DSCR Loan Houston

OfferMarket Loans

Check your rate

60 seconds · no credit pull

DSCR Loan Houston Example Deal

DSCR Loan Houston calculation

DSCR Loan Requirements

DSCR Loan Houston Common Questions

Last updated: June 23, 2025

Investing in rental properties is an exciting journey, whether you're just starting or expanding your portfolio. Every decision you make plays a crucial role in your success, and finding the right financing options can be a game-changer. That’s where DSCR loans come in, offering a tailored solution specifically for real estate investors like you.

If you're navigating the Houston market, you know it’s full of opportunities but also comes with its challenges. Understanding how a DSCR loan works and how it can help you manage risk while maximizing returns is key to staying ahead. In this article, you'll discover actionable insights to leverage DSCR loans effectively, helping you grow and optimize your rental property investments with confidence.

What Is A DSCR Loan?

A DSCR loan, or Debt Service Coverage Ratio loan, is a financing option designed for property investors focusing on rental income rather than personal income. It evaluates your property's ability to cover its debt obligations using rental income alone. Unlike traditional loans, it doesn't rely on employment history or personal income documentation, making it especially appealing to self-employed investors and those managing multiple properties.

Lenders assess the property's DSCR by dividing its net operating income by the total debt payments. A DSCR of 1.0 indicates the property generates just enough income to cover its debt. Ratios above 1.2 are often preferred, as they show excess income that ensures debt payments and reduces risk. For example, a property generating $3,600 monthly with a $3,000 total debt payment yields a DSCR of 1.2.

A DSCR loan can work well in strategies such as fix-and-rent loans, where you purchase, renovate, and rent properties to generate consistent rental income. With these loans, you can grow your rental portfolio without focusing on personal income thresholds. Including proper landlord insurance, like dwelling coverage and loss of rent coverage, alongside your DSCR loan increases investment security and minimizes risks.

Benefits Of DSCR Loans In Houston

DSCR loans provide unique advantages for real estate investors in Houston. They are designed to simplify financing for rental property acquisitions, focusing on a property's cash flow rather than an individual’s income.

Flexible Lending Terms

DSCR loans offer flexibility with repayment structures, allowing you to choose options that align with your investment goals. Lenders prioritize a property’s debt service coverage ratio (DSCR) when determining eligibility, enabling you to secure financing that matches your projected rental income. Loan terms often include options like interest-only payments, competitive fixed or variable rates, and amortization periods extending up to 30 years. These features make it easier for you to manage cash flow, especially when handling multiple rental properties or employing fix-and-rent loan strategies. The flexibility ensures tailored solutions for different types of investors.

No Personal Income Verification

With DSCR loans, there’s no need to provide proof of personal income, as lenders base their decision on a rental property’s financial performance. This is ideal if you’re self-employed or own multiple properties, eliminating the challenges of meeting traditional income requirements. By focusing solely on net operating income and debt obligations of the property, lenders streamline the approval process for you. This approach permits you to scale your investments efficiently without personal financial scrutiny. Additionally, it complements strategies involving landlord insurance and loss of rent coverage by reinforcing the emphasis on rental cash flow.

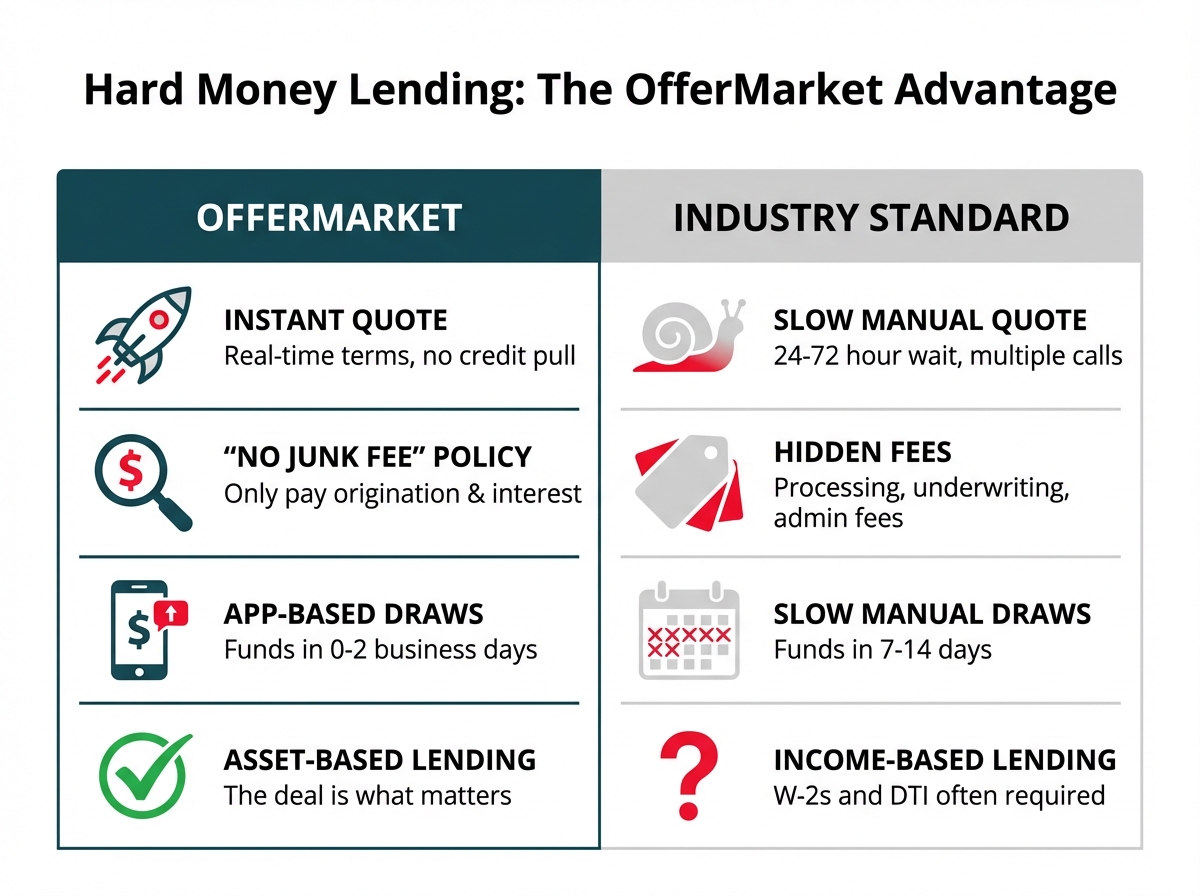

Faster Approval Process

DSCR loans typically offer faster approval compared to traditional mortgages, as the criteria revolve around property performance. Fewer document requirements, like income or tax returns, reduce the time it takes for underwriting, helping you close deals quickly in Houston’s competitive real estate market. If leveraging a fix-and-rent loan, the expedited process allows you to smoothly transition from acquisition to renovation or renting. Prompt approval ensures opportunities aren't missed, facilitating steady growth in your rental property portfolio. Efficiency in funding enables you to adapt swiftly to market conditions while optimizing investment timelines.

How To Qualify For A DSCR Loan In Houston

Qualifying for a DSCR loan in Houston involves meeting specific criteria and providing the necessary documentation. Lenders primarily focus on the property's cash flow and not your personal income.

Key Eligibility Criteria

- Debt Service Coverage Ratio (DSCR): Lenders typically require a DSCR of at least 1.0. This ratio compares the property's net operating income to its total debt payments. A higher ratio demonstrates strong cash flow.

- Property Type: Eligible properties include single-family rentals, multifamily units, and commercial properties generating rental income.

- Loan-to-Value Ratio (LTV): Most lenders offer up to 75-80% LTV, depending on the property's performance and location.

- Rental Income: The property's rental income should support debt obligations. Providing a reliable rental market analysis can strengthen your application.

- Credit Profile: While DSCR loans don't heavily rely on personal credit, a minimum credit score of 620 might be expected to ensure favorable terms.

Documents Required

- Property Income Details: Rent roll statements or lease agreements showing consistent income from tenants.

- Operating Expenses: A breakdown of expenses like maintenance, taxes, and landlord insurance premiums.

- Property Appraisal Report: This report verifies the property's value and condition.

- Proof of Ownership or Purchase Agreement: For refinancing or purchasing the property.

- Business Entity Documents: If applying under an LLC or corporation, provide entity formation and operating agreements.

- Rental Market Analysis (Optional): A report showing rental market trends supports your case for stable income generation.

Comparing DSCR Loans To Traditional Loans

When evaluating DSCR loans versus traditional loans, understanding the distinctions is critical for optimizing financing strategies for your rental property investments.

Key Differences

DSCR loans prioritize property cash flow over personal income, assessing the rental income's ability to cover debt obligations. Traditional loans rely heavily on your personal income and credit score, making them less accessible for self-employed investors or those managing multiple properties. A DSCR above 1.2 is generally sufficient for loan approval, whereas traditional loans often demand extensive personal financial verification.

DSCR loans typically streamline the approval process by focusing on income-generating property performance, enabling faster closings. Traditional loans, in contrast, involve stricter underwriting requirements, delaying approvals. Additionally, DSCR loans do not require personal income documentation, while traditional options mandate comprehensive financial disclosures. For Houston investors seeking fix-and-rent loan opportunities, DSCR loans offer tailored flexibility.

Pros And Cons Of Each

DSCR loans provide a streamlined approval process, no need for personal income verification, and flexibility in repayment terms. However, they often come with higher interest rates compared to traditional loans. In Houston's real estate market, DSCR loans suit investors prioritizing speed and scalability while balancing higher borrowing costs.

Traditional loans feature lower interest rates and longer repayment terms, reducing overall borrowing costs. Despite this, their stringent credit and income prerequisites can make qualifying difficult, particularly for those with diverse income streams. Stick with traditional loans if personal financial stability is priority; lean towards DSCR loans if you want an asset-based approach. For scaling investments in Houston, DSCR loans paired with landlord insurance, such as loss of rent coverage, mitigate risk efficiently.

| Feature | DSCR Loans | Traditional Loans |

|---|---|---|

| Debt Service Coverage Ratio (DSCR) | Focus on cash flow; typically requires a DSCR of 1.0 or higher | Based on personal income and creditworthiness |

| Income Verification | Less emphasis on personal income; primarily looks at rental income | Requires detailed income documentation (W-2s, tax returns) |

| Credit Score Requirements | More flexible; can accommodate lower credit scores | Generally requires higher credit scores for approval |

| Loan Purpose | Primarily for investment properties | Used for primary residences, second homes, and investment properties |

| Down Payment | May require a higher down payment | Varies; can be lower with certain programs (FHA, VA) |

| Interest Rates | Typically higher due to perceived risk | Generally lower rates for qualified borrowers |

| Loan Terms | Often shorter terms (5-30 years) | Standard terms (15-30 years) |

Top Tips For Securing A DSCR Loan In Houston

Securing a DSCR loan in Houston requires careful preparation and strategic planning. Focus on collaborating with reliable lenders and submitting a comprehensive application.

Working With Experienced Lenders

Partner with experienced lenders who specialize in DSCR loans to improve your approval chances. Established lenders understand Houston’s rental market and can guide you through the loan process efficiently. Look for lenders with tailored programs like fix-and-rent loans and favorable terms suited for property investors.

Evaluate a lender’s reputation by checking client reviews and success rates in securing DSCR loans. Confirm they offer products that include critical benefits like streamlined underwriting. A knowledgeable lender also ensures you consider essential protections such as landlord insurance, including dwelling coverage and loss of rent coverage, to manage risks effectively.

Preparing A Strong Loan Application

Submitting a complete, accurate loan application boosts approval potential. Present well-documented financial records detailing rental income, operating expenses, and property performance. Include a current property appraisal and proof of ownership or purchase agreements.

For a DSCR loan, emphasize the property’s ability to generate stable cash flow. Strengthen your application with a rental market analysis showcasing income potential. Maintain a DSCR of at least 1.2 to meet lender expectations. Optional risk-mitigating measures like general liability coverage further illustrate your financial stability while protecting investment assets.

Key Takeaways

- DSCR loans are tailored for real estate investors, focusing on rental property cash flow instead of personal income, making them ideal for self-employed individuals or those with multiple properties.

- In Houston's dynamic market, DSCR loans provide flexibility and faster approval processes, enabling investors to seize opportunities and scale their rental portfolios efficiently.

- Key benefits of DSCR loans include no personal income verification, flexible repayment terms, and simplified underwriting, streamlining the financing process compared to traditional loans.

- To qualify for a DSCR loan, lenders prioritize a property’s DSCR (typically 1.2 or higher), rental income, and Loan-to-Value (LTV) ratio while requiring minimal personal financial documentation.

- DSCR loans are ideal for fix-and-rent strategies and pairing them with landlord insurance enhances investment security by mitigating risks like property damage or rental income loss.

- Working with experienced DSCR lenders in Houston and preparing a thorough loan application with accurate financial documentation can significantly boost approval chances.

Conclusion

DSCR loans offer a powerful financing option for real estate investors in Houston, combining flexibility with a focus on property cash flow. By leveraging these loans, you can streamline the approval process, scale your investments, and adapt repayment terms to align with your goals.

Whether you're self-employed or managing multiple properties, DSCR loans provide a tailored solution to navigate Houston's competitive rental market. Partnering with experienced lenders and presenting a strong application can position you for success while minimizing risks. With the right strategy, you can unlock the full potential of your rental property portfolio.

Frequently Asked Questions

What is a DSCR loan, and how does it work for rental property investors?

A DSCR (Debt Service Coverage Ratio) loan is designed for real estate investors. Unlike traditional loans, DSCR loans assess the property’s income rather than personal income. Lenders look at the property’s DSCR by dividing net operating income by total debt payments, with a ratio of 1.2 or above usually required. This makes it ideal for self-employed investors or those managing multiple properties.

Why are DSCR loans popular in the Houston real estate market?

DSCR loans are popular in Houston because they focus on rental income, offer flexible terms, and streamline the approval process. These loans allow faster closings in Houston’s competitive market, appealing to investors scaling their rental portfolios.

What are the eligibility requirements for a DSCR loan?

To qualify for a DSCR loan, you typically need a DSCR of at least 1.0, and a credit score of at least 620 though most DSCR lenders will require a minimum credit score of 680 and interest rate and LTV are significantly more favorable for borrowers with credit scores of 720 and higher. Documentation like property income details, operating expenses, and an appraisal report is required. The appraisal report is ordered by your DSCR lender.

How do DSCR loans differ from traditional loans?

DSCR loans prioritize property cash flow, not personal income, making them accessible to self-employed investors. They have faster approval processes but may come with higher interest rates. Traditional loans, by contrast, have stricter income and credit requirements.

What are the benefits of using DSCR loans over traditional financing?

DSCR loans simplify approvals, focus on property performance, and avoid personal income verification. They’re faster to close, offer flexible terms, and help investors scale their portfolios efficiently.

Are there any downsides to DSCR loans?

The primary downside of DSCR loans is that they often have higher interest rates compared to traditional loans. However, the flexibility and speed of the approval process usually outweigh this for many investors.

What tips can help me secure a DSCR loan in Houston?

To secure a DSCR loan, ensure your property has a DSCR of 1.0 or higher, prepare detailed financial records, and highlight the property’s cash flow potential. Collaborate with experienced lenders to strengthen your application and include optional risk-mitigation measures like landlord insurance.

Do DSCR loans require personal income verification?

No, DSCR loans do not require personal income verification. They focus on the rental income of the property being financed, which is a significant advantage for self-employed investors.

What property types are eligible for DSCR loans?

DSCR loans can finance a range of property types, including single-family homes, multifamily units, and commercial rental properties. However, lenders may have specific requirements, so it’s best to confirm eligibility beforehand.

How can landlord insurance protect my investment?

Landlord insurance covers risks like property damage, tenant injuries, or loss of rental income. It protects your investment and may demonstrate responsibility to lenders, strengthening your loan application.

How to calculate DSCR

To calculate the Debt Service Coverage Ratio (DSCR), use the formula: Gross Rent / PITIA (Principal, Interest, Taxes, Insurance, and Association fees). This ratio measures a property's ability to cover its debt obligations. A DSCR greater than 1 indicates sufficient income to meet debt payments, making it a key metric for investors.

Texas DSCR Loan Products

Ohio real estate investors have access to various Debt Service Coverage Ratio (DSCR) loan products tailored to their needs. One popular option is the 30-year term loan, which offers a long repayment period, allowing for lower monthly payments. These loans are typically fully amortizing, meaning that the principal and interest are paid off over the term, providing stability in budgeting.

Another option is the partial interest-only loan, where investors pay only interest for the first 5 or 10 years. This can enhance cash flow during the initial years, making it easier to manage other expenses. However, investors should be prepared for higher payments once the interest-only period ends.

Lastly, there are adjustable-rate mortgages (ARMs), which can be less attractive due to their fluctuating interest rates. While they may offer lower initial rates, the risks associated with potential rate increases can lead to higher payments in the future.

| Loan Product | Term | Amortization Type | Notes |

|---|---|---|---|

| 30-Year Fixed | 30 Years | Fully Amortizing | Stable monthly payments |

| Partial Interest Only | 5 or 10 Years | Interest Only (initial period) | Improved cash flow initially |

| Adjustable Rate Mortgage (ARM) | Varies | Variable | Higher risk due to rate fluctuations |

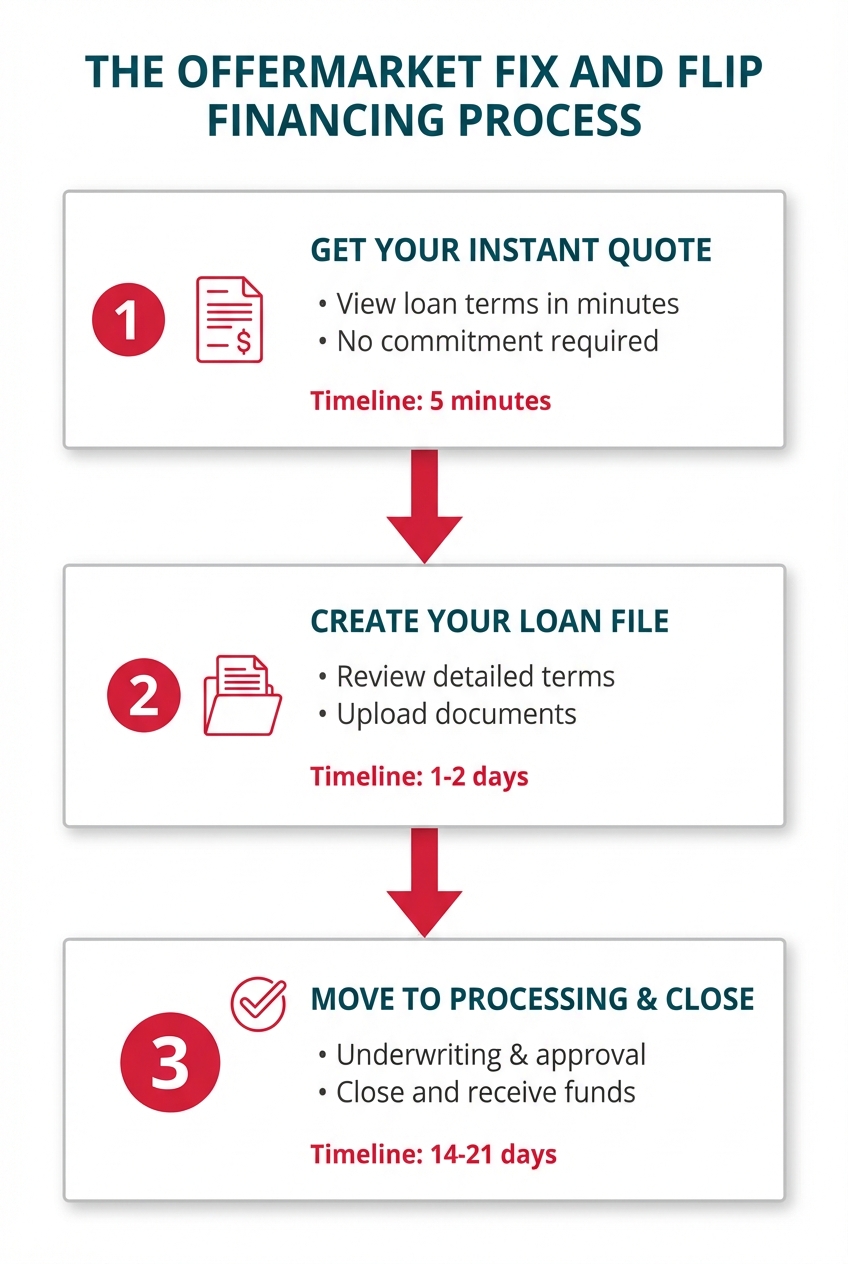

How to Apply for a DSCR Loan in Houston

Applying for a DSCR loan in Houston involves gathering necessary documents and completing the application process efficiently. Understanding these steps ensures a smoother experience.

Grow your Houston portfolio with OfferMarket

If you've found this helpful and would like access to more rental property investing resources, sign up for OfferMarket. Membership is free and comes with the following benefits:

🏠 Off market properties 💰 Private lending ☂️ Landlord insurance rate shopping 💡 Community & insights

If you are not already a member, we hope you will accept our invitation to join us!

OfferMarket Loans

Check your rate

60 seconds · no credit pull