*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

DSCR Loans Explained: Unlocking Investment with Cash Flow-Based Financing

Last updated: Jan 5, 2025

In the dynamic realm of real estate investment, securing financing is often one of the most significant hurdles investors face. Traditional mortgage loans typically require substantial down payments, which can limit the ability to diversify or expand a property portfolio. However, the emergence of Debt Service Coverage Ratio (DSCR) loans with no down payment is revolutionizing the landscape, providing investors with new avenues to maximize their investments while minimizing upfront costs. This comprehensive guide explores DSCR loans, their benefits, eligibility criteria, application process, potential risks, and future trends, empowering you to make informed decisions in your real estate ventures.

Understanding DSCR: The Foundation of DSCR Loans

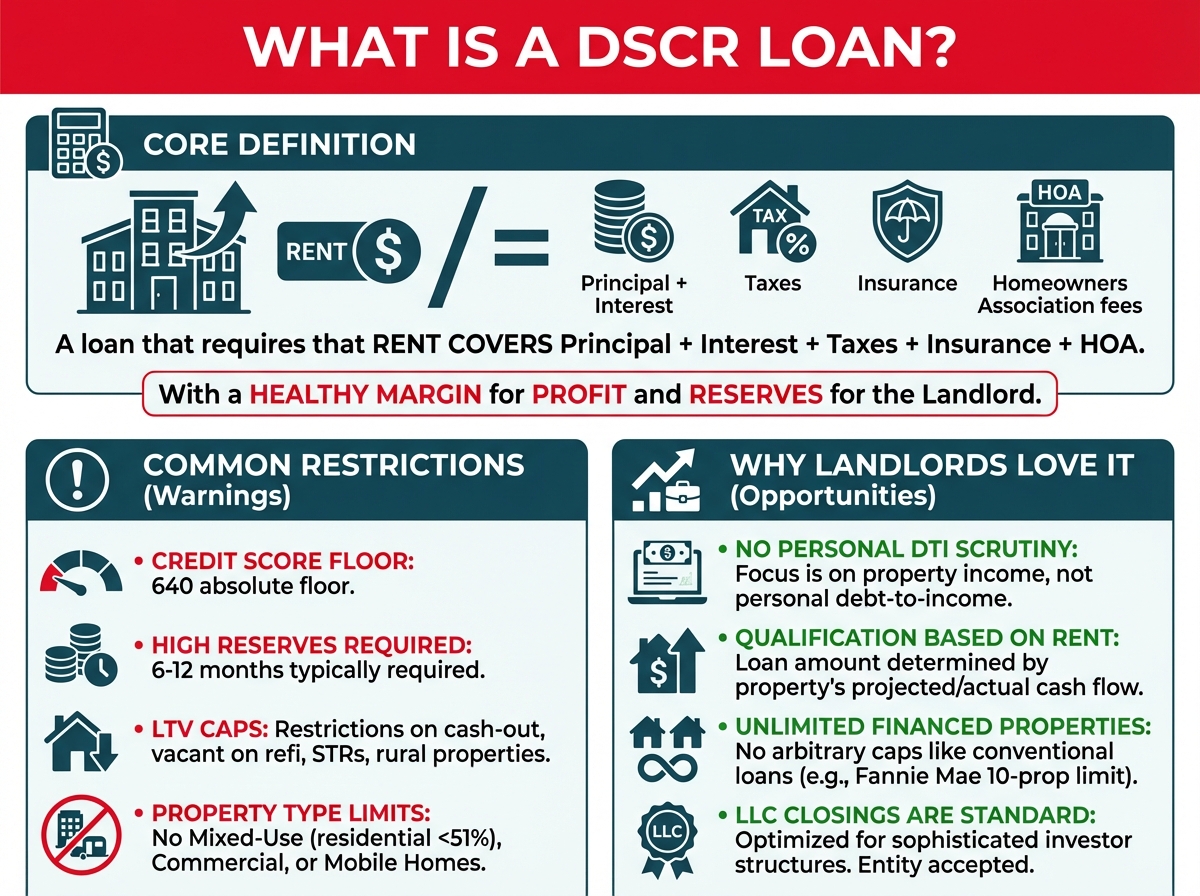

Debt Service Coverage Ratio (DSCR) is a critical financial metric used by lenders to assess a property's ability to generate enough income to cover its debt obligations. Essentially, it measures the cash flow available to pay current debt obligations. The formula for calculating DSCR is straightforward:

DSCR= Net Operating Income (NOI)/Total Debt Service

- Net Operating Income (NOI): This is the income generated from the property after deducting operating expenses such as maintenance, taxes, and management fees but before deducting taxes and interest.

- Total Debt Service: This encompasses all principal and interest payments required to service the loan.

A DSCR of 1.0 indicates that the property generates just enough income to cover its debt obligations. Lenders typically seek a DSCR greater than 1.0, commonly 1.2 or higher, to ensure there is a buffer to cover unexpected expenses or income fluctuations.

What is a DSCR Loan?

A Debt Service Coverage Ratio (DSCR) loan is a type of commercial real estate financing that focuses on the property's ability to generate sufficient income to cover its debt obligations, rather than the borrower's personal income or creditworthiness. This distinction makes DSCR loans particularly attractive to real estate investors who may not have substantial personal income but possess income-generating properties.

DSCR loans are classified as Non-Qualified Mortgages (Non-QM) and qualify borrowers based solely on the property’s cash flow, not their personal income. Qualification is based on the Debt Service Coverage Ratio (DSCR), calculated as:

DSCR = Gross Rental Income / PITIA (Principal, Interest, Taxes, Insurance, and HOA fees)

Most lenders require a minimum DSCR of 1.0–1.2, depending on borrower profile and loan structure.

Key Features of DSCR Loans:

Property-Centric Evaluation: Lenders assess the property's income-generating potential rather than the borrower's financial standing.

No Down Payment Options Advantage of No Down Payment: DSCR loans typically require a down payment ranging from 20% to 35%, depending on property type and borrower credit score. The maximum Loan-to-Value (LTV) is usually 80% for purchases and 75% for cash-out refinances.

While DSCR loans do not require personal income documentation like W-2s or tax returns, investors must contribute substantial equity. No-down-payment options do not apply to DSCR loans; these are different from products like OfferMarket’s “Slow Flip” loan.

Flexible Terms: DSCR loans often come with more flexible terms tailored to the property's cash flow.

Higher Loan Amounts: Given the focus on the property's income, DSCR loans can sometimes offer higher loan amounts compared to traditional mortgages.

The Advantage of No Down Payment

Traditionally, securing a loan for real estate investment requires a down payment, typically ranging from 20% to 30% of the property's purchase price. This substantial upfront cost can limit an investor's ability to acquire multiple properties or allocate funds to other critical areas such as property improvements or reserves.

Benefits of DSCR Loans with No Down Payment

- Lower Initial Investment: As mentioned, eliminating the down payment reduces the capital required to invest in real estate, allowing for greater flexibility in investment strategies.

- Leverage Opportunities: Investors can use the same capital to finance multiple properties, increasing potential returns through portfolio diversification.

- Focus on Cash Flow: DSCR loans prioritize the property's income, encouraging investors to focus on properties that generate strong cash flow, enhancing long-term profitability.

- Flexibility in Loan Terms: DSCR loans often offer negotiable terms, such as varying repayment periods and interest rates, tailored to the specific income profile of the property.

- Credit Neutrality: Since the loan is based on the property's performance, investors with less-than-perfect personal credit can still secure financing, broadening the pool of potential investors.

- Potential Tax Benefits: Interest payments on DSCR loans are often tax-deductible, providing additional financial incentives for investors.

- Preservation of Personal Assets: By relying on the property's income rather than personal income or assets, investors can protect their personal wealth from potential business liabilities.

Eligibility Criteria for DSCR Loans

While DSCR loans with no down payment offer numerous advantages, they come with specific eligibility requirements that investors must meet to secure financing:

- Sufficient Property Income:

- The property must generate enough income to cover its debt obligations, typically reflected by a DSCR of at least 1.2.

- Lenders will analyze current and projected income streams to ensure the property's viability.

- Property Type:

- Lenders usually finance income-producing properties such as multifamily apartments, commercial office buildings, retail spaces, and rental homes.

- Certain property types may be preferred based on market demand and stability.

- Loan-to-Value (LTV) Ratio:

- While no down payment is required, lenders may set maximum LTV ratios to mitigate risk, often around 80-85%.

- A higher LTV ratio means more leverage but also higher risk for both borrower and lender.

- Investor Experience:

- Investors with a proven track record in real estate are favored, as experience indicates the ability to manage and maintain income-generating properties effectively.

- First-time investors may still qualify but might face stricter scrutiny or higher interest rates.

- Comprehensive Documentation:

- Detailed financial records, including property financials, rent rolls, maintenance records, and market analysis, are essential.

- Lenders require transparency to accurately assess the property's income potential and risk factors.

- Market Conditions:

- The property's location and the overall market conditions play a significant role in loan approval.

- Properties in stable or growing markets with high demand are more likely to be approved.

- Legal Compliance:

- A minimum FICO score of 620 is required to qualify.

- OfferMarket generally prefers 680+ for more favorable terms (better interest rates, higher LTV).

- Credit scores between 660–679 may be considered case-by-case.

- All guarantors undergo a background check. Any history of foreclosure, bankruptcy, late payments, or liens may trigger higher reserve requirements or ineligibility. the property's operation.

- Property Appraisal:

- An independent appraisal is typically required to verify the property's value and income-generating potential.

- The appraisal helps determine the LTV ratio and overall loan terms.

How to Secure a DSCR Loan with No Down Payment

Securing a DSCR loan with no down payment involves a strategic approach that emphasizes the property's income-generating potential and thorough preparation of financial documentation. Here's a step-by-step guide to help you navigate the process:

1. Assess Property Income Potential

Before seeking financing, it's essential to evaluate the income potential of the property you're interested in. Consider the following:

- Current Rent Rolls: Analyze existing leases to understand current income streams.

- Occupancy Rates: High occupancy rates indicate stable income, while low rates may signal potential challenges.

- Market Rent Comparisons: Ensure that the property's rents are competitive within the local market to attract and retain tenants.

- Potential for Rent Increases: Identify opportunities for future rent hikes based on market trends and property improvements.

2. Calculate DSCR

Determine the property's DSCR to assess its capacity to cover debt obligations. A higher DSCR provides a safety margin, ensuring the property can handle unexpected expenses or income fluctuations. Aim for a DSCR of at least 1.2, which indicates that the property generates 20% more income than required to service the debt.

3. Prepare Comprehensive Financial Documentation

Lenders require detailed financial records to assess the property's viability. Prepare the following documents:

- Tax Returns: Provide personal and property-specific tax returns for the past few years.

- Profit and Loss Statements: Detailed statements showing income and expenses related to the property.

- Rent Rolls: A list of all tenants, lease terms, and rental income.

- Maintenance Records: Documentation of ongoing maintenance and repairs.

- Operating Expenses: Breakdown of costs such as utilities, insurance, property management fees, and taxes.

4. Choose the Right Lender

Not all lenders offer DSCR loans with no down payment. Research and identify financial institutions that specialize in commercial real estate financing. Consider the following when selecting a lender:

- Reputation: Choose lenders with a strong track record in DSCR lending.

- Loan Terms: Compare interest rates, repayment periods, and other loan conditions.

- Customer Service: Opt for lenders known for responsive and supportive customer service.

- Flexibility: Seek lenders willing to negotiate terms based on the property's performance and your investment strategy.

5. Negotiate Loan Terms

Once you've identified potential lenders, engage in negotiations to secure favorable loan terms. Leverage the property's strong performance and your comprehensive financial documentation to negotiate:

- Interest Rates: Aim for the lowest possible rates to minimize borrowing costs.

- Repayment Periods: Choose terms that align with your cash flow projections and investment goals.

- Covenants: Understand and negotiate any covenants or conditions attached to the loan.

- Prepayment Options: Inquire about penalties or fees for early repayment, providing flexibility in managing debt.

6. Undergo Property Appraisal

Lenders will require an independent appraisal to verify the property's value and income-generating potential. The appraisal process involves:

- Site Visit: An appraiser inspects the property to assess its condition, amenities, and overall appeal.

- Market Analysis: Evaluating comparable properties in the area to determine market value.

- Income Assessment: Reviewing the property's income streams to ensure they align with lender expectations.

7. Finalize the Loan Agreement

Upon approval, carefully review the loan agreement to ensure all terms align with your investment strategy. Pay attention to:

- Interest Rate Structure: Fixed vs. variable rates and their implications on your payments.

- Repayment Schedule: Monthly, quarterly, or annual payment structures.

- Fees and Penalties: Understand all associated costs, including origination fees, closing costs, and penalties for late payments or defaults.

- Legal Clauses: Ensure clarity on all legal terms and conditions to avoid future disputes.

DSCR Loan Documentation Checklist

To apply for a DSCR loan, borrowers must typically provide:

Articles of Organization / Operating Agreement (LLC or Corporation)

Certificate of Good Standing

IRS EIN Letter or W-9

Credit Report and Background Check for all guarantors

Property Appraisal Report

Rent Roll and Lease Agreements

Bank Statements (last 2 months)

Insurance and Title Documentation

Understanding Loan-to-Value (LTV) and Down Payment

DSCR lenders use the Loan-to-Value (LTV) ratio to determine how much they are willing to lend. For example:

If a property is worth $200,000 and the lender caps LTV at 80%, the loan amount would be $160,000.

The remaining $40,000 would be the borrower’s down payment.

Most DSCR loans require a minimum down payment of 20%, though higher down payments may apply for riskier properties or lower credit scores.

Comparing DSCR Loans with Traditional Mortgages

To appreciate the unique advantages of DSCR loans, it's helpful to compare them with traditional mortgage loans. The table below highlights the key differences:

| Feature | DSCR Loans | Traditional Mortgages |

|---|---|---|

| Focus | Property's income-generating potential | Borrower's personal credit and income |

| Down Payment | Often no down payment required | Typically requires 20% down |

| Eligibility | Based on DSCR and property performance | Based on credit score, income, and debt-to-income ratio |

| Interest Rates | Generally higher | Typically lower |

| Loan Terms | More flexible, tailored to property cash flow | Standardized terms based on borrower profiles |

| Best For | Experienced real estate investors with income-producing properties | Homebuyers and investors with strong personal credit and capital |

| Loan Amounts | Can be higher due to focus on property income | Limited by borrower's personal financials |

| Approval Time | May take longer due to detailed property analysis | Often quicker with standardized processes |

Key Takeaways:

- DSCR Loans are ideal for investors focusing on the property's performance rather than personal financial standing.

- Traditional Mortgages are more suited for individuals with strong personal credit and sufficient capital for down payments.

- Interest Rates: DSCR loans typically come with higher interest rates due to the increased risk from no down payment.

- Flexibility: DSCR loans offer more tailored terms, accommodating various investment strategies and property types.

DSCR Loans vs. Other OfferMarket Loan Products

It’s important to distinguish DSCR loans from other financing options:

DSCR Loans: Designed for stabilized rental properties; qualify based on cash flow; require 20–35% down.

Fix and Flip / Hard Money Loans: Short-term, interest-only loans for acquiring and rehabbing properties.

Fix and Rent Loans: A bundled product combining a hard money loan (for purchase/rehab) with a DSCR refinance once the property is stabilized and leased.

Slow Flip Loans: May have very low upfront capital requirements, but are not DSCR loans and have specific structuring (contract for deed, longer holding periods).

Potential Risks and Mitigation Strategies of Dscr Loans with no Down Payment

While DSCR loans with no down payment present significant opportunities, they also come with inherent risks that investors must navigate to ensure long-term success.

1. Income Fluctuations

Risk: Economic downturns, tenant vacancies, or rent defaults can reduce the property's income, making it challenging to service the debt.

Mitigation Strategies:

- Diversified Tenant Base: Avoid reliance on a single tenant or industry, spreading risk across multiple income sources.

- Reserve Funds: Maintain a reserve fund to cover unexpected expenses or temporary income shortfalls.

- Market Research: Invest in properties located in stable or growing markets with high demand and low vacancy rates.

- Lease Agreements: Secure long-term leases with reliable tenants to ensure consistent income streams.

2. Higher Interest Rates

Risk: DSCR loans often come with higher interest rates compared to traditional mortgages, increasing borrowing costs and impacting profitability.

Mitigation Strategies:

- Rate Negotiation: Negotiate the best possible interest rates with lenders, leveraging the property's strong income performance.

- Fixed vs. Variable Rates: Consider fixed-rate loans to lock in rates and avoid future increases associated with variable rates.

- Refinancing Options: Monitor market conditions and consider refinancing when interest rates become more favorable.

- Cash Flow Management: Ensure robust cash flow projections that can accommodate higher interest payments without straining finances.

3. Property Management Challenges

Risk: Effective property management is crucial to maintaining income streams. Poor management can lead to increased vacancies, maintenance issues, and tenant dissatisfaction.

Mitigation Strategies:

- Professional Management: Hire experienced property managers or management companies to handle day-to-day operations efficiently.

- Maintenance Plans: Implement regular maintenance schedules to prevent costly repairs and maintain property value.

- Tenant Relations: Foster positive relationships with tenants to encourage lease renewals and reduce turnover.

- Technology Utilization: Use property management software to streamline operations, track expenses, and monitor performance metrics.

4. Market Volatility

Risk: Real estate markets can be unpredictable, with fluctuations in property values and rental demand impacting investment returns.

Mitigation Strategies:

- Market Analysis: Conduct thorough market research to understand trends, demand, and economic indicators influencing the real estate sector.

- Geographical Diversification: Invest in properties across different regions to spread risk and reduce exposure to localized market downturns.

- Flexible Investment Strategies: Be prepared to adapt investment strategies based on market conditions, such as shifting focus to different property types or investment models.

- Long-Term Planning: Maintain a long-term investment perspective, allowing time to weather market fluctuations and capitalize on recovery periods.

5. Regulatory and Legal Risks

Risk: Changes in zoning laws, building codes, or rental regulations can affect property operations and profitability.

Mitigation Strategies:

- Legal Compliance: Stay informed about local regulations and ensure all properties comply with zoning laws, building codes, and rental regulations.

- Legal Counsel: Engage legal professionals to navigate complex regulatory environments and address any legal challenges promptly.

- Insurance Coverage: Obtain comprehensive insurance coverage to protect against legal liabilities and unforeseen events.

Strategic Tips for Maximizing DSCR Loan Benefits

To fully leverage the advantages of DSCR loans with no down payment, consider implementing the following strategic tips:

1. Choose High-Performing Properties

Invest in properties with strong income potential, low vacancy rates, and opportunities for rent increases. Conduct thorough due diligence to ensure the property's financial health and market position.

2. Optimize Property Management

Effective property management is crucial for maintaining and enhancing income streams. Implement efficient management practices, invest in property upgrades, and foster positive tenant relationships to ensure long-term profitability.

3. Maintain Strong Financial Records

Accurate and comprehensive financial documentation is essential for securing DSCR loans. Keep meticulous records of income, expenses, maintenance activities, and tenant information to facilitate the loan application process.

4. Build Relationships with Specialized Lenders

Develop relationships with lenders who specialize in DSCR financing. These lenders are more likely to understand your investment strategy and offer tailored loan products that align with your goals.

5. Diversify Your Portfolio

Spread your investments across different property types and locations to mitigate risk and enhance overall portfolio performance. Diversification can provide stability and reduce the impact of market fluctuations on your investments.

6. Monitor Market Trends

Stay informed about real estate market trends, economic indicators, and regulatory changes that could impact your investments. Adapt your strategies accordingly to capitalize on emerging opportunities and navigate potential challenges.

7. Leverage Technology

Utilize property management software, financial analysis tools, and data analytics to streamline operations, enhance decision-making, and optimize property performance. Technology can provide valuable insights and improve overall efficiency.

8. Plan for Contingencies

Prepare for unexpected events by maintaining reserve funds, securing adequate insurance coverage, and developing contingency plans. Being prepared can help you navigate challenges without jeopardizing your investments.

9. Seek Professional Advice

Engage with real estate advisors, financial planners, and legal professionals to guide your investment decisions and ensure compliance with regulatory requirements. Professional expertise can enhance your investment strategy and mitigate risks.

10. Continuously Educate Yourself

Stay updated on the latest developments in DSCR financing, real estate investment strategies, and market dynamics. Continuous education empowers you to make informed decisions and stay competitive in the real estate market.

Conclusion

DSCR loans with no down payment represent a transformative opportunity for real estate investors seeking to expand their portfolios with minimal upfront capital. By focusing on the property's income-generating potential rather than the borrower's personal financial standing, these loans democratize access to commercial real estate investment, allowing both seasoned investors and newcomers to capitalize on lucrative opportunities.

However, success with DSCR loans requires careful property selection, thorough financial analysis, and strategic management to mitigate inherent risks. Investors must stay informed about market trends, maintain robust financial records, and foster strong relationships with specialized lenders to maximize the benefits of DSCR financing.

As the real estate market continues to innovate and adapt, DSCR loans are poised to become even more integral to investment strategies, offering flexible and efficient financing solutions tailored to the evolving needs of investors. While DSCR loans eliminate the need for income documentation, they do not eliminate the need for a down payment or credit review. It’s important to work with a knowledgeable lender to understand how your credit score, property cash flow, and market conditions affect your terms. Embracing DSCR loans with no down payment can unlock new avenues for growth, diversification, and long-term profitability in the competitive world of real estate investment.

DSCR Loan Quote

Our mission is to help you build wealth through real estate. Let's grow and optimize your rental property portfolio!

- Get your instant DSCR loan quote today!

- Save big on premiums with our landlord insurance rate shopping service!

- Interested in exclusive investment opportunities? Browse off market properties now!

- Join our Facebook community to stay up-to-date with the latest platform updates and market insights.

- Subscribe to our Youtube channel for our monthly DSCR loan update.

OfferMarket Loans

Check your rate

60 seconds · no credit pull