*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Understanding DSCR Loan Rate Volatility and Prepayment Penalty Strategy

Last update: March 15, 2025

What’s up everyone, this is Daniel Sperling-Horowitz with OfferMarket, and today I want to talk about our DSCR Loan Interest Rate Prediction.

Actually, I’d like to clarify that anyone who thinks they can predict interest rates is probably in for a rude awakening. So, what we’re advising our clients—rental property investors and those on the fix-and-flip side of our private lending business—is to seriously consider lower prepayment penalty options. Specifically, when focusing on DSCR loans, the DSCR Loan Interest Rate Prediction can be challenging, but understanding prepayment penalties and structuring loans accordingly can help investors make more informed decisions.

If you're a real estate investor looking for financing options, a DSCR loan might be the solution you need. Unlike traditional loans that rely on your personal income, a DSCR (Debt Service Coverage Ratio) loan evaluates the cash flow generated by your investment property. This makes it an ideal choice for investors with variable income or those who own multiple rental properties. DSCR loans don’t require personal income verification like W-2s or tax returns. However, borrowers must meet other documentation requirements including credit check, background report, and property income documentation.

DSCR loans are designed to help you qualify based on your property's financial performance, not your personal finances. Whether you're looking to purchase a new property, refinance an existing one, or access cash-out options, this loan type offers flexibility and faster approval times. If you're ready to explore a financing option tailored to your investment goals, a DSCR loan could be the key to unlocking your next opportunity.

DSCR Loan Interest Rate Market Update

DSCR interest rates are currently volatile due to inflation uncertainty, Fed policy shifts, and strong labor market data. We expect elevated rates (7–8%+) to persist through 2025. So before we get into prepayment penalties, I just want to provide a quick update on DSCR Loan Interest Rate Predictions. Our benchmark for gauging DSCR loan pricing trends is the 5-Year US Treasury yield, not conventional mortgage rates. While there may be short-term correlation, DSCR rates are largely influenced by capital market dynamics and perceived credit risk., which, as of this morning—and certainly as of yesterday—was at 6.65%, down from a peak of around 7.3%. Over the last few weeks, we saw a convergence between the 30-year fixed-rate conventional mortgage and the DSCR Loan Interest Rate. For prime borrowers, we were quoting nearly the same rate on the DSCR loan side. Last week, we were quoting 7.2%, and sometimes even lower than 7.2% when the 30-year fixed rate was at 7.2%.

However, since the latest inflation reports have come out, the 30-year fixed rate (conventional mortgage) and underlying treasury yields, such as the 10-year treasury, have come down significantly. This has led to the 30-year fixed rate (conventional mortgage) dropping to that 6.65% number. Unfortunately, despite this drop, many borrowers are asking, “Hey, are DSCR loan interest rates lower now?” What we’re seeing is that DSCR loan interest rates have remained flat or stable, and in some cases, they’ve actually increased slightly.

If you read into it based on the DSCR Loan Interest Rate Index, the market participants—such as large insurance companies, pension funds, and credit funds—want to be compensated for perceived risk in the market. Real estate investors, especially those who don’t have these properties as their primary residence, are seen as a little riskier. These are no-doc loans; we’re not looking at W2s, tax returns, or other typical documentation, so that spread between the 30-year fixed-rate conventional mortgage and the 30-year DSCR loan has actually widened again. In many cases, it's upwards of 0.75% to 1.5% premium.

Current DSCR loan interest rates in the U.S. range from 7.5% to 12%, depending on lender, loan term, and property cash flow. Non-QM and portfolio lenders dominate this space, offering 30-year terms with 1.20–1.25x minimum DSCR requirements. Rates have risen slightly due to Fed policies, but private lenders remain competitive for strong rental property deals. Short-term bridge DSCR loans start around 9.5%, while long-term fixed rates average 8.25–10%.

How to Know Your Actual Rate

Because rates change daily and depend on several personal and deal-specific factors, the best way to know your actual DSCR loan rate is to:

Get an instant quote (no credit pull)

Complete underwriting

Only after your file receives Agreed To Fund status will your final interest rate be locked. OfferMarket does not guarantee loan terms before this step.

| Lender Type | Interest Rate Range | Minimum DSCR | Loan Term | Best For |

|---|---|---|---|---|

| Traditional Banks | 7.5% – 9.5% | 1.25x | 5–30 years | Strong credit borrowers |

| Private/Non-QM Lenders | 8.5% – 10.5% | 1.20x | 30 years (fixed/ARM) | Investors with lower DSCR |

| Hard Money Lenders | 9.5% – 12% | 1.15x | 6–36 months | Fix-and-flip rentals |

| Portfolio Lenders | 8.0% – 10.0% | 1.20x | 15–30 years | Long-term rentals |

Note: Rates vary by LTV (typically 70–80%), location, and borrower experience.

Why OfferMarket.us Stands Out for DSCR Loans

When it comes to DSCR loans for rental properties, OfferMarket.us dominates the competition with unbeatable terms: rates as low as 6.5%, just 0.5–2 points in fees, and 30-year fixed terms—far better than most private lenders. While banks and non-QM lenders typically start at 7.5%+, OfferMarket.us provides faster approvals, higher leverage (up to 80% LTV), and flexible DSCR requirements (as low as 1.0x for strong properties). Their streamlined process caters specifically to real estate investors, making them a top choice for long-term rental financing. Whether you're scaling a portfolio or locking in low rates, OfferMarket.us delivers the best blend of affordability and investor-friendly terms.

| Lender | Rate Range | Points/Fees | Term | Min DSCR | Max LTV | Speed | Best For |

|---|---|---|---|---|---|---|---|

| OfferMarket.us | 6.5% – 8% | 0.5 – 2 | 30-year fixed | 1.0x | 80% | 10–14 days | Lowest rates, long-term stability |

| Kiavi | 7.75% – 9.5% | 1 – 3 | 30-year | 1.25x | 75% | 2–4 weeks | Fix-and-flip investors |

| LendingOne | 8.25% – 10.5% | 2 – 4 | 5/1 ARM | 1.20x | 75% | 3–5 weeks | Short-term rentals |

| Visio Lending | 7.99% – 9.5% | 1.5 – 3 | 30-year | 1.25x | 80% | 3+ weeks | High LTV deals |

| Lima One Capital | 8.5% – 11% | 2 – 4 | 6mo–30yr | 1.20x | 75% | 2–3 weeks | Flexible terms |

Key Takeaways: Why OfferMarket.us Wins

- Lowest Rates (6.5% vs. 7.75%+ elsewhere) – Saves 10K+annually on a 500K loan.

- Minimal Fees (0.5–2 points vs. 2–4 points) – Lower upfront costs.

- True 30-Year Fixed – Rare among private lenders (most offer ARMs or shorter terms).

- Flexible DSCR (1.0x accepted) – Better for lower-cash-flow properties.

- Faster Closings (10–14 days) – Beats traditional lenders by weeks.

What is a DSCR Loan?

A DSCR loan is a financing option designed for real estate investors, where loan approval depends on the property's cash flow rather than the borrower's personal income. The Debt Service Coverage Ratio (DSCR) is calculated by dividing the property's annual net operating income (NOI) by its annual mortgage debt service. A DSCR of 1.25 or higher is often required, indicating the property generates sufficient income to cover its debt obligations.

How does a DSCR loan work?

DSCR loans evaluate the property's income potential to determine eligibility. Lenders analyze the rental income, operating expenses, and debt payments to ensure the property can sustain the loan. For example, if a property generates $12,000 annually in NOI and has $6,000 in yearly mortgage payments, the DSCR is 2.0. This ratio helps lenders assess risk and set loan terms, including interest rates and repayment schedules. Unlike traditional loans, DSCR loans don't require personal income verification, making them ideal for investors with variable income or multiple properties.

What is a Prepayment Penalty?

But now let’s get into PPP Prepayment Penalty. The standard prepayment penalty for DSCR loans from our perspective, across all of the capital providers on our platform, is a 3-2-1 structure. What that means is it’s otherwise known as a step-down from 3% to 2% to 1% of the outstanding loan amount at the time of payoff. So, if it’s a 3-2-1 prepayment penalty and you decide within year 1 that you want to pay off the loan—whether you sell the property or refinance—you’re paying 3% of the outstanding loan balance at that time. For example, if the outstanding loan balance is $100,000, that’s a $3,000 penalty.

Are there Any Prepayment Penalties for DSCR Loans?

Most DSCR loans include prepayment penalties, which are contractual clauses requiring you to pay an additional fee for early repayment. Common structures include:

- 54321 Structure: A 5% penalty in year one, 4% in year two, and so on, decreasing by 1% annually until year five.

- 321 Structure: A 3% penalty in year one, 2% in year two, and 1% in year three, with no penalty afterward.

- 300 Structure: A flat 3% penalty in the first year, which disappears after that.

These penalties don’t necessarily impact your DSCR loan if you plan to hold the property long-term, as most DSCR borrowers retain properties for more than 3-5 years.

Hidden Fees

Review your loan agreement carefully to identify any hidden fees that may not be clearly disclosed upfront. Common fees include:

- Loan origination fees

- Underwriting fees

- Administrative fees

Lenders may present these fees on a term sheet or loan estimate. Since DSCR loans aren’t qualified mortgages (QM), they aren’t subject to the same federal disclosure requirements as traditional loans, making it crucial to scrutinize the terms.

Appraisal Issues

Lenders require a property appraisal to determine its value and rental income potential. Unexpected appraisal issues, such as lower-than-expected valuations, can impact loan eligibility or require a larger down payment. Discuss your options with the lender upfront and prepare a backup plan to address potential appraisal discrepancies.

Market Conditions

Economic and market conditions influence lending criteria and interest rates. Be prepared for potential changes in market conditions that may affect loan terms or financing availability. Staying informed about market trends helps you anticipate adjustments and make strategic decisions regarding your DSCR loan.

5-4-3-2-1 Prepayment Penalty

Now, if you have a higher prepayment penalty like a 5-4-3-2-1, where 5% is the fee or penalty in year 1, you’re likely going to get a slightly lower DSCR loan interest rate. But is it worth it? Again, going back to the start of this video, it’s really a fool's errand to try to predict interest rates, but what we can say is that these rates do seem a bit elevated and potentially unsustainable. That might be an understatement. Certainly, the housing market is experiencing extreme pressure due to these elevated rates, which is something to consider when evaluating your prepayment penalty options in DSCR loans.

A 5-4-3-2-1 prepayment penalty is a common structure in DSCR loans, designed to discourage early repayment. This structure imposes a declining fee if you pay off the loan within the first five years. For example, if you repay the loan in the first year, you incur a 5% penalty. In the second year, the penalty drops to 4%, and it continues to decrease by 1% annually until it reaches 1% in the fifth year. After the fifth year, no penalty applies.

This structure benefits lenders by ensuring a minimum return on their investment, especially if you refinance or sell the property early. For investors planning to hold properties long-term, the penalty may not be a concern. However, if you anticipate selling or refinancing within the first five years, this penalty can significantly impact your costs.

Some lenders offer alternatives, such as higher interest rates, to eliminate prepayment penalties entirely. Review your loan agreement carefully to understand the specific terms and choose the option that aligns with your investment strategy.

Prepayment Penalty and DSCR Refi Strategy

Prepayment penalties are structured to protect investors who fund your loan by ensuring a minimum return. However, if you anticipate refinancing in 1–3 years, choosing a lighter prepay structure (like 3-2-1 or even 1-0-0) can minimize exit costs. The trade-off is a slightly higher interest rate.

So it's within reason to expect that there might be opportunities to refinance 2, 3 years down the road and so you have options on the prepayment penalty side and that's what we're advising our clients. Instead of that 5-4-3-2-1 prepayment penalty, look at a 3-2-1 pre-payment penalty. The difference in monthly payment is not that significant and you have a much lower penalty if in year 2 or year 3 you're looking to payoff the loan through a refi or sell off the property.

Prepayment penalties are a common feature of DSCR loans, and understanding their structure is crucial for planning your refinancing strategy. These penalties can impact your costs if you decide to pay off the loan early, so reviewing the terms carefully ensures you make informed decisions.

DSCR Loan Requirements

DSCR loans have specific criteria that borrowers must meet to qualify. Key requirements include:

- Minimum credit score of 620: Lenders evaluate your credit history and financial stability, though some may accept lower scores depending on the loan terms.

- Loan amount between $100,000 and $20,000,000: This range provides flexibility for financing properties of varying costs.

- Property appraisal: An appraisal determines the property's market value and rental income potential, which are critical for loan approval.

- Investment property use: DSCR loans are exclusively for non-owner-occupied, income-generating properties used for business purposes.

Lenders calculate your Debt Service Coverage Ratio (DSCR) by dividing the property's annual net operating income (NOI) by its annual mortgage debt service. A DSCR of 1.25 or higher is typically required to qualify.

Property Eligibility

Not all properties qualify for DSCR loans. Eligible properties must meet the following criteria:

- Income-producing: The property must generate rental income, such as single-family rentals, multi-family units, or commercial properties.

- Non-owner-occupied: DSCR loans cannot be used for primary residences or vacation homes.

- Business use: The property must be used for business purposes, such as long-term rentals or short-term vacation rentals.

Lenders assess the property's income potential, including rental income and operating expenses, to determine eligibility. This focus on the property's cash flow rather than your personal income makes DSCR loans an attractive option for real estate investors.

No Prepayment Penalty

There's even more flexibility on the pre-payment penalty side. We have options where you can do let's say 1% in year 1 and then no prepayment penalty in year 2. So the worst you're getting hit with is let's say a 1% fee which is very manageable, right, and in exchange you're paying a higher interest rate which the difference between lets say 8% quote on a 3-2-1 and an 8.5% quote on a 1-0-0, it might be worth it, you can almost look at it as, at that point, like a bridge loan to get you to a point where you can refinance. So we're here to help you evaluate your options and provide you with the most competitive DSCR loan quotes.

Prepayment penalties are common in DSCR loans, but some lenders offer options without this fee. A prepayment penalty is a charge imposed if you pay off your loan early, either through refinancing or selling the property. These penalties typically follow structures like 5-4-3-2-1 or 3-2-1, where the fee decreases annually over a set period. For example, a 5-4-3-2-1 structure imposes a 5% penalty in the first year, 4% in the second, and so on until the penalty expires after five years.

Opting for a DSCR loan without a prepayment penalty provides greater flexibility, especially if you plan to sell or refinance within the first few years. However, loans without prepayment penalties often come with higher interest rates. This trade-off allows you to avoid additional costs if you decide to pay off the loan early. Review your loan agreement carefully to understand whether a prepayment penalty applies and how it’s structured.

For long-term investors who intend to hold their properties for more than five years, prepayment penalties may have minimal impact. In such cases, choosing a loan with a prepayment penalty could result in lower interest rates, reducing overall borrowing costs. Always compare loan terms and consider your investment timeline to determine the best option for your financial goals.

How to Improve Your DSCR

Improving your Debt Service Coverage Ratio (DSCR) enhances your eligibility for DSCR loans and secures more favorable loan terms. Here are actionable strategies to optimize your DSCR and strengthen your financial position.

Increase Rental Income

Raising rental income directly improves your DSCR by increasing your property's cash flow. Conduct regular market research to ensure your rental rates align with current trends. Consider raising rents for new tenants or during lease renewals if the market supports it. Invest in property upgrades, such as modern appliances or added amenities, to justify higher rents. Implement targeted marketing strategies to minimize vacancies, including online listings, social media campaigns, and local advertising. Maintain strong tenant relationships by addressing concerns promptly and offering lease renewal incentives to reduce turnover.

Refinance Existing Loans

Refinancing existing loans at lower interest rates or with longer repayment terms reduces your monthly debt obligations, improving your DSCR. Explore options to add an interest-only feature, which lowers monthly payments temporarily. Refinancing can also help consolidate debt or secure better terms, freeing up cash flow for other investments. Ensure you compare offers from multiple lenders to find the most favorable terms and avoid unnecessary fees.

Increase Property Value

Enhancing your property's value can lead to higher rental income and improved DSCR. Focus on upgrades that attract tenants and justify higher rents, such as updated kitchens, energy-efficient systems, or enhanced curb appeal. Regularly maintain your property to preserve its condition and appeal. Consider adding amenities like fitness centers, co-working spaces, or smart home features to differentiate your property in the market.

Manage Your Expenses

Reducing operating expenses increases your net operating income (NOI), directly boosting your DSCR. Review contracts with service providers and negotiate better rates for maintenance, utilities, and property management. Implement energy-efficient solutions to lower utility costs. Regularly audit your expenses to identify areas for cost savings without compromising property quality or tenant satisfaction.

How to Apply for a DSCR Loan

Applying for a DSCR loan involves a structured process that ensures you meet lender requirements and secure favorable terms. Below are the key steps to guide you through the application process.

Assess Your DSCR

Calculate your Debt Service Coverage Ratio (DSCR) by dividing your property’s annual Net Operating Income (NOI) by its annual mortgage debt service. Lenders typically require a DSCR of 1.25 or higher. If your ratio falls below this threshold, consider strategies like increasing rental income or refinancing existing loans to improve your eligibility.

Request access to our DSCR Loan Calculator Excel Formula Google Sheet

Research Lenders and Compare Offers

Identify lenders specializing in DSCR loans, as they offer tailored solutions for real estate investors. Evaluate lenders based on their reputation, industry experience, and loan approval rates. Obtain quotes from multiple lenders to compare interest rates, loan terms, and fees, ensuring you secure the most competitive offer.

Complete the Application

Contact your chosen lender to discuss your financing needs and gather details about their application requirements. Provide essential information about your property, including NOI, debt obligations, and rental income. Submit the necessary documentation, such as property appraisals and rent schedules, to validate your property’s income potential.

Lock in Your Interest Rate

Once your application is reviewed, the lender will offer an interest rate based on your DSCR and property details. Lock in this rate to protect against market fluctuations as you proceed through the final stages of loan approval.

Close the Loan

After approval, finalize the loan by signing the agreement and completing any remaining steps. Unlike traditional loans, DSCR loans don’t require proof of personal income, streamlining the closing process.

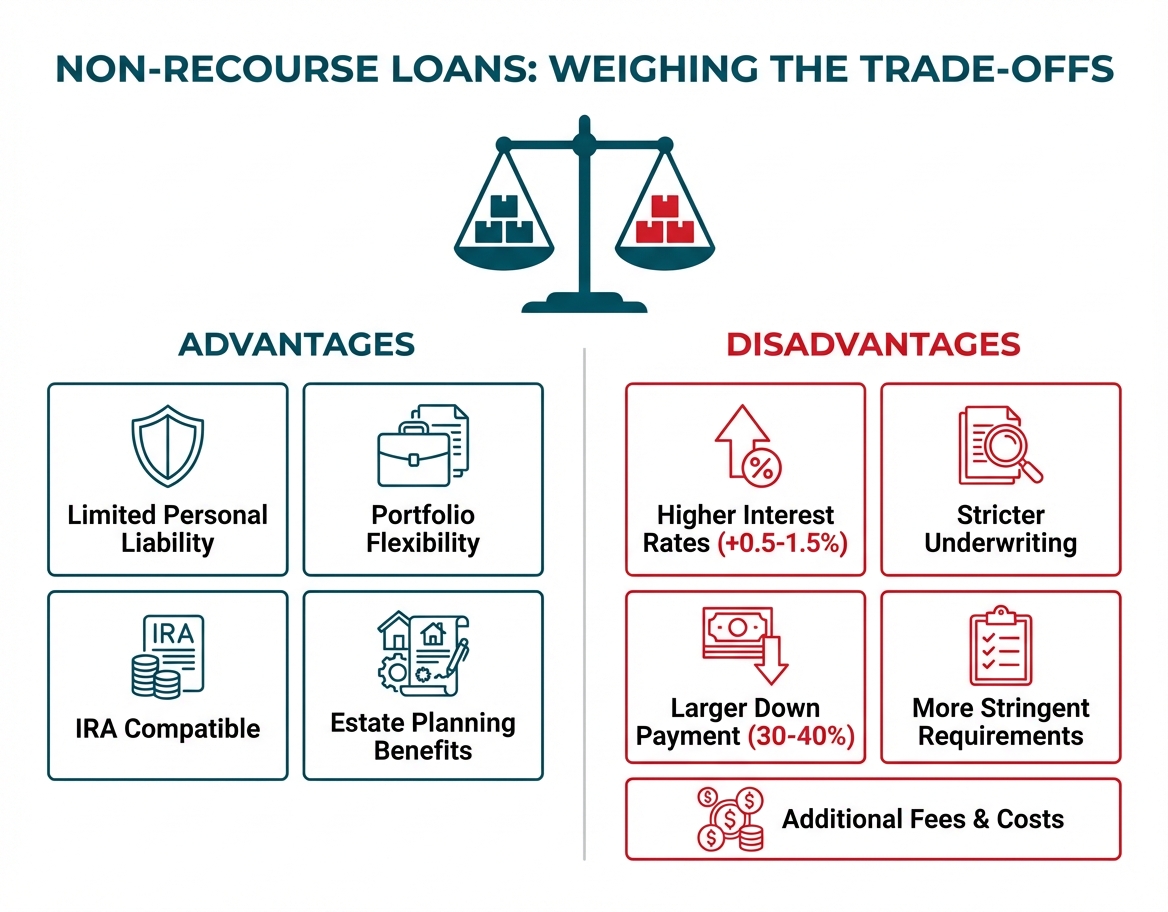

Pros and Cons of DSCR Loans

DSCR loans offer unique advantages and drawbacks for real estate investors.

Pros

- Easier qualification with no personal income verification.

- Reduced documentation compared to conventional loans.

- Faster approval times for quicker access to financing.

- No limit on the number of properties eligible for financing.

- Flexible loan terms tailored to your investment strategy.

Cons

- Higher interest rates compared to traditional mortgages.

- Larger down payment requirements.

- Prepayment penalties for early loan repayment.

- Limited to non-owner-occupied, income-generating properties.

Understanding these pros and cons helps you determine if a DSCR loan aligns with your investment goals.

OfferMarket.us - One Stop Solution

OfferMarket.us simplifies the process of securing a DSCR loan by providing a comprehensive platform tailored to real estate investors. The platform connects you with lenders specializing in DSCR loans, ensuring access to competitive rates and terms that align with your investment goals. By leveraging OfferMarket.us, you streamline the application process, saving time and effort while maximizing your chances of approval.

Key Features of OfferMarket.us

- Lender Network: Access a curated list of lenders offering DSCR loans with varying terms, interest rates, and prepayment penalty structures.

- Rate Comparison: Compare multiple loan offers side by side to identify the most favorable terms for your investment property.

- Streamlined Application: Complete a single application form to receive pre-qualified offers from multiple lenders, reducing redundancy and paperwork.

- Expert Guidance: Benefit from personalized support and insights to navigate the complexities of DSCR loans, including prepayment penalties and hidden fees.

How OfferMarket.us Enhances Your DSCR Loan Experience

- Efficiency: The platform eliminates the need to research and contact lenders individually, consolidating the process into one user-friendly interface.

- Transparency: Gain clarity on loan terms, fees, and prepayment penalties upfront, enabling informed decision-making.

- Customization: Match your specific investment needs with lenders offering tailored solutions, whether you're purchasing or refinancing a property.

- Speed: Accelerate the approval process by submitting a single application and receiving multiple offers within a short timeframe.

Why Choose OfferMarket.us?

OfferMarket.us stands out as a trusted resource for real estate investors seeking DSCR loans. The platform's focus on transparency, efficiency, and expert support ensures you secure financing that aligns with your investment strategy. Whether you're a seasoned investor or new to real estate, OfferMarket.us provides the tools and resources to optimize your loan application and achieve your financial goals.

💡 Want to see your potential DSCR loan rate?

👉 Get an instant quote — no credit pull required

🔢 Use our DSCR calculator to model your cash flow and understand your eligibility

Key Takeaways

- DSCR loans focus on property cash flow: Unlike traditional loans, DSCR loans evaluate the property's income potential rather than the borrower's personal income, making them ideal for real estate investors with variable income or multiple properties.

- Higher interest rates: DSCR loan rates are typically 150 to 300 basis points higher than consumer mortgage rates due to the increased risk associated with investment properties.

- Prepayment penalties are common: Most DSCR loans include prepayment penalties, often structured as 5-4-3-2-1 or 3-2-1, which decrease annually over a set period. However, some lenders offer no-prepayment-penalty options, usually at higher interest rates.

- Eligibility requirements: To qualify, properties must generate rental income, be non-owner-occupied, and meet a minimum DSCR of 1.25. Borrowers typically need a credit score of 620 or higher.

- Flexible financing options: DSCR loans are suitable for purchasing, refinancing, or cash-out purposes, with faster approval times and no personal income verification required.

- Hidden fees and appraisal considerations: Be aware of potential hidden fees like origination or underwriting costs, and ensure property appraisals align with lender expectations to avoid delays or additional down payments.

DSCR Loan Quote

Our mission is to help you build wealth through real estate. Let's grow and optimize your rental property portfolio!

- Get your instant DSCR loan quote today!

- Save big on premiums with our landlord insurance rate shopping service!

- Interested in exclusive investment opportunities? Browse off market properties now!

- Join our Facebook community to stay up-to-date with the latest platform updates and market insights.

- Subscribe to our Youtube channel for our monthly DSCR loan update.

OfferMarket Loans

Check your rate

60 seconds · no credit pull