*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Fix and Flip Lending Explained: Leverage, Terms & Scaling

Fix and flip lending, also known as hard money or bridge lending, provides short-term, interest-only financing designed specifically for real estate investors who purchase, renovate, and sell non-owner-occupied 1-4 unit residential properties for profit. Unlike traditional mortgages, which are built for long-term homeownership, these loans are structured for speed and flexibility, accommodating the rapid lifecycle of an investment project. Lenders finance both the acquisition of the property and the planned renovations, with the loan typically repaid in full from the proceeds of the final sale.

![1. Task: Create an infographic that visually summarizes the core concepts of Fix and Flip Lending to provide a quick, at-a-glance understanding for real estate investors.

2. Visual Structure: A vertically oriented infographic with a clear title at the top, followed by five distinct, icon-driven sections arranged in a clean, two-column grid below the header. The overall design should be modern and professional.

3. ASCII Layout Reference:

```

+--------------------------------------------------+

| The Anatomy of a Fix and Flip Loan |

|--------------------------------------------------|

| [Icon 1] | [Icon 2] |

| **For Investors,** | **Short-Term** |

| **Not Homeowners** | **Financing** |

| Loans for business- | Typically 12-month |

| purpose properties. | terms, not 30 years. |

|--------------------------|-----------------------|

| [Icon 3] | [Icon 4] |

| **Funds Rehab Costs** | **Interest-Only** |

| Finances purchase AND | **Payments** |

| renovation budget. | Lower monthly costs |

| | during the project. |

|--------------------------|-----------------------|

| [Icon 5] - Center Aligned |

| **Asset-Based Underwriting** |

| Focus is on the property's After- |

| Repair Value (ARV), enabling fast |

| approvals and closings. |

+--------------------------------------------------+

```

4. Image section breakdown:

- **Header Section:** The title](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1773345510407_lqz2qm.jpg?alt=media&token=2a8ceffe-ec38-423a-929e-c822a88513f8)

The core of a fix and flip loan is its asset-based underwriting. While a borrower's credit and experience are important, the lender's primary focus is on the viability of the property and the project itself—specifically, its potential After-Repair Value (ARV). This approach allows for much faster closing times, often in as little as 10-21 days, giving investors a critical competitive edge in fast-moving markets. This guide will break down every component of fix and flip lending, from the essential leverage metrics and loan terms to the complete lifecycle of a deal, so you can finance your next project with confidence.

Part 1: What is Fix and Flip Lending?

Defining Fix and Flip Loans

A fix and flip loan is a specialized, short-term financing instrument used by real estate investors to purchase and renovate a property with the intention of selling it for a profit. Unlike conventional loans that are underwritten based primarily on the borrower's personal income and debt (DTI ratio), fix and flip loans are asset-based. This means the lender's decision is heavily weighted on the financial viability of the investment property itself, including its purchase price, renovation budget, and most importantly, its After-Repair Value (ARV). These loans are designed to cover both the acquisition cost and the construction expenses, providing a comprehensive financing solution for the entire project lifecycle.

Target Audience: Real Estate Investors, Not Homeowners

It is critical to understand that fix and flip loans are strictly for business purposes and are not available to individuals seeking to buy and live in a home. The property must be a non-owner-occupied, 1-4 unit residential property. Lenders require the borrower to be a legal business entity, such as a Limited Liability Company (LLC) or a Corporation. This legal structure separates the investor's personal assets from their business activities, a standard practice in commercial lending. The loan is made to the business, though it is typically secured by a personal guaranty from the principal members of the entity. This distinction is fundamental; these are commercial loans for professional investors, not consumer mortgages for homeowners.

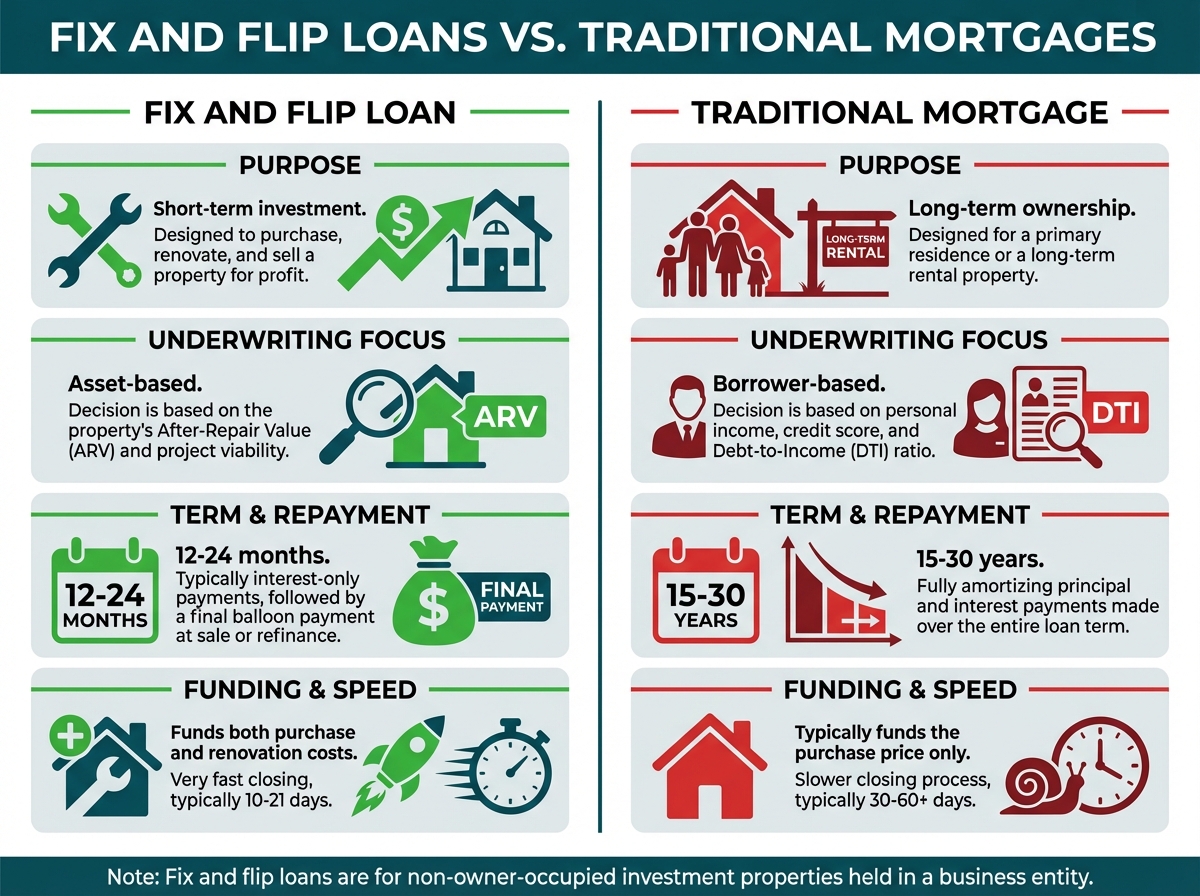

Key Differences from Traditional Mortgages

The structure, purpose, and underwriting of fix and flip loans are fundamentally different from traditional mortgages, such as those backed by Fannie Mae or Freddie Mac.

| Feature | Fix and Flip Loan | Traditional Mortgage |

|---|---|---|

| Purpose | Short-term investment (buy, renovate, sell) | Long-term primary residence or rental |

| Term Length | 12-24 months | 15-30 years |

| Payment Structure | Interest-only | Principal and Interest (P&I) |

| Repayment | Balloon payment at sale or refinance | Fully amortizing over the loan term |

| Underwriting Focus | Property's ARV and project viability | Borrower's personal income and DTI |

| Closing Speed | 10-21 days | 30-60+ days |

| Funding Scope | Purchase price and renovation costs | Purchase price only (typically) |

| Prepayment Penalty | Typically none | Can sometimes apply |

These differences highlight why traditional financing is ill-suited for the fast-paced world of house flipping. An investor needs to close quickly to secure a deal, access capital for renovations, and maintain low carrying costs during the project—all features that are hallmarks of a well-structured fix and flip loan.

The Primary Goal: Short-Term Financing for Non-Owner-Occupied Properties

The ultimate objective of fix and flip lending is to provide investors with the necessary capital to execute their business plan within a short timeframe. The entire loan product is engineered around the "get in, get out" nature of flipping. The 12-month term provides ample time to complete renovations and market the property. The interest-only payment structure keeps monthly holding costs low, preserving the investor's capital for other project needs. The lack of a prepayment penalty ensures that the investor can sell the property and pay off the loan as soon as the project is complete without incurring extra fees, thereby maximizing their net profit.

Part 2: Core Characteristics of a Fix and Flip Loan

Understanding the key components of a fix and flip loan is essential for any investor. These characteristics dictate how much capital you can borrow, what your costs will be, how renovation funds are managed, and what qualifications you and your property must meet.

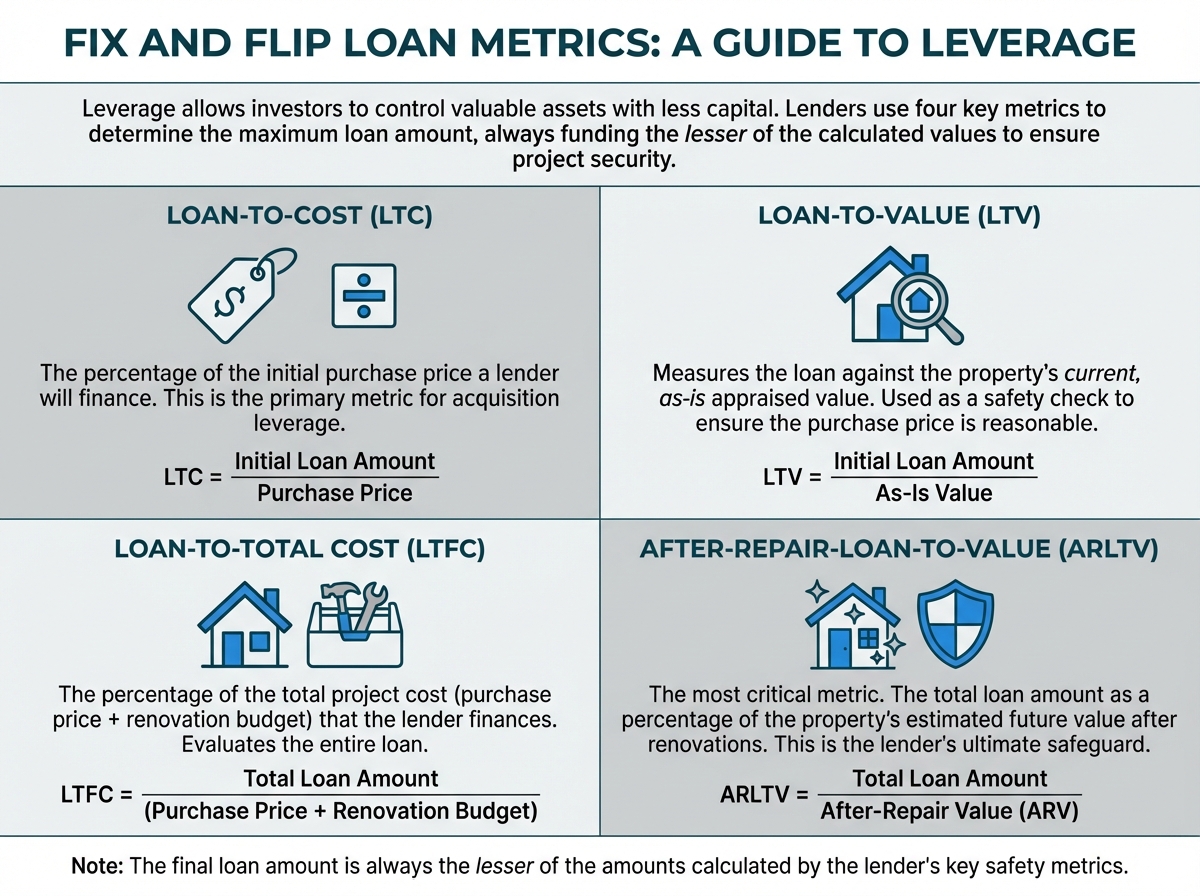

Understanding Leverage Metrics

Leverage is the cornerstone of fix and flip financing. It allows you to control a valuable asset with a smaller amount of your own capital, amplifying potential returns. Lenders use four primary metrics to determine your maximum loan amount: Loan-to-Cost (LTC) for the initial purchase, Loan-to-Value (LTV) based on current condition, Loan-to-Total Cost (LTFC) to factor in the renovation budget, and After-Repair-Loan-to-Value (ARLTV) to cap the final risk. The actual loan amount you receive will always be the lesser of the amounts calculated by these key safety metrics."*Leverage is the cornerstone of fix and flip financing. It allows you to control a valuable asset with a smaller amount of your own capital, amplifying potential returns. Lenders use three primary metrics to determine the maximum loan amount for a project: Loan-to-Cost (LTC), Loan-to-Value (LTV), and After-Repair-Loan-to-Value (ARLTV). The final loan amount will be the lesser of the amounts calculated by these key metrics.

LTC and LTV

In fix and flip lending, your initial acquisition leverage for a standard purchase is dictated by your Loan-to-Cost (LTC), which is based strictly on your purchase price. However, lenders also use **Loan-to-Value (LTV)**—which measures the loan against the current, as-is appraised value—as a secondary safety check in riskier scenarios (like refinances, high wholesale fees, or recent price run-ups). When both metrics are evaluated, the lender will base your initial loan amount on the lesser of your purchase price or the as-is value.

Formulas:

- LTC = Initial Loan Amount / Purchase Price

- LTV = Initial Loan Amount / As-Is Value

Example:

- Purchase Price: $250,000

- As-Is Appraised Value: $260,000

- If you qualify for a maximum of 90% initial leverage, the loan amount is capped by the lower metric (the purchase price): 0.90 * $250,000 = $225,000.Loan-to-Value measures the loan amount against the current, as-is value of the property at the time of purchase. This metric is more prominent in traditional lending but is also used by fix and flip lenders as a secondary check, especially to ensure the purchase price is reasonable.

Formula: LTV = Loan Amount / As-Is Value or Purchase Price (whichever is lower)

Example:

- Purchase Price: $250,000

- As-Is Appraised Value: $260,000

- If the lender's maximum LTV is 90%, the loan amount is based on the lower value (the purchase price): 0.90 * $250,000 = $225,000.

Loan-to-Total Cost (LTC): Financing the Purchase and Rehab

Loan-to-Total Cost (LTFC) is the percentage of the total project cost (purchase price + renovation budget) that the lender is willing to finance. For example, a lender may finance up to 90% of the initial purchase price (this specific metric is called LTC, or Loan-to-Cost) and 100% of the renovation costs for qualified borrowers. However, the entire loan is often evaluated as a single LTFC percentage against the total project cost.

Formula: LTFC = Total Loan Amount / (Purchase Price + Renovation Budget)

Example:

- Purchase Price: $250,000

- Renovation Budget: $70,000

- Total Project Cost: $320,000

- If a lender allows a maximum of 85% LTFC, the maximum total loan amount based on this metric would be: 0.85 * $320,000 = $272,000

After-Repair-Loan-to-Value (ARLTV): The Lender's Risk Cap

ARLTV is arguably the most important metric in fix and flip lending. It represents the total loan amount as a percentage of the property's estimated future value after all renovations are complete. This is the lender's ultimate safeguard, ensuring that even if they have to foreclose, there is a sufficient equity cushion to recoup their investment. Most lenders cap their ARLTV at 70-75%.

- Formula: ARLTV = Loan Amount / After-Repair Value (ARV)

- Example:

- After-Repair Value (ARV): $400,000

- If the lender's maximum ARLTV is 75%, the maximum loan amount based on this metric would be: 0.75 * $400,000 = $300,000.

How These Metrics Determine Your Required Down Payment

The lender will calculate the maximum loan amount using all relevant metrics (typically LTFC and ARLTV) and offer you the lowest resulting figure. This determines your required cash-to-close.

Let's put it all together with our example:

- Total Project Cost: $320,000

- ARV: $400,000

- Max Loan based on 85% LTFC: $272,000

- Max Loan based on 75% ARLTV: $300,000

The lender will approve a loan for $272,000, as it is the lower of the two calculations. Your required down payment (plus closing costs) would be:

- Total Project Cost ($320,000) - Loan Amount ($272,000) = $48,000

This calculation is crucial for budgeting. You can use a fix and flip calculator to run these numbers before you ever make an offer on a property.

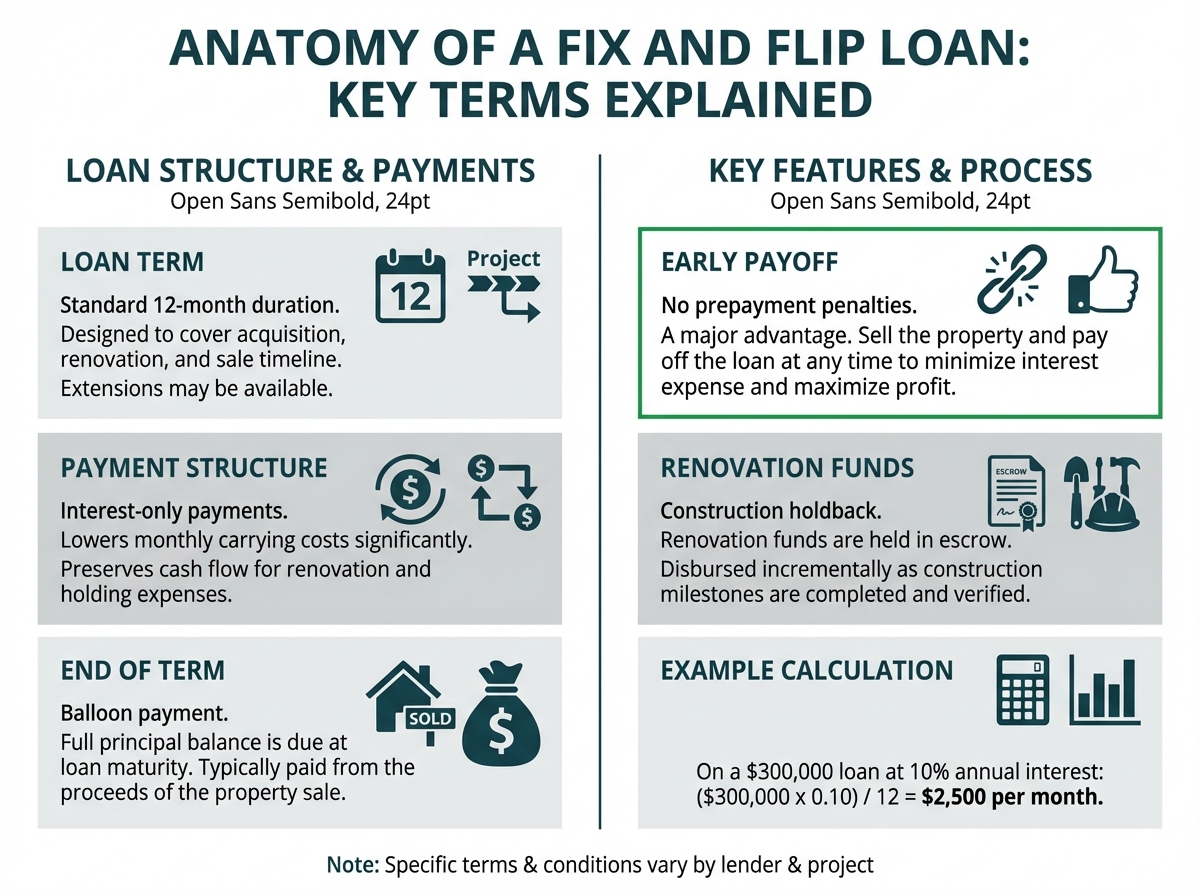

Decoding Loan Terms

The terms of a fix and flip loan are tailored for the project's lifecycle. They are simple and predictable, allowing investors to model their costs accurately.

Typical Duration: 12-Month Short-Term Financing

The standard term for a fix and flip loan is 12 months. This is generally considered sufficient time to acquire the property, complete even substantial renovations, market it effectively, and close the sale. Some lenders may offer slightly shorter (e.g., 6-9 months) or longer (18-24 months) terms, sometimes with an option to extend for a fee. The goal is to match the loan duration to a realistic project timeline.

Payment Structure: Interest-Only Payments

During the 12-month term, the borrower is only required to pay the interest that accrues on the outstanding loan balance. No principal is paid down. This structure significantly lowers the monthly carrying costs compared to a fully amortizing loan, preserving the investor's cash flow for managing the renovation, paying utilities, taxes, and other holding expenses.

- Example: On a $300,000 loan with a 10% annual interest rate, the monthly interest-only payment would be:

- ($300,000 * 0.10) / 12 = $2,500 per month.

The Balloon Payment at Maturity

At the end of the 12-month term (or whenever the property is sold), the entire principal balance of the loan is due in one lump sum, known as a balloon payment. This payment is typically made from the proceeds of the property sale. If the property hasn't sold by the maturity date, the investor must either pay off the loan with other funds, negotiate an extension with the lender, or refinance into a different loan product, such as a DSCR loan for a rental property.

The Investor Advantage: No Prepayment Penalties

A key feature of most fix and flip loans is the absence of prepayment penalties. This is a massive advantage for investors. If you finish your project in 5 months instead of 12, you can sell the property, pay off the loan, and stop paying interest immediately without any extra fees. This flexibility allows efficient investors to maximize their profitability by minimizing their interest expense and turning their capital over more quickly.

The Construction Holdback and Draw Process

When a fix and flip loan includes financing for renovations, the lender does not give you the full rehab budget at closing. Instead, these funds are placed in an escrow account and disbursed incrementally as work is completed. This is known as the construction holdback.

![1. Task: Create a flowchart infographic explaining the Construction Draw Process for a fix and flip loan.

2. Visual Structure: A simple, top-to-bottom flowchart with four main steps, connected by arrows. Each step will have a number, a title, a short description, and a corresponding icon.

3. ASCII Layout Reference:

```

+--------------------------------------------------+

| The Fix and Flip Construction Draw Process |

|--------------------------------------------------+

| [ICON 1: Checklist] |

| Step 1: Work Completed |

| Investor completes a phase |

| of the approved SOW. |

| | |

| V |

| [ICON 2: Document] |

| Step 2: Request Draw |

| Investor submits draw request |

| & documentation to lender. |

| | |

| V |

| [ICON 3: Magnifying Glass] |

| Step 3: Lender Inspects |

| Lender sends an inspector to |

| verify the completed work. |

| | |

| V |

| [ICON 4: Money Transfer] |

| Step 4: Funds Disbursed |

| Upon approval, lender releases|

| funds from the holdback. |

+--------------------------------------------------+

```

4. Image section breakdown:

- **Title:**](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1773344934177_mjl98j.jpg?alt=media&token=2b3d2a2f-bd72-4f9d-9f48-4e31045365af)

Defining the Construction Holdback

The construction holdback (or rehab escrow) is the portion of the loan allocated for renovations. This money is held by the lender to ensure it is used specifically for the improvements detailed in the Scope of Work (SOW) that was approved during underwriting. This protects the lender's investment by ensuring the property's value is increased as planned, thereby justifying the After-Repair Value.

Example:

- Total Loan Amount: $272,000

- Amount to Purchase Property: $250,000 (less down payment)

- Initial Loan Disbursement at Closing: $202,000 (to seller)

- Construction Holdback: $70,000 (held by lender for rehab)

How Renovation Funds Are Disbursed Through Draws

When you complete a phase of your renovation (e.g., demolition and framing, or rough-in plumbing and electrical), you can request a "draw" from your construction holdback. You submit a draw request to the lender, detailing the work that has been completed.

The Inspection Process for Approving Draws

Upon receiving a draw request, the lender will dispatch a third-party inspector to the property. The inspector's job is to verify that the work claimed on the draw request has been completed in a workmanlike manner and generally aligns with the original Scope of Work. They will take photos and file a report with the lender. Once the lender reviews and approves the inspection report, they will release the funds for that portion of the work, typically via wire transfer or ACH. This process, from request to funding, usually takes a few business days.

Managing Your Project Timeline and Budget with Draws

The draw process is a critical part of project management. It forces you to structure your renovation in logical phases and ensures you have the funds to pay contractors as work is completed. However, it also means you must have enough initial capital to get the project started and cover the costs of the first phase of work before you can be reimbursed.

Pro Tip: Always have a clear and detailed Scope of Work (SOW) before you start. A well-defined SOW is essential for getting your loan approved and for streamlining the draw process. Share it with your contractor so everyone is aligned on the project phases, which will correspond to your draw requests. Efficiently managing your draws is key to keeping your project on schedule and your contractors happy.

Borrower and Property Requirements

Fix and flip lenders have specific requirements for both the borrower and the property to mitigate risk and ensure compliance with commercial lending regulations.

The Necessity of a Business Entity (LLC or Corporation)

As mentioned, these are business-purpose loans. Therefore, the borrower must be a legally registered business entity, not an individual. The most common entities are a Limited Liability Company (LLC) or an S-Corporation. This structure provides a liability shield for the investor's personal assets. Lenders will require copies of your entity's formation documents, such as the Articles of Organization and Operating Agreement. Information on setting up a business entity can be found on the U.S. Small Business Administration (SBA) website.

The Role of the Personal Guaranty

While the loan is made to the business entity, lenders require a personal guaranty from the principal owners. This is a legal promise from an individual to repay the debt if the business entity defaults. Typically, any member with a significant ownership stake (e.g., 20-25% or more) will be required to sign the guaranty. Lenders generally require members representing at least 51% of the entity's ownership to provide a full recourse personal guaranty. This means if the loan goes into default, the lender can pursue the personal assets of the guarantors to satisfy the debt.

Minimum Credit Score and Financial Requirements

Lenders will review the personal credit of the guarantors. The minimum qualifying FICO score is typically around 680. A higher credit score can often lead to better loan terms, including lower interest rates and origination fees. In addition to credit, lenders will want to see that you have sufficient liquidity—cash reserves to cover your down payment, closing costs, monthly interest payments, and a contingency fund for unexpected renovation expenses. They will verify this by reviewing recent bank statements.

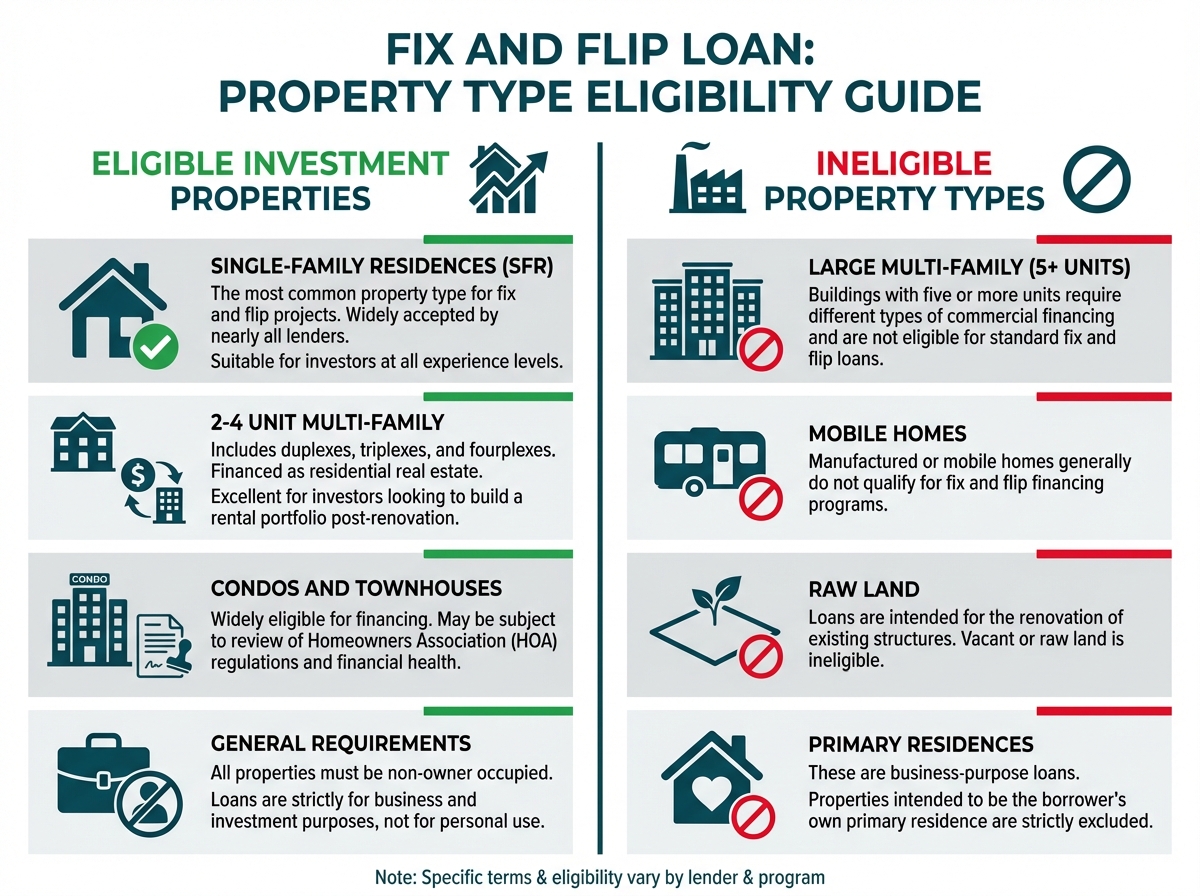

Eligible Property Types: 1-4 Unit Residential

Fix and flip loans are designed for residential properties that are not the borrower's primary residence. Eligible property types include:

- Single-Family Residences (SFRs)

- Condominiums

- Townhouses

- 2-4 Unit Multi-Family Properties

Properties that are generally ineligible include mobile homes, raw land, and large multi-family buildings (5+ units), which require different types of commercial financing. The property must be used strictly for business or investment purposes.

The Impact of Experience Tiers

Your track record as a real estate investor is one of the most significant factors influencing your loan terms. Lenders categorize borrowers into experience tiers based on the number of successful projects (flips or rentals) they have completed in a recent period, typically the last 24-36 months. More experience translates to lower risk for the lender, which is rewarded with better leverage and more flexible terms.

Tier 1: First-Time Flippers and Their Limitations

A Tier 1 investor has zero documented projects in the last three years. Lenders view first-time flippers as higher risk, so they impose stricter limitations.

- Leverage: Lower LTC and ARLTV, meaning a larger down payment is required.

- Renovation Budget: The rehab budget may be capped. For example, some lenders limit a Tier 1 investor's renovation to a maximum of $100,000, and it cannot exceed 25% of the purchase price.

- Loan Size: The total loan amount may be smaller.

- Pricing: Interest rates and origination fees may be slightly higher.

Mid-Level Tiers: Gaining More Leverage and Flexibility

As you complete successful flips, you move up the tiers. An investor with 2-4 completed flips (Tier 2/3) will see significant improvements.

- Higher Leverage: Access to the lender's maximum leverage (e.g., 90% of purchase, 100% of rehab, up to 75% ARLTV).

- Larger Projects: Restrictions on renovation budget size are often removed.

- Better Pricing: Rates and fees become more competitive.

Tier 5: Benefits for Seasoned Professionals with 10+ Flips

Investors at the highest tier (e.g., Tier 5 with 10+ flips) are considered top-tier clients. They have a proven ability to manage projects and deliver returns.

- Best Possible Terms: They receive the most aggressive leverage and the lowest interest rates and fees.

- Larger Loan Amounts: Access to higher loan amounts, sometimes up to $3,500,000 or more with special pre-screening.

- Streamlined Underwriting: The underwriting process may be faster and require less documentation, as their track record speaks for itself.

- Portfolio Options: They may gain access to portfolio loans or lines of credit to finance multiple projects simultaneously.

Building your experience is the single most effective way to improve your financing options and scale your fix and flip business.

Part 3: The Fix and Flip Loan Lifecycle: From Application to Profit

The lifecycle of a fix and flip loan follows the lifecycle of the project itself. It can be broken down into four distinct phases, from finding the deal and securing financing to completing the renovation and realizing your profit at the closing table.

![1. Task: Create a visually engaging infographic that illustrates the four-phase lifecycle of a fix and flip loan.

2. Visual Structure: A circular or winding path infographic with four key stages. Each stage will be a distinct section with an icon, a title, and a brief description of the activities involved. The flow should guide the viewer's eye logically from one phase to the next.

3. ASCII Layout Reference:

```

+----------------------------------------------------------------+

| The Fix and Flip Loan Lifecycle |

|----------------------------------------------------------------|

| |

| (Phase 1: Pre-Approval) --arrow--> (Phase 2: Closing) |

| [Icon: Magnifying Glass] [Icon: Keys] |

| - Analyze Deal - Fund Acquisition |

| - Apply for Loan - Sign Documents |

| - Underwriting - Take Possession |

| |

| ^ | |

| | V |

| |

| (Phase 4: Exit) <----------arrow-- (Phase 3: Renovation) |

| [Icon: For Sale Sign] [Icon: Hammer] |

| - List & Sell Property - Execute SOW |

| - Pay Off Loan - Manage Draws |

| - Realize Profit - Work with Contractors |

| |

+----------------------------------------------------------------+

```

4. Image section breakdown:

- **Central Title:**](https://firebasestorage.googleapis.com/v0/b/offer-market-us.appspot.com/o/generated_images%2Fgenerated_1773345418545_0zhnjr.jpg?alt=media&token=b0563656-ec93-43b2-b688-af5361f7204c)

Phase 1: Pre-Approval and Underwriting

This initial phase is where you identify a viable project and secure the financing commitment needed to acquire it.

Finding and Analyzing a Potential Deal

Success in flipping starts with finding the right deal. This involves sourcing undervalued properties through various channels like the MLS, OfferMarket's marketplace, wholesalers, auctions, or direct-to-seller marketing. Once you identify a potential property, you must perform rigorous due diligence. This includes:

Estimating the After-Repair Value (ARV): Analyze recent sales of comparable renovated properties (comps) in the immediate vicinity to determine a realistic sales price.

Creating a Detailed Scope of Work (SOW): Walk the property with a contractor to build a line-item budget for all necessary repairs and upgrades.

Calculating Holding and Closing Costs: Factor in all expenses, including loan payments, insurance, taxes, utilities, and agent commissions on both the purchase and sale.

Submitting a Loan Application and Initial Documents

With a deal under contract (or identified), you can submit a formal loan application. Many modern lenders like OfferMarket allow you to get an instant quote online to see your potential terms before ever submitting a full application.

This typically involves providing:

- Your investment experience (number of flips/rentals in the last 36 months)

- Estimated credit score (no credit pull)

- Borrowing entity (Personal name or LLC)

- Portfolio loan (i.e. for multiple properties)

- Property type

- Unit size

- Subject property address

- Loan Purpose

- Estimated as-is value

- Purchase price

- Tenant type

- Leasing strategy

- Monthly rent

- Annual taxes

- Annual insurance

- Annual HOA

- Citizenship status

Create Your Loan File Application

Once you've reviewed your instant quote and decided to move forward, the next step is straightforward. When you click "SELECT" to continue to the term sheet and pre-approval on your instant quote, OfferMarket automatically creates a personalized Loan File for you. Think of this as your command center for managing your entire loan application.

Your Loan File contains much more detailed information than your initial quote, including:

Preliminary Loan Terms:

- Specific interest rate ranges based on your investor profile

- Detailed breakdown of all estimated fees (origination, processing, underwriting)

- Exact loan-to-value (LTV) and after-repair loan-to-value (ARLTV) ratios

- Draw schedule structure for your renovation budget

- Closing cost estimates

Your Loan File also serves as your project dashboard throughout the financing process. You can:

- Track the status of your application in real-time

- Upload required documents

- Communicate directly with OfferMarket's processing team

- Receive notifications about next steps and outstanding items

Everything you need lives in one place, organized and accessible 24/7. That's how financing should work.

Move to Processing & Expedite with Document Uploads

After thoroughly reviewing your preliminary Loan Terms in your Loan File, you're ready to formally begin the underwriting process. This is where you signal your intent to proceed by clicking "Move to processing" within your Loan File. This action lets OfferMarket's team know you're ready to roll and prepared to submit your documentation.

The Document Upload Phase:

Once you're here, head to the "Processing" section of your Loan File where you'll find a clear checklist of urgent section that's what we need from you.

You’ll complete and upload:

- Bank Statements

- ID Verification

- Borrowing Entity Details (LLC/Corp)

- Track Record (Past project history)

- Personal Financial Statement

- Personal guarantor information

- Insurance information (OfferMarket can help with that since we specialize in insurance for Fix and Flip properties)

OfferMarket's Speed Promise: Closing in Under 1-3 Weeks

Phase 2: Closing and Acquiring the Property

With a financing commitment in hand, you can proceed to the closing, where ownership of the property is officially transferred.

The Closing Process and Required Legal Documentation

The closing is managed by a title company or real estate attorney. You will be required to sign a package of legal documents, including:

- The Promissory Note: Your promise to repay the loan.

- The Mortgage or Deed of Trust: The document that secures the loan with the property as collateral.

- The Personal Guaranty: Your personal commitment to back the loan.

- Loan Agreement: Details all the terms, conditions, and covenants of the loan.

Funding the Acquisition and the Initial Rehab Draw

At closing, the lender wires the acquisition portion of the loan funds to the title company. The title company then disburses these funds to the seller. Your down payment and closing costs are also paid at this time. The renovation funds are not given to you; they are set aside in the construction holdback account managed by the lender.

Taking Possession of the Property

Once the closing is complete and the deed is recorded, you are the official owner of the property. You will receive the keys and can begin the renovation phase immediately.

Finalizing Insurance and Title

Before closing, you will be required to secure a builder's risk or vacant property insurance policy. This protects you and the lender from damage or liability during the renovation. The title company will also issue a lender's title insurance policy, which protects the lender's lien position.

Phase 3: The Renovation

This is the "fix" phase of the project, where you execute your business plan and transform the property.

Executing Your Scope of Work

This phase involves managing your contractors and subcontractors to carry out the renovations as detailed in your SOW. Effective project management is crucial to staying on schedule and on budget. Regular site visits and clear communication with your general contractor are essential.

Requesting and Receiving Construction Draws

As you complete major milestones (e.g., foundation work, framing, roofing, mechanicals), you will submit draw requests to your lender. As described earlier, this will trigger an inspection and the subsequent release of funds from your rehab holdback. A smooth draw process is vital for maintaining project momentum.

Working with Inspectors and the Lender

Throughout the renovation, you will interact with two types of inspectors:

Municipal Inspectors: To sign off on permitted work (e.g., electrical, plumbing, structural) and issue a Certificate of Occupancy.

Lender's Inspectors: To verify work for draw requests.

It's important to build good relationships with both and ensure all work is done to code to avoid costly delays.

Managing Contractors and Project Timelines

The success of your renovation hinges on your ability to manage your team. This includes:

- Having solid contracts in place.

- Setting clear expectations and timelines.

- Approving change orders in writing.

- Ensuring timely payment upon completion of work (often funded by your draws).

Phase 4: The Exit Strategy

With the renovation complete, the final phase is focused on selling the property and realizing your profit.

Listing and Marketing the Renovated Property

Work with a qualified real estate agent who understands the local market. You can post your deal on free marketplaces like OfferMarket's marketplace. They will help you stage it effectively, and market it to potential buyers. High-quality professional photography and a strong online presence are non-negotiable in today's market.

Navigating the Sale Process

Once you receive an offer, you can negotiate the price and terms directly. After going under contract, the buyer will conduct their own inspections and their lender will order an appraisal. It's important to be responsive and address any issues that arise to keep the sale on track.

Paying Off the Loan Balance with Sale Proceeds

At the closing of the sale, the title company will use the proceeds from the buyer to pay off your outstanding fix and flip loan balance in full. This includes the entire principal amount and any accrued interest.

Calculating and Realizing Your Net Profit

After the loan, closing costs, agent commissions, and all other project expenses are paid, the remaining funds are your net profit. These funds are wired directly to your business bank account.

Example Profit Calculation:

- Sale Price: $400,000

- Less Loan Payoff: $272,000

- Less Remaining Project Costs (your down payment, holding costs, closing costs, commissions, etc.): $80,000

- Net Profit: $48,000

BRRRR Note

While the primary exit is selling, some investors choose an alternative: the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) method. Instead of selling, they rent the property out and then refinance the short-term fix and flip loan into a long-term DSCR loan. This allows them to pull their capital out while holding the property as a cash-flowing rental. This is a powerful strategy for building long-term wealth.

Part 4: Advanced Strategies for Maximizing ROI

Once you've mastered the basics of a single fix and flip, the next step is to learn how to scale your operations and protect your business from common risks. This is how you transition from a hobbyist to a professional real estate investor.

Scaling Your Fix and Flip Business

Scaling is about creating efficient, repeatable systems that allow you to handle more volume without being overwhelmed.

Leveraging Your Track Record for Better Terms

As you complete more projects, you become a more attractive borrower. Actively use your growing portfolio to negotiate better terms on future loans. Go back to your lender after every 2-3 successful flips and ask for a review of your pricing and leverage. A small reduction in your interest rate or origination fee can add thousands to your bottom line over several projects.

Managing Multiple Projects Simultaneously

Scaling inevitably means juggling more than one project at a time. This requires exceptional organization and delegation.

Project Management Software: Use tools like Trello, Asana, or specialized construction management software to track timelines, budgets, and tasks for each property.

Standardized Systems: Create checklists and standardized processes for every phase of a flip, from due diligence to final punch-lists. This ensures consistency and reduces errors.

Financial Tracking: Maintain separate P&L statements for each project to accurately track profitability and identify areas for improvement.

Building a Reliable Team of Contractors and Agents

You cannot scale alone. Your success depends on the quality of your team.

General Contractors: Find one or two reliable GCs who understand your quality standards and can manage crews effectively. Treat them as partners and provide them with a steady stream of work.

Real Estate Agents: Work with an investor-savvy agent who can bring you off-market deals and accurately price your finished properties.

Bookkeepers and Accountants: Offload financial tracking to a professional who specializes in real estate. This frees you up to focus on finding deals and managing projects.

Strategies for Creating a Repeatable Flipping System

The most successful flippers treat their business like a factory assembly line.

Define Your "Box": Specialize in a particular neighborhood, property type (e.g., 3-bed, 2-bath ranch homes), or price point. This allows you to become an expert, making your ARV and rehab estimates more accurate.

Standardize Materials: Use a consistent palette of paint colors, flooring, fixtures, and finishes across all your projects. This allows you to buy materials in bulk, simplifies decision-making, and creates a recognizable brand for your flips.

Create a Deal Analysis Template: Use a detailed spreadsheet to analyze every potential deal using the same criteria. This removes emotion from the decision-making process and ensures you only pursue projects that meet your profit targets.

OfferMarket Loans

Check your rate

60 seconds · no credit pull