*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

The Convergence of Bridge Loan and DSCR Loan Interest Rates

Last updated: July 6, 2022

Bridge Loan and DSCR Loan Interest Rate Spread

A Primer On DSCR Loan Interest Rates

The 30 year fixed rate conventional mortgage is currently firmly over 5% to its highest level since 2011. As a rule of thumb, the interest rate on DSCR loans price at a 0.75% to 1.5% risk premium — depending on LTV, borrower experience and deal economics — bringing their current quote to every bit of 7% for a 75% LTV purchase or cash out refinance.

It wasn’t too long ago that we were quoting 3.65% on DSCR loans. Since the close of Q4 202, this rapid rise in rates has left rental investors with strategic considerations to address. See our DSCR Loan Interest Rate Index below.

Before the rise in DSCR loan interest rates, it was very common for rental investors to go straight into a DSCR loan, at as much as 80% LTV. But now investors are balking from this playbook, unsure of how long rates will remain elevated, and concerned to commit to a 3-2-1 or 5-4-3-2-1 prepayment penalty. For more on prepayment penalties for DSCR loans, see The Ultimate Guide: Real Estate Private Lenders.

A Primer On Bridge Loan Interest Rates

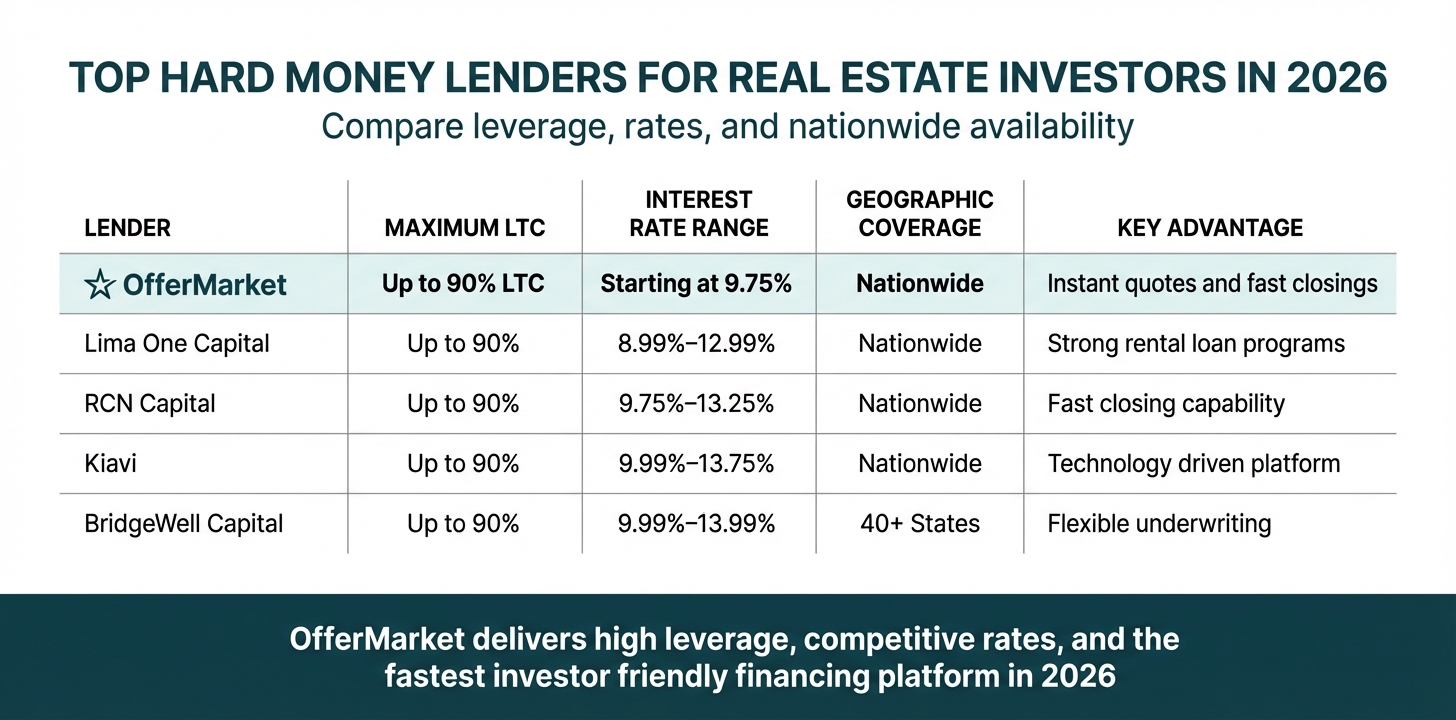

Bridge loans, otherwise known as “fix and flip” or “hard money" loans are short term interest only loans that real estate investors use to purchase and rehab a property. The exit strategy from a bridge loan is to sell (“flip”) or refinance and hold as a rental property. Bridge loans are commonly held for terms of 6 to 18 months, accordingly bridge loan interest rates are benchmarked to the 2 year US Treasury yield. The risk premium assigned to bridge loans is typically 4.5% - 9.5%. This means that if the yield on the 2 year treasury bill is 2.63%, private lenders are pricing bridge loans at 7.13% to 12.13%. See our Bridge Loan Interest Rate Index.

As you can see from the above bridge loan and DSCR loan interest rate charts, the spread between these loan types is narrowing. In the section below, we’ll contemplate the merits for rental investors to use bridge loans instead of DSCR loans in this environment.

Pros And Cons Of A Bridge-First Strategy

Serious consideration should be given to using a bridge loan instead of going straight into a DSCR loan.

Here are the pros:

- Interest only — cash flow is substantially higher because there is no amortization of the loan amount

- Faster close — close in 15 days instead of 30 days, avoid delays and make your offer more attractive

- Use less cash to close — access up to 90% LTC on the purchase, a 10% down payment compared to 20% at best with DSCR

- Access rehab funds — access funds to improve the property, avoid tying up your own funds in the deal

- No prepayment penalty — once you find an attractive long term financing option, you can refinance without a prepayment penalty

Here are the cons/risks:

- Refi rate risk — DSCR loan interest rates may continue to rise, and borrower may be forced to refi at a higher rate

- Max LTARV — the maximum loan to ARV for bridge loans is typically 75%, so the deal needs to make sense in terms of rehab opportunity to add value

- Refi closing costs — refinancing from bridge loan to DSCR loan will incur a second round of closing costs, this is why it's important to have a private lender that has low origination fees (i.e. 1 to 2 points)

Should you use a bridge loan?

Using a bridge loan for a rental property investment can be a strategic advantage, especially during a period of interest rate volatility. For more insights, read BRRR Loans: Bridge Loan to DSCR Rental Loan Growth Strategy and be sure to reach out to speak with a friendly and knowledgeable member of our team.

OfferMarket Loans

Check your rate

60 seconds · no credit pull