*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

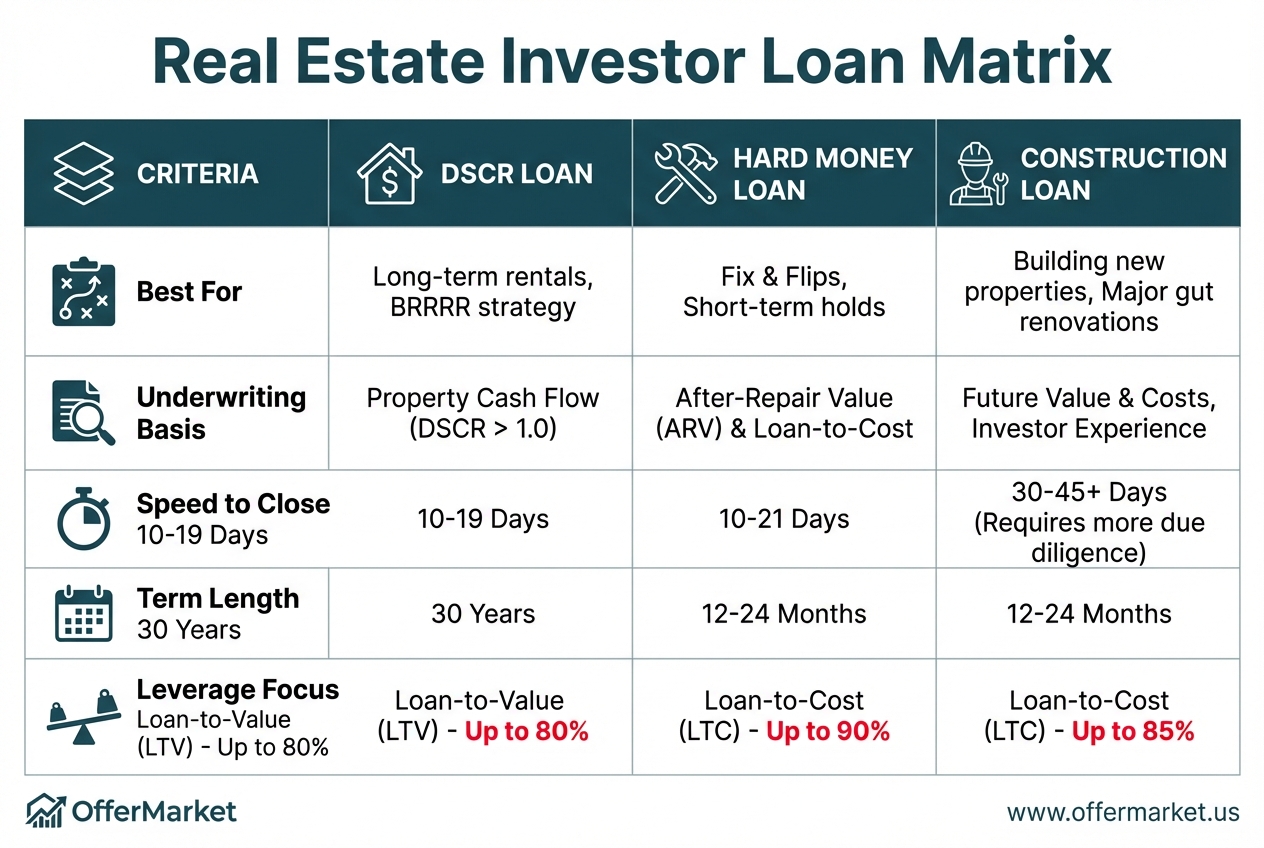

DSCR Meaning

Last updated: October 20, 2025

The Debt Service Coverage Ratio (DSCR) is a financial metric that measures an asset’s ability to support debt based on its generated cash flow. Lenders use DSCR to assess the suitable loan amount for an investment property or business. While applicable across various industries to evaluate asset-backed loans, this guide focuses specifically on its use for real estate investors.

DSCR Formulas

Two distinct formulas for calculating the Debt Service Coverage Ratio (DSCR) yield slightly different results. Therefore, it’s essential to identify which DSCR formula is appropriate for your specific situation.

[ ](https://www.offermarket.us/blog/dscr-formula?ref=content-dscr-meaning

](https://www.offermarket.us/blog/dscr-formula?ref=content-dscr-meaning

| Formula | Rent ÷ PITIA | NOI ÷ Debt Service |

|---|---|---|

| Property types | 1-4 unit residential | multifamily (5+ unit), commercial, industrial |

| Lender type | private lenders | private lenders, banks, credit unions |

Evaluating DSCR

A DSCR greater than 1.0 indicates positive cash flow after covering loan expenses, whereas a DSCR less than 1.0 signifies negative cash flow. A DSCR of 1.0 represents a breakeven point for cash flow.

As most DSCR loans utilize method 1 (Rent ÷ PITIA), we will concentrate on this formula while discussing insights and example scenarios.

| Meaning | |

|---|---|

| > 1.0 | Positive cash flow |

| 1.0 | Breakeven cash flow |

| < 1.0 | Negative cash flow |

DSCR Exceeding 1.0

A DSCR above 1.0 indicates that the property produces positive free cash flow, meaning its rental income surpasses its expenses. If you maintain a dedicated bank account for the property, you should see the cash balance grow monthly, unless one or more of the following occurs:

- Tenant fails to pay rent

- Property taxes rise

- Insurance premiums go up

- Maintenance is needed

- Property management fees increase

DSCR of 1.0

A DSCR of 1.0 indicates that the property achieves breakeven cash flow, where rental income matches the property’s expenses. If you maintain a dedicated bank account for the property, the cash balance should remain steady each month, unless one or more of the following occurs:

- Tenant fails to pay rent

- Rent rises

- Property taxes change (increase or decrease)

- Insurance premiums change (increase or decrease)

- Maintenance is needed

- Property management fees change (increase or decrease)

DSCR Less Than 1.0

A DSCR below 1.0 indicates that the property produces negative free cash flow, meaning its rental income falls short of its expenses. If you maintain a dedicated bank account for the property, you should expect the cash balance to decrease monthly (which is risky!) unless one or more of the following occurs:

- Rent increases

- Property taxes decrease (unlikely!)

- Insurance premiums decrease

- Property management fees change (increase or decrease)

DSCR Calculations

High DSCR

Suppose you're acquiring a single-family rental (SFR) with a DSCR loan, aiming for the lowest possible down payment and thus the highest possible loan-to-value (LTV) ratio. You discover a DSCR lender named OfferMarket and receive the following quote:

- Purchase price: $200,000

- Loan amount: $160,000 (80% LTV)

- Interest rate: 6.25%

- Annual property taxes: $2,000

- Annual insurance: $1,000

- Annual HOA fees: $0

- Monthly rent: $2,000

- Monthly loan payment: $1,261

- DSCR: 1.59

In this scenario, the property generates $739 in monthly free cash flow, which most rental property investors would consider a strong starting point, allowing for potential rent increases over time.

Low DSCR

Suppose you're a BRRRR method investor pursuing a cash-out refinance with no seasoning. You aim for a 75% LTV, but your DSCR is too low, suggesting you may need to reduce your LTV to qualify for the DSCR loan.

| Criteria | 75% LTV | 70% LTV |

|---|---|---|

| Interest rate | 6.50% | 6.25% |

| Loan amount | $150,000 | $140,000 |

| DSCR | 0.95 | 1.01 |

| Cash out proceeds | $141,000 | $132,000 |

| Loan commitment | No, DSCR too low | Yes |

In this scenario, the DSCR at 75% LTV falls below the industry-standard minimum of 1.0. Even if a DSCR lender permits a DSCR under 1.0, this is not advisable from a risk management standpoint. At OfferMarket, we highly recommend maintaining a DSCR of 1.1 or above, as a DSCR of 1.0 does not allow for building cash reserves to cover inevitable maintenance costs and vacancies that should be budgeted for.

DSCR Loan

The DSCR loan is a rapidly expanding financing option for rental property investors, with qualification based solely on the property’s DSCR and the borrower’s credit score, rather than verified income sources like W-2s or tax returns.

OfferMarket: Real Estate Investing Platform

OfferMarket is a platform dedicated to supporting rental property investors, small builders, and flippers, specializing exclusively in 1-4 unit residential properties in non-rural markets.

We invite you to join our community of over 20,000 registered members. Membership is completely free and includes the following benefits:

- 🏚️ Off-market properties

- 💰 Private lending options

- ☂️ Landlord insurance rate comparison

- 💡 Market insights

Our mission is to empower you to build wealth through real estate, and we are excited to contribute to your success!

OfferMarket Loans

Check your rate

60 seconds · no credit pull