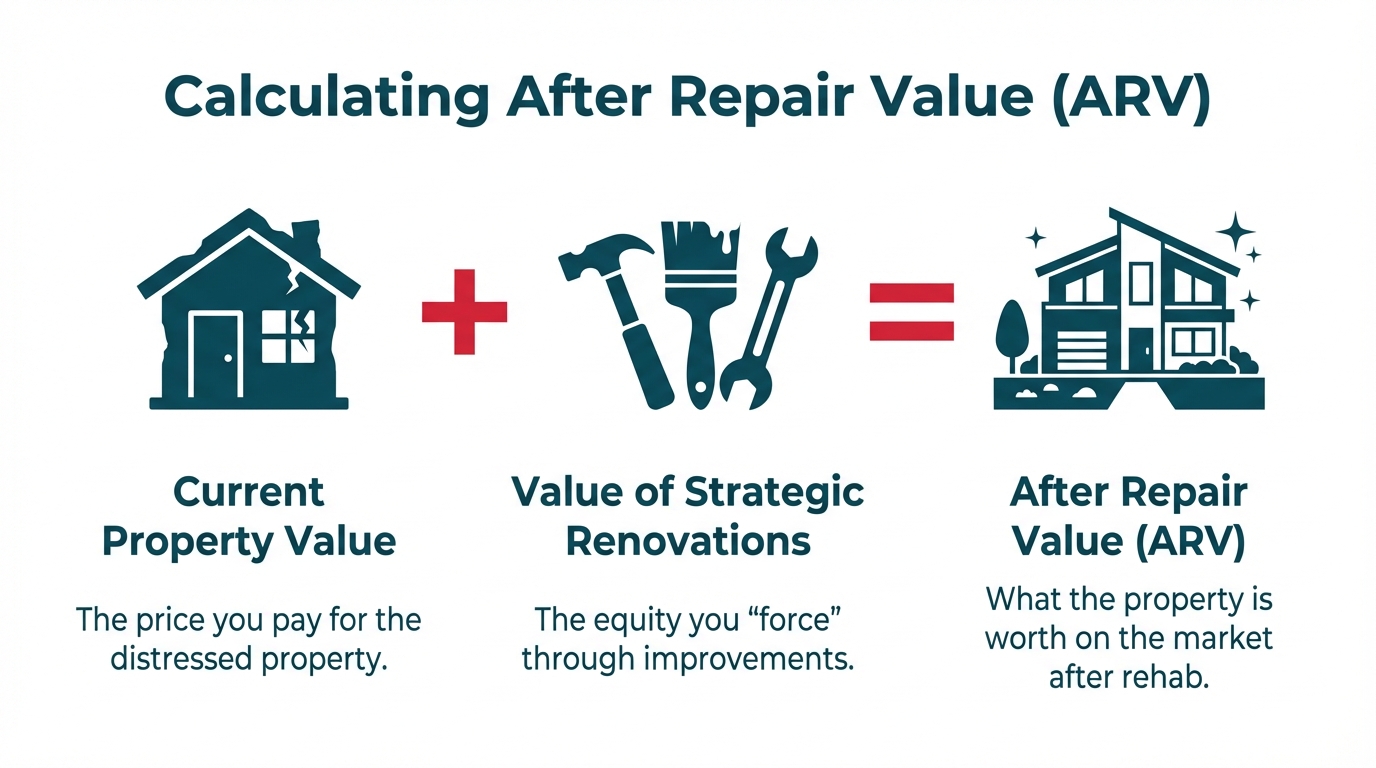

Market appreciation is passive; it happens to you. Forced appreciation is active; you create it. The BRRRR method is fundamentally about manufacturing equity. You buy a property for a price significantly below its potential future value (the After Repair Value, or ARV). The gap between the purchase price and the ARV is where you create value. By investing in strategic renovations—such as modernizing kitchens and bathrooms, improving curb appeal, or updating major systems—you are not just repairing the property; you are systematically increasing its market value. An appraiser will recognize these improvements and assign a higher value, which is the equity you will tap into during the refinance stage.

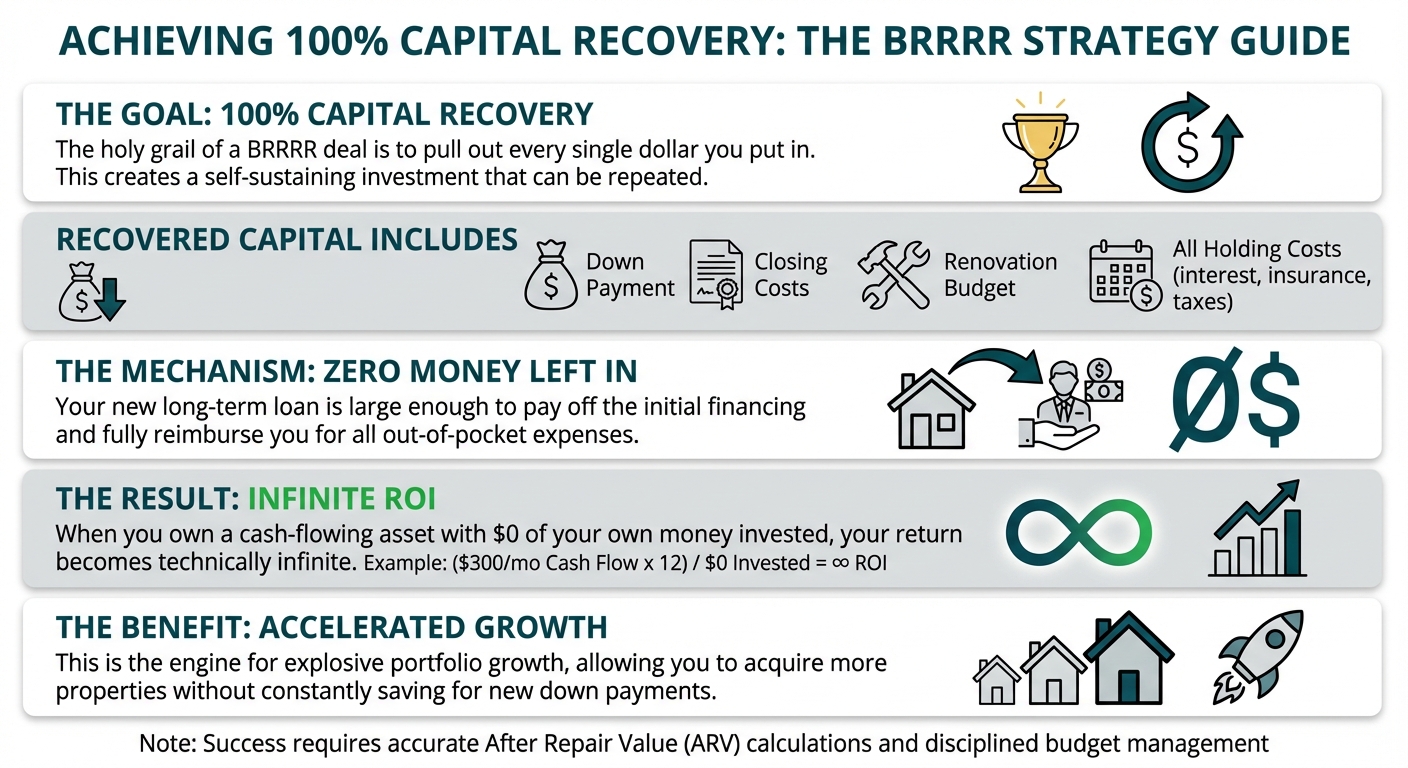

Achieving 100 percent capital recovery to enable infinite ROI

The holy grail of a BRRRR deal is to pull out every single dollar you put in. This includes your down payment, closing costs, renovation budget, and all holding costs (interest, insurance, taxes, utilities). When your new long-term loan is large enough to pay off the initial short-term loan and reimburse you for all your out-of-pocket expenses, you have achieved 100% capital recovery.

At this point, you own a cash-flowing rental property with zero of your own money invested. Your return on investment (ROI) becomes technically infinite. For example, if the property cash flows $300 per month and you have $0 of your own cash in the deal, your cash-on-cash return is ($300 * 12) / $0 = ∞. This is the mechanism that allows for explosive portfolio growth without the need to constantly save up new capital for down payments.

The critical role of specialized financing at each stage

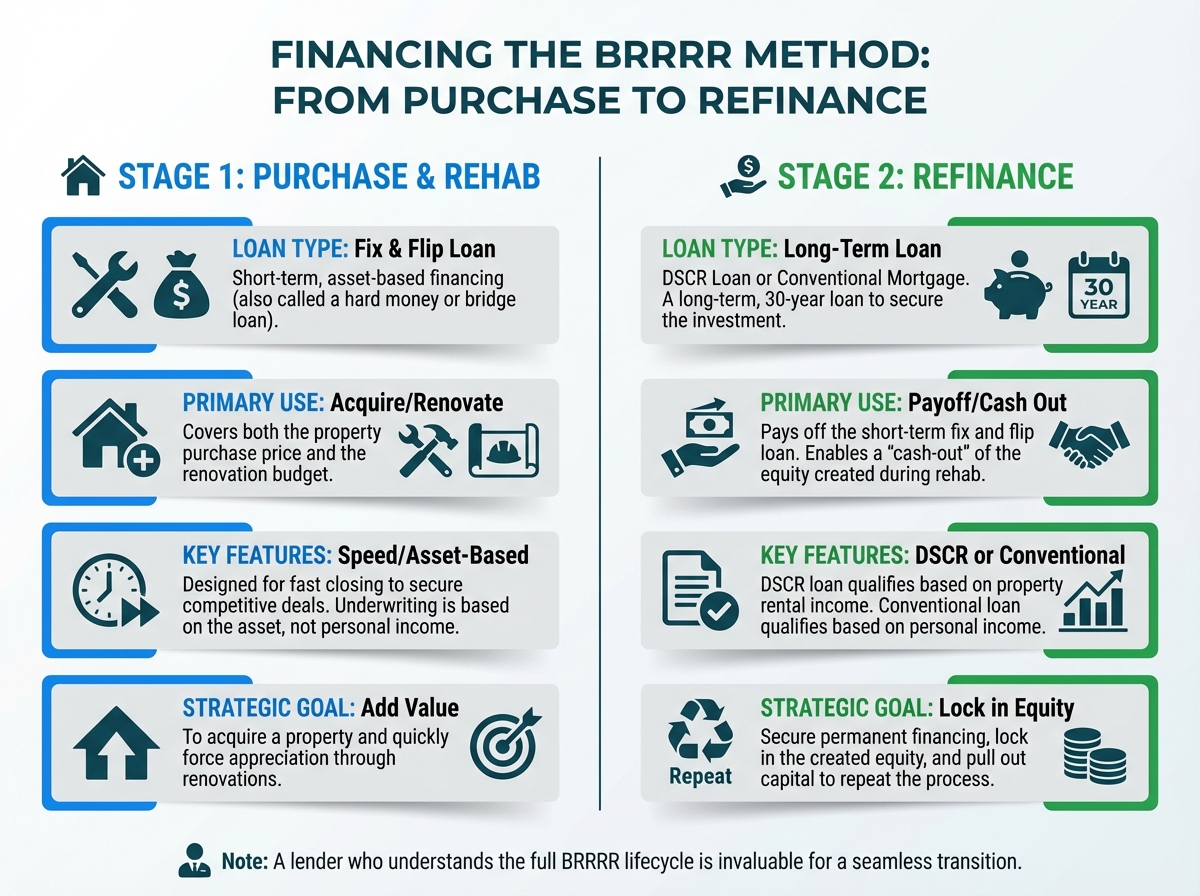

The BRRRR method is a financing strategy as much as it is an acquisition and renovation strategy. Each stage requires a specific type of financial tool:

- Purchase & Rehab: A short-term, asset-based loan is ideal here. A fix and flip loan (often called a hard money or bridge loan) is designed for this. It covers not just the purchase price but also the renovation budget, and it can be closed quickly to secure competitive deals.

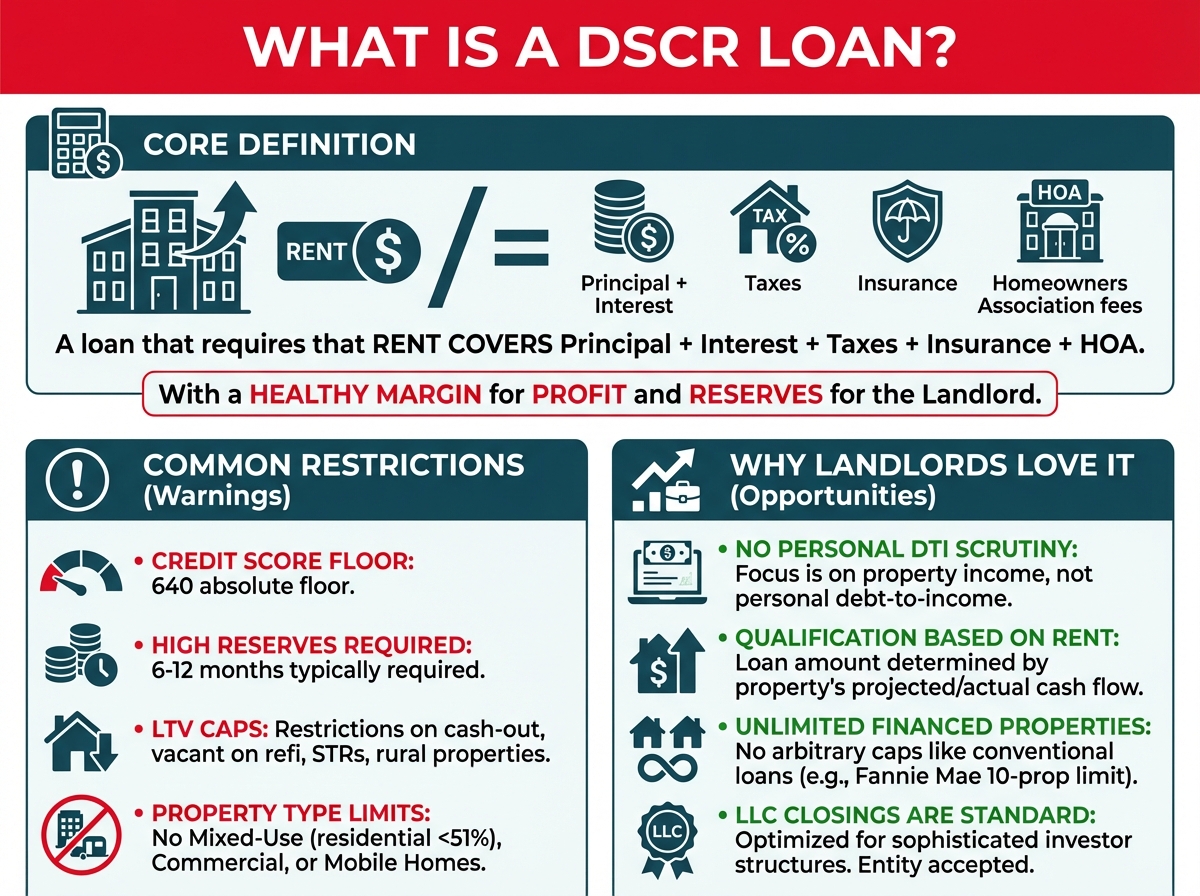

- Refinance: A long-term, 30-year loan is used to pay off the short-term debt and "cash out" the equity you created. The most common options are a DSCR (Debt Service Coverage Ratio) loan, which qualifies based on the property's rental income, or a conventional mortgage, which qualifies based on your personal income.

A lender who understands the entire BRRRR lifecycle is invaluable. They can offer a seamless transition from the short-term rehab loan to the long-term rental loan, ensuring the documentation and appraisals are handled correctly from day one to meet the requirements of the Fast-Track refinance.

Step 1: BUY - Strategic Acquisition and Financial Setup

The success of a BRRRR project is often determined before you even own the property. The "Buy" phase is about more than just finding a cheap house; it's about finding the right house at the right price and structuring the financing to set you up for a successful refinance later.

Deal analysis using the After Repair Value (ARV) formula

Every BRRRR deal begins with the end in mind. You must have a confident understanding of what the property will be worth after you've completed the renovations. This is the After Repair Value (ARV). The most common way to estimate ARV is by analyzing "comps" – comparable properties that have recently sold in the immediate vicinity (typically within a 0.5-mile radius and within the last 3-6 months).

Your analysis should focus on properties that are similar in size, age, bedroom/bathroom count, and style to what your property will be once renovated. A simplified formula is:

Subject Property Value + Value of Renovations = After Repair Value (ARV)

However, a more practical approach is to find a recently sold, fully renovated comp and adjust its sale price based on differences with your subject property. For example, if a nearby updated home sold for $300,000 but it has a garage and yours doesn't, you might adjust your ARV down by $15,000 (the approximate local value of a garage) to an estimated $285,000. This analysis is crucial because the lender for your refinance will base their loan amount on a professional appraisal of the ARV.

Sourcing undervalued properties suitable for the BRRRR model

BRRRR-able properties are not typically the turn-key, picture-perfect homes listed on the MLS. You are looking for properties with "good bones" that are cosmetically outdated, neglected, or functionally obsolete. These are properties where you can force appreciation.

- On-Market (MLS): Look for listings that have been on the market for a long time, are listed "as-is," or have descriptions that mention "TLC needed" or "investor special." An investor-friendly real estate agent can set up automated searches for these keywords.

- Wholesalers: Real estate wholesalers specialize in finding off-market deals and putting them under contract. They then sell the rights to that contract to an investor for a fee. This can be a great source of deals, but you must do your own due diligence on the numbers.

- Driving for Dollars: This old-school method involves driving through target neighborhoods and looking for signs of distressed properties (overgrown lawns, boarded-up windows, visible disrepair). You can then use public records or apps to find owner information and reach out directly.

- Auctions: Foreclosure auctions or online auction sites like Auction.com can be a source of undervalued properties, but they often require cash purchases and come with higher risk.

Financing the purchase and rehab with a short-term bridge loan

To move quickly and have the funds for both the purchase and the renovation, most BRRRR investors use short-term financing. A bridge loan or a fix and flip loan is the perfect tool for this. These loans are asset-based, meaning the lender is more concerned with the viability of the property deal than your personal income.

Key features of these loans include:

- High Leverage: Lenders often finance up to 90% of the purchase price and 100% of the renovation costs.

- Speed: They can close in a fraction of the time of a conventional loan, which is critical for competing for deals.

- Interest-Only Payments: Payments are typically interest-only, which keeps holding costs low during the renovation phase when there is no rental income.

When you apply for this loan, the lender will underwrite the deal based on your proposed renovation budget and your estimated ARV.

The Fast-Track requirement of obtaining an as-is appraisal pre-rehab

This is a non-negotiable step for the Fast-Track BRRRR method. To qualify for the Delayed Financing Exception, you must be able to prove to the new, long-term lender that you added substantial value to the property. The best way to do this is with a timeline of evidence.

Before you start any demolition or renovation, you must obtain a full "as-is" appraisal of the property. This appraisal, along with the original purchase contract and detailed photos of the property's pre-rehab condition, serves as your baseline. It's a third-party, professional valuation of the property's worth at the time you bought it. This document becomes critical evidence during the refinance stage, proving that the increase in value was a direct result of your investment and efforts, not just market fluctuation. Skipping this step can lead to a denial of the exception and force you to wait out the full six-month seasoning period.

Step 2: REHAB - Executing the Renovation for Maximum Value

The rehab phase is where you physically manufacture the equity that makes the BRRRR strategy work. It's a race against time and budget. Efficient and effective management of the renovation process is critical to protect your profit margins and keep your project on track for a quick refinance.

Developing a detailed Scope of Work (SOW) to control costs

Before the first hammer swings, you need a highly detailed Scope of Work (SOW). This document is the blueprint for your entire renovation. It should list every single task to be completed, from demolition to the final paint touch-ups, and specify the exact materials to be used (e.g., "Install 'Calacatta Laza' quartz countertops," not just "install new countertops").

A detailed SOW serves several purposes:

- Accurate Bidding: It allows you to get apples-to-apples bids from multiple contractors. Without a detailed SOW, each contractor will be bidding on their own interpretation of the project, making it impossible to compare costs effectively.

- Budget Control: It becomes your primary tool for tracking progress and expenses. You can check off completed items and ensure you're not paying for work that isn't finished or up to standard.

- Contractual Basis: The SOW should be incorporated directly into your contract with your General Contractor (GC). This makes it legally binding and reduces the likelihood of disputes over what was included in the price.

Managing contractors and navigating the construction draw process

Finding and managing reliable contractors is one of the biggest challenges for investors. Always vet contractors thoroughly by checking references, verifying licenses and insurance, and reviewing their past work.

If you are using a fix and flip loan that finances your rehab, you won't receive the renovation funds as a lump sum. Instead, the money is disbursed in "draws." The process typically works like this:

- Work Completion: Your contractor completes a portion of the work outlined in the SOW (e.g., demolition and framing).

- Draw Request: You submit a draw request to the lender, along with any required documentation like photos or receipts.

- Inspection: The lender sends an inspector to the property to verify that the work claimed on the draw request has been completed satisfactorily.

- Funds Released: Once the inspection is approved, the lender releases the funds for that portion of the work, either to you or directly to the contractor.

This process protects both you and the lender, ensuring that money is only paid out for work that has actually been done. It's crucial to understand your lender's specific draw process and timeline to manage your contractor's payment expectations and keep the project moving smoothly.

The importance of documenting all expenses for cost basis verification

Meticulous record-keeping is not just good business practice; it's essential for both your lender and the IRS. For the Fast-Track refinance, your new lender will want to see proof of the funds you invested in the renovation. This helps them justify the new loan amount and verify that the value was indeed added through substantial improvements.

Keep a detailed spreadsheet of every single expense, and save every receipt and invoice in a dedicated digital folder. This includes:

- Contractor payments

- Material purchases from stores like Home Depot or Lowe's

- Permit fees

- Architectural or engineering fees

- Dumpster rentals

This documentation also establishes your property's "cost basis" for tax purposes. Your cost basis is the original purchase price plus all the capital improvements you made. When you eventually sell the property, your capital gain will be calculated as the sale price minus the cost basis. A higher, well-documented cost basis means a lower taxable gain.

Focusing renovations on items that yield the highest appraisal value

Not all renovation dollars are created equal. Some improvements add significantly more value in an appraiser's eyes than others. While you want the property to be attractive to tenants, your primary goal during the rehab is to maximize the appraised value. Focus your budget on the "money rooms" and high-impact items:

- Kitchens: This is almost always the highest ROI renovation. Modern cabinets, quartz or granite countertops, a tile backsplash, and a new set of stainless steel appliances can dramatically increase value.

- Bathrooms: Updated vanities, modern tile in the shower and on the floor, and new fixtures can transform a dated bathroom and command a higher appraisal.

- Curb Appeal: The first impression matters. A new front door, fresh exterior paint, updated landscaping, and modern light fixtures can significantly boost perceived value.

- Flooring: Replacing old, worn carpet with durable and attractive Luxury Vinyl Plank (LVP) or refinishing hardwood floors provides a clean, cohesive look throughout the house that tenants and appraisers love.

- Paint: A fresh coat of neutral paint (like greige or a soft white) is one of the cheapest ways to make a property feel clean, bright, and new.

Avoid over-improving for the neighborhood or spending on lavish personal preferences that don't have a broad appeal or a proven ROI. The goal is a clean, modern, and durable rental property that appraises for top dollar.

Step 3: RENT - Asset Stabilization and Cash Flow Generation

Once the dust has settled from the renovation, your focus shifts to converting the property from a construction site into a stabilized, income-producing asset. This phase is the bridge between the short-term rehab loan and the long-term refinance. Getting it right is absolutely critical, especially for a DSCR loan exit.

The critical need for a signed 12-month lease for DSCR financing

For investors planning to use a DSCR loan for their refinance, this is the single most important part of the "Rent" phase. A DSCR loan's underwriting is based almost entirely on the property's ability to generate enough income to cover its debt obligations. The lender needs proof of this income.

A signed 12-month lease with a qualified tenant is the primary evidence. It's not enough to have a projection of what the property could rent for. The lender needs to see a legally binding agreement that locks in a specific monthly income for the next year. Without this executed lease, the DSCR loan application cannot proceed. This is why it's essential to begin marketing the property for rent as soon as the rehab is nearing completion.

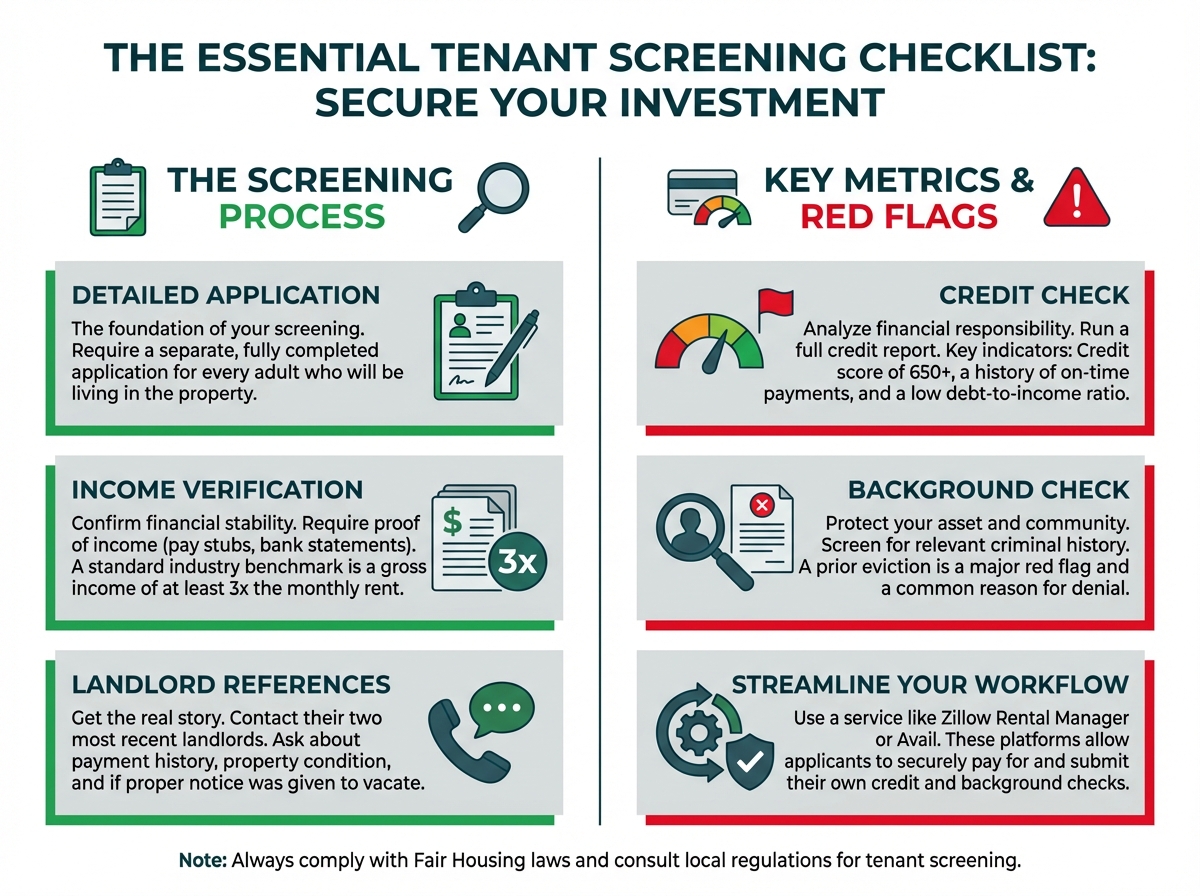

Effective tenant screening to secure a reliable income stream

The quality of your tenant determines the quality of your investment. A great tenant pays on time, takes care of the property, and makes your life as a landlord easy. A bad tenant can cause costly damage, require an expensive eviction, and turn your cash-flowing asset into a money pit.

A rigorous tenant screening process is your best defense. Don't cut corners. Your process should include:

- Application: A detailed application form for every adult who will be living in the property.

- Credit Check: Run a full credit report. Look for a history of on-time payments, a low debt-to-income ratio, and a credit score that meets your minimum criteria (e.g., 650+).

- Background Check: Screen for any relevant criminal history or past evictions. A prior eviction is a major red flag.

- Income Verification: Require proof of income (pay stubs, bank statements, or offer letters) showing that the applicant earns at least 3 times the monthly rent. This is a standard industry benchmark.

- Landlord References: Call their previous two landlords. Ask specific questions: Did they pay rent on time? Did they give proper notice to vacate? Did they leave the property in good condition?

Using a service like Zillow Rental Manager or Avail can streamline this process by allowing applicants to pay for and submit their own credit and background checks.

Proving cash flow with security deposits and first month rent receipts

In addition to the signed lease, the DSCR lender will need to see proof that the tenancy has officially begun and funds have been exchanged. This is called "seasoning the lease." You will typically be required to provide:

- Proof of Security Deposit: A copy of the cleared check or a bank statement showing the electronic transfer of the security deposit from the tenant to you.

- Proof of First Month's Rent: Similar proof showing that the first month's rent has been paid and received.

These documents prove that the lease is not just a piece of paper but an active agreement with a real, paying tenant. This gives the lender the confidence they need to approve the loan based on that income stream.

Why Short-Term Rentals (STRs) are incompatible with the Fast-Track strategy

While short-term rentals (like Airbnb or VRBO) can be a lucrative strategy, they generally do not work for the Fast-Track BRRRR refinance, particularly with DSCR loans. DSCR lenders underwrite based on stable, long-term income. The fluctuating, seasonal nature of STR income is considered too volatile and unpredictable.

The core requirement is a 12-month lease. An STR, by definition, does not have this. Therefore, if your exit strategy is a DSCR loan, you must secure a long-term tenant. Some investors may choose to operate the property as an STR after completing a conventional cash-out refinance (which is based on personal income), but it cannot be the basis for the initial refinance itself.

Step 4: REFINANCE - The Fast-Track Capital Extraction

This is the step where all your hard work pays off. The refinance is the mechanism that allows you to pull out the equity you've created, pay off your expensive short-term debt, and recoup your initial investment. Executing this step quickly and efficiently is the essence of the Fast-Track BRRRR method.

Understanding the standard 6-month refinance seasoning rule

Most conventional lenders and many portfolio lenders adhere to a strict "seasoning" rule. This rule dictates that a property's title must be "seasoned"—meaning owned by the current borrower—for a minimum period, typically six months (and sometimes up to a year), before the lender will consider a cash-out refinance based on a new, appraised value.

The rationale behind this rule is to prevent loan fraud and to mitigate risk from rapid, speculative property flipping. Lenders want to see a period of stable ownership before they will lend against a value that is significantly higher than the recent purchase price. For a BRRRR investor, this rule is a major bottleneck, tying up capital for half a year and slowing down portfolio growth.

Executing the Rehab Exception to bypass the seasoning period

The "Rehab Exception," officially known as the Delayed Financing Exception, is the key to unlocking the Fast-Track. This is a specific guideline that allows a borrower to bypass the six-month seasoning rule if they meet a strict set of criteria.

The core premise is that the borrower initially purchased the property with cash or a short-term loan (that did not finance the rehab), and the subsequent loan transaction is being used to recoup the purchase price and documented renovation costs. A lender specializing in BRRRR financing, like OfferMarket, will have a process specifically designed to accommodate this. They understand that the higher value is not due to market speculation but to documented, substantial improvements made to the property. By leveraging this exception, you can initiate your cash-out refinance as soon as the rehab is complete and the property is rented, collapsing the timeline from six months to as little as 60 days.

Meeting the strict documentation and secondary valuation review requirements

To successfully use the Rehab Exception, you must provide the lender with an airtight case file. The burden of proof is on you to demonstrate that you manufactured the new value. The required documentation typically includes:

- Original Purchase HUD-1/Settlement Statement: Proves the initial purchase price and date.

- "As-Is" Pre-Rehab Appraisal: The third-party valuation of the property before you touched it.

- Before and After Photos: A comprehensive visual record of the transformation.

- Detailed Scope of Work (SOW): The blueprint for your renovation.

- Proof of Rehab Expenses: All receipts, invoices, and contractor payments that add up to your total renovation cost.

- Executed 12-Month Lease: Proof of stabilization and income.

- New "As-Repaired" Appraisal: The new appraisal showing the post-rehab value (ARV).

Even with all this, the file will undergo a secondary valuation review. The lender will run the new appraisal through an automated system, like the Fannie Mae Collateral Underwriter (CU) or a Collateral Desktop Analysis (CDA) from a third party like Clear Capital. These systems use big data and algorithms to assess the credibility of the appraisal. If the appraisal gets a low score (e.g., a CU score of 4 or 5), it indicates a higher risk, and the lender may require a second appraisal or reduce the loan-to-value (LTV) they are willing to offer.

Choosing the optimal long-term loan: DSCR vs. Conventional

Once you're cleared for the refinance, you have two primary loan options for your long-term hold:

DSCR Loan: This is a business-purpose loan designed for real estate investors.

- Pros: Qualification is based on the property's cash flow, not your personal W-2 income. This is ideal for self-employed investors or those with many existing mortgages. They also allow you to close in an LLC for asset protection.

- Cons: Interest rates are typically 1-2% higher than conventional loans.

- Best for: Investors who are scaling, self-employed, or want to keep their personal finances separate from their investments.

Conventional Loan: This is the standard mortgage you would get for a primary residence, but used for an investment property.

- Pros: Generally offers the lowest interest rates and best terms available.

- Cons: Qualification is based on your personal Debt-to-Income (DTI) ratio, requiring W-2s, tax returns, and extensive income verification. There's a limit (typically 10) on the number of financed properties you can have. You must close in your personal name.

The choice depends on your personal financial situation and your long-term goals. For rapid scaling, the DSCR loan is often the superior tool because your ability to qualify is not limited by your personal income.

A Deeper Dive into The Rehab Exception

Successfully navigating the Rehab Exception is what separates a good BRRRR investor from a great one. It requires a forensic level of documentation and a clear understanding of what the lender's underwriter needs to see to approve the loan and bypass the seasoning period. Let's break down the critical components.

Required evidence: Original listing photos and pre-rehab appraisal

The foundation of your case is establishing a clear "before" picture. You need to prove, beyond any doubt, the property's condition at the moment of purchase.

- Original Listing Photos: Before you close, download and save all the photos from the original real estate listing (MLS, Zillow, etc.). These photos, created by a third party (the seller's agent), provide an unbiased view of the property's initial state.

- Pre-Rehab Appraisal: As mentioned in Step 1, this is the most crucial piece of evidence. It's a formal, licensed appraiser's opinion of the property's value before any of your work began. This "as-is" appraisal, dated at or near the time of your purchase, serves as the official starting line. When the new appraisal comes in much higher, the "as-is" appraisal proves the value was not there to begin with.

Together, these documents create a timeline. They show the lender: "Here is what I bought, as verified by the listing agent and a licensed appraiser, and here is the price I paid for it."

The role of the new post-rehab appraisal in establishing value

After the renovation is complete and the tenant is in place, your refinance lender will order a new appraisal. This appraiser's job is to determine the current market value of the property in its newly renovated condition—the After Repair Value (ARV).

The appraiser will:

- Physically inspect the property: They will walk through the entire house, noting the quality of the finishes, the scope of the updates, and the overall condition.

- Select comparable sales ("comps"): They will find recently sold properties in the immediate area that are most similar to your renovated property. This is why your rehab quality must match or exceed the local market standard.

- Make adjustments: They will adjust the sale prices of the comps to account for differences between them and your property (e.g., +$5,000 for your superior kitchen, -$10,000 for their extra half-bath).

- Arrive at a final value: Based on this analysis, they will provide a final opinion of value, which will be the basis for your new loan amount.

Your loan amount will be a percentage of this new appraised value (the Loan-to-Value, or LTV), typically up to 75% or 80%.

Passing secondary valuation with a Clear Capital CDA or FNMA CU score

The appraisal is a human opinion of value, and lenders need a way to check that opinion against objective data. This is where secondary valuation tools come in.

- Fannie Mae Collateral Underwriter (CU): For conventional loans, the appraisal is automatically submitted to this powerful tool. CU uses a massive database of appraisals and property data to assign a risk score from 1 (lowest risk) to 5 (highest risk). A score of 1, 2, or 2.5 is generally considered good and the appraisal is accepted. A score of 4 or 5 is a major red flag, suggesting the appraised value may be inflated, and will trigger a manual review or a request for a new appraisal.

- Collateral Desktop Analysis (CDA): For non-conventional loans like DSCR, lenders often use a third-party service like Clear Capital to perform a CDA. A human reviewer, often another appraiser, will review the original appraisal report from their desk, checking the logic, the chosen comps, and the adjustments. They will then issue a report either concurring with the value or raising concerns.

To pass these reviews, the appraisal must be well-supported with relevant, recent, and geographically close comps. An appraiser who uses comps from a different neighborhood or that sold nine months ago is setting the loan up for failure in the secondary review.

Understanding the potential 5 percent LTV penalty for this exception

Because bypassing the seasoning period carries a slightly higher risk for the lender, some may impose a small penalty on the Loan-to-Value (LTV). For example, if their standard cash-out refinance LTV is 80%, they might cap a Rehab Exception loan at 75%.

This 5% reduction means you'll be able to pull out slightly less cash. It's crucial to factor this potential penalty into your initial deal analysis. If your numbers only work at 80% LTV, the deal is too thin. You need to ensure your project will be profitable and you can still pull out all your capital even if you're limited to a 75% LTV on the refinance. A conservative investor always plans for the lower LTV and is pleasantly surprised if they get the higher one.

Step 5: REPEAT - Scaling Your Portfolio Systematically

The final "R" in BRRRR is what transforms it from a single successful project into a wealth-building engine. The "Repeat" phase is about taking the capital and the lessons learned from the completed deal and immediately deploying them into the next one, creating a compounding effect on your portfolio growth.

Using cash-out proceeds to fund subsequent acquisitions

The cash-out refinance provides you with a lump sum of tax-free cash (since it's loan proceeds, not income). This capital is the lifeblood of your scaling operation. A successful BRRRR deal should return all of your initial investment plus, in some cases, a little extra. This recovered capital becomes the down payment and rehab fund for your next project.

For example:

- Deal 1: You invest $80,000 total. After refinance, you receive an $80,000 check.

- Deal 2: You use that same $80,000 to purchase and rehab the next property.

- Result: You now own two cash-flowing rental properties, but you are still only using your original $80,000 pool of capital.

This is how investors can acquire a multi-million dollar portfolio in a matter of years, rather than decades, because they are not constrained by the slow process of saving up a new 20-25% down payment for each property.

Satisfying lender cash reserve requirements from loan proceeds

When you apply for a long-term loan (both conventional and DSCR), lenders require you to have "cash reserves." This is liquid cash available to cover the property's expenses (principal, interest, taxes, and insurance - PITI) for a certain number of months in case of a vacancy or unexpected repairs. The standard requirement is typically 6 months of PITI.

A huge advantage of the cash-out refinance is that you can often use the proceeds from the loan itself to satisfy this requirement. For example, if your PITI is $1,500/month, you'll need $9,000 in reserves. If you are receiving $80,000 from the cash-out, you simply need to show that $9,000 of it is being held in your bank account after closing. You don't need to bring new, separate cash to the table. This makes scaling much more efficient, as your reserves for one property are funded by the equity of another.

Leveraging an experienced investor track record for better loan terms

Lenders love experienced borrowers. An investor who has successfully completed one or two BRRRR deals is seen as a much lower risk than a complete novice. As you build your track record, you'll find that you can secure better financing terms.

This can manifest in several ways:

- Higher Leverage: A lender might offer you 80% LTV on a refinance instead of 75%.

- Lower Interest Rates: You may qualify for a lower interest rate, which improves your cash flow.

- Lower Fees: Origination fees and other lender charges may be reduced.

- Faster Processing: As a known and trusted client, your loan applications may be processed more quickly.

It's crucial to document every deal meticulously. Create a portfolio summary that lists your properties, purchase prices, rehab costs, and final appraised values. This professional presentation of your track record will be a powerful tool in negotiating your next loan.

Building a scalable operational system for multiple projects

Repeating the BRRRR process once or twice can be done with brute force. Scaling to 5, 10, or 20+ properties requires systems. You cannot be the bottleneck in your own business. You need to build a machine that can handle multiple projects simultaneously.

This involves:

- Standardizing Your Rehab: Develop a standard set of materials and finishes for all your properties (e.g., the same LVP flooring, paint color, and kitchen cabinets). This simplifies purchasing, reduces decision fatigue, and makes maintenance easier.

- Building a Reliable Team: You need a go-to real estate agent, contractor, lender, and property manager who understand your strategy and can work efficiently without constant supervision.

- Automating Processes: Use software for project management (like Trello or Asana), property management (like Buildium or AppFolio), and bookkeeping (like QuickBooks).

- Creating Checklists: Develop detailed checklists for every phase of the process, from deal analysis to tenant move-in. This ensures no critical step is missed, especially when you're juggling multiple projects.

The goal is to transition from being an active participant in every task to being the CEO of your real estate business, overseeing the system rather than doing all the work yourself.

The Core Financials of a BRRRR Deal

The BRRRR method is a numbers game. Your success hinges on accurate analysis and conservative underwriting before you ever make an offer. Understanding these core calculations is non-negotiable.

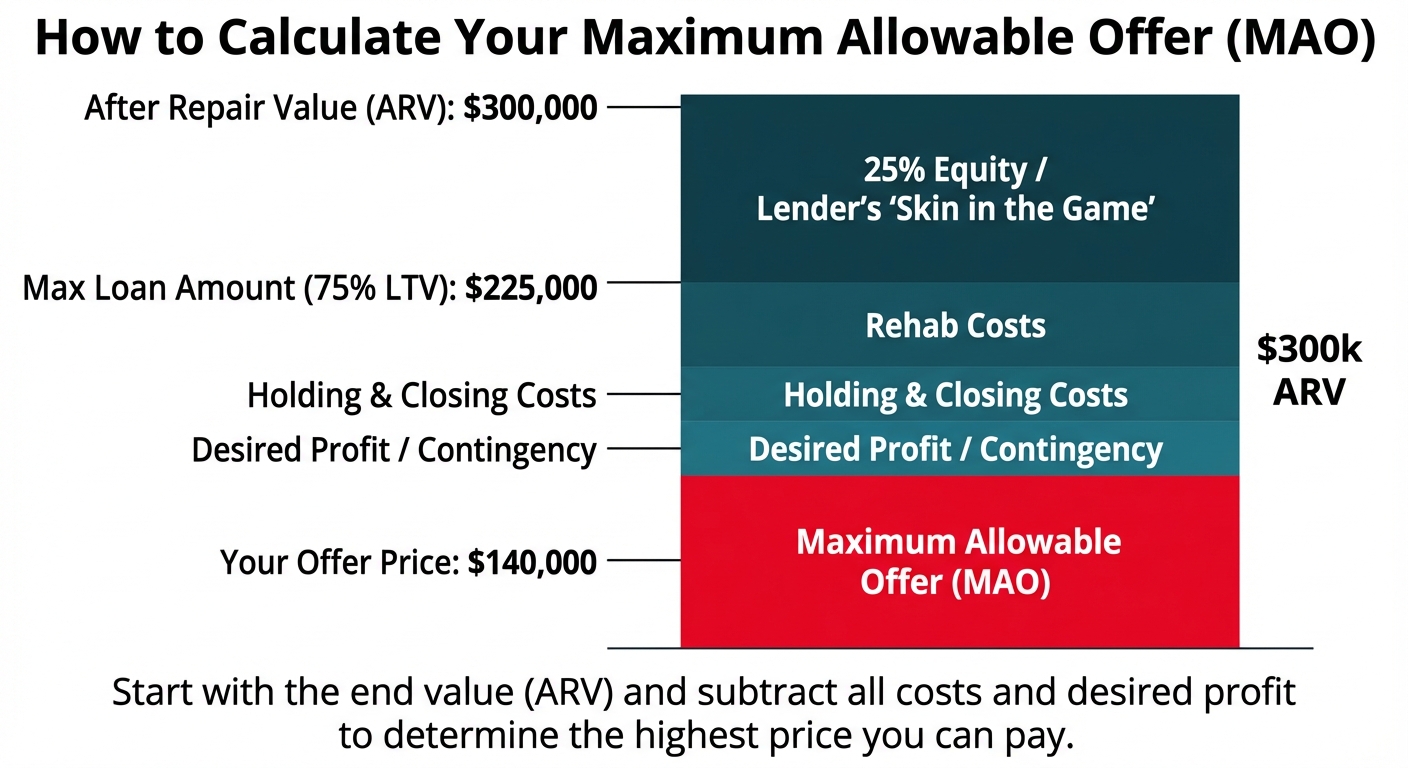

Calculating Maximum Allowable Offer (MAO) to ensure profitability

The most common mistake new investors make is overpaying for a property. The Maximum Allowable Offer (MAO) is a formula that forces you to start with the end goal in mind and work backward to determine the highest price you can possibly pay.

The formula is: MAO = (ARV x Max LTV) - Rehab Costs - Closing/Holding Costs - Desired Profit/Contingency

Let's break it down with an example:

- After Repair Value (ARV): You've done your comps and are confident the property will be worth $300,000 after rehab.

- Max LTV: Your refinance lender will give you a loan for 75% of the ARV. ($300,000 * 0.75 = $225,000)

- Rehab Costs: Your detailed SOW estimates the renovation will cost $50,000.

- Closing/Holding Costs: Estimate about $15,000 for closing costs (on purchase and refi), loan interest, insurance, taxes, and utilities during the project.

- Desired Profit/Contingency: You want to build in a $20,000 buffer for unexpected issues or to ensure you pull out some extra cash.

MAO = $225,000 - $50,000 - $15,000 - $20,000 = $140,000

This means $140,000 is the absolute highest price you can offer on this property to achieve your goals. If you pay more, you will be forced to leave cash in the deal. Sticking to your MAO is the ultimate form of discipline.

Projecting total project costs including purchase, rehab, and holding costs

Your "all-in" number is more than just the purchase price and rehab budget. You must account for all the "soft costs" that accumulate during the project.

- Purchase Costs: Down payment + Lender fees + Appraisal + Inspection + Title/Escrow fees.

- Rehab Costs: Your entire SOW budget, including a 10-15% contingency fund for overruns.

- Holding Costs:

- Loan Interest: Monthly payments on your short-term loan.

- Insurance: Builder's risk policy during rehab, then a landlord policy.

- Taxes: Prorated property taxes.

- Utilities: Water, electric, gas during the rehab period.

- Refinance Costs: Lender fees + Appraisal + Title/Escrow fees for the new loan.

- Leasing Costs: Any fees for marketing the property or tenant screening services.

Failing to account for these holding costs can erode your profit and is a common reason why investors end up leaving more money in a deal than they planned.

Calculating the Debt Service Coverage Ratio (DSCR) for the refinance

If you're using a DSCR loan, this is the most important metric. It measures the property's ability to pay its own bills.

The formula is: DSCR = Gross Monthly Rent / Monthly PITI (PITI = Principal, Interest, Taxes, Insurance)

Lenders have a minimum DSCR they require, typically 1.20x or higher. This means the rent must be at least 20% greater than the total monthly housing payment.

Example:

- Gross Monthly Rent: $2,500

- Monthly PITI:

- Principal & Interest: $1,400

- Taxes: $300

- Insurance: $100

- Total PITI: $1,800

DSCR = $2,500 / $1,800 = 1.39x

Since 1.39 is greater than the 1.20 minimum, this property's cash flow would qualify for the DSCR loan. If the rent was only $2,100, the DSCR would be 1.16x, and the loan would be denied on a cash flow basis. You must analyze your projected rents and PITI to ensure your DSCR will be well above the lender's minimum threshold.

Analyzing the deal for true infinite return potential

A "true" BRRRR is one where you pull out 100% (or more) of your invested capital. To analyze this, you need to compare your total cash invested with the total cash you will receive from the refinance.

- Total Cash Invested: Down payment + All rehab costs paid out of pocket + All holding/closing costs paid out of pocket.

- Total Cash Returned: (New Loan Amount) - (Payoff of Short-Term Loan).

If Cash Returned ≥ Cash Invested, you have achieved an infinite return. You own a cash-flowing asset with $0 of your own money left in it. Any positive cash flow from this point forward is an infinite percentage return on your $0 investment. This is the ultimate goal of the BRRRR method.

Analyze Your Next Deal With Our BRRRR Calculator

Running these numbers manually can be complex. To streamline your deal analysis and ensure you don't miss any critical variables, use a dedicated tool. Analyze your next deal with our free DSCR Calculator to quickly project your costs, estimate your cash-out potential, and determine if a property meets the criteria for a successful BRRRR.

Strategic Advantages of the BRRRR Method

Investors are drawn to the BRRRR method because it offers a unique combination of benefits that are difficult to achieve with other real estate strategies. When executed correctly, it's a powerful engine for building wealth.

Potential for infinite Cash-on-Cash Return by pulling all capital out

This is the most celebrated benefit of the BRRRR method. Cash-on-Cash (CoC) Return is a standard metric calculated as: (Annual Pre-Tax Cash Flow) / (Total Cash Invested).

In a typical rental purchase where you put 25% down, your CoC return might be 8-12%. For example, if you invest $50,000 to get a $400/month ($4,800/year) cash flow, your CoC is 9.6%. In a successful BRRRR deal, your "Total Cash Invested" at the end of the project is $0. When you divide the annual cash flow by $0, the result is a mathematically infinite return. While you still have a loan and risks, the fact that you have a cash-producing asset without any of your own capital tied up in it is a uniquely powerful position.

Rapid portfolio growth without saving for new down payments

The single biggest obstacle to scaling a real estate portfolio is the down payment. Saving up $50,000, $60,000, or more for a 25% down payment on a new rental property can take the average person years. The BRRRR method shatters this limitation. Because you are recycling the same pool of capital over and over again, your growth is limited only by your ability to find good deals and manage projects, not by your ability to save money from a W-2 job. An investor with $100,000 in capital could potentially acquire 3-4 properties in a single year, whereas a traditional investor might only acquire one every 2-3 years.

Building equity through forced appreciation not just market movement

Many real estate investment strategies are passive, relying on market appreciation over time to build equity. This is hoping for growth. The BRRRR method is active; it's manufacturing growth. You are not waiting for the market to give you equity; you are creating it with a sledgehammer and a spreadsheet. This "forced appreciation" provides a significant equity cushion from day one. If the market goes flat or even dips slightly after your project is complete, you still have the equity you created through the renovation, making the investment far more resilient to market fluctuations than a turnkey rental purchased at full market value.

No personal income verification required for DSCR loan exits

For many entrepreneurs, small business owners, and professional real estate investors, qualifying for a conventional mortgage is a nightmare of paperwork and strict debt-to-income (DTI) requirements. The rise of the DSCR loan as the preferred exit for BRRRR investors has been a game-changer. Because the loan is underwritten based on the property's income potential, the lender is not concerned with your personal tax returns or W-2s. As long as the property's rent covers the mortgage payment (plus taxes and insurance) by a sufficient margin (the DSCR), you can be approved. This allows investors to scale their portfolio based on the quality of their deals, not the constraints of their personal income documentation.

Inherent Risks and How to Mitigate Them

While the BRRRR method is powerful, it is not without significant risks. It is an advanced strategy with many moving parts, and a failure in any one phase can jeopardize the entire project. Understanding these risks and planning for them is critical.

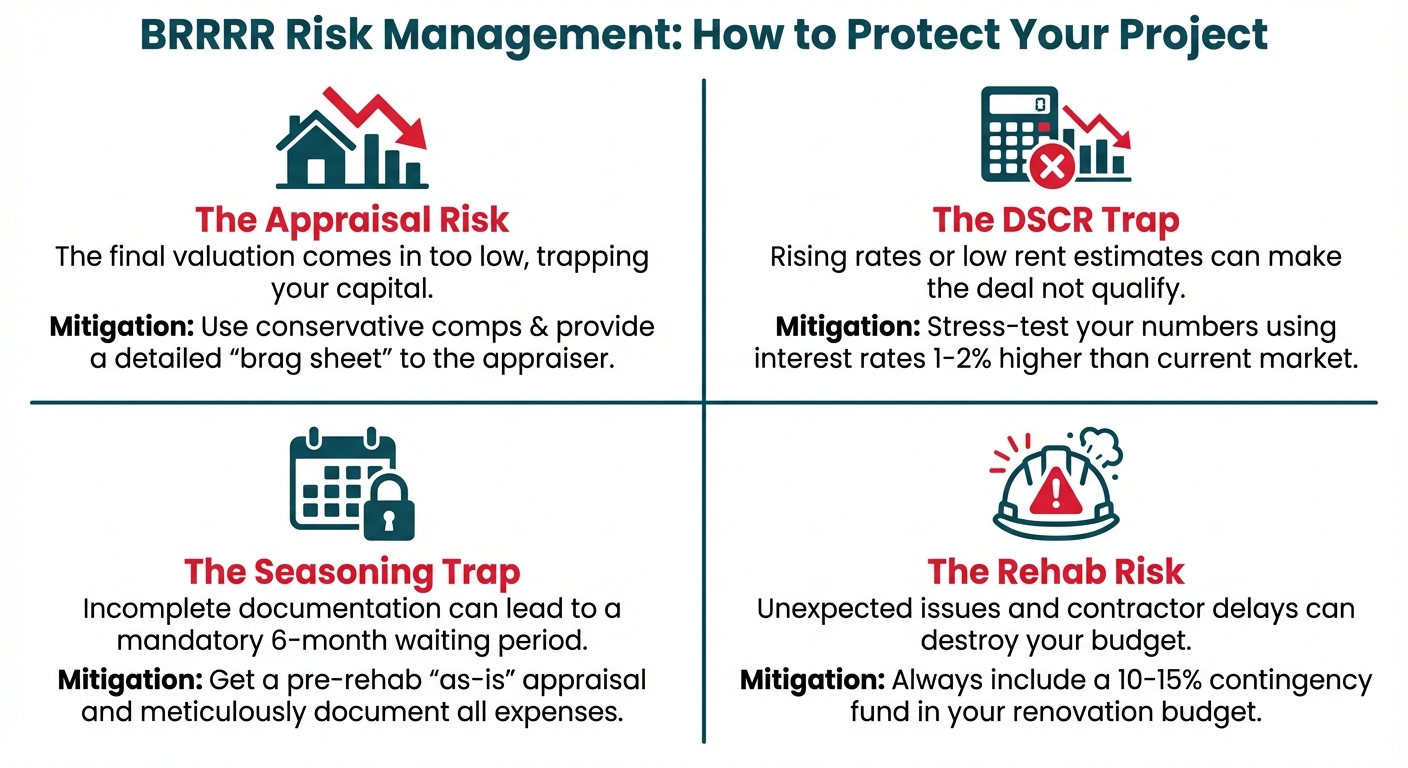

The Appraisal Risk: The final value comes in too low

This is the most terrifying risk for a BRRRR investor. You can do everything right—buy at a great price, execute a flawless renovation—but if the final appraisal comes in lower than your projected ARV, your entire financial model collapses. A low appraisal means the lender will offer a smaller loan, and you will not be able to pull out all of your capital, potentially leaving tens of thousands of dollars trapped in the deal.

- Mitigation:

- Conservative Comps: When calculating your ARV, be brutally honest. Use only the most relevant, recent, and geographically close comps. Never stretch for a higher value.

- Know Your Appraisers: Work with lenders who use a panel of local, investor-savvy appraisers who understand renovated properties.

- Provide a "Brag Sheet": Give the appraiser a packet of information including the SOW, a list of all improvements with costs, before-and-after photos, and the comps you used for your own analysis. This helps them understand the full scope of the transformation.

- Have a Contingency: Always have a backup plan. Can you afford to leave $10,000 or $20,000 in the deal if you have to? If not, the deal is too risky.

The DSCR Trap: Rising rates or low rent estimates kill cash flow

Your DSCR calculation is based on two variables: rent and PITI. If either one goes in the wrong direction, your deal may no longer qualify for a refinance.

Rising Rates: The interest rate environment can change between the time you buy the property and the time you refinance. A 1% increase in the interest rate can significantly raise your monthly PITI, potentially pushing your DSCR below the lender's minimum.

Low Rent Estimates: You may project a rent of $2,000/month, but if the rental market softens and you can only secure a tenant for $1,800, your DSCR will suffer.

Mitigation:

- Stress Test Your Numbers: When analyzing a deal, calculate your DSCR using an interest rate that is 1-2% higher than current rates. If the deal still works, it's robust.

- Conservative Rent Estimates: Base your rent projections on actual, current listings for comparable properties, not optimistic hopes. It's better to be pleasantly surprised than disappointed.

- Lock Your Rate: As soon as you are able, lock in the interest rate on your refinance to protect against market volatility.

The Seasoning Trap: Failing to meet documentation for the Rehab Exception

The Fast-Track BRRRR is entirely dependent on your ability to qualify for the Rehab Exception. If your documentation is sloppy or incomplete, the lender will deny the exception and force you to wait the full six months. This can cause a major liquidity crisis if you were counting on getting that capital back quickly to pay off high-interest debt or fund your next deal.

- Mitigation:

- Create a Documentation Checklist: From day one, have a checklist of every single document you will need for the refinance.

- Get the "As-Is" Appraisal: Do not start any work before you have the pre-rehab appraisal in hand.

- Save Everything: Create a dedicated digital folder for each project and save every photo, receipt, contract, and statement. Back it up to the cloud. There is no such thing as too much documentation.

The Rehab Risk: Budget overruns and contractor delays

Renovations rarely go exactly as planned. You might open a wall and discover unexpected termite damage, your contractor might get delayed on another job, or the cost of lumber could suddenly spike. Budget overruns and delays increase your holding costs and can eat directly into your profit and the capital you can pull out.

- Mitigation:

- Detailed SOW: A vague scope of work is an invitation for cost overruns. A detailed SOW locks in the price.

- Contingency Fund: Always include a 10-15% contingency line item in your rehab budget. If the budget is $50,000, plan to spend $57,500.

- Thorough Vetting of Contractors: Hire experienced, reliable contractors with proven systems. Check references, verify insurance, and have a rock-solid contract in place.

- Regular Site Visits: Don't be an absentee investor. Visit the job site regularly to monitor progress and address issues before they become major problems.

Download Our Free BRRRR Project Checklist

To help you stay on track and mitigate these risks, we've created a comprehensive checklist that covers every stage of the BRRRR process, from initial deal analysis to the final refinance. Download Our Free BRRRR Project Checklist to ensure you don't miss a single critical step on your next project.

Building Your BRRRR Power Team

You cannot successfully scale a BRRRR operation on your own. It's a team sport. Assembling a "power team" of skilled, reliable professionals who understand investor needs is just as important as finding a good deal.

Finding an investor-focused real estate agent

Not all real estate agents are created equal. You need an agent who is also an investor or works primarily with investors. An investor-focused agent understands your goals and has the skills you need.

They will:

- Understand deal analysis and terms like ARV, cash flow, and cap rate.

- Have access to off-market deals through their network.

- Be skilled at writing compelling offers that appeal to sellers of distressed properties.

- Be able to recommend investor-friendly contractors, inspectors, and other professionals.

- Not waste your time sending you turnkey properties at full retail prices.

You can find these agents at local Real Estate Investor Association (REIA) meetings or by getting referrals from other investors.

Vetting and managing reliable contractors

Your contractor is arguably the most important member of your team during the rehab phase. A great contractor can make a project a smooth, profitable success, while a bad one can turn it into a nightmare of delays, poor workmanship, and budget overruns.

When vetting a contractor:

- Verify License and Insurance: Never hire an unlicensed or uninsured contractor. Ask for a copy of their general liability and worker's compensation insurance certificates.

- Check References: Don't just ask for references; actually call them. Ask about their experience, communication, and whether the project was completed on time and on budget.

- Inspect Past Work: If possible, ask to see a recently completed project to judge the quality of their work firsthand.

- Get a Detailed Contract: Your contract should include the detailed SOW, a clear payment schedule tied to milestones (draws), a projected timeline, and a process for handling change orders.

Partnering with a lender specializing in BRRRR financing

Your lender is not just a source of money; they are a strategic partner. A lender who doesn't understand the BRRRR method, and specifically the Fast-Track Rehab Exception, will be a constant source of friction and delays.

A true BRRRR-specialist lender will:

- Offer both short-term fix and flip loans and long-term DSCR loans.

- Have a streamlined process for transitioning from one loan to the other.

- Have underwriters and processors who are experts in the Rehab Exception documentation requirements.

- Be able to close loans quickly, both on the purchase and the refinance.

Partnering with a one-stop-shop lender saves you time, reduces paperwork, and ensures that the team underwriting your refinance already understands the history and merits of your project from the initial purchase.

Assembling legal and accounting professionals for asset protection

As you begin to acquire assets, you need to protect them. It's crucial to bring legal and accounting professionals onto your team early.

- Real Estate Attorney: An attorney can help you set up the proper legal structure for your business, typically an LLC, to protect your personal assets from any liability associated with your rental properties. They will also review all your contracts and closing documents.

- Certified Public Accountant (CPA): A CPA with experience in real estate can be invaluable for tax strategy. They can advise you on how to properly track your expenses, maximize deductions like depreciation, and plan for the tax implications of your investments, saving you thousands of dollars in the long run.

The Ideal Financing Partner for Your BRRRR Strategy

The BRRRR method is a financing-intensive strategy that demands a lender built for speed, flexibility, and expertise. OfferMarket is designed from the ground up to be the ideal financing partner for serious BRRRR investors. We provide the specialized tools and seamless process you need to execute your strategy efficiently and scale your portfolio faster.

Using our Fix and Flip Loans for up to 90 percent LTC and 100 percent rehab financing

The journey starts with the acquisition. Our Fix and Flip Loans are structured to maximize your leverage and preserve your capital. We can fund up to 90% of the property's purchase price and 100% of your renovation budget, significantly reducing the amount of cash you need to bring to the closing table. With a fast, streamlined application and closing process, we give you the ability to compete with cash buyers and lock down the best deals.

Transitioning seamlessly to our DSCR loans for the long-term hold

We are not just a short-term lender. We are your end-to-end financing partner. Once your renovation is complete and your tenant is in place, we facilitate a smooth and efficient transition to one of our long-term DSCR loans. Because we handled the initial financing, our team already has the property's history and documentation. We are experts in executing the Rehab Exception, allowing you to bypass the 6-month seasoning period and get your capital back in weeks, not months.

How our process is designed for the speed and demands of BRRRR investors

We understand that for a BRRRR investor, time is money. Every day your capital is tied up is a day you're not working on the next deal. Our entire platform is built around this principle:

- Instant Quotes: Get real-time loan quotes online in minutes.

- Dedicated Experts: You work with a single point of contact who understands your project from start to finish.

- Transparent Process: We have clear guidelines and checklists for the Rehab Exception, so you know exactly what you need to provide.

- Integrated Platform: We offer the full suite of loan products you need under one roof, eliminating the hassle of working with multiple lenders.

Stop letting slow, inexperienced lenders dictate the pace of your growth. Partner with a lender that is as ambitious about scaling your portfolio as you are.

Get an Instant Quote for Your Next BRRRR Loan

Ready to finance your next BRRRR deal? See what's possible with a lender designed for investors. Get an instant, no-obligation quote for your fix and flip and DSCR loan in under two minutes.

OfferMarket Loans

Check your rate

60 seconds · no credit pull