*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Hard Money For Down Payment

Last Updated: September 25, 2025

For single-family rental (SFR) investors targeting 1-4 unit residential properties, leveraging financing is a cornerstone of building a portfolio. One approach some investors consider is using hard money loans to cover the down payment, aiming to enter deals with minimal personal capital. While this strategy might seem appealing, it introduces significant risks that can jeopardize financial stability and long-term success. This article explores the dangers of using hard money for down payments, the mechanics of 100% Combined Loan-to-Value (CLTV) financing, the implications for Debt Service Coverage Ratio (DSCR) loans, and the critical role of liquidity and equity in risk management.

What is Hard Money Lending?

Hard money loans are short-term, asset-based loans provided by private lenders or firms, typically used for real estate investments. Unlike traditional mortgages, hard money loans are secured by the property’s value rather than the borrower’s creditworthiness. They come with higher interest rates (often 10-15% or more), shorter terms (6 months to 3 years), and significant fees, reflecting their riskier nature. For SFR investors, hard money is commonly used for acquisition or rehab financing, but some consider it for down payments to achieve 100% CLTV financing—covering the entire purchase price with debt.

The Risks of Using Hard Money for Down Payments

Using hard money to fund a down payment significantly increases financial risk for SFR investors. This approach eliminates the investor’s personal equity in the deal, leaving no buffer against market fluctuations, unexpected costs, or operational challenges. Here are the primary risks:

1. Increased Debt Burden

Hard money loans for down payments typically take a second-lien position behind a primary mortgage. The high interest rates and fees on the second loan amplify the total debt service, reducing cash flow and squeezing profit margins.

2. Negative Cash Flow

For SFR investors, cash flow is critical. A high debt load from 100% CLTV financing often results in a Debt Service Coverage Ratio (DSCR) below 1.0, meaning rental income cannot cover debt payments. This can lead to financial strain, especially if vacancies or maintenance costs arise.

3. Violation of Loan Agreements

Many DSCR lenders explicitly prohibit secondary financing (e.g., a second-lien hard money loan) as it undermines their risk assessment. Using hard money for a down payment without disclosure can breach the loan agreement, risking a “call” on the loan, where the lender demands immediate repayment.

4. Lack of Equity as a Safety Net

Equity—the difference between the property’s value and the debt owed—serves as a cushion against market downturns or unexpected expenses. With 100% CLTV financing, there’s no equity, leaving investors vulnerable to foreclosure if they can’t meet debt obligations.

5. Liquidity Constraints

Real estate investments, especially rehab projects, often encounter cost overruns or delays. Without personal liquidity, investors relying on hard money for down payments may struggle to cover these costs, increasing the risk of default.

Example: Cost of 100% CLTV Financing

To illustrate the financial impact, consider a $300,000 single-family rental property financed with an 80% LTV first mortgage and a 20% LTV hard money second loan. The table below outlines the costs, assuming a 30-year fixed rate first mortgage at 6.5% interest and a 12-month hard money loan at 12% interest with 2 points (2% of the loan amount) in upfront fees.

| Loan Type | Loan Amount | Interest Rate | Monthly Payment | Upfront Fees | Total Annual Cost |

|---|---|---|---|---|---|

| First Mortgage (80% LTV) | $240,000 | 6.5% | $1,517 | $2,400 (1 point) | $18,203 (principal + interest) |

| Hard Money (20% LTV) | $60,000 | 12% | $600 (interest-only) | $1,200 (2 points) | $8,400 (interest + fees) |

| Taxes | $250 | $750 (escrow) | $3,000 | ||

| Insurance | $100 | $1,500 (prepaid + escrow) | $1,200 | ||

| Total | $300,000 | 7.57% | $2,467 | $5,850 | $29,604 |

Assumptions:

- The first mortgage has a 30-year amortization schedule.

- The hard money loan is interest-only, due in 12 months.

- The property generates $2,000/month in rental income

In this scenario, the PITIA monthly debt service ($2,467) exceeds the rental income ($2,000), resulting in a DSCR of 0.81 ($2,000 / $2,467). A DSCR below 1.0 indicates negative cash flow, meaning the investor must cover the shortfall from personal funds each month to the tune of $467 or more because this does not even factor in maintenance costs or property management fees.

Properties that generate negative cash flow (considered by many experienced investors to be liabilities, not assets) can put investors with low liquidity in a dangerous position racking up credit card debt. This can cause your tri merge credit score to drop.

Additionally, the hard money loan’s balloon payment of $60,000 plus any unpaid interest comes due in 12 months. How are you going to handle this payoff without refinancing or selling the property to avoid default?

Refinancing may not be an option for one or more of the following reasons:

- property value has not increase => you have 0% equity and the lender requires a minimum of 20% equity and you would need to bring that plus closing costs to closing (over $60,000...)

- property has decreased => you have negative equity (you owe more than the property is worth) and you would need to bring well over $60,000 to close

- your credit score has decreased from 720 to 600 and you do not qualify for a DSCR loan

Selling may not be an option for one or more of the following reasons:

- property is tenant occupied and buyers are not interested in paying market price

- property value has not increased and you would need to bring cash to cover closing costs

- property value has decreased and you would need to bring a considerable amount of cash to close

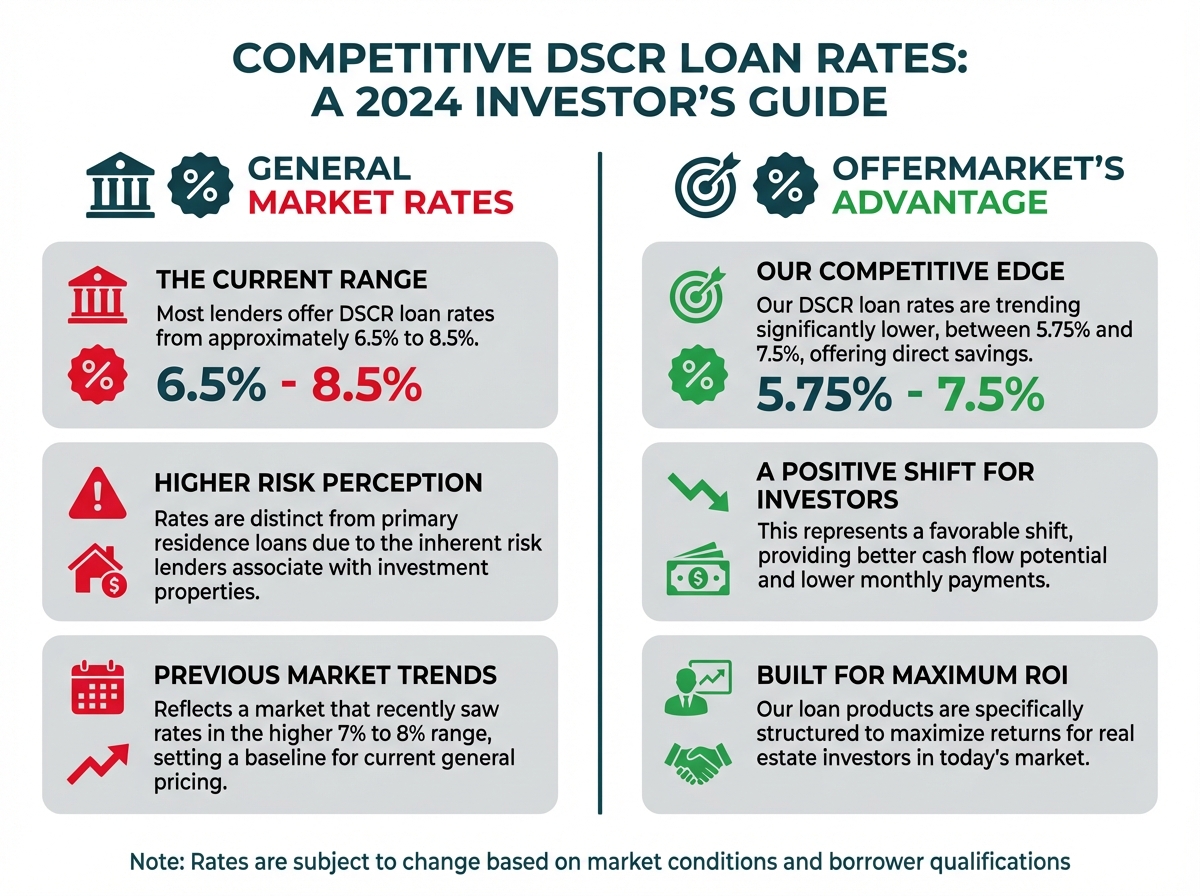

DSCR Loan Guidelines and Risks

DSCR loans are popular among SFR investors because they focus on the property’s income potential rather than the borrower’s personal income. However, these loans come with strict guidelines that conflict with using hard money for down payments:

Prohibition of Secondary Financing: Most DSCR lenders do not allow second-lien loans, as they increase the total debt burden and risk of default. Using a hard money loan for the down payment without disclosure violates the loan agreement, risking severe consequences like loan acceleration or legal action.

Liquidity Verification: DSCR lenders typically require borrowers to demonstrate liquidity (e.g., 6-12 months of debt service reserves). Large deposits, such as proceeds from a hard money loan, trigger scrutiny and require a letter of explanation. If the lender discovers the deposit is a loan, they may reject the application or deem it a violation post-closing.

Negative Cash Flow Danger: A DSCR below 1.0, as shown in the example above, creates immediate financial strain. For SFR investors, this can lead to missed payments, depleted reserves, and ultimately foreclosure if the property underperforms or market conditions worsen.

Attempting to bypass these guidelines by not disclosing the hard money loan is both unethical and risky. Lenders often conduct post-closing audits, and discovery of an undisclosed second lien can trigger default proceedings.

The Importance of Liquidity

Liquidity (cash reserves or easily accessible funds) is a critical safety net for SFR investors. Relying on hard money for a down payment often indicates limited personal capital, which can trap investors in problematic deals. Consider these scenarios:

Rehab Cost Overruns: Renovations frequently exceed budgeted costs due to unforeseen issues like structural damage or permitting delays. Without liquidity, investors may struggle to complete the project, delaying rental income or sale.

Cash to Close: When refinancing or selling a property, investors may need to bring cash to closing to cover closing costs, pay down debt, or meet lender requirements. Without reserves, they may be unable to exit the deal profitably.

Market Downturns: If property values decline, investors with 100% CLTV financing have no equity cushion. A forced sale or refinance could result in a loss, as the debt exceeds the property’s value.

Paying high interest on a hard money loan while lacking liquidity compounds these issues. The combination of excessive debt and no cash reserves can lead to foreclosure or bankruptcy, especially in a volatile market.

Equity Equals Safety in Risk Management

Equity—the investor’s stake in the property—serves as a critical risk management tool. By contributing personal capital to the down payment, investors create a buffer that protects against financial challenges. For example:

- Market Protection: If property values drop, equity reduces the risk of being “underwater” (owing more than the property’s worth).

- Lender Confidence: Lenders view equity as “skin in the game,” signaling the borrower’s commitment to the deal. This can lead to better loan terms and lower scrutiny.

- Flexibility: Equity provides options, such as selling at a breakeven price or refinancing without needing additional cash.

Using hard money for the down payment eliminates this safety net, leaving investors exposed to market risks and operational challenges.

Lenders Want Skin in the Game

Lenders, whether traditional or DSCR, prioritize borrowers who have personal capital invested in the deal. This “skin in the game” demonstrates financial discipline and reduces the lender’s risk. By using hard money for the down payment, investors signal higher risk to lenders, as they’re fully leveraged with no personal stake. This can lead to:

- Stricter Loan Terms: Lenders may impose higher rates or additional reserves if they suspect over-leverage.

- Loan Denials: DSCR lenders may reject applications if they detect secondary financing or insufficient liquidity.

- Post-Closing Issues: Undisclosed hard money loans can trigger audits, leading to loan default or legal consequences.

Additional Considerations for SFR Investors

Beyond the risks outlined, SFR investors should consider the following strategies to manage financing responsibly:

1. Build Cash Reserves

Aim to maintain 6-12 months of debt service reserves, plus additional funds for rehab or operational costs. This ensures flexibility during unexpected challenges.

2. Explore Alternative Financing

Instead of hard money for down payments, consider seller financing, private money from trusted partners, or joint ventures to reduce personal capital requirements without excessive debt.

3. Focus on Cash Flow

Prioritize properties with strong DSCR (ideally 1.2 or higher) to ensure rental income covers debt service and provides a buffer for expenses.

4. Plan for Exit Strategies

Before entering a deal, map out refinance or sale scenarios. Ensure you have liquidity or equity to cover costs and avoid being trapped in a high-debt deal.

5. Understand Market Risks

Analyze local market trends, such as vacancy rates and appreciation potential, to avoid over-leveraging in a declining market.

6. Wholesale To Build Liquidity

Real estate wholesaling is a great way to build liquidity and experience. Some of the best real estate investors started as wholesalers, accumulated strong liquidity and then started to cherry-pick their best deals for their own portfolio.

Conclusion

Using hard money for a down payment may seem like a shortcut to acquiring SFR properties, but it introduces significant risks that can undermine an investor’s financial stability. The high costs of 100% CLTV financing, combined with the strict guidelines of DSCR loans, create a precarious situation with little margin for error. Liquidity and equity are essential for managing risks, ensuring cash flow, and maintaining flexibility in real estate investments. By prioritizing personal capital and conservative financing strategies, SFR investors can build sustainable portfolios while avoiding the pitfalls of over-leverage. For those considering hard money, weigh the risks carefully and consult with experienced professionals to ensure your investment strategy aligns with long-term success.

Join OfferMarket

OfferMarket is a real estate investing platform focused on serving rental property investors, small builders and flippers. We focus exclusively on 1-4 unit residential properties in non-rural markets. Transparency and proactive risk management are core to our real estate investing and client service philosophy.

We hope you will accept our invitation to join us and over 20,000 registered members.

Membership is entirely free and comes with the following benefits:

🏚️ Off market properties 💰 Private lending ☂️ Landlord insurance rate shopping 💡 Market insights

Our mission is to help you build wealth through real estate and we look forward to contributing to your success!

OfferMarket Loans

Check your rate

60 seconds · no credit pull