*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

DSCR Rates

Last updated: 5 minutes ago

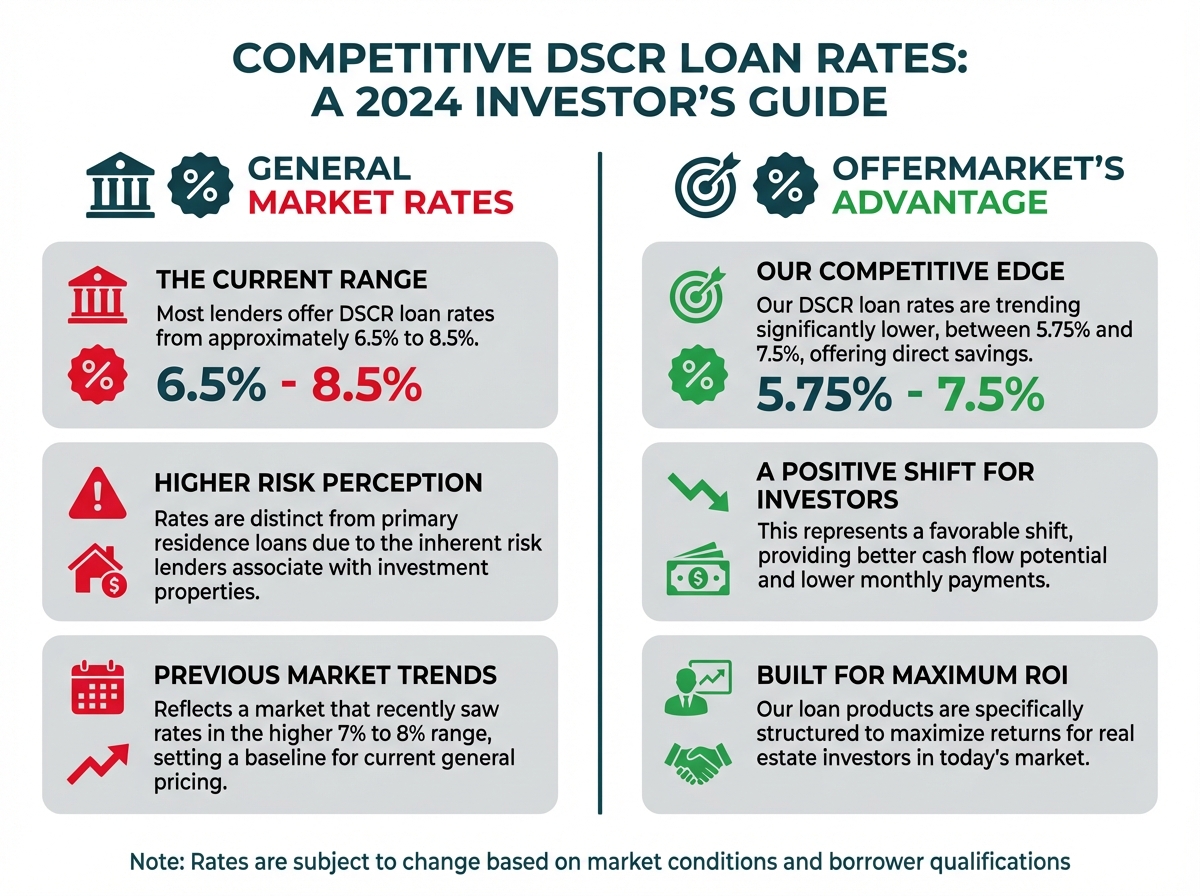

Current DSCR Rates

OfferMarket, via OfferMarket Capital LLC, is a leading DSCR lender for 1-4 unit residential properties. Since 2022, OfferMarket has been publishing the DSCR Loan Interest Rate Index™, a proprietary index that estimates the national average DSCR rate.

Disclaimer: The DSCR Loan Interest Rate Index and associated market credit spread and OfferMarket credit spread are approximations based on best available data and are not a guarantee of interest rate pricing for your particular scenario. Your interest rate may be higher or lower than the index indicates.

DSCR Rates Comparison

How are DSCR rates priced?

DSCR rates are calculated based on the current 5 Year US Treasury (the "risk free rate") plus a credit spread (the "risk premium"). It's important for rental investors to understand how DSCR rates are priced, as this will help with the timing and structuring of your DSCR loan transactions.

A helpful way to think about DSCR rates is the production line analogy. Most DSCR loans are originated by a private lender, sold to an aggregator, bundled with hundreds of other DSCR loans into a securitization, and then sold to fixed income investors such as an insurance company, mortgage REIT or credit fund which we will refer to as "end investor". In some cases, the loan is sold directly to an end investor. Each step of the way, there are profit motivated companies that are capturing value. From month to month, the appetite of aggregators and end investors may change, in some cases substantially. An example is that in November 2024, one of the largest aggregators which was the most competitive in the market decided to stop purchasing DSCR loans because they had met their annual target early. Overnight, the credit spread increased by 30 basis points (0.3%) as the next most competitive "takeouts" were pricing much less aggressively. This is why it's so important to work with low-cost private lenders that have access to multiple low-cost, competitive aggregators and insurance companies.

Current 5 Yr US Treasury

Current Market Credit Spread

Current OfferMarket Credit Spread

OfferMarket's credit spread is consistently -0.1% to -0.25% below the national average. This is because we pass on the lowest available credit spread offered by the institutional capital providers on our platform and we make these capital providers compete for deal flow.

How to get the lowest DSCR rate?

Work with the most competitive DSCR lender

It's important to note that the interest rate is not the only factor you should be considering. It's important to calculate the APR (factors in lender fees) and understand other important loan terms such as prepayment penalty and LTV, as many DSCR lenders advertise competitive interest rates only for you to find out that they are charging higher than market lender fees (origination fee, underwriting, doc prep or other "junk fees"). Comparing loan terms can be a bit like comparing apples to oranges. OfferMarket onboarding specialists are always happy to help you compare term sheets or quotes to make sure you get the best possible loan terms with no surprises.

Structure your loan properly

Prepayment penalty Unless you're in a state that has limitations on prepayment penalties, if you absolutely do not plan to sell or refinance the property in the next 5 years, you can accept a higher prepayment penalty in exchange for a lower rate.

LTV While DSCR rate sheets from institutional credit investors change daily, it's not uncommon for there to be a large increase in credit spread for max LTV. Unless you absolutely want/need max LTV, it's worth considering 5% lower LTV in order to get a significantly lower interest rate.

Monitor the 5 Yr Treasury The 5 Year US Treasury has a tendency to "overshoot" on the downside and the upside and then revert to the mean. If you start to see aggressive downward moves in the 5 Yr Treasury, there's a good chance the market will eventually bounce higher. This is especially true during times of unprecedented economic uncertainty.

Market expectations for Federal Reserve actions, such as future fed funds rate cuts, are typically already reflected in the 5-year Treasury yield. This can confuse rental property investors who, on the day of a Fed rate cut, might ask, "The Fed cut rates by 0.25%, so why hasn't my quote decreased by 0.25%?" The reason lies in market dynamics: leading up to the Fed's decision, the 5-year Treasury yield already incorporates the anticipated 0.25% rate cut, as well as expectations for future cuts. However, if the Fed's press conference or "dot plot" projections signal a more conservative approach to rate cuts, the market may react by selling off Treasuries, driving yields higher as expectations adjust.

Unexpected economic data can further amplify volatility in the 5-year Treasury yield. For instance, if the Consumer Price Index (CPI) exceeds market forecasts, investors may anticipate that the Fed will delay rate cuts, prompting a sharp upward repricing of the 5-year Treasury. The complex interplay of economic indicators, Fed guidance, and geopolitical tensions can lead to significant fluctuations in Treasury yields, which directly impact mortgage rates, including DSCR loans.

If you feel the market is overly optimistic about Fed rate cuts, and you have a time sensitive transaction, you may want to push forward with your financing before the market revises expectations. This said, timing the market can be mentally exhausting and ultimately unsuccessful. Worse, it can be a major distraction from your core objective of growing your rental portfolio. The best rental investors tend to be those who are less sensitive to interest rate, less likely to wait and attempt to time the market, and more likely to focus on establishing consistent, high quality deal flow (which is typically off market properties).

Comparing DSCR Loan APR

To effectively compare DSCR loan term sheets, you need to go beyond the stated interest rate and calculate the Annual Percentage Rate (APR) for each offer. Since these loans lack the standardized Loan Estimate (LE) and Closing Disclosure (CD) required for regulated mortgages, lenders can present fees differently, making direct comparison challenging.

The APR provides a single, consistent metric because it incorporates the interest rate plus most closing costs, such as origination fees, discount points, and lender-specific administrative fees, converting them into an equivalent annual cost.

Start by collecting all fee information from each lender's term sheet. The key is to identify all charges paid to the lender or for lender services that are typically included in the APR calculation. Third-party costs (like title insurance, appraisal, or attorney fees) are usually excluded, but a conservative approach is to include all lender-side costs.

Use an online APR calculator to input the loan amount, the interest rate, the loan term, and the total of the relevant closing costs. Comparing the resulting APRs will give you a true "apples-to-apples" comparison, revealing the most cost-effective loan despite varying fee structures. A lower APR indicates a cheaper loan overall. It's crucial to confirm with each lender exactly which fees are included in their internal APR calculation, if provided, to ensure consistency in your own calculations. Never rely solely on the stated interest rate.

Let's take a look at an example:

| Lender A | Lender B | |

|---|---|---|

| Loan amount | $200,000 | $200,000 |

| Loan term (years) | 30 | 30 |

| Interest rate | 6.5% | 6.625% |

| Origination fee | 2% | 1% |

| Legal/doc prep fee | $995 | $995 |

| Underwriting fee | $995 | $0 |

| APR | 6.795% | 6.772% |

Lender B is actually providing a better term sheet. However, choosing a lender strictly based on APR can lead rental property investors to negative outcomes. Some DSCR lenders are easy to work with and provide exceptional, expert client service and differentiated offerings (i.e. cash out refi no seasoning).

Instant DSCR Rates

OfferMarket is a real estate investing platform focused on serving rental property investors. Our core business is DSCR lending and we focus exclusively on 1-4 unit residential properties in non-rural markets.

We hope you will accept our invitation to join us and over 20,000 registered members.

Membership is entirely free and comes with the following benefits:

🏚️ Off market properties 💰 Private lending ☂️ Landlord insurance rate shopping 💡 Market insights

Our mission is to help you build wealth through real estate and we look forward to contributing to your success!

OfferMarket Loans

Check your rate

60 seconds · no credit pull