*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Dwg 3 Insurance Policy

A DWG-3 insurance policy, more commonly known as a DP-3 policy, is the most comprehensive type of coverage available for a non-owner-occupied residential property. It is the preferred choice for landlords and real estate investors who want robust protection for their rental properties. The "DWG" designation is an alternative name used by some carriers, particularly in states like Louisiana, but it refers to the same policy form as the DP-3.

This policy is considered a "special form" policy because it provides open perils coverage for the main dwelling (the house itself) and any attached structures. This means the structure is covered against all causes of loss except for those specifically listed as exclusions in the policy. For a landlord's personal property left on-site (like appliances), coverage is on a named perils basis, meaning it's only covered for the specific risks listed in the policy, such as fire or theft. Critically, claims for damage to the dwelling and other structures under a DP-3 are typically settled on a Replacement Cost Value (RCV) basis, which pays to rebuild the structure with similar materials without deducting for depreciation.

Breaking Down DP-3 Policy Coverage

A DP-3 policy is structured with several distinct coverage parts, each designed to protect a different aspect of your investment. Understanding these components is key to ensuring you are adequately insured.

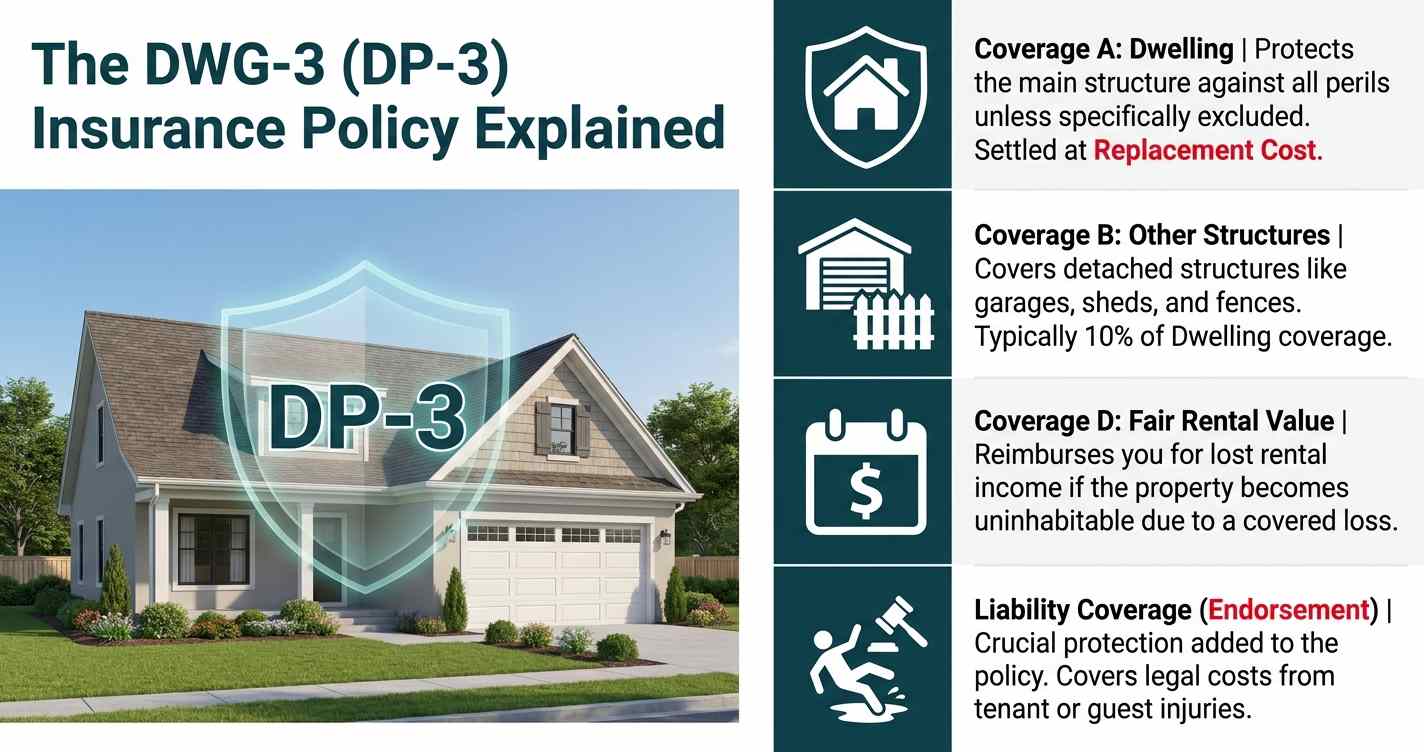

Coverage A: Dwelling

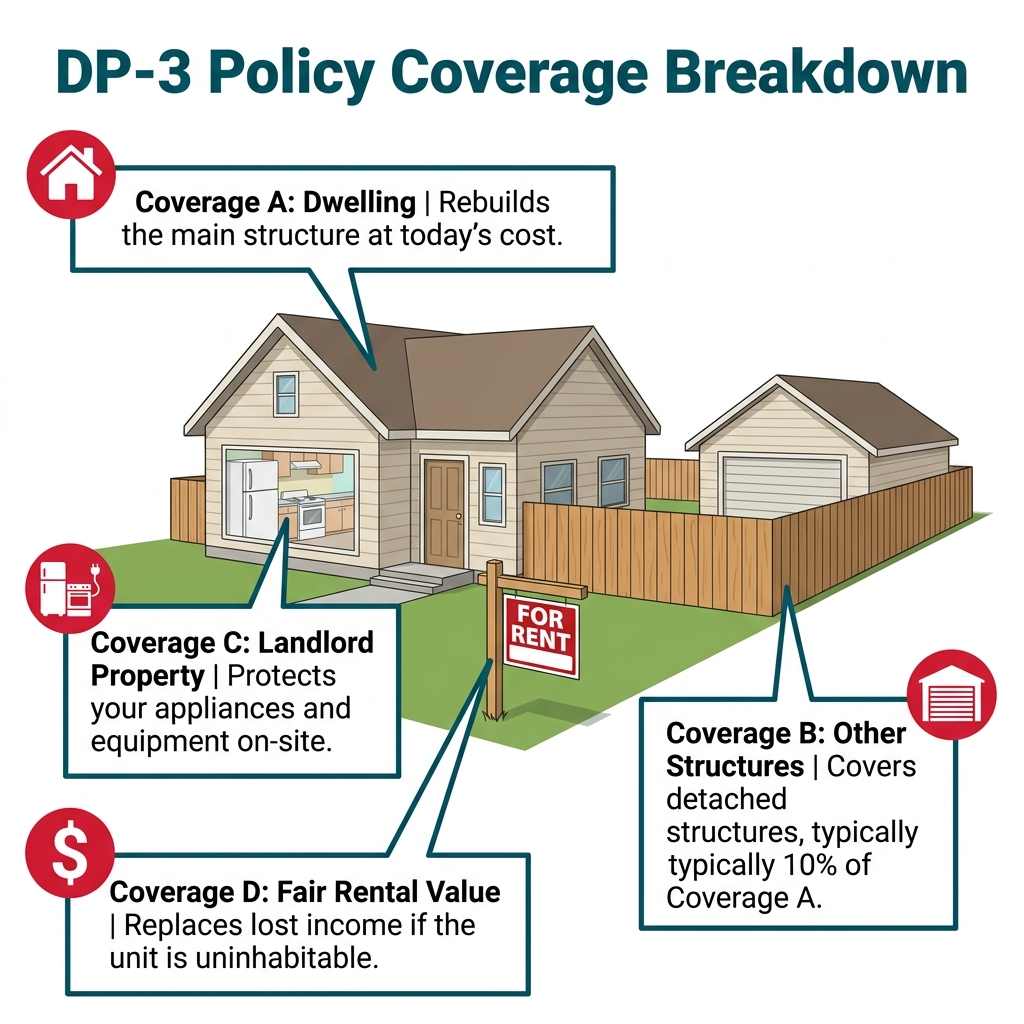

This is the core of the policy. Coverage A protects the main residential building and any attached structures, such as a garage, deck, or porch. The coverage limit for the dwelling should be set at its Replacement Cost Value (RCV). This is the estimated cost to rebuild the home from the ground up with materials of similar kind and quality, at today's prices, without any deduction for depreciation. It is crucial not to insure for the market value, which includes the land, but for the actual cost of reconstruction. Most insurers use specialized software to calculate this value accurately.

Coverage B: Other Structures

This part of the policy covers structures on the property that are not attached to the main dwelling. Common examples include a detached garage, a shed, a gazebo, or a fence. Coverage B is typically calculated as a percentage of your Coverage A limit, most often 10%. For example, if your dwelling is insured for $300,000 (Coverage A), your other structures would automatically be covered for up to $30,000. While this is usually sufficient, you may need to increase this limit if you have substantial or high-value detached structures on your property.

Coverage C: Landlord Personal Property

Coverage C is designed to protect personal property owned by the landlord that is used to service the rental or is available for the tenant's use. This includes items like refrigerators, washing machines, dryers, and lawnmowers. It does not cover the tenant's personal belongings—for that, they need their own renters insurance policy.

Unlike Coverage A and B, Coverage C is provided on a named perils basis, meaning it only covers losses from a specific list of events (e.g., fire, lightning, windstorm, theft). Furthermore, claims are usually settled on an Actual Cash Value (ACV) basis, which accounts for depreciation. The coverage limit is typically a smaller, fixed amount, such as $5,000 or $10,000.

Coverage D: Fair Rental Value (Loss of Rent)

This is one of the most valuable protections for a landlord. If your rental property becomes uninhabitable due to a covered loss (like a fire or major storm damage), Coverage D, also known as Fair Rental Value, will reimburse you for the lost rental income while the property is being repaired or rebuilt. This coverage ensures your cash flow is not interrupted, allowing you to continue meeting your mortgage and other obligations. The coverage limit is often set at 20% of the Coverage A limit and is paid out over the "period of restoration," typically up to 12 months.

Get an Instant Insurance Quote

Protect your investment property with competitive rates — quote in minutes.

Get Insurance Quote →Understanding Landlord Liability Coverage

If you have read other guides on DP-3 policies, you may have come across the claim that a DP-3 does not include liability coverage. That statement refers to the bare ISO standard form (DP 00 03), which is a property-only document on paper. In practice, virtually every carrier that serves landlords and investment property owners bundles liability coverage into their DP-3 product automatically by attaching a personal liability supplement endorsement to the base form. When you get a landlord insurance quote through OfferMarket, liability is included as part of the policy, not sold as a separate add-on you need to remember to request.

The real issue is not whether liability is included. It is whether the limit is high enough.

Many default DP-3 policies ship with $100,000 or $300,000 in premises liability. For a rental property, that is dangerously low. A tenant trips on a broken step and fractures an ankle, that is a $50,000 to $200,000 claim. A faulty wire you were responsible for causes a fire that damages a tenant's belongings, that can run into six figures. A visitor's child is injured on a playset in the backyard, a single lawsuit can reach seven figures. When a judgment exceeds your policy limit, the difference comes out of your personal assets: your bank accounts, your other properties, your retirement savings.

OfferMarket's coverage benchmark for landlord policies is $500,000 per occurrence in premises liability, 12 months of loss of rent coverage, and a flat $5,000 deductible across all perils including wind and hail. If a quote comes back with $100,000 or $300,000 liability, the in-house team flags it and works to get it increased before the policy is bound. This is one of the most common gaps caught during OfferMarket's quote review process because many carriers default to lower limits unless someone specifically requests more.

The same applies to loss of rent: some carriers default to 3 or 6 months, which leaves landlords exposed if a major repair takes longer, and to deductibles, where percentage-based wind and hail deductibles can quietly inflate your out-of-pocket costs on a claim by thousands of dollars compared to a flat $5,000.

For investors with multiple properties or higher-value portfolios, an excess liability policy (sometimes called an umbrella policy) that adds $1,000,000 or more above your existing limit is worth serious consideration. These typically run $80 to $100 per month and create a second layer of protection that shields your personal assets if a judgment exceeds your primary policy limit. If you own three, five, or ten rental properties, the cumulative liability exposure across your portfolio is substantial, and a single uninsured judgment on one property can put the rest of your portfolio at risk.

Common DWG-3 Policy Exclusions

A DP-3 policy covers everything unless it is specifically excluded. That is the advantage of open perils coverage. But the exclusion list is where most investors get caught, not because they did not read the policy, but because they assumed a broad policy meant total coverage. It does not. Here are the exclusions that matter most for rental property investors and what to do about each one.

Flood

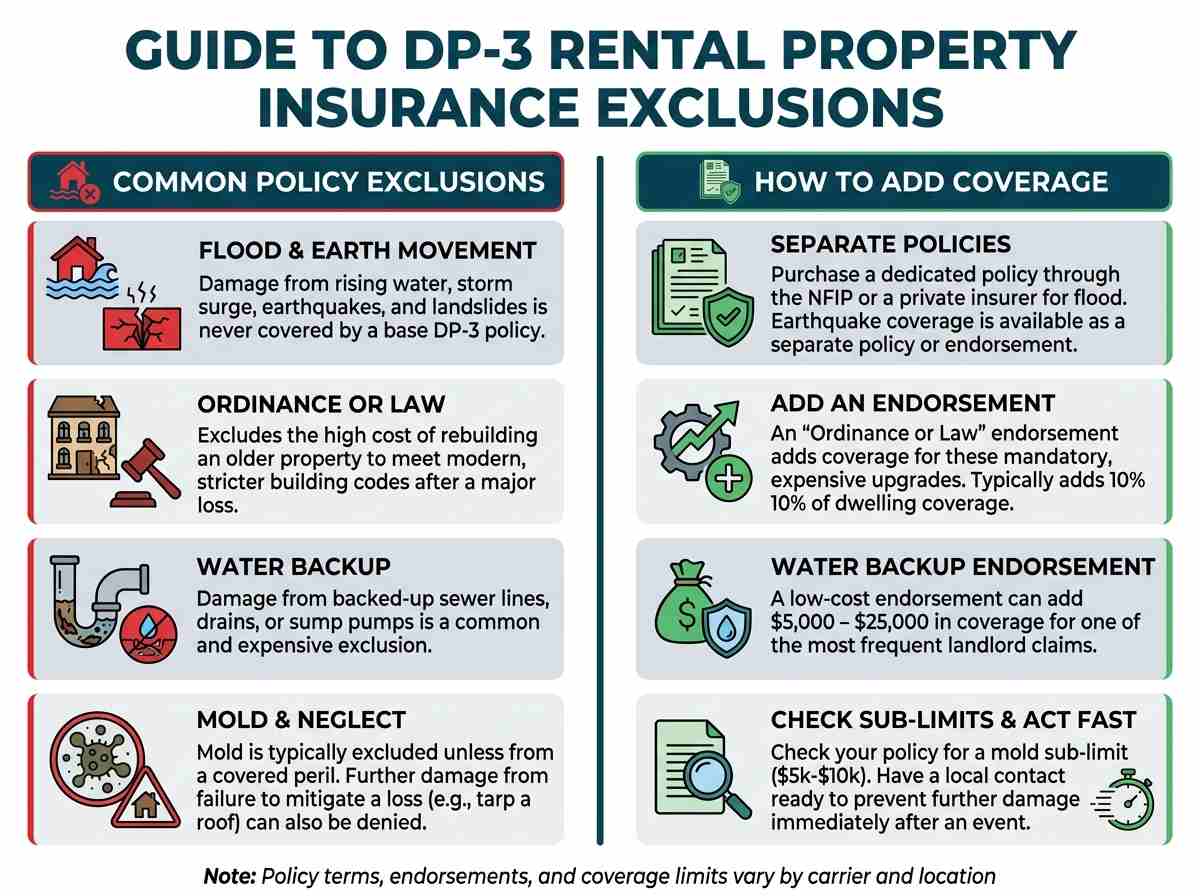

Damage from rising surface water, storm surge, and overflowing rivers is never covered under a DP-3 policy regardless of the carrier. If your rental property is in a FEMA-designated flood zone, your lender will require a separate flood policy before funding the loan. Even if the property is not in a mapped flood zone, flood damage can happen anywhere. A separate policy through the National Flood Insurance Program (NFIP) or a private flood insurer is the only way to cover this risk.

Earthquake and Earth Movement

This includes earthquakes, landslides, sinkholes, and mudflow. If you are investing in markets like California, the Pacific Northwest, or parts of the Midwest near the New Madrid fault line, this exclusion matters. Earthquake coverage is available as a separate policy or endorsement depending on the carrier and location.

Ordinance or Law

This is the exclusion that blindsides investors who own older properties. When a rental property built in the 1970s suffers major fire damage, the local building department does not let you rebuild to 1970s code. They require the rebuild to meet current code: updated electrical, fire-rated materials, sprinkler systems, ADA compliance. Those upgrades can add tens of thousands of dollars to the rebuild cost, and the base DP-3 policy will not pay for any of it. The fix is an ordinance or law endorsement. When you get a quote through OfferMarket, the in-house team checks that ordinance or law coverage is included as part of the policy. Most carriers that serve landlords default this endorsement to 10% of dwelling coverage. On a property with $500,000 in dwelling coverage, that gives you $50,000 toward code-compliance upgrades during a rebuild. Some carriers omit the endorsement entirely, which would leave you covering the full cost of mandatory building code upgrades out of pocket. The in-house team flags any quote where ordinance or law is missing so it gets added before the policy is bound.

Water Backup

Damage from a sewer line, drain, or sump pump that backs up into the property is excluded from the base DP-3 policy. This is one of the most common and most expensive claims for landlords, particularly in older cities with aging municipal sewer infrastructure. A single backup event can cause $5,000 to $30,000 in damage to finished basements, flooring, drywall, and personal property. The endorsement typically costs $50 to $150 per year and provides $5,000 to $25,000 in coverage.

Mold, Fungus, and Wet or Dry Rot

Most DP-3 policies exclude mold damage unless it results directly from a covered peril. Some carriers include a small sublimit (typically $5,000 to $10,000) for mold remediation. If your property is in a humid climate or has older plumbing, this is a risk worth understanding. Check your quote for the mold sublimit and whether it is adequate for the property.

Neglect

If a covered event damages the property and you fail to take reasonable steps to prevent further damage, the carrier can deny the claim for the additional deterioration. For out-of-state investors who may not be able to respond immediately to a property emergency, this underscores the importance of having a reliable property manager or local contact who can tarp a damaged roof, shut off water to a burst pipe, or board up a broken window before the damage gets worse.

Intentional Acts

Damage caused intentionally by the insured is not covered. This is straightforward but worth noting: if a tenant causes intentional damage, that is typically covered under vandalism (which is included in a DP-3). If the landlord causes intentional damage, it is not.

War, Nuclear Hazard, and Power Failure

These are standard exclusions across virtually all property insurance policies. Power failure specifically refers to damage caused by an outage that originates off the property, such as a grid failure. If a power surge from an off-premises outage damages HVAC equipment or appliances in the rental, the base policy will not cover it. An equipment breakdown endorsement can help fill this gap.

The pattern across all of these exclusions is the same: the base DP-3 policy provides broad coverage for the dwelling, but the exclusions create specific gaps that can cost landlords thousands of dollars on a single claim. The most cost-effective way to close those gaps is through targeted endorsements added at the time the policy is quoted, not after a loss has already occurred. When you get a landlord insurance quote through OfferMarket, the in-house team reviews every quote against these benchmarks and flags any missing endorsements before the policy is bound, so you are not discovering a coverage gap for the first time when you file a claim.

DWG-3 vs. Other Dwelling Policies: DP-1 and DP-2

To fully appreciate the value of a DP-3, it's helpful to compare it to the other two common dwelling policy forms: the DP-1 and DP-2.

DP-1: Basic Form | The "Bare Minimum

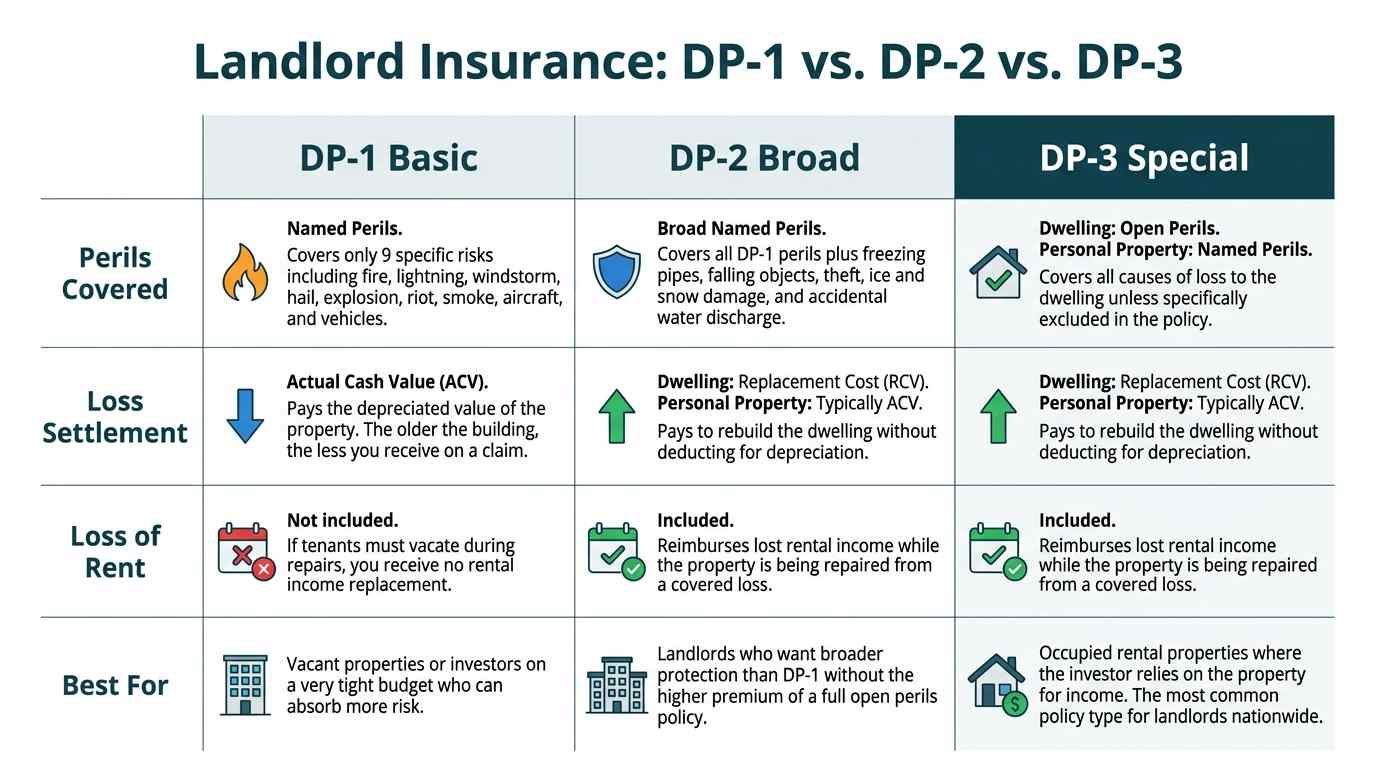

The DP-1 is the most stripped-down landlord insurance policy available. It is a "Named Peril" policy, meaning it only covers the specific risks listed in the policy document. Everything else is excluded. If the cause of damage to your rental property is not one of the listed perils, the carrier will deny the claim.

The base DP-1 covers three perils:

- 🔥 Fire

- 🌩️ Lightning

- 💥 Internal explosion

Extended Coverage (EC) Perils

The acronym WCcSHAVVER is used to help remember all of the extended coverage perils that you can add to your basic form property insurance policy:

- 🌬️ Windstorm

- 🦹♂️ Civil commotion

- 🔥 Smoke damage (if not from fire, must result from sudden damage)

- 🌨️ Hail

- ✈️ Aircraft

- 🚗 Vehicle (e.g., a car crashes into the house)

- 🌋 Volcanic action

- 💥 Explosion

- ❗ Riot

V&MM is the acronym for vandalism and malicious mischief.

- 🏚️ Vandalism

- 🦹♂️ Malicious mischief

What a DP-1 Does NOT Include

Even with Extended Coverage and V&MM added, a DP-1 leaves significant gaps that rental property investors need to understand:

- ❌ No Loss of Rent. If your tenants must vacate during repairs from a covered loss, you receive zero reimbursement for lost rental income.

- ❌ No Water Damage. Burst pipes, accidental water discharge, and freezing pipes are not covered.

- ❌ No Falling Objects. A tree falls on the property, the DP-1 does not cover it.

- ❌ No Ice, Snow, or Sleet Damage. Weight of ice or snow collapses a roof section, not covered.

- ❌ No Theft or Burglary Damage. Someone breaks in and damages the property, not covered.

How a DP-1 Pays Claims

📉 Actual Cash Value (ACV). The insurance company deducts depreciation from your payout based on the age and condition of the property. The older the building, the less you receive.

🏠 Example: A 15-year-old roof gets destroyed by a covered peril. The carrier will not pay to replace it with a new roof. They pay what a 15-year-old roof is worth today after depreciation, which could be a fraction of the actual replacement cost.

When a DP-1 Makes Sense

A DP-1 is generally only suitable in a narrow set of scenarios:

- 🏚️ Vacant properties where there is no rental income to protect and the investor only needs basic coverage to satisfy a lender requirement

- 🏷️ Properties being sold where the investor only needs short-term coverage during the disposition period

- 💰 Very low-value properties where the investor is comfortable self-insuring the gap between ACV and actual repair costs

For any occupied rental property that generates income, a DP-3 (Special Form) is the better choice. The premium difference between a DP-1 and a DP-3 is often only $200 to $500 per year, while a single denied claim under a DP-1 for an uncovered peril can cost tens of thousands of dollars.

DP-2: Broad Form | The "Middle Ground

The DP-2 is a step up from the DP-1. It is still a "Named Peril" policy, meaning it only covers risks specifically listed in the policy. However, the list of covered perils is significantly longer, and it pays claims on the dwelling at Replacement Cost Value (RCV) instead of Actual Cash Value.

A DP-2 includes all DP-1 perils plus Extended Coverage (EC) and V&MM, and adds the following:

BIG AFFECT is the acronym that insurance agents use to remember all of the broad form perils included in addition to the basic form and extended coverage perils:

- 🥷 Burglary damage

- 🧊 Ice, sleet, snow (weight of)

- 🪟 Glass breakage

- 🚰 Accidental discharge of water or steam (plumbing failures)

- 🧊 Freezing of plumbing, heating, and AC systems

- ✈️ Falling objects (trees, debris)

- ⚡ Electrical current (artificially generated)

- 🏚️ Collapse (from specific covered causes)

- 💥 Tearing asunder, cracking, burning, or bulging of heating/AC/water systems

How a DP-2 Pays Claims

This is where the DP-2 separates itself from the DP-1:

- ✅ Dwelling: Replacement Cost Value (RCV). The carrier pays to rebuild or repair the dwelling with similar materials at today's prices without deducting for depreciation. If a 15-year-old roof is destroyed by a covered peril, the carrier pays to replace it with a new roof, not a depreciated value.

- ⚠️ Personal Property: Typically Actual Cash Value (ACV). Landlord-owned appliances, fixtures, and furnishings provided to tenants are still paid at depreciated value on most DP-2 policies.

What a DP-2 Adds Over a DP-1

- ✅ Loss of Rent. If tenants must vacate during repairs from a covered loss, the DP-2 reimburses lost rental income. This alone makes the DP-2 significantly more valuable for any investor who depends on monthly cash flow.

- ✅ Water Damage. Covers sudden and accidental discharge of water or steam from plumbing, heating, or AC systems.

- ✅ Freezing Pipes. Covers damage from frozen plumbing, heating, and air conditioning systems.

- ✅ Falling Objects. A tree falls on the roof, the DP-2 covers it.

- ✅ Burglary Damage. Covers physical damage to the building caused during a break-in.

- ✅ Ice and Snow. Covers damage from the weight of ice, sleet, or snow collapsing a roof section or damaging gutters.

What a DP-2 Still Does NOT Include

Even with the broader peril list, a DP-2 has a fundamental limitation that separates it from a DP-3:

- ❌ Still a Named Perils policy. If the cause of loss is not specifically listed in the policy, the claim is denied. The burden of proof is on you, the policyholder, to prove the damage was caused by a covered peril.

- ❌ No Open Perils coverage. A DP-3 flips this: it covers everything unless it is specifically excluded. That means unexpected or unusual causes of loss that nobody anticipated are covered under a DP-3 but denied under a DP-2.

- ❌ No Water Backup. Sewer and drain backup damage is still excluded and requires a separate endorsement.

- ❌ No Flood or Earthquake. Same as DP-1, these require separate policies.

When a DP-2 Makes Sense

- 🏠 Landlords who want more protection than a DP-1 but are working within a tight budget and cannot stretch to a DP-3 premium

- 🔑 Properties where the RCV settlement on the dwelling is important but the investor does not need the broadest possible peril coverage

- 📊 Cost-conscious investors who understand the coverage gaps and are comfortable with the risk of a denied claim for an unlisted peril

For most occupied rental properties, the DP-2 is better than a DP-1 but still leaves gaps that a DP-3 (Special Form) closes. The premium difference between a DP-2 and a DP-3 is typically modest, and the jump from named perils to open perils coverage on the dwelling is the single most important upgrade an investor can make. With a DP-3, you stop worrying about whether the specific cause of loss is on a list and instead only need to check that it is not excluded.

DP-3: Special Form | The "Gold Standard

The DP-3 is the most comprehensive landlord insurance policy available for rental properties. Instead of listing what is covered, a DP-3 covers everything unless it is specifically excluded in the policy. This is the fundamental difference that separates it from every other dwelling policy. With a DP-3, you stop worrying about whether the specific cause of loss appears on a list. You only need to check that it is not excluded.

The DP-3 is also referred to as "Special Form," "Open Perils," "All Risk," or "Dwelling Fire Form 3." In Louisiana, the state-mandated forms use "DWG-3" instead of "DP-3." Same policy, different naming convention.

How a DP-3 Covers Your Property

🏠 Dwelling (Coverage A): Open Perils. The structure of the property is covered against all causes of direct physical loss unless specifically excluded. Fire, wind, hail, vandalism, burst pipes, falling objects, electrical surges, vehicle impact, and any other cause of loss that is not on the exclusion list. If it is not excluded, it is covered.

🏗️ Other Structures (Coverage B): Open Perils. Detached garages, sheds, fences, pool houses, and detached ADUs are covered on the same open perils basis as the main dwelling. Default limit is typically 10% of Coverage A.

🛋️ Personal Property (Coverage C): Named Perils. Landlord-owned appliances, fixtures, and furnishings are covered, but only for specifically listed perils such as fire, theft, and vandalism. This is a key distinction: the dwelling gets open perils, personal property gets named perils.

💸 Loss of Rent / Fair Rental Value (Coverage D): Included. If a covered loss makes the property uninhabitable and tenants must vacate during repairs, the policy reimburses your lost rental income. Default limit is typically 10% of Coverage A. OfferMarket recommends coverage for up to 12 months of rental income.

How a DP-3 Pays Claims

- ✅ Dwelling: Replacement Cost Value (RCV). The carrier pays to rebuild or repair the dwelling with similar materials at today's prices without deducting for depreciation. This is the settlement method every rental property investor should have.

- ✅ Other Structures: Replacement Cost Value (RCV). Detached structures are also settled at replacement cost.

- ⚠️ Personal Property: Replacement Cost Value (RCV). Most DP-3 policies extend RCV to landlord-owned personal property, though some carriers may default to ACV. Check your quote.

- ⚠️ Roof: Variable by Roof Age. Some carriers settle roof claims at full replacement cost regardless of age. Others switch to Actual Cash Value once the roof exceeds a certain age (commonly 10 to 15 years). This varies by carrier and is noted on your quote as "Variable by Roof Age." Ask your agent or check your policy for the specific threshold.

Liability Coverage

You may have read elsewhere that a DP-3 does not include liability coverage. That refers to the bare ISO standard form. In practice, virtually every carrier that serves landlords bundles liability into their DP-3 product automatically:

⚖️ Premises Liability. Protects you if you are found legally responsible for bodily injury or property damage at your rental property. A tenant trips on a broken step, a visitor's child is injured, a contractor gets hurt on site. Liability covers legal defense fees, settlements, and judgments.

🐕 Animal Liability Sublimit. Covers claims related to animals on the property, typically at a sublimit (commonly $10,000).

🏥 Medical Payments. Covers minor medical expenses for injuries on the property regardless of fault, typically $500 to $5,000 per person.

⚠️ The real issue is not whether liability is included. It is whether the limit is high enough. Many default DP-3 policies ship with only $100,000 or $300,000 in premises liability, which is dangerously low for a rental property. OfferMarket's coverage benchmark is $500,000 per occurrence. When you get a quote through OfferMarket, the in-house team flags any policy with liability below $500,000 and works to get it increased before the policy is bound.

What a DP-3 Covers That DP-1 and DP-2 Do Not

Because a DP-3 is open perils, it automatically covers causes of loss that a DP-1 or DP-2 would deny simply because they were not on the named perils list. Examples include:

- ✅ Accidental damage from an unusual or unexpected event that does not fit neatly into a named peril category

- ✅ Weight of people or personal property causing structural damage

- ✅ Collapse from hidden decay, insect damage, or defective construction materials

- ✅ Damage from vehicles owned by the insured (excluded under DP-1 and DP-2)

With a named perils policy (DP-1 or DP-2), the burden of proof is on you to prove the loss was caused by a listed peril. With a DP-3, the burden shifts to the insurance company to prove the cause of loss is excluded. That shift alone is worth the premium difference.

Common DP-3 Exclusions

A DP-3 covers everything except what is specifically excluded. Be sure to read your policy. Common exclusions include:

- 🌊 Flooding -- will need a separate flood insurance policy

- 🌎 Earthquake -- will need to add an earthquake "endorsement"

- 🤡 Intentional damage

- ⚠️ Building code enforcement

- 🔌 Power interruption off premises

- 🇺🇸 Government seizure

OfferMarket's DP-3 Coverage Benchmarks

When you get a landlord insurance quote through OfferMarket, the in-house team reviews every quote against these benchmarks:

- 🏠 Dwelling Coverage: Full replacement cost value with zero coinsurance

- 💵 Deductible: Flat $5,000 across all perils

- ⚖️ Premises Liability: $500,000 per occurrence minimum

- 💸 Loss of Rent: Up to 12 months of rental income

- 📋 Ordinance or Law: Included (typically 10% of dwelling coverage)

- 🚰 Water Backup: Included (typically $5,000)

- 🏗️ Loss Settlement: Replacement Cost Value on dwelling, other structures, and personal property

If any of these are missing, below benchmark, or structured in a way that would leave you exposed, the team flags it and works to correct it before the policy is bound. This is the QC layer that separates getting a quote from getting the right coverage.

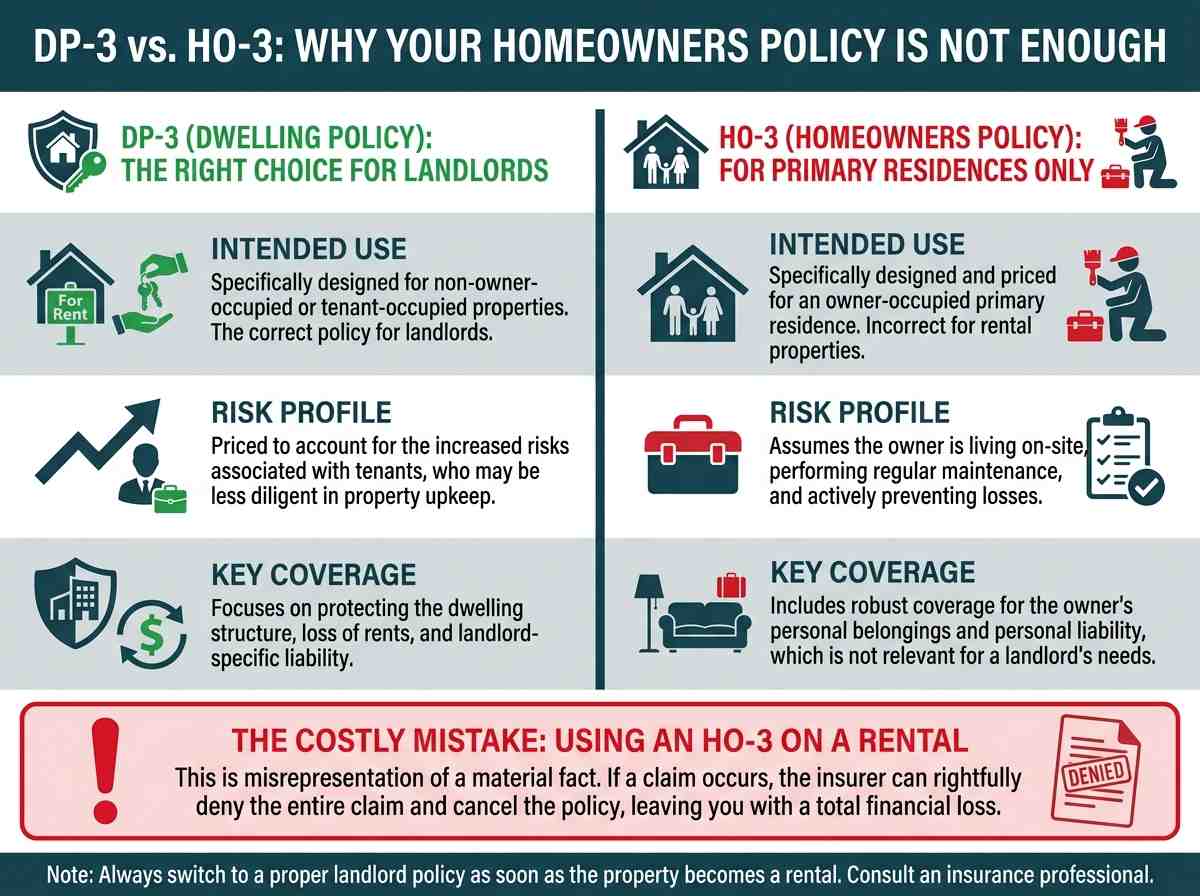

DP-3 vs. HO-3: Why Your Homeowners Policy Is Not Enough

A common and costly mistake made by new landlords is assuming their existing homeowners insurance policy (typically an HO-3) will cover their property once they move out and rent it to tenants. This is incorrect and can lead to an immediate claim denial and policy cancellation.

HO-3 (Homeowners Policy): This policy is specifically designed and priced for an owner-occupied primary residence. The risk profile assumes the owner is living on-site, performing regular maintenance, and actively preventing losses. It includes robust coverage for the owner's personal belongings and liability that follows them anywhere in the world.

DP-3 (Dwelling Policy): This policy is designed for a non-owner-occupied or tenant-occupied property. The underwriting and pricing account for the increased risks associated with tenants, who may not be as diligent in property upkeep as an owner.

Using an HO-3 on a rental property constitutes misrepresentation or concealment of a material fact to the insurer. If a fire occurs and the insurance company discovers you haven't lived there for a year, they are within their rights to deny the entire claim, leaving you with a total loss. Always switch to a proper landlord policy, like a DP-3, as soon as the property becomes a rental.

Factors That Determine Your DWG-3 Premium

The cost of a DP-3 policy can vary significantly based on a number of risk factors that insurers evaluate:

Property Location: The single biggest factor. Is the property in an area prone to hurricanes, tornadoes, hail, or wildfires? Is it in a high-crime area? Proximity to a fire hydrant and a fire station also plays a role.

Property Characteristics: The age of the home, type of construction (frame vs. masonry), and especially the age and condition of the roof are major rating factors.

Coverage Limits: Higher limits for the dwelling, liability, and loss of rent will naturally result in a higher premium.

Deductible: A higher deductible (the amount you pay out-of-pocket on a claim) will lower your premium. Common deductibles range from $1,000 to $5,000.

Claims History: If you or the property has a history of recent insurance claims, your premium will be higher.

Protective Devices: Having centrally monitored fire and burglar alarms, smoke detectors, and fire extinguishers can sometimes result in small discounts.

Is a DP-3 Right for Your Investment?

For nearly every real estate investor who owns a one-to-four-unit residential rental property, the DP-3 policy is the correct choice. It represents the industry standard for balancing comprehensive protection with reasonable cost.

The open perils coverage for the structure and replacement cost settlement provide the financial security needed to weather a significant loss and rebuild your asset without catastrophic out-of-pocket expenses. The Fair Rental Value coverage protects your income stream, and the ability to add crucial endorsements like liability and water backup allows you to create a policy that fully shields your investment. While a DP-1 might be cheaper, the coverage gaps are vast and can easily lead to a financial disaster that a slightly higher premium for a DP-3 would have prevented.

Get an Instant DWG-3 Insurance Quote

Protecting your rental property portfolio is the cornerstone of a successful real estate investment strategy. The DP-3 policy is the most effective tool for mitigating the physical and financial risks you face as a landlord.

Ready to secure the right coverage for your investment?

Get an instant online quote for a tailored DWG-3 policy in minutes.

Know You Need a DP-3. Now Get the Right One.

Shop 40+ carriers in under a minute. OfferMarket's in-house team reviews every quote for coverage gaps, flags low liability limits, and makes sure your policy meets lender requirements before it is bound.

Get Insurance Quote →

OfferMarket Loans

Check your rate

60 seconds · no credit pull