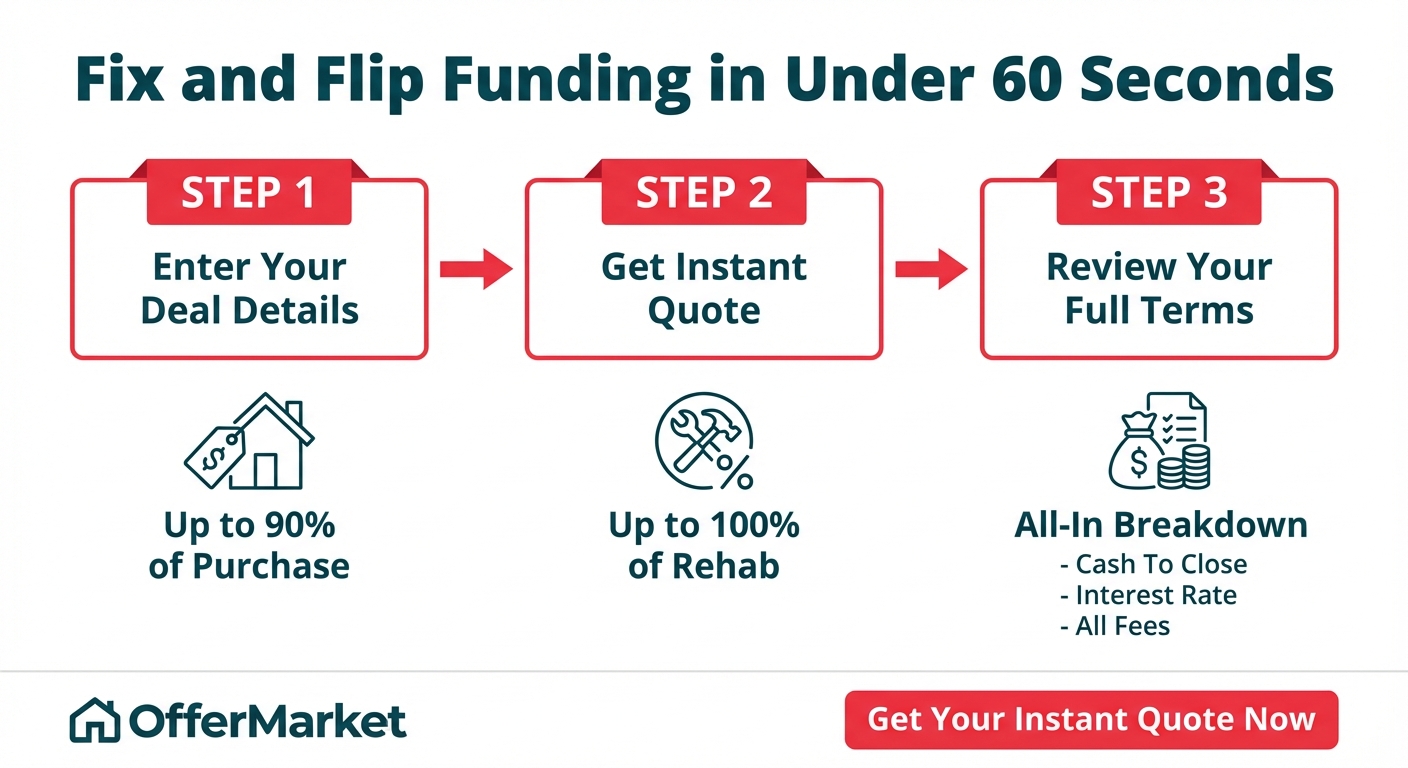

*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Best Hard Money Lenders for First Time Investors

Last Updated: October 6, 2025

We've been there, we know the feeling, and we've designed our platform to help you from your first transaction and onwards.

You're eager to start building your real estate portfolio but the idea of hard money seems intimidating and possibly even risky. You want to find a lender that specializes in serving first time investors. A lender that can help you climb the learning curve and start you on your journey.

If you're tech-forward with a high FICO, that lender may very well be OfferMarket Capital LLC. If you're not tech-forward or your credit score is below 680, then OfferMarket is likely not a fit.

Many hard money lenders explicitly only work with experienced real estate investors. Other hard money lenders charge higher interest rates and fees to first time investors.

We believe there's no better time to start our relationship than with your first project. This gives us the opportunity to transfer valuable knowledge and best practices that will help optimize your trajectory and likelihood of success. Our focus is squarely on helping you manage risk and complete your rehab projects on time, on/under budget and in a manner that doesn't cut corners.

We believe hard money should be easy to learn, and the process --from instant loan quote, to rehab, to final payoff request-- should be simple and repeatable.

Understanding Hard Money Lending

What Is a Hard Money Loan?

A hard money loan is short-term financing from private lenders who focus on the property offered as collateral (the "subject property"). The home or building secures the financing and covers the risk to the lender. This approach makes the borrower's experience and income less of a factor, since the loan is tied to the value and future potential of the asset. Hard money can assist with projects like fix and flips, ground up construction, or fast purchases of stabilized properties where the exit strategy is a cash out refi with no seasoning.

In many cases, these loans close significantly faster than standard bank loans. Some lenders design their approval steps to be efficient, which is helpful for first time investors who want to act quickly. The process often includes an analysis or appraisal of the property, a review of any property rehab plans, a trimerge credit report and background check.

Speed is a big benefit, but rates and fees usually stand above conventional loan structures. Sources like the National Association of Realtors offer data showing that time-sensitive purchases often lean on these specialized loans.

How a Hard Money Loan Works

Hard money loans rely on written agreements where you offer the property as security. The lender calculates a funding amount based on a percentage of its current value or its after-repair value. For instance, if the place needs improvements, some lenders factor in the anticipated worth after the upgrades. The term is usually short, often 12 months, though some lenders extend these loans to longer periods in some situations.

Once you speak with a lender, they assess the collateral and decide how much they want to lend. This helps new investors move without delay, locking in deals that might slip away if they wait for a standard bank. Because these agreements have higher rates, it's important to have a plan to repay the debt or refinance once the project nears completion. Speed is the draw, so lenders offset that benefit by charging more in interest or points. Each lender sets different criteria, though they typically prefer borrowers who have a plan to fix or sell quickly.

Har money loans for real estate are most commonly structured with an initial advance and a construction holdback. The initial advance is funded towards the purchase of the property at settlement (you pay the difference as a down payment as well as closing costs), while the construction holdback is funded via draw requests based on the % of your scope of work you have completed.

Your loan amount is typically limited to 65%, 70% or 75% of the property's after-repair value (ARV) depending on lender guidelines. This is called your loan to after repair value or "LTARV". By limiting your loan LTARV, it reduces the risk that you will need to bring money to closing when you sell the property refinance into a DSCR loan.

First Time Investor Guidelines

The best hard money lenders focus on risk management -- protecting you from taking on excessive risk relative to your experience. You should expect the following guidelines as a first time hard money borrower:

- LTARV: 65% to 70% LTARV -- this will ensure you have a safe amount of projected equity once your rehab is complete

- Initial advance: 75% to 85% -- you will need to bring a slightly higher down payment than experienced investors

- Scope of Work: "light" or "cosmetic" -- you will be limited to a rehab scope where your rehab budget is less than 25% of your purchase price. Your first project should not be a moderate or full gut rehab and should not include anything structural (i.e. removing moving load bearing walls, SqFt extensions, floor additions). Keep it simple: crawl, walk, run.

Compensating Factors

As a first time investor, there's no better time to learn about the concept of "compensating factors". A compensating factor is something that offsets a concerning aspect of a loan application. For example, your first project is a $500,000 purchase price with a $1,000,000 ARV and a $150,000 rehab budget. Let's say that's a $400,000 initial advance (80% of purchase price) + $150,000 construction holdback for a $550,000 total loan amount. This is a significantly higher loan amount than most first time investors should be taking on, as it's best to focus on smaller dollar, lower end projects to get experience. But let's say you have an 800 credit score and you have $1,000,000 of liquidity in your brokerage account. A high credit score, high liquidity and low LTARV are compensating factors that allow your lender's loan committee to justify approving your loan.

Interest Rates on Hard Money Loans

Hard money interest rates depend on several factors including but not limited to:

- 2 Yr Treasury Yield (the "risk free rate")

- Credit spread (the "risk premium")

- Experience

- Property type

- Loan amount

- LTARV

- LTC (loan to cost)

- Property location

- Lender competitiveness

Points, which are fees added at closing, also raise costs. One point equals 1% of the loan balance, so a few points can add up. Some lenders might charge two or three points, covering the rapid funding they provide. It's wise to compare costs by checking the annual percentage rate (APR) and total closing fees. Certain lenders list fees on their websites, letting you see how your overall expenses stack up. This lets you decide if the faster funding—compared to the drawn-out bank routine—makes sense for your situation as a first time investor.

Uses of Hard Money Loans

Hard money loans fit various investment strategies. They often support fix-and-flip projects, where you purchase a distressed property, upgrade it, and sell it for a higher price. These loans also help land acquisition efforts if you plan to build, though terms can depend on the lender’s willingness to fund raw property. Some new investors tap into hard money for short-term needs, such as bridging the gap between property purchase and standard refinancing a few months later.

Individuals also look to hard money when seizing time-sensitive deals. Waiting for conventional bank underwriting could take too long, so paying a higher rate might be worth it if the project profits are large. Some use the funds to cover multiple investment properties, spread out across different markets, so they can scale up their real estate plans. Lenders are largely open to properties in workable condition, though each one has its own list of property types it accepts, including single-family homes, multifamily properties, or commercial buildings.

What to Expect From Hard Money Lenders

Private lenders who offer hard money loans may run smaller operations than large banks. You might find individuals, small firms, or specialized business entities. They usually move quickly, since they base decisions on the collateral instead of deep reviews of your credit. A good lender asks about your timeline, improvement plan, and exit strategy. They might want to see that you have some funds upfront, since they seldom hand out 100% of a property's worth.

They also charge higher fees and use shorter repayment terms. Expect rates and points that can add up to more than you’d pay on a bank loan. Still, the swift process can save time for first time investors who want to secure a deal. Some lenders even allow you to roll loan costs into the final balance. Check each lender’s track record and see if they offer flexible guidelines. You might find that some charge fees for extension requests, so it’s wise to build a payoff plan before signing.

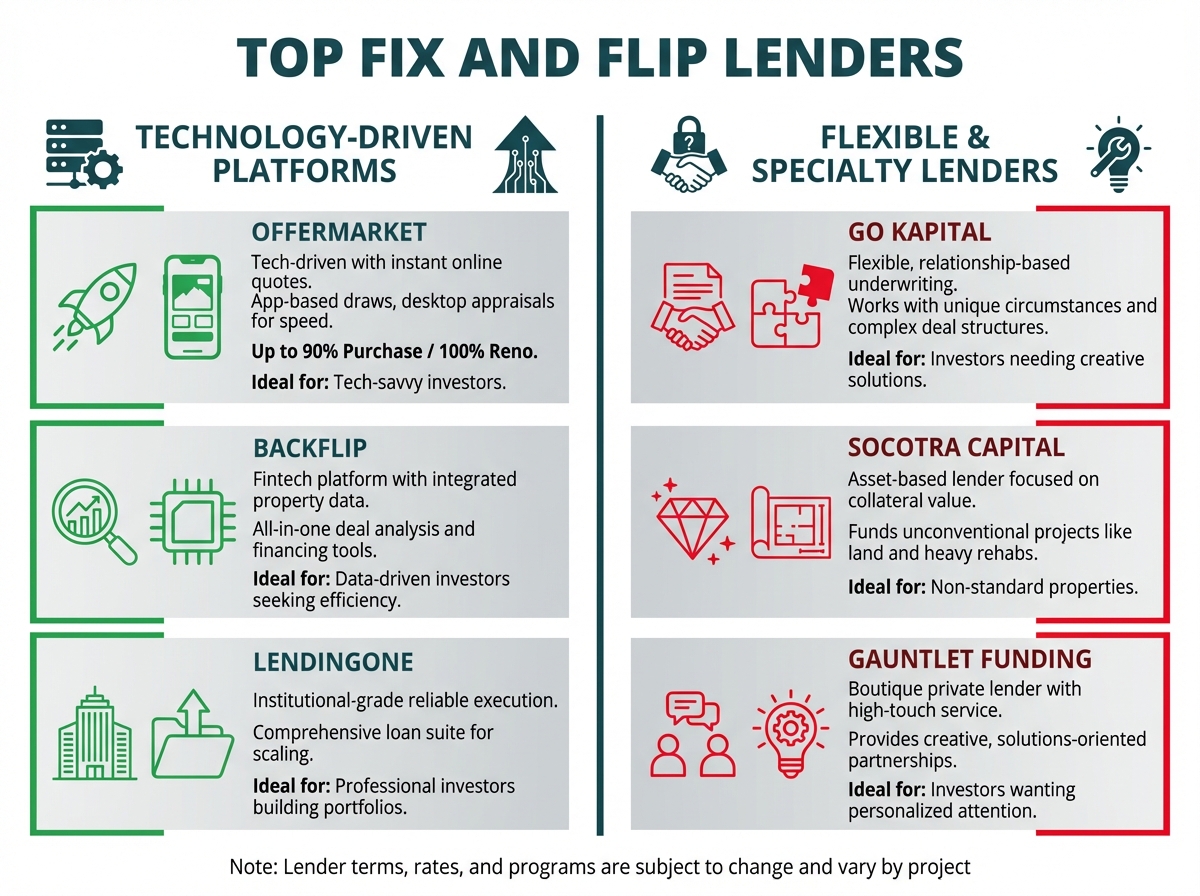

Best Hard Money Lenders

Some large names in the private funding world serve many states, offering terms for new investors. Seek out lenders who focus on transparency in rates and fees. Some examples include lenders that publish clear hard money loan program guidelines maximum loan-to-value (LTV) ratios, interest ranges, and points. Look for any references or data from financial trade groups, as they often track performance and regulatory compliance.

Certain companies state typical approval timelines on their sites, letting you know if you can close within a week or two. Some lenders specialize in residential flips, while others back commercial or mixed-use properties. The best option depends on your local market and your specific plan. It’s also useful to compare initial fees, since some charge several percentage points at closing. A wise approach is to contact at least three lenders and see which one offers terms that fit your project’s plan. This lets you spot any unusual charges or terms.

Important

Hard money brings ease of approval but includes higher risk. If you miss payments or can’t repay by the end of the term, the lender might foreclose. Make sure your project or exit plan has enough potential gains to justify the additional costs. Assess the timeline for remodeling or any needed construction, and keep a buffer for unexpected delays, such as hold-ups with permits or contractor schedules.

You may find that some properties need heavier repairs than expected. That can strain a rehab budget. A thorough estimate of all costs helps prevent shortfalls. Also consider how you’ll stay on top of interest payments, which are usually monthly. Study whether the loan’s short timeframe aligns with your plan to fix or hold the property. In some cases, you could refinance into a regular mortgage later, but that step demands stable credit and a property in good shape.

Special Considerations

Hard money lenders often require that you have some skin in the game. They might finance 70% or 80% of the property’s value, leaving you to fill the remainder with cash. This ensures you are invested in the project’s success. Some lenders request that you show proof of funds for repairs or ask for an appraisal that details the expected worth after upgrades.

Regulations for these loans vary by region, so it’s useful to check any local rules. Some states have stricter limits on rates or fees. Others require certain disclosures. The Consumer Financial Protection Bureau (CFPB) might have guidelines for real estate financing. Check official references if you’re unsure about local restrictions. Also, keep an eye on possible prepayment charges. Some lenders add a fee if you repay the loan ahead of schedule, while others don’t. If your plan is to fix and sell the property soon, you might want a lender without a prepayment clause.

Advantages and Disadvantages of a Hard Money Loan

Hard money loans offer a mix of pluses and minuses. It’s wise to consider both before jumping in.

Advantages

- Fast approval and closing: Lenders give decisions fast, allowing you to grab timely deals.

- Flexible guidelines: Some but not all hard money lenders can be especially flexible and willing to look past lower credit scores and limited experience.

Disadvantages

- Higher interest: Rates can be a few percentage points above what banks charge.

- Short payoff windows: You might feel rushed to complete improvements and get it sold or rented. This can be stressful, especially if delays arise that are unexpected or outside of your immediate control.

- Extra fees: Hard money loans can be quite expensive once you add up origination fees, lender fees, extension fees, etc. This is why it's important to work with a transparent lender.

- Collateral risk: If you don't pay off the loan by the end of the term or extension term, your lender may foreclose on your property to recoup their principal and any unpaid interest.

What Are the Typical Terms of a Hard Money Loan?

Many hard money lenders offer loans for a term of 6 or 12 months, with possible renewals/extensions if the borrower meets certain conditions. The loan amount can range from 65% to 75% of the property’s ARV. A few may allow more, though that’s rare and risky. Interest is often in the high single digits to high double digits. At closing, you might pay two or three points based on the total amount borrowed.

Monthly payments typically cover interest, and the final payment covers the balloon balance. This works well if you plan to sell the property or refinance into a standard loan. Collateral is at risk if you fall behind, so a successful exit plan is a must. Some lenders give you a minor grace period, though that extra time can trigger fees. You might also need to supply statements confirming you can cover the interest or any work planned.

Is a Hard Money Loan a Good Investment?

Using a hard money loan can be a good source of capital if the project has enough upside to handle the higher costs. For a fix-and-flip, an investor might find a distressed house at a low price, make upgrades, then list it for a profit. The bigger profit can offset the steep rates. Experienced investors may handle a brief term easily, since the plan is to unload the property as soon as it’s ready.

First time investors should be cautious. Check local property values, renovation timelines, and the lender’s practices. You’ll need a clear idea of how fast you can handle improvements or sell. If you lack a strategy, it might be safer to consider other funding, or partner with someone who has experience. Some projects stall due to unplanned repairs, which can push you past the loan’s expiration date. Late fees or a forced sale might wipe out any return.

What Are The Risks of a Hard Money Loan?

Hard money funding gives you speed, but it carries notable risks. One major risk is the loss of the property if the project fails. Missed payments can prompt the lender to initiate a foreclosure. Another challenge is the higher interest, which can weigh on monthly cash flow. If the renovations or sale take longer than planned, you incur extra interest that hurts profits.

Short loan terms demand a swift exit strategy. If the property requires bigger upgrades than expected, the clock still runs on interest payments. Delays might lead to balloon payments that you can’t handle on time. Some loans also include extension fees. It’s essential to crunch numbers carefully. If a contractor’s timeline slips, or if property values dip, you might not clear enough profit to cover the cost. By studying data from local real estate associations and planning for contingencies, you reduce the chance of being caught off-guard.

Factors To Consider Before Closing

You want to check a few points before finalizing a deal with a hard money lender. Payment schedules, local property rules, and your exit plan matter. It's also wise to look at the lender's track record. Investigate if they're recognized in the region. This can help you see if they offer quick closings. Think about how fees might impact your budget. Some lenders might have additional charges for property inspections or loan extensions. It's good to have some capital set aside for these. Take time to read the contract. If terms are vague, ask for clearer phrasing before you sign. You want to avoid misunderstandings later.

Loan Terms And Fees

You want to be aware of interest expenses since they can impact your monthly dues. Hard money rates are often higher than traditional loans. This is because these lenders accept higher risk. It's important to ask how interest is calculated and whether points are part of the initial fees. Some lenders charge origination fees, while others might add application costs. These could raise the total expense. Check if the lender demands inspections, as these might come with extra charges. You also want to understand the repayment window. Many hard money loans last from 6 months to a year, though some can stretch longer. Be mindful of interest adjustments that may occur if the lender sets a variable rate. Clarify any prepayment penalties so you won't face surprising bills.

Hard Money Loan Features & Considerations

| Loan Feature | Typical Range/Value | Key Considerations |

|---|---|---|

| Loan Term | 6-12 months (up to 24 months) | Short term—must match your exit plan and project timeline. |

| Max LTARV | 65% to 75% | A lower LTARV may require additional cash investment, a better deal (i.e. lower purchase price), or a more cost effective scope of work. |

| Interest Rate | 9% to 18% | Higher rates generally indicate faster funding but involve more risk. |

| Points | 1-3 points paid at closing | Extra fees can affect the overall cost of financing. |

| Lender fees | $500 to $2,000 | Legal/doc prep, underwriting. These can add up and make it hard to compare lenders objectively. |

| Repayment Structure | Interest-only with balloon payment | Ensure your exit plan covers the balloon payment at term end. |

| Points Out | 0% to 1% | Some lenders charge a "point" on the payoff statement, we do not feel this is appropriate. Be sure to confirm before proceeding. |

Tips For A Smooth Financing Experience

- Stay organized -- keep your docs in a digital folder to make it easy to provide to your lender. This includes government issued ID for each member of your borrowing entity, borrowing entity docs (articles of organization, operating agreement, W-9, IRS EIN Letter, bank account statements)

- Protect your credit score -- this is arguably the number 1 issue for real estate investors. Your credit score should always be 680+, preferably 720+.

- Work with experienced contractors -- estimating rehab costs and preparing a scope of work is a skill you will learn over time as you accumulate more experience. As a first time investor, you should be working with an investor-friendly general contractor who can help you conservatively estimate your rehab budget.

- Run your numbers -- many first time investors struggle with bad deals. Hard money lenders want to fund good deals. The price you pay for the property is critical. Use our top-rated offer calculator to help you quickly run your numbers.

Related resources:

Conclusion

You've explored a practical path to fund your first investment property. Hard money lenders offer speed and flexibility that conventional loans can't match. Keep in mind each lenders unique requirements so you can maintain control of your finances and timelines

Always focus on thorough research and realistic exit strategies. Stay proactive by tracking costs and renovations if you're tackling fix-and-flips. By doing your homework and aligning with lenders who understand your ambitions you'll position yourself for greater success in building a profitable real estate portfolio

Frequently Asked Questions

What Are Hard Money Loans?

Hard money loans are short-term, property-backed loans from private lenders. They focus on the property’s value, not the borrower’s credit score. This makes them ideal for investors needing fast cash or who have less-than-perfect credit. Because the loan is secured by the property, approvals are often quicker than traditional bank loans. These loans typically come with higher interest rates and fees, so having a clear plan for repayment is crucial. They’re commonly used for fix-and-flips or quick property purchases where speed and flexibility matter most.

Why Consider Hard Money for a First Real Estate Deal?

Hard money loans allow first-time investors to secure properties quickly, even with limited credit history. They focus on a property’s after-repair value rather than the borrower’s financial profile. This faster approval process helps new buyers act in competitive markets. While rates are higher than standard loans, they’re often the best short-term solution if traditional financing isn’t available. By having a well-structured exit strategy or improvement plan, you can manage the loan term effectively and potentially build credibility with lenders for future deals.

Are Credit Checks Required with Hard Money Lenders?

Yes. This is a common misconception that hard money loans do not require a credit check, or that hard money lenders allow borrowers with low credit scores. Your credit score is extremely important -- it tells the lender how likely you are to repay the loan, of course the lender cares about this, very much indeed! We advise our clients to protect their credit scores as a priority: strive for 720+ and never use credit cards excessively. This is especially important if you want to be able to rent the property out and refinance into a DSCR loan.

How Do Hard Money Loan Terms Differ from Traditional Mortgages?

Hard money loans generally have higher interest rates and shorter repayment terms, often lasting a few months to a couple of years. They involve up-front fees, like origination costs, and can require a down payment. In contrast, traditional mortgages take longer to close, but tend to have lower rates and longer repayment periods—commonly 15 to 30 years. Hard money provides fast approval and lower documentation underwriting (i.e. no tax returns, no W-2 or paystub income verification), making it useful for quick acquisitions or fix-and-flip projects. Borrowers must plan carefully for repayment and budget for the loan’s higher costs.

Which Projects Benefit Most from Hard Money Loans?

Fix-and-flips, quick property acquisitions, land purchases, and bridge financing often benefit from hard money loans. These projects typically require fast funding or face strict deadlines. Hard money lenders focus on a project’s potential, so if you can improve the property and increase its value quickly, it’s more likely you’ll receive approval. For example, if you plan to renovate and sell a home within six months, a short-term hard money loan could be the perfect fit. However, always consider higher fees and prepare a solid exit strategy to avoid issues.

What Do Typical Repayment Terms Look Like?

Repayment for hard money loans are most commonly balloon (principal is not repaid until the full loan amount is due to be repaid at the end of the term via property sale or refinance). The term is most commonly 12 months but can range from 6 to 60 months depending on lender. There is rarely a prepayment penalty though some lenders charge "points out" at the time of payoff.

Many lenders will charge extension fess when the loan is not repaid by the end of the term. It is crucial to avoid delays with your property rehab to ensure you have ample time to list the property for sale or for rent and complete your exit strategy before your hard money loan matures. If you are unable to sell or refinance and pay off your hard money loan by the time your extension expires, your lender may pursue foreclosure to recoup their principal and any unpaid interest.

Who Are Some Hard Money Lenders for First-Time Investors?

- OfferMarket

- Kiavi

These are the only hard money lenders we can recommend to first time investors based on our extensive industry experience and investor feedback.

What Should I Check Before Closing on a Hard Money Loan?

Conservatively underwrite the deal Carefully identify and review comps. Thoughtfully consider your scope of work based on your exit strategy and market comps. Don't use best case assumptions (i.e. wishful ARV). Work with an experienced and trusted investor mentor with local market experience.

Evaluate multiple lenders with an emphasis on transparency Request a transparent term sheet with everything you can expect to see on the settlement statement. Ask them to explain their process for draw requests and loan extensions.

Beware of upfront payments outside of closing Never pay the lender directly for anything prior to settlement. Lenders should only be paid via the title company. The only exception is an appraisal report -- some lenders charge for the appraisal report while other lenders have an appraisal management company handle appraisal payment.

Join OfferMarket

OfferMarket is a real estate investing platform focused on serving rental property investors, small builders and flippers. We focus exclusively on 1-4 unit residential properties in non-rural markets. Our platform is designed to serve first time investors and continue to serve you for every subsequent transaction on your real estate investing journey.

We hope you will accept our invitation to join us and over 20,000 registered members.

Membership is entirely free and comes with the following benefits:

🏚️ Off market properties 💰 Private lending ☂️ Landlord insurance rate shopping 💡 Market insights

Our mission is to help you build wealth through real estate and we look forward to contributing to your success!

OfferMarket Loans

Check your rate

60 seconds · no credit pull