Bridge Loan South Carolina

Last Updated: May 2, 2025

At OfferMarket, we're passionate about empowering your real estate ambitions throughout the vibrant state of South Carolina. Our goal is simple: to help Palmetto State investors like you expand your portfolio, boost returns, and navigate the investment landscape with greater confidence.

Through our fully integrated platform, you'll gain access to: 💰 Flexible private lending options

☂️ Tailored insurance rate comparisons for real estate investors

🏚️ Exclusive access to off-market properties across South Carolina

Our South Carolina Bridge Loan program is designed to deliver fast, dependable, and affordable financing—helping you move quickly to purchase, renovate, and grow your residential investment projects statewide.

Whether you’re flipping for fast profits or building passive income through the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat), OfferMarket is ready to support your investment journey every step of the way.

What Is a South Carolina Bridge Loan?

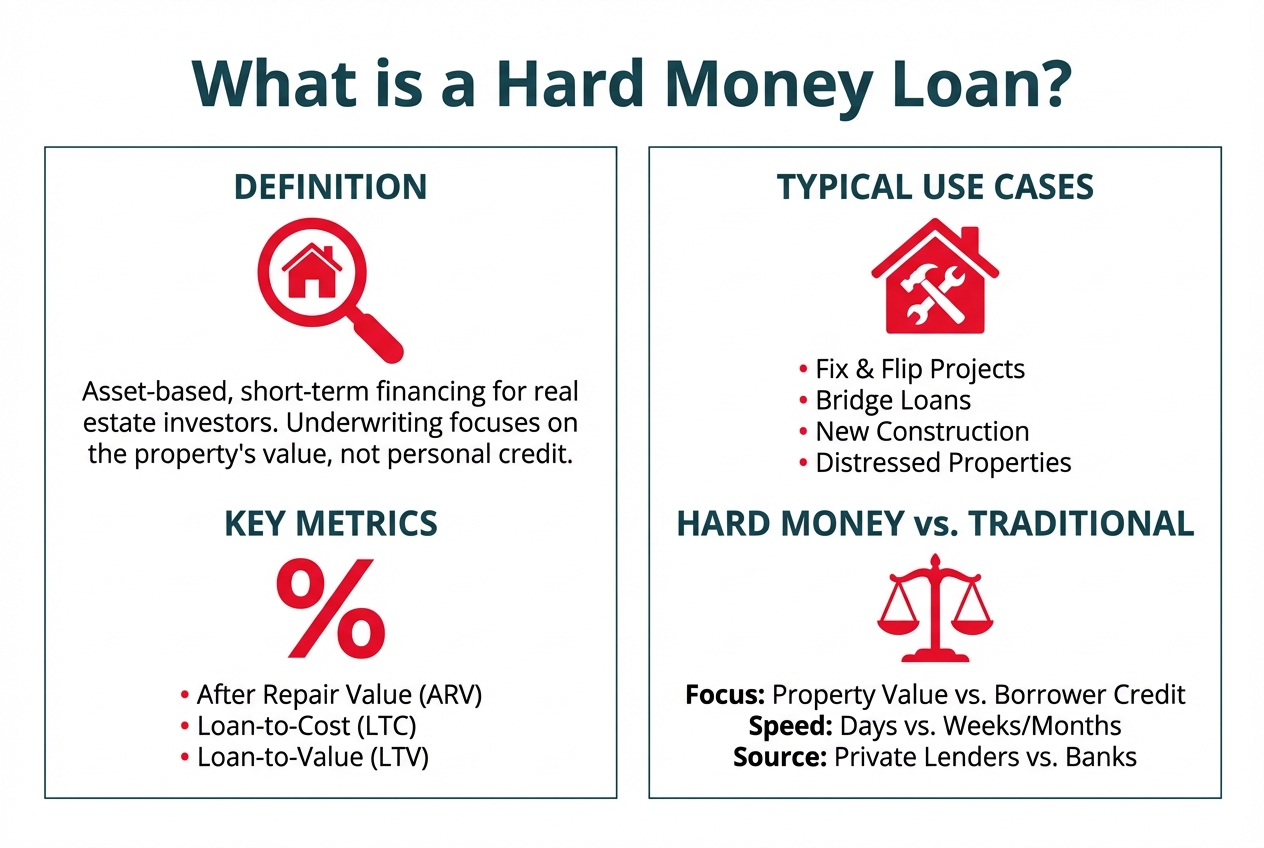

A South Carolina bridge loan is a short-term financial solution designed specifically for real estate investors who need quick access to capital. It serves to bridge the gap until a longer-term loan or exit strategy is achieved.

Common Use Cases for South Carolina Bridge Loans

Across South Carolina, investors turn to bridge loans for a range of scenarios, including:

Purchasing and rehabbing distressed properties: Secure the funding needed to acquire and renovate homes, keeping your own cash free for other investments.

Refinancing and renovating: Bought a fixer-upper with cash? A bridge loan can help you unlock your equity to fund necessary improvements.

Paying off an existing loan and completing a project: If you need to repay an initial lender but still have work to finish, a bridge loan offers the breathing room you need.

Purchasing without a renovation plan: Snap up undervalued South Carolina properties at below-market prices without intending to renovate, aiming for a quick AS-IS resale.

Refinancing a cash purchase (no rehab): Access the equity tied up in a property you purchased with cash—even if you don't plan to renovate.

Refinancing after completing a rehab: Finished your renovations but need extra time to sell or refinance? A bridge loan can help extend your runway.

In the real estate world, bridge loans are often called "hard money loans" or "fix-and-flip loans." These terms are used interchangeably by seasoned investors and lenders alike.

How Our South Carolina Bridge Loan Works

Every OfferMarket South Carolina bridge loan comes with two main components:

Initial Advance

This portion covers your property's purchase price and is wired directly to the title company at the time of closing.

Construction Holdback

This section funds your rehab budget and is disbursed through a draw process as you make progress on your renovations.

The beauty of our program lies in its flexibility. You can choose to use both the initial advance and the construction holdback—or just one, depending on your project's needs.

Many South Carolina investors combine both to maximize leverage while preserving personal liquidity. But if you prefer to handle renovations out-of-pocket or skip them altogether, that’s perfectly fine too. Our program adapts to your investment strategy.

When it comes to South Carolina real estate investing, flexibility is everything. Our bridge loan program gives you the freedom to pivot your exit strategy as needed.

1. Sell for Profit (Fix and Flip)

Planning to renovate and flip for a strong return? Our loan terms are designed to help you stay agile and maximize profits without restrictive financing.

2. Rent and Refinance (BRRRR Method)

Building a rental portfolio? Buy, renovate, rent, and refinance into a Debt Service Coverage Ratio (DSCR) loan—all while keeping your cash flow healthy and your investments thriving.

Who Benefits from South Carolina Bridge Loans?

Whether you’re dipping your toes into real estate investing for the first time or you’re a seasoned expert with a deep portfolio, our South Carolina bridge loans are built to meet you where you are.

Fix and Flip Investors ("Flippers")

Need fast funding to purchase, rehab, and resell properties? Our bridge loans provide the capital you need to move quickly and stay competitive.

BRRRR Method Investors (Buy, Rehab, Rent, Refinance, Repeat)

Looking to expand your rental portfolio across South Carolina? Our Fix and Rent bundle combines a bridge loan for acquisition and renovation with a discounted DSCR loan for your refinance, helping you maximize your returns.

Many successful South Carolina investors employ a hybrid strategy—flipping some properties while holding others for rental income. We encourage this flexible approach to help you adapt to shifting market conditions and grow your wealth strategically.

South Carolina Bridge Loan Program Guidelines

Here’s a clear overview of our lending guidelines for investors throughout South Carolina:

| Criteria | Guideline |

|---|---|

| Loan Amount (Min-Max) | $25,000 – $2,000,000 |

| After Repair Value (ARV) | Minimum $100,000 |

| Experience Requirement | None required |

| Minimum Credit Score | 680 |

| Borrowing Entity | LLC or Corporation (no personal loans) |

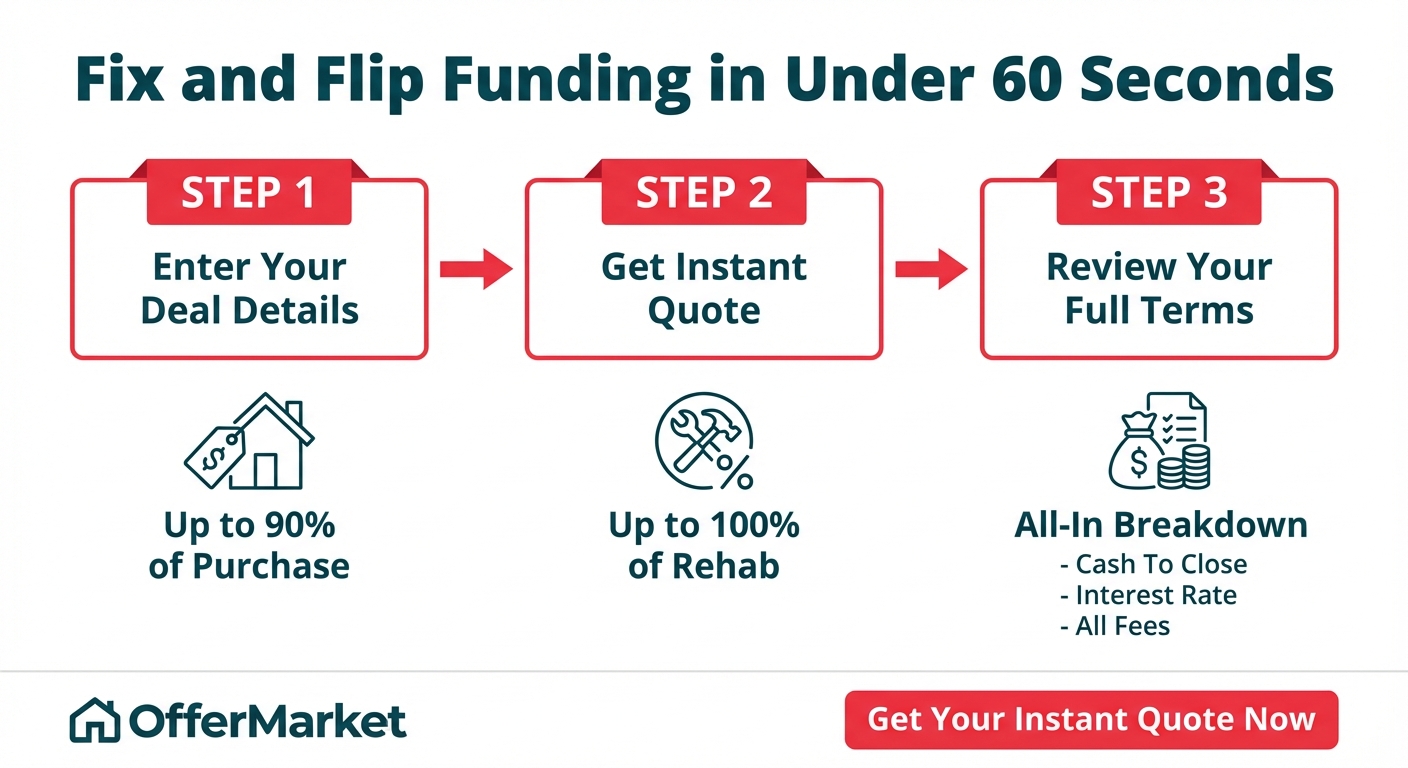

| Initial Advance | Up to 90% of purchase price |

| Construction Holdback | Up to 100% of rehab budget |

| Loan-To-ARV (LTARV) | Maximum 75% |

| Interest Rate | Instant quote available |

| Origination Fee | 1.5 to 2 points |

| Loan Term | 12 to 24 months |

| Prepayment Penalty | None |

| Structure | Interest-only with balloon payment |

| Recourse | Full recourse (51% of borrowing entity must guarantee) |

| Exit Strategy (Sale) | Minimum 30% projected ROI |

| Exit Strategy (Refinance) | Minimum 1.1 DSCR after repairs |

| Valuation Method | Appraisal report or in-house valuation |

| Minimum Property Size | Single family: 700+ SQFT, 2–4 unit: 500+ SQFT per unit, Condo: 500+ SQFT |

| Max Acreage | 5 acres |

| Interest Accrual | Under $100K: full loan amount ("Full Boat"); $100K+: as disbursed |

| Advanced Draws | Subject to lender discretion |

| Minimum Down Payment | $10,000 |

Project Eligibility

At OfferMarket, our focus is helping South Carolina real estate investors build durable, lasting wealth—while prioritizing safety and smart risk management. That’s why we’re selective about the deals we fund, ensuring alignment with your goals and project feasibility.

We’re proud to report that across all loans we’ve originated, fewer than 0.5% have ended in foreclosure. This reflects our commitment to responsible lending—and your success as an investor.

It’s important to know: projects with higher complexity, like heavy or extensive rehabs, carry more risk. Delays, unexpected expenses, and changing market dynamics can impact profitability—even for seasoned investors. During times of market uncertainty, this becomes even more critical.

At OfferMarket, we’re more than just your lender—we’re your financing partner, deal advisor, and risk management guide. Our priority is helping you grow your South Carolina real estate business successfully and sustainably.

Initial Advance

Your initial advance—the portion of your loan that covers the purchase price—is determined by your experience level, credit score, and the specifics of the deal.

When evaluating your initial advance, we take into account:

Number of investment properties owned in the past 24 months

Number of comparable rehab projects completed in the last 5 years

Minimum credit score of 680 (720+ preferred for personal guarantors)

Licensed professionals such as Realtors, General Contractors, or Professional Engineers may qualify for enhanced leverage

Important: If your contract price exceeds the property's As-Is appraised value, the initial advance will be based on the lower As-Is value.

Your exit strategy also factors into your advance:

For fix-and-flip projects: we require at least a 30% projected gross margin and $15,000 minimum projected profit.

For BRRRR projects: the post-repair Debt Service Coverage Ratio (DSCR) should be at least 1.1.

Properties located in more rural parts of South Carolina may have lower leverage caps and require a minimum Tier 3 experience level.

Experience-Based Tiers

| Tier | Verifiable Experience |

|---|---|

| 1 | 0 completed projects |

| 2 | 1 to 2 completed projects |

| 3 | 3 to 4 completed projects |

| 4 | 5 to 9 completed projects |

| 5 | 10+ completed projects |

Initial Advance by Experience Tier

| Tier | Initial Advance (% of Purchase Price) |

|---|---|

| 1 | 80% (up to 85% with excellent credit/liquidity) |

| 2 | 85% |

| 3 | 85% |

| 4 | 90% |

| 5 | 90% |

Adjustments to Initial Advance

Depending on the specifics of your deal, your initial advance may be adjusted:

| Scenario | Adjustment |

|---|---|

| Credit score less than 720 | -5% |

| Full gut rehab | -5% |

| New market (first project in a new area) | -5% |

| Licensed Realtor | Up to +5% |

| Licensed General Contractor | Up to +10% |

| Licensed Professional Engineer | Up to +10% |

| Rural property | -20% (requires 3+ completed projects) |

Rehab Scope Classification

| Rehab Scope | Definition |

|---|---|

| Light | Rehab budget is less than 25% of the purchase price |

| Moderate | Rehab budget is 25% to 49.99% of the purchase price |

| Heavy | Rehab budget is 50% to 99.99% of the purchase price |

| Extensive | Rehab budget exceeds 100% of the purchase price—such as major additions, expansions, or “lopsided deals” |

Note: A "lopsided deal" refers to scenarios where the rehab budget exceeds the purchase price or As-Is value. For these projects, Loan-To-Full-Cost (LTFC) limits apply.

Rehab Scope Eligibility

Your eligibility for different rehab scopes depends on your experience tier:

| Tier | Experience | Light | Moderate | Heavy | Extensive |

|---|---|---|---|---|---|

| 1 | 0 | Eligible | Ineligible | Ineligible | Ineligible |

| 2 | 1-2 | Eligible | Eligible | Eligible | Ineligible |

| 3 | 3-4 | Eligible | Eligible | Eligible | Eligible |

| 4 | 5-9 | Eligible | Eligible | Eligible | Eligible |

| 5 | 10+ | Eligible | Eligible | Eligible | Eligible |

Pro Tip: Newer investors in South Carolina are encouraged to start with light or moderate rehabs to reduce complexity and risk.

LTARV Limits

Your maximum Loan-To-After-Repair-Value (LTARV) depends on your experience tier and rehab scope:

| Tier | Experience | Light | Moderate | Heavy | Extensive |

|---|---|---|---|---|---|

| 1 | 0 | 70% | Ineligible | Ineligible | Ineligible |

| 2 | 1-2 | 70% | 70% | 70% | Ineligible |

| 3 | 3-4 | 75% | 75% | 75% | 70% |

| 4 | 5-9 | 75% | 75% | 75% | 70% |

| 5 | 10+ | 75% | 75% | 75% | 70% |

LTFC Limits

For projects classified as Extensive, we apply Loan-To-Full-Cost limits:

| Tier | Experience | Light | Moderate | Heavy | Extensive |

|---|---|---|---|---|---|

| 1 | 0 | N/A | Ineligible | Ineligible | Ineligible |

| 2 | 1-2 | N/A | N/A | N/A | Ineligible |

| 3 | 3-4 | N/A | N/A | N/A | 85% |

| 4 | 5-9 | N/A | N/A | N/A | 90% |

| 5 | 10+ | N/A | N/A | N/A | 90% |

Refinance Using As Is Value Instead of Cost Basis for Initial Advance

Our standard underwriting in South Carolina is based on your cost basis—the combined total of your purchase price and rehab costs to date. This approach protects equity and mitigates risk.

However, in certain refinance scenarios where the property's As Is value exceeds your total investment, we may offer financing based on that higher value.

To qualify for As Is value-based refinance:

The property must be habitable (C4 condition or better)

It must have been seasoned for at least 3 years

Payoff lender must not be a bridge or construction lender (no default interest, late charges, or extension fees)

Minimum credit score of 680

Experience Tier 3 or higher (at least 3–4 similar completed projects)

Strong comparable sales to support the valuation

Clear context for the valuation (such as prior use as a rental)

Transactions Involving Wholesalers, Price Run-Ups

It’s common in South Carolina for investors to work with wholesalers or encounter deals with assignment fees or price markups. OfferMarket can accommodate these transactions under specific guidelines.

If your project involves a wholesaler, we allow the assignment fee or markup to be included in your cost basis—up to 20% of the A-to-B purchase price.

Example:

| Item | Amount |

|---|---|

| A-B Contract (Seller to Wholesaler) | $100,000 |

| B-C Contract (Wholesaler to You) | $125,000 |

| As Is Value | $125,000 |

| Eligible Value Basis for Initial Advance | $120,000 (max 20% markup allowed) |

If the assignment fee or markup exceeds 20%, the excess must be funded out-of-pocket.

Wholesaler Transaction Guidelines

To ensure proper compliance:

Submit full chain of contracts (A-B and B-C)

Provide the wholesaler’s operating agreement

Confirm that the transaction is arm’s-length (no familial or business ties)

The property must not be MLS-listed at the time of assignment

Finder’s fees or referral fees are not eligible for financing

Maximum assignment fee markup: 20% of A-B contract price

Projects exceeding the 20% limit may be reviewed on a case-by-case basis but typically require additional borrower contribution.

Construction Holdback

The construction holdback is the portion of your bridge loan earmarked specifically for rehab expenses. These funds are reimbursed through draw requests as you complete milestones.

If you prefer to fund your own rehab or don't plan to renovate, that's fine too—you can choose a loan without a holdback.

For loans $100,000 or more, you’ll benefit from “As Disbursed” interest accrual. For loans under $100,000, interest accrues on the full amount ("Full Boat").

Draw Processing Guidelines

| Criteria | Guideline |

|---|---|

| Minimum Draw Amount | None |

| Maximum Draw Amount | 100% of remaining construction holdback |

| Minimum Number of Draws | 0 |

| Maximum Number of Draws | None |

| Materials Delivered but Not Installed | Up to 50% reimbursement (with invoice or receipt) |

| Draw Inspection | Self-serve via app (photo upload) |

| Draw Turnaround Time | 0 to 2 business days |

| Draw Fee | $270 per draw |

| Wire Fee | $30 per wire |

Pro Tip: Our fast, app-based inspection process helps South Carolina investors stay on schedule and avoid delays.

Appraisal and In-House Valuation

Every South Carolina Bridge Loan through OfferMarket requires a valuation, satisfied either by a full appraisal or our in-house valuation service depending on eligibility.

In-House Valuation Eligibility

| Criteria | Requirement |

|---|---|

| Property Type | Single family, Duplex, Triplex, Quadplex |

| Experience Tier | 4 or higher |

| Credit Score | 720+ |

| Rural Property | Not eligible |

| New Market | Not eligible |

| LTARV | 70% maximum |

OfferMarket reserves the right to require an appraisal even when in-house valuation eligibility is met.

Exterior Appraisal Guidelines

Exterior-only appraisals are acceptable for:

REO sales

Foreclosure auctions

Sheriff's sales

Online auctions

Bankruptcy sales

Exterior appraisals must be dated within 120 days of settlement (or recertified if between 120–179 days old).

Interior Appraisal Guidelines

For all other transactions, a full interior appraisal is required.

| Property Type | Required Forms |

|---|---|

| Single Family | 1004 + 1007 ARV with As Is value included (non-gridded) |

| 2–4 Unit Multifamily | 1025 + 216 ARV with As Is value included (non-gridded) |

| Condominium | 1073 + 1007 ARV with As Is value included (non-gridded) |

Borrowers are responsible for appraisal invoices. Loans cannot close without paid appraisals.

Stabilized Bridge Loan

If your South Carolina investment property is already stabilized—meaning it's in solid, rentable condition—you may qualify for our Stabilized Bridge Loan. This option lets you borrow against the property's current As Is value without needing a rehab plan or construction budget.

It’s ideal for properties that are already rent-ready or market-ready for sale but require short-term financing to bridge to your next move.

Criteria for Stabilized Bridge Loans

| Criteria | Guideline |

|---|---|

| LTV (Maximum) | Tier 1: 70% / Tier 2: 70% / Tier 3: 75% / Tier 4: 75% / Tier 5: 75% |

| LTFC (Maximum) | Tier 1: 80% / Tier 2: 80% / Tier 3: 90% / Tier 4: 90% / Tier 5: 90% |

| Appraisal Condition Rating | C1, C2, C3, or C4 (must be habitable and stable) |

| Loan Term (Maximum) | 12 months |

Note: Stabilized Bridge Loans are perfect for South Carolina properties that don't require renovations, focusing solely on short-term financing flexibility.

Key Loan Details

| Criteria | Details |

|---|---|

| Loan Amount Range | $25,000 to $2,000,000* |

| Units per Property | 1–4 units |

| Eligible Property Types | Non-owner occupied single-family homes, 2–4 unit multifamily properties, condos, townhomes, and PUDs |

| Minimum Property Size | Single Family: 700+ SQFT / Condo or 2–4 unit: 500+ SQFT per unit |

| Maximum Acreage | 5 acres |

| Loan to Cost (LTC) | Up to 90% purchase, 100% rehab |

| Loan to ARV (LTARV) | Up to 75% |

| Minimum Down Payment | $10,000 for purchases under $100K |

| Loan Term | 12 months standard; 18–24 months available for some projects |

| Extensions | Up to 50% of original term (fees apply) |

| Points (Origination Fee) | 1.5 to 2 points ($2,000 minimum) |

| Prepayment Penalty | None |

| Occupancy | Non-owner occupied—business use only |

| Transaction Types | Purchase and refinance |

| Geographic Coverage | All US states except AK, AZ, HI, MN, ND, NV, OR, SD, UT, VT |

| Amortization Structure | Interest-only with balloon at maturity |

| Interest Accrual Method | < $100K: full amount / ≥ $100K: as disbursed |

Extensions

Our South Carolina bridge loans are structured for 12 to 24 months. Most projects finish well before the loan matures. However, if you need more time, extensions are available up to 50% of the original term.

Extension Limits

| Initial Loan Term | Maximum Extension |

|---|---|

| 12 months | 6 months |

| 18 months | 9 months |

| 24 months | 12 months |

Extension Terms and Fees

| Extension Term | Fee |

|---|---|

| 3 months (1st request) | 1% of total loan amount |

| 3 months (2nd request) | 1.5% of total loan amount |

| 6 months (1st request) | 2.5% of total loan amount |

Extension fees are added to your final payoff balance.

Extension Prerequisites

Before an extension is approved:

Your builder’s risk insurance must stay active through the extended term.

Any additional lender conditions must be satisfied.

Important: Extensions should be viewed as a backup plan—not part of your core investment strategy.

Ineligible Property Types

We fund non-owner occupied 1–4 unit residential properties only. The following property types are not eligible for the South Carolina Bridge Loan Program:

Mixed-use properties

5+ unit multifamily

Condotels

Co-ops

Mobile or manufactured homes

Commercial properties

Cabins or log homes

Properties with oil or gas leases

Active farms, ranches, or orchards

Vacation or seasonal rentals

Exotic, unique, or luxury homes

Properties with unpaved access

Exception Scenarios

Certain edge cases may be reviewed individually:

| Extension Term | Fee |

|---|---|

| 3 months (1st request) | 1% of total loan amount |

| 3 months (2nd request) | 1.5% of total loan amount |

| 6 months (1st request) | 2.5% of total loan amount |

Approval is not guaranteed and depends on underwriting discretion.

Borrower and Guarantor Requirements

We have strict requirements for South Carolina borrowers and guarantors to ensure strong project outcomes:

| Item | Requirements |

|---|---|

| Borrowing Entities | LLC or Corporation only (no nonprofits) |

| Eligible Borrowers | U.S. Citizens, Permanent Residents, select Foreign Nationals |

| Credit Requirements | 680 minimum FICO score |

| Liquidity | Cash to close + 25% of rehab budget |

| Verification of Liquidity | Two most recent statements (bank, brokerage, retirement) |

| Guaranty Structure | 51% of entity must guarantee (100% for cash-out refinances) |

| Recourse | Full recourse required |

| Aggregate Net Worth | Must be at least 50% of the loan amount |

Liquidity Verification

To ensure financial stability throughout your South Carolina project, we verify liquidity based on these standards:

Eligible accounts: personal bank, business bank, brokerage, retirement (50% haircut on retirement funds)

No requirement to transfer or consolidate accounts

Down payment must be wired directly to the title company

Pro Tip: Having a business bank account is strongly recommended for better financial management.

Credit and Background Items

We carefully evaluate creditworthiness and background history for all borrowers and guarantors.

| Scenario | Requirement |

|---|---|

| Middle credit score | Used if 3 scores available; lowest of 2 if only 2 |

| No mortgage tradelines | Require 6 months of interest reserves |

| Fewer than 5 credit tradelines | Require 6 months of interest reserves |

| Bankruptcy | Must be discharged 4+ years prior |

| Foreclosure | Must be completed 4+ years prior |

| Bankruptcy or foreclosure within 4–7 years | Requires 3 months reserves |

| Late mortgage payments (past 12 months) | LOE required |

| Past due balances | Must be cleared before funding |

| Involuntary liens or judgments | Must be cleared |

| Pending civil lawsuits | LOE required; subject to review |

| Pending criminal lawsuits | Ineligible |

| Financial crimes | Ineligible |

| Repeat criminal offenses | LOE required; subject to review |

Interest Reserves

Interest reserves are payments collected upfront and held in escrow to cover future interest payments during the loan term. The amount required depends on your credit profile and overall application strength.

Interest Reserve Requirements

| Guarantor FICO Score / Scenario | Interest Reserve Requirement |

|---|---|

| Lender discretion | 0 months |

| Guarantor FICO 700+ | 1 month |

| Guarantor FICO 660–699 | 3 months |

| FICO 660–699 with concerning credit or background | 6 months |

Note: Stronger credit profiles enjoy lighter reserve requirements.

Financed Interest Payments

To help you manage cash flow during your South Carolina rehab project, you may qualify for financed interest payments. This means interest accrues and is added to your payoff balance, instead of being paid monthly.

Example:

| Item | Amount |

|---|---|

| Loan Amount | $100,000 |

| Interest Rate | 12% annual |

| Loan Duration | 9 months |

| Accrued Interest | $9,000 |

Your payoff at closing would include both the principal ($100,000) and the accrued interest ($9,000).

Property Sourcing Guidelines

At OfferMarket, we ensure that every South Carolina deal we finance is well-vetted for success. Here's how we approach property eligibility:

New market transactions require either:

A signed General Contractor (GC) agreement, or

A Letter of Explanation (LOE) detailing why a GC isn't needed

For wholesale transactions, prior sale price increases, or non-arm’s-length deals, extra documentation will be required.

Projects involving major structural changes (such as additions) may require:

Architectural plans

Engineer letters

Applicable permits

Bridge Loan Insurance Guidelines

Protecting your South Carolina investment property is just as important as financing it. OfferMarket requires every property funded through our South Carolina Bridge Loan Program to carry appropriate insurance coverage throughout the life of the loan.

This specialized coverage is often referred to as Builders Risk Insurance or Fix and Flip Insurance—designed for properties under construction, vacant, or undergoing significant renovations.

Coverages and Limits

| Coverage Type | Required Limit |

|---|---|

| Dwelling Coverage | Replacement cost or loan amount (no coinsurance) |

| Liability Coverage | $1M per occurrence / $2M aggregate |

| Builders Risk | Included in standard policy |

| Flood Insurance | Greater of $250,000 or loan balance if located in FEMA flood zone |

Insurance Policy Details

| Policy Feature | Requirement |

|---|---|

| AM Best Rating | A- VIII or higher |

| Policy Type | Special Form |

| Deductible | Between $1,000 and $5,000 |

| Lender’s Designation | OfferMarket listed as Mortgagee and Additional Insured |

| Coverage Exclusions | No exclusions for windstorm, hail, or named storms |

| Cancellation Notice | 30-day notice minimum |

Pro Tip for South Carolina Investors:

After taking ownership, install smoke detectors, secure locks, and set up security cameras immediately. This not only protects your property but also ensures compliance with insurance requirements—preventing claims from being denied due to missing basic protections.

Frequently Asked Questions

What states does OfferMarket fund bridge loans?

- Arizona*

- Alabama

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Mississippi

- Missouri

- Minnesota*

- Montana

- Nebraska

- Nevada*

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota*

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota*

- Tennessee

- Texas

- Utah

- Vermont*

- Virginia

- Washington

- Washington DC

- West Virginia

- Wisconsin

- Wyoming

(*) In states where NMLS license is required for business purpose lending or we do not directly lend, OfferMarket operates as a rate shopping service and refers your loan to a licensed capital provider.

Can I have multiple bridge loans active at the same time?

Absolutely. Many South Carolina investors have multiple active projects funded through OfferMarket bridge loans.

We’ll always help you manage your liquidity, timelines, and exposure smartly to ensure continued success.

Are bridge loans considered commercial loans?

Yes.

Bridge loans through OfferMarket are classified as commercial business-purpose loans, meaning they are issued to your LLC or Corporation—not personally to you.

What is the minimum bridge loan amount?

| Item | Minimum |

|---|---|

| Loan Amount | $25,000 |

Even smaller investment opportunities in South Carolina can qualify under our program.

What types of properties are eligible?

Eligible property types:

Non-owner occupied single-family homes

Townhomes

2–4 unit multifamily residences

Warrantable condominiums

Planned Unit Developments (PUDs)

Not eligible:

Mixed-use properties

5+ unit apartment buildings

Retail, office, or industrial buildings

Condotels

Cooperative housing (co-ops)

Vacation or seasonal rentals

Ultra-luxury or exotic properties

How is Loan-To-Value (LTV) or Loan-To-After-Repair Value (LTARV) calculated?

For South Carolina Bridge Loans, we typically use Loan-To-After-Repair Value (LTARV):

Initial advance is based on the lower of:

Purchase contract price, or

Appraised As-Is value

LTARV is calculated by:

(Initial Advance + Construction Holdback) ÷ ARV

This ensures responsible lending aligned with the project's true post-repair value.

What are the credit score requirements?

| Credit Criteria | Details |

|---|---|

| Minimum Credit Score | 680 |

| Exception Review Range | 660–679 (case-by-case approval possible) |

| Evaluated Parties | All members of the borrowing entity who will personally guarantee the loan |

Do I need prior investing experience to qualify?

Not necessarily!

| Experience Requirement | Details |

|---|---|

| Required Experience | Not mandatory to qualify |

| Benefit of Experience | Greater leverage and better terms for experienced investors |

| Evaluation Method | Based on completed, verifiable rehab projects where you were financially responsible |

Even first-time investors in South Carolina can access our bridge loans, though experience helps secure higher leverage options.

Does wholesaling experience count toward project experience?

| Scenario | Eligibility |

|---|---|

| Acting as wholesaler only | Not counted as completed rehab experience |

Wholesaling provides valuable market insight but does not count toward direct project management experience.

What documentation is required for loan processing?

OfferMarket uses a secure Loan File system for fast, organized loan processing.

For Purchase Transactions:

| Loan File Sections | Documents |

|---|---|

| Purchase Contract | Fully signed by buyer and seller |

| Credit Report | Soft pull tri-merge report for all guarantors |

| Background Report | Required for each guarantor |

| Track Record | Details of completed projects |

| ID Verification | Government-issued ID (license, passport, Green Card) |

| Borrowing Entity | Formation documents, Operating Agreement, Certificate of Good Standing, W-9 |

| Scope of Work | Detailed rehab scope and budget |

| Appraisal Report | Ordered through OfferMarket’s AMC partner |

| Bank Statements | Two most recent personal or business statements |

| Letter of Explanation (LOE) | If requested by underwriting |

For Refinance Transactions:

| Loan File Sections | Documents |

|---|---|

| Settlement Statement | Fully signed |

| Credit Report | Soft tri-merge |

| Background Report | For each guarantor |

| Track Record | Completed investment projects |

| ID Verification | Driver’s license, passport, or Green Card |

| Borrowing Entity | Same as above |

| Sunk Costs List | All costs paid so far |

| Scope of Work | Rehab plan |

| Appraisal Report | Ordered through OfferMarket’s AMC |

| Bank Statements | Two statements |

| Letter of Explanation (LOE) | If applicable |

Glossary of Key Terms

| Term | Definition |

|---|---|

| ADU | Accessory Dwelling Unit — A second, self-contained living space built on the same lot as a primary single-family home. |

| Arms-length | A transaction between unrelated parties acting independently to achieve fair market value. |

| Non Arms-length | A deal where the buyer and seller share a relationship that could affect the fairness of the transaction terms. |

| Initial Advance | The portion of your bridge loan used for the property purchase, wired to the title company at closing. |

| Construction Holdback | The funds reserved specifically for renovation costs, released through draws as work progresses. |

| Interest Reserves | Funds collected upfront to cover interest payments based on creditworthiness and underwriting guidelines. |

| LOE (Letter of Explanation) | A written explanation clarifying underwriting concerns like large deposits, late payments, or legal issues. |

| LTC (Loan-To-Cost) | The ratio of your loan amount to the combined purchase price and renovation expenses. |

| LTFC (Loan-To-Full-Cost) | The ratio of the full loan amount to your total project costs, including both acquisition and rehab. |

| LTV (Loan-To-Value) | Ratio comparing the loan amount to the property’s current As-Is value, often used for refinances. |

| LTARV (Loan-To-After-Repair Value) | Also called ARLTV — compares the total loan amount to the projected value after renovations are complete. |

| As Disbursed Interest | Interest charged only on the disbursed portions of your bridge loan, not the full approved amount. |

| Full Boat Interest | Also called Dutch Interest — interest accrues on the full loan amount from day one, regardless of disbursement. |

| Lopsided Deal | A project where the rehab budget exceeds the purchase price or property value, requiring stricter loan-to-cost limits. |

| GC Agreement | A contract with a licensed General Contractor outlining project work, costs, and schedules. |

| DSCR (Debt Service Coverage Ratio) | A measure of a rental property’s income relative to expenses — must exceed 1.1 after repairs for refinances. |

Get Your Instant Bridge Loan Quote

At OfferMarket Capital LLC, we’re honored to serve real estate investors across South Carolina and the entire United States.

Our specialty? Making real estate financing fast, simple, and reliable — so you can focus on what you do best: finding great opportunities and turning them into profitable investments.

We offer two primary loan products tailored to help you grow your South Carolina real estate portfolio:

Bridge Loans for fix-and-flip, value-add, and rental acquisition strategies

DSCR (Debt Service Coverage Ratio) Loans for long-term rental financing

Every month, thousands of investors benefit from OfferMarket’s services. When you join our free membership, you unlock exclusive resources to supercharge your investing career, including:

💰 Flexible private lending solutions

☂️ Access to insurance rate shopping tools to protect your properties

🏚️ Exclusive off-market property deals

💡 Market insights and data-driven investment strategies

Whether you're tackling your first South Carolina flip or expanding a multi-state portfolio, we are here to make your journey faster, safer, and more profitable.

Get started today and request your instant bridge loan quote!

Let’s grow your real estate business together.

Thousands of real estate investors get value from OfferMarket every month. Membership is entirely free and includes the following benefits:

💰 Private lending ☂️ Insurance rate shopping 🏚️ Off market properties 💡 Market insights