*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Short-Term Rental Loans: 5 Types to Finance an Airbnb (2026)

Financing a short-term rental (STR) like an Airbnb or VRBO requires a different approach than financing a traditional long-term rental. Lenders view STRs as a hybrid between a real estate investment and an active hospitality business, leading to specialized loan products and underwriting criteria. The most powerful tool for STR investors is the Debt Service Coverage Ratio (DSCR) loan, which qualifies you based on the property's rental income potential rather than your personal W-2s or tax returns. This asset-based lending approach allows savvy investors to scale their portfolios without being limited by their personal debt-to-income ratio.

Beyond DSCR loans, investors can leverage other financing vehicles depending on their strategy, including fix and flip loans for renovations, ground-up construction loans for new builds, and even home equity loans on other properties to fund an STR purchase. Understanding these five primary loan types is the first step to successfully acquiring, renovating, or building your next short-term rental investment.

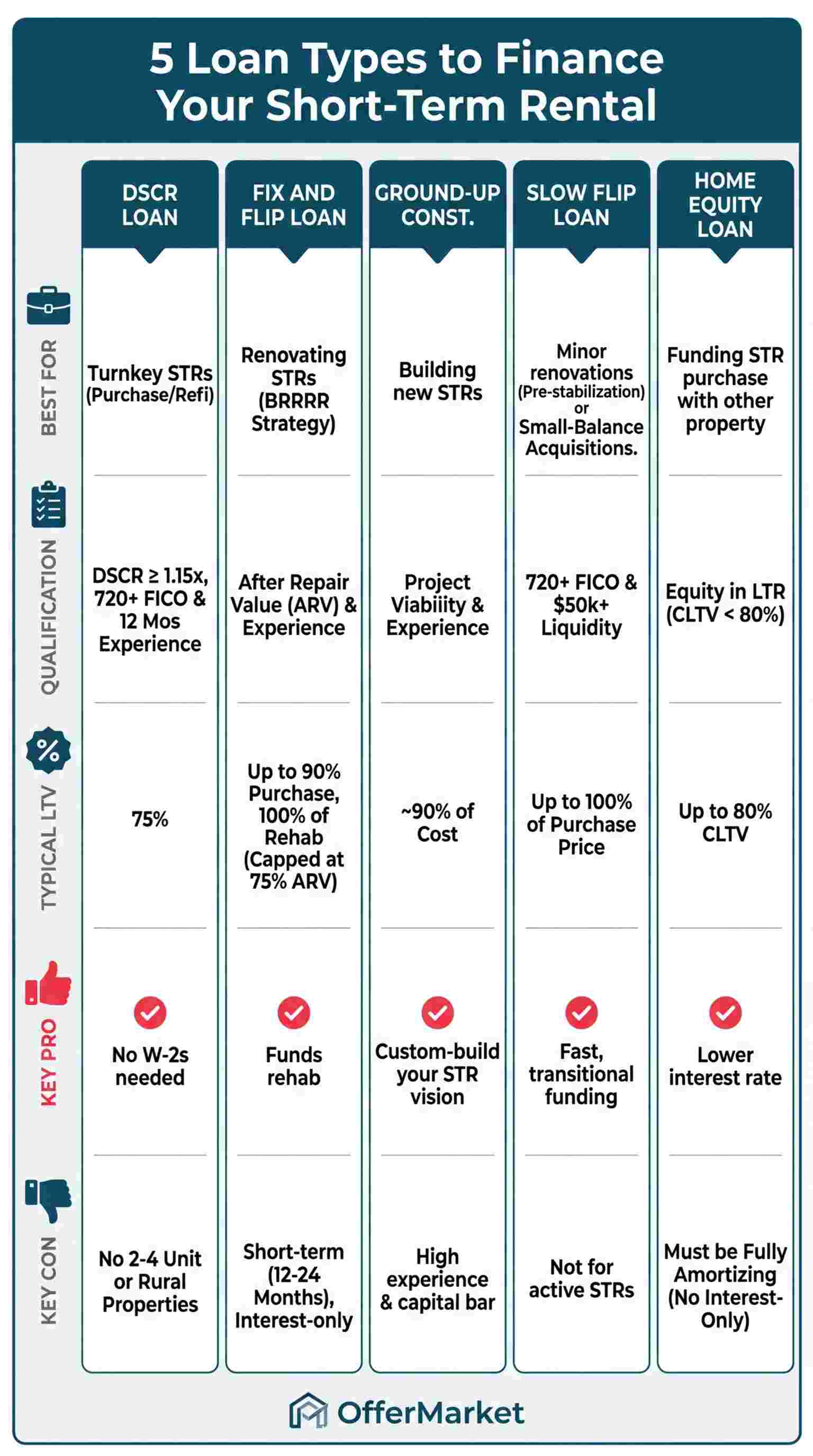

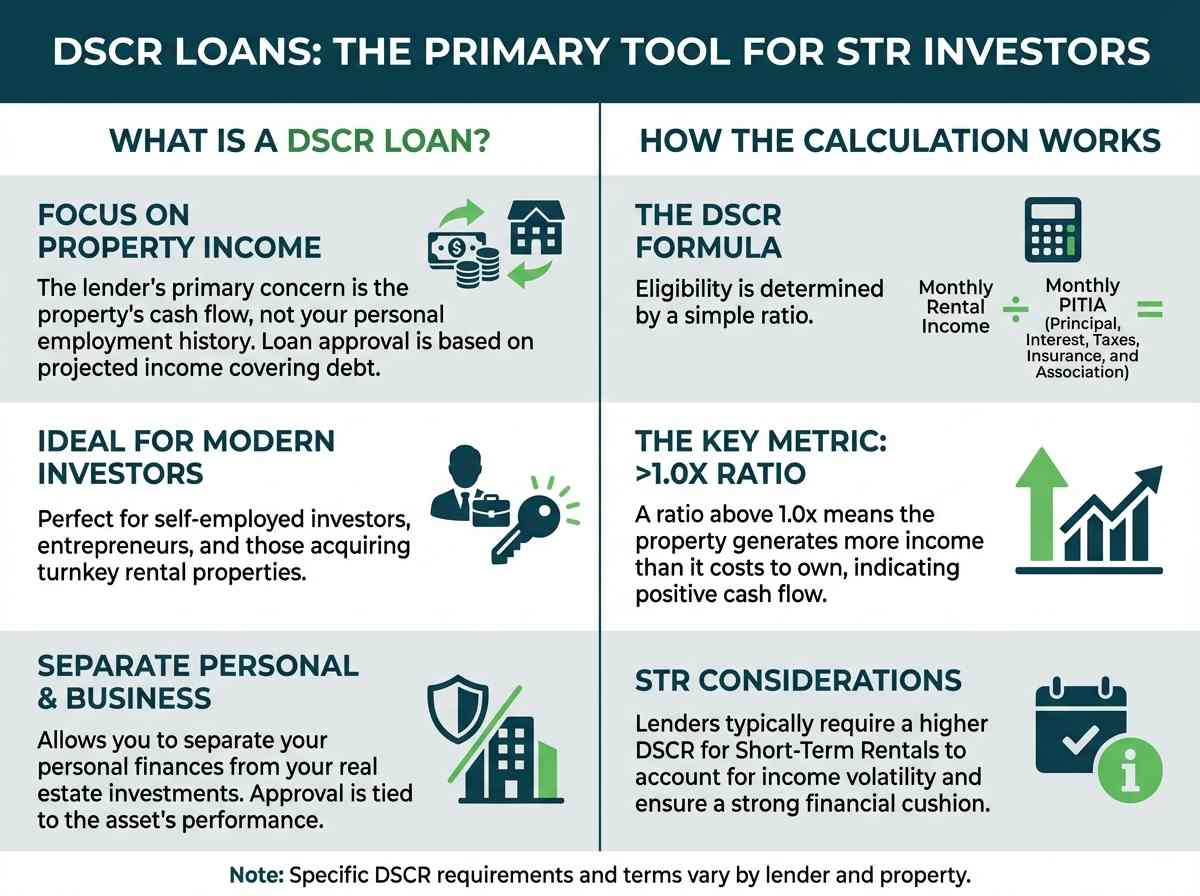

Type 1: DSCR Loans - The Primary Tool for STR Investors

DSCR loans are the go-to financing solution for acquiring or refinancing a turnkey short-term rental property. The core principle of a DSCR loan is simple: if the property's projected income is sufficient to cover its debt obligations, the loan can be approved. This makes it an ideal product for self-employed investors, entrepreneurs, and anyone looking to separate their personal finances from their real estate investments.

The lender's primary concern is the property's cash flow, not your personal employment history. They calculate the Debt Service Coverage Ratio by dividing the property's monthly income by its total debt service (Principal, Interest, Taxes, Insurance and HOA fees - PITIA). A ratio above 1.0x means the property generates more income than it costs to own. For STRs, lenders typically require a higher ratio to account for income volatility.

How Lenders Calculate STR Income

Unlike long-term rentals with a signed lease agreement, short-term rental income is variable. Lenders have developed sophisticated methods to underwrite this income stream confidently.

For a purchase of a new STR property without an operating history, lenders rely on third-party data projections. They will require a report from an approved service like AirDNA to project the subject property's potential Annual Gross Revenue. To qualify, the property must meet a strict minimum Occupancy Rate threshold, which is typically 50% or 60%. To be conservative, lenders then apply an "expense haircut" to this gross revenue projection—multiplying it by 80% (a 20% reduction)—to account for management fees, cleaning costs, and other operational expenses before calculating the DSCR.

For a refinance of an existing STR, the lender will require a minimum of 12 months of operating history, which can be verified through statements from platforms like Airbnb, VRBO, or property management software. The lender averages the income over the last 12 months and then applies the same 20% expense haircut (multiplying the average monthly gross income by 80%) to establish the final qualifying income figure used to calculate the DSCR.

Common STR Underwriting Overlays

Because of the perceived higher risk associated with the hospitality-like nature of STRs, lenders apply specific underwriting rules, or "overlays," that differ from those for long-term rentals.

- Reduced Loan-to-Value (LTV): While a long-term rental might qualify for 80% LTV (requiring a 20% down payment), an STR loan is often capped at 75% LTV, meaning you'll need a 25% down payment. This extra equity reduces the lender's risk.

- Higher DSCR Minimums: A long-term rental might only need a DSCR of 1.0x or 1.10x to qualify. For a short-term rental, the minimum DSCR is almost always higher, frequently set at 1.15x or even 1.20x. This ensures a larger cash flow buffer to handle seasonal dips in occupancy or revenue.

DSCR Loan Qualification for Short-Term Rentals

Meeting the qualification criteria for an STR DSCR loan involves more than just the property's cash flow. Lenders also assess your financial stability and experience as an investor.

Minimum Credit Score: A minimum FICO score of 720+ is typically required to qualify. A higher credit score signals financial responsibility and reduces the perceived risk for the lender.

Down Payment: As mentioned, expect a minimum down payment of 25%. For investors with lower credit scores or less experience, the lender may require a 30% down payment to further mitigate risk.

DSCR Hurdle: The property must demonstrate it can meet the lender's DSCR requirement, which is often 1.15x or higher. This is a non-negotiable metric. If the projected income doesn't support this ratio, the loan will likely be denied, or the LTV will be reduced until the ratio is met.

Investor Experience: This is a critical factor, especially for purchases. Most lenders will not allow a first-time real estate investor to use projected STR income to qualify. They typically require you to own at least one other investment property (which can be a long-term rental) to demonstrate you understand the fundamentals of property management and real estate investing. For refinances, the 12-month operating history serves as proof of experience with that specific property.

Type 2: Fix and Flip Loans - For Acquiring and Renovating Future STRs

While DSCR loans are perfect for rent-ready properties, they aren't suitable for assets that require significant renovation. If your strategy is to buy a distressed property, add value through improvements, and then launch it as a short-term rental, a fix and flip loan is your ideal starting point. These are short-term, interest-only bridge loans designed to cover both the acquisition and renovation costs of a property.

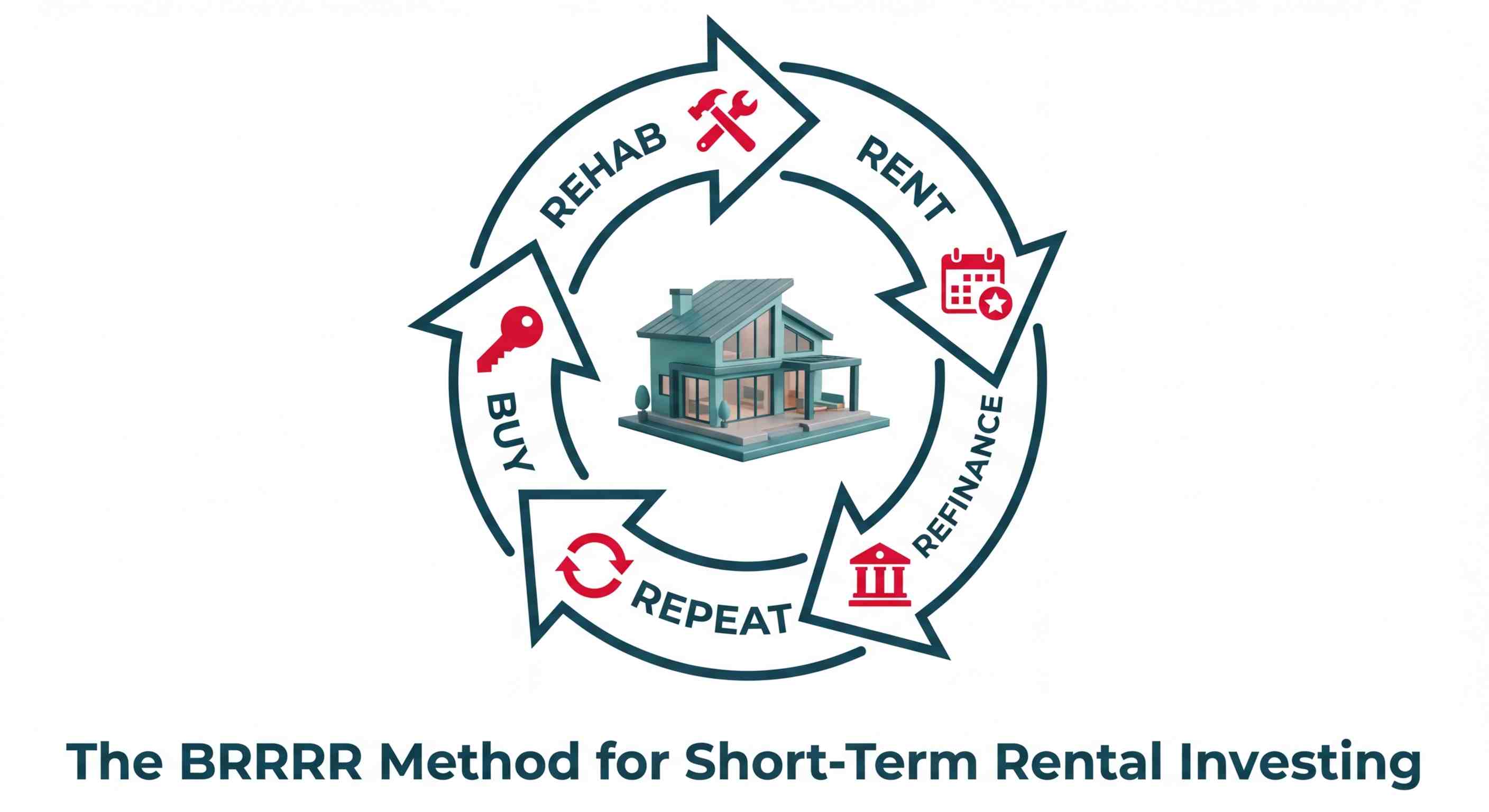

This financing is the first step in the popular "BRRRR" (Buy, Rehab, Rent, Refinance, Repeat) strategy, adapted for the short-term rental market. The goal is not to sell the property after renovation (a "flip"), but to refinance into a long-term loan and hold it as a cash-flowing rental.

How to Structure a BRRRR Strategy for a Short-Term Rental

The BRRRR method allows you to build a portfolio with potentially little to no money left in the deal after refinancing. Here's how it works for an STR:

Buy: You identify an undervalued property in a strong vacation rental market. You secure a fix and flip loan to purchase it, often financing up to 90% of the purchase price.

Rehab: The same fix and flip loan provides 100% of the renovation budget. You execute your renovation plan, focusing on creating a desirable, marketable space for vacationers. This includes not just structural repairs but also furnishing and staging the property.

Rent: Once the renovation is complete and the property is furnished, you launch it on platforms like Airbnb and VRBO. You begin generating rental income and building an operating history.

Refinance: After a "seasoning" period (typically 6 months), you refinance the short-term fix and flip loan into a long-term DSCR loan. The refinance appraisal is based on the new, higher After Repair Value (ARV), not your original purchase price. This allows you to pull out your initial capital (down payment, closing costs) and sometimes even more.

Repeat: You take the capital you've pulled out and use it as the down payment for your next BRRRR project, scaling your STR portfolio.

Refinancing From a Fix and Flip Loan into a Permanent DSCR Loan

The exit strategy is the most critical component of a fix and flip loan. The lender needs to be confident that you can pay off the short-term, high-interest bridge loan. When your goal is to hold the property as an STR, the exit is a refinance into a permanent DSCR loan.

To underwrite the initial fix and flip loan, the lender will analyze your projected exit. They will look at STR income data from AirDNA for the area to ensure that once stabilized, the property's income will be sufficient to qualify for a DSCR loan. You will need to present a clear budget, renovation plan, and income projections to get the initial bridge loan approved.

It's important to note that you cannot operate the property as an active vacation rental while it is financed by a fix and flip loan. These loans are for properties in a transitional state (i.e., under renovation). The rental income generation begins after the rehab is complete, just before you initiate the refinance process.

Fix and Flip Loan Qualification

Qualification for fix and flip loans is heavily based on the viability of the project and the experience of the investor.

Leverage: Lenders typically offer high leverage, such as up to 90% of the purchase price and 100% of the renovation costs, not to exceed 75% of the property's After Repair Value (ARV).

Experience Requirements: While some lenders work with first-time flippers, you will receive significantly better terms (higher leverage, lower interest rates) if you have a verified track record of successful projects. Lenders want to see that you can manage a renovation budget and timeline effectively.

Loan Term: These are short-term loans, typically for 12 months, though some programs offer up to 18 or 24 months. Payments are interest-only, which keeps your holding costs low during the renovation phase when there is no income.

Exit Strategy: This is the key underwriting focus. You must present a clear and convincing plan to either sell the property or refinance into a long-term loan. For an STR BRRRR, this means showing the lender that the post-renovation property will meet all the criteria for a DSCR loan.

Type 3: Ground-Up Construction Loans - Building a New STR Property

For investors with a vision to create a custom-built short-term rental from scratch, a ground-up construction loan is the necessary financing vehicle. This type of loan funds the entire construction process, from site work and foundation to framing and final finishes. It is the most complex and demanding type of financing, reserved for experienced builders and developers.

These loans are structured to disburse funds in stages, or "draws", as construction milestones are completed. The lender will require inspections at each stage to verify progress before releasing the next round of funding. This ensures that the loan proceeds are being used as intended and that the project is staying on track and on budget.

The Two-Step Financing Process

Financing a new STR construction is a two-loan process, similar to the BRRRR strategy:

The Construction Loan: This is a short-term, interest-only loan (typically 12-18 months) that covers the cost of construction. The lender underwrites the loan based on the total project cost and the "as-complete" appraised value of the future property.

The Permanent Loan (DSCR Refinance): Upon completion of construction and issuance of a Certificate of Occupancy, the property is ready to be operated as an STR. The investor then refinances the construction loan into a long-term, permanent DSCR loan. The lender will use projected income from AirDNA to qualify the property for the DSCR loan, allowing the investor to pay off the construction debt and begin amortizing the permanent mortgage.

A key underwriting consideration is the status of the land. If the land was purchased less than 12 months prior to the loan application, the lender will typically base the loan on the total project cost (land purchase price + hard & soft construction costs). If the land has been owned for more than 12 months, the lender may use the current appraised value of the land, which can increase the total leverage available for the project.

Ground-Up Construction Loan Qualification

Lenders have extremely strict requirements for ground-up construction loans due to the high level of risk involved.

Experience Mandate: This is the most significant hurdle. Lenders will not approve a construction loan for an investor without a proven track record of successfully completing similar ground-up construction projects. You will need to provide a portfolio of past projects, including budgets, timelines, and photos. This is a non-negotiable requirement.

Capital & Liquidity: You must have significant cash reserves. Lenders will require you to have liquidity to cover potential cost overruns, carrying costs (interest payments during construction), and a down payment that could be 20-25% of the total project cost.

Project Viability: The project itself will be heavily scrutinized. The lender must approve your general contractor, your detailed construction budget (line-item by line-item), architectural plans, and all necessary permits. They need to be confident that the project is feasible, well-planned, and compliant with all local regulations.

Leverage Limits: Leverage is typically based on a percentage of the total project cost or the loan-to-as-completed-value. For example, a lender might offer to finance up to 90% of the total cost, or 70% of the as-completed appraised value, whichever is less.

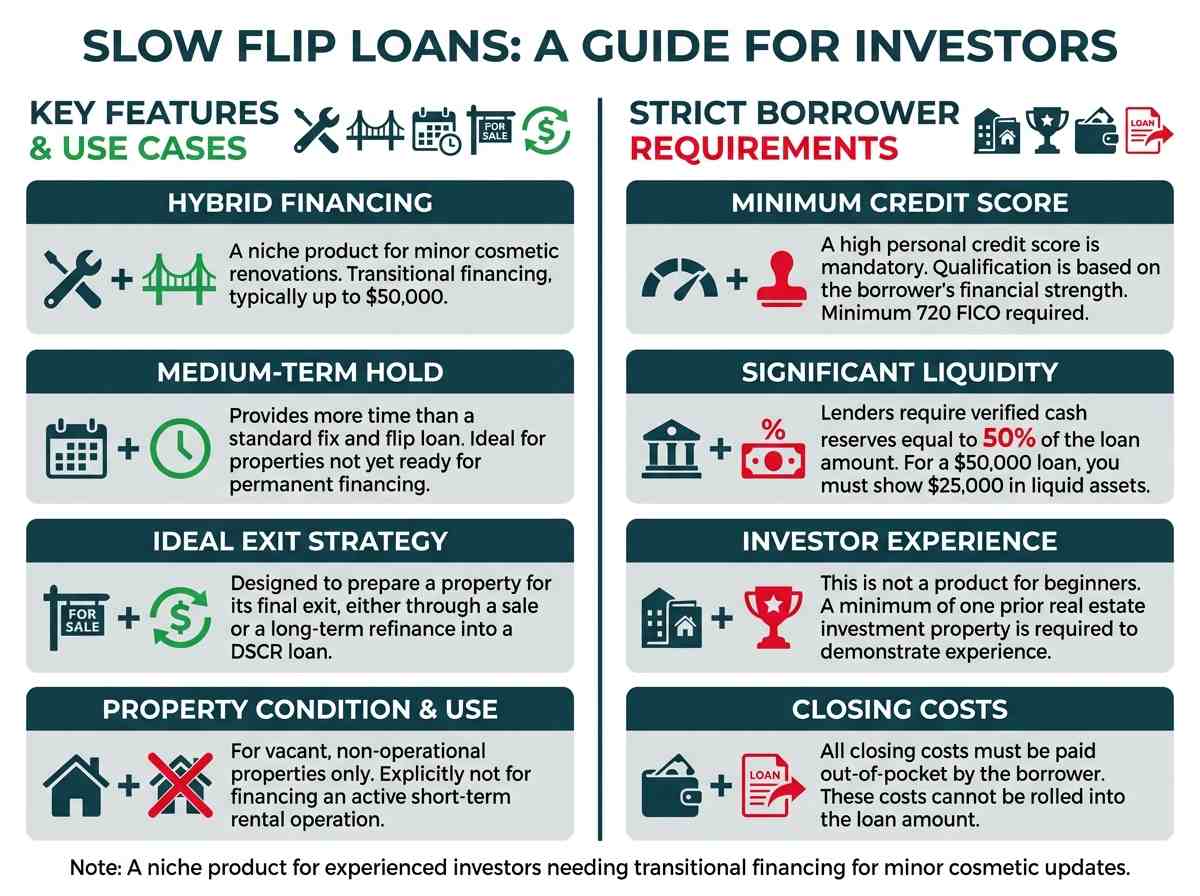

Type 4: Slow Flip Loans - A Niche Product for Minor Renovations

Slow flip loans are a specialized, niche product that can be thought of as a hybrid between a bridge loan and a hard money loan. They are designed for investors who need transitional financing for a property that requires minor cosmetic updates but is not a full-gut renovation. This product is best suited for situations where a small amount of capital—typically up to $50,000—is needed to prepare a property for its final exit strategy, whether that's a sale or a long-term refinance.

A key feature of a slow flip loan is its function as a medium-term hold solution. It provides a bridge for investors who need more time than a typical 12-month fix and flip loan allows but are not yet ready for permanent financing.

However, it is crucial to understand that this loan product is explicitly not designed for financing an active short-term rental operation. The property must be vacant and non-operational. It can be used to acquire and lightly renovate a future STR, but like a fix and flip loan, it must be refinanced into a DSCR loan once the property is ready to be rented out.

Slow Flip Loan Qualification

Qualification for a slow flip loan is heavily dependent on the borrower's personal financial strength, rather than the property's cash flow potential.

Credit Score: A high personal credit score is mandatory, with a minimum FICO of 720 required. This demonstrates a strong history of financial responsibility.

Liquidity: Lenders require significant verified cash reserves. Typically, the borrower must have liquid assets (cash in the bank) equal to at least 50% of the requested loan amount. For a $50,000 loan, this means you would need to show proof of at least $25,000 in cash reserves.

Investor Experience: This is not a product for beginners. A minimum of one prior real estate investment property is required to demonstrate experience.

Closing Costs: All closing costs must be paid out-of-pocket by the borrower. Unlike some other loan programs, these costs cannot be rolled into the loan amount.

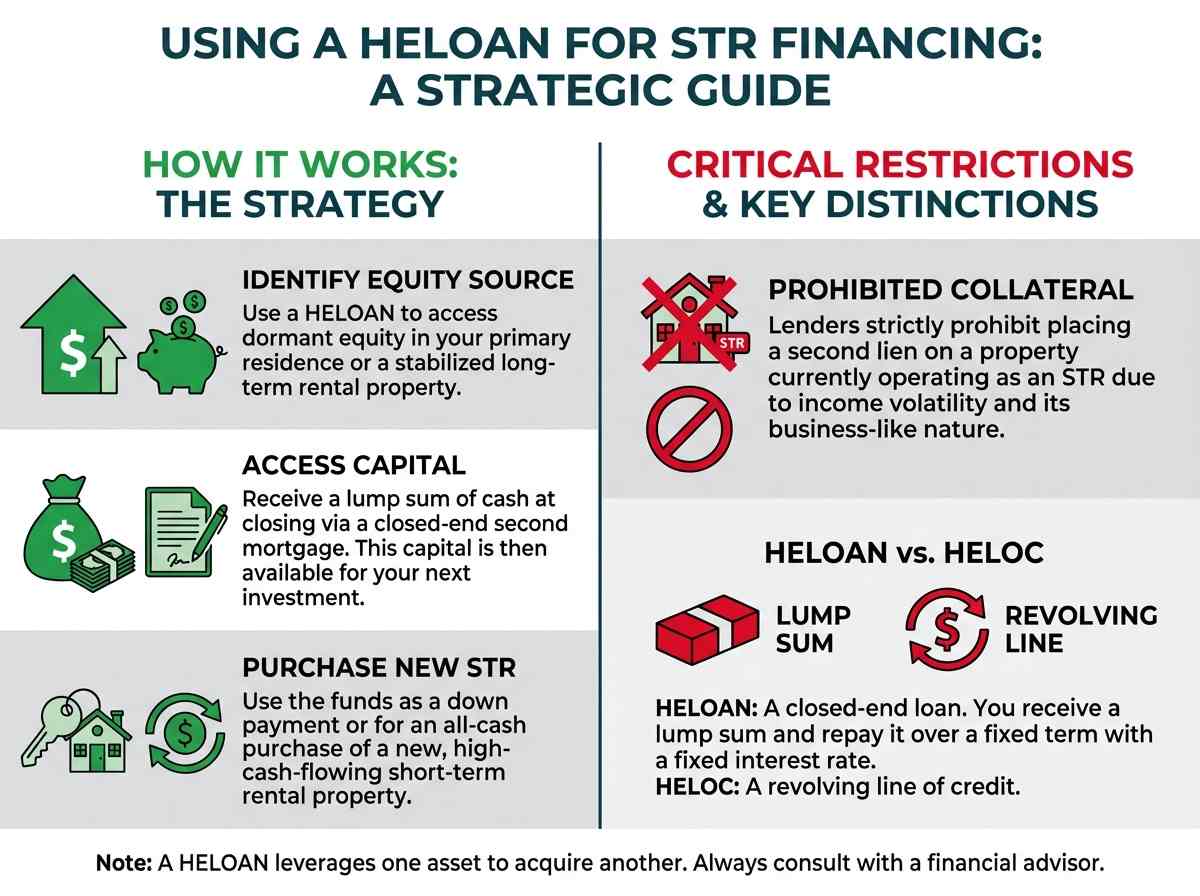

Type 5: Home Equity Loans - Accessing Equity in Long-Term Rentals Only

A Home Equity Loan (HELOAN) can be a strategic tool for financing a short-term rental purchase, but with one critical and non-negotiable caveat: the loan cannot be placed on a property that is currently operating as a short-term rental. Lenders strictly prohibit placing a second lien on an STR due to the income volatility and business-like nature of the asset.

Instead, investors can use a HELOAN to tap into the equity of a different property in their portfolio, such as their primary residence or a stabilized long-term rental. By taking a cash-out second mortgage on a property with a traditional lease, you can access capital to use as a down payment or even for an all-cash purchase of a new short-term rental property.

This strategy allows you to leverage dormant equity in one asset to acquire a new, high-cash-flowing asset. A HELOAN is a closed-end second lien, meaning you receive a lump sum of cash at closing and repay it over a fixed term with a fixed interest rate. This is different from a Home Equity Line of Credit (HELOC), which is a revolving line of credit.

Home Equity Loan Qualification

To qualify for a HELOAN on an investment property, the property must be a stabilized long-term rental.

Property Type: The subject property for the HELOAN must be a long-term rental with a valid, executed lease agreement in place. The lender will require a copy of the lease and may verify the tenant's payment history. Properties listed on Airbnb or VRBO are strictly ineligible.

Combined Loan-to-Value (CLTV): Lenders will cap the total debt on the property. The sum of the existing first mortgage and the new home equity loan cannot exceed 80% of the property's current appraised value. For example, if your long-term rental is worth $500,000 and your existing mortgage is $300,000 (60% LTV), your maximum HELOAN would be $100,000, bringing your total debt to $400,000 (80% CLTV).

Credit Score: A minimum FICO score of 680 is required.

Reserves: One of the advantages of this loan type is that there is typically no cash reserve requirement, as the equity in the property serves as sufficient collateral for the lender.

Unlock Your STR Investment Quote

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →How to Choose the Right Short-Term Rental Loan

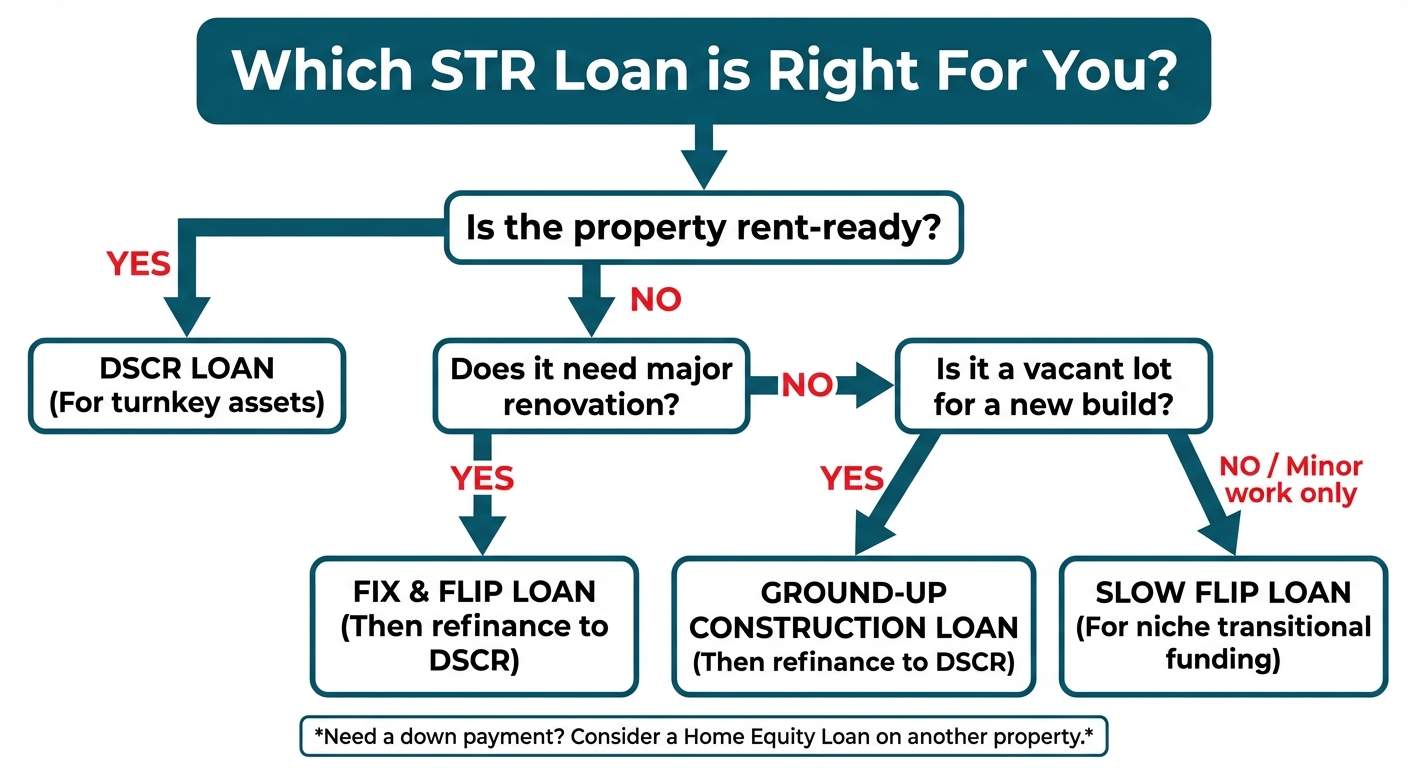

Selecting the correct financing is just as important as choosing the right property. The optimal loan for your project depends entirely on your investment strategy, the property's condition, and your personal financial profile. Aligning these three elements will ensure you have the right capital structure for success.

Aligning Financing with Your Investment Strategy

Your overarching goal for the property will dictate the type of loan you need.

Buy-and-Hold (Turnkey): If you are purchasing a move-in ready property that is already operating as an STR or requires only minor cosmetic updates, the DSCR Loan is your best choice. It offers a long-term, 30-year fixed-rate mortgage based on the property's income potential.

Buy, Renovate, and Hold (BRRRR): If your strategy is to buy a distressed property, force appreciation through renovation, and then operate it as an STR, you will need a two-loan process. Start with a Fix and Flip Loan to cover the purchase and rehab, then refinance into a permanent DSCR Loan once the property is stabilized.

Build-and-Hold: For investors building a custom STR from the ground up, the path is similar to the BRRRR strategy. You will begin with a Ground-Up Construction Loan and then refinance into a DSCR Loan upon completion.

Assessing Property Condition

The physical state of the property is a primary determinant of the loan type.

Move-in Ready: Properties that are in excellent condition and ready to be listed on Airbnb immediately are prime candidates for a DSCR Loan.

Distressed Asset: A property that is uninhabitable or requires significant renovation (e.g., new kitchen, roof, structural work) cannot qualify for a DSCR loan. It must be financed with a short-term bridge product like a Fix and Flip Loan.

Minor Cosmetic Needs: For properties that need only light updates (e.g., paint, new fixtures, landscaping) and you need transitional funding, a Slow Flip Loan could be a niche option, but remember it must be refinanced before you can begin renting it out.

The STR Loan Application Process: A Step-by-Step Guide

At OfferMarket, we've streamlined the loan application process to be as transparent and efficient as possible. Understanding the steps involved helps you prepare and ensures a smooth journey from application to closing.

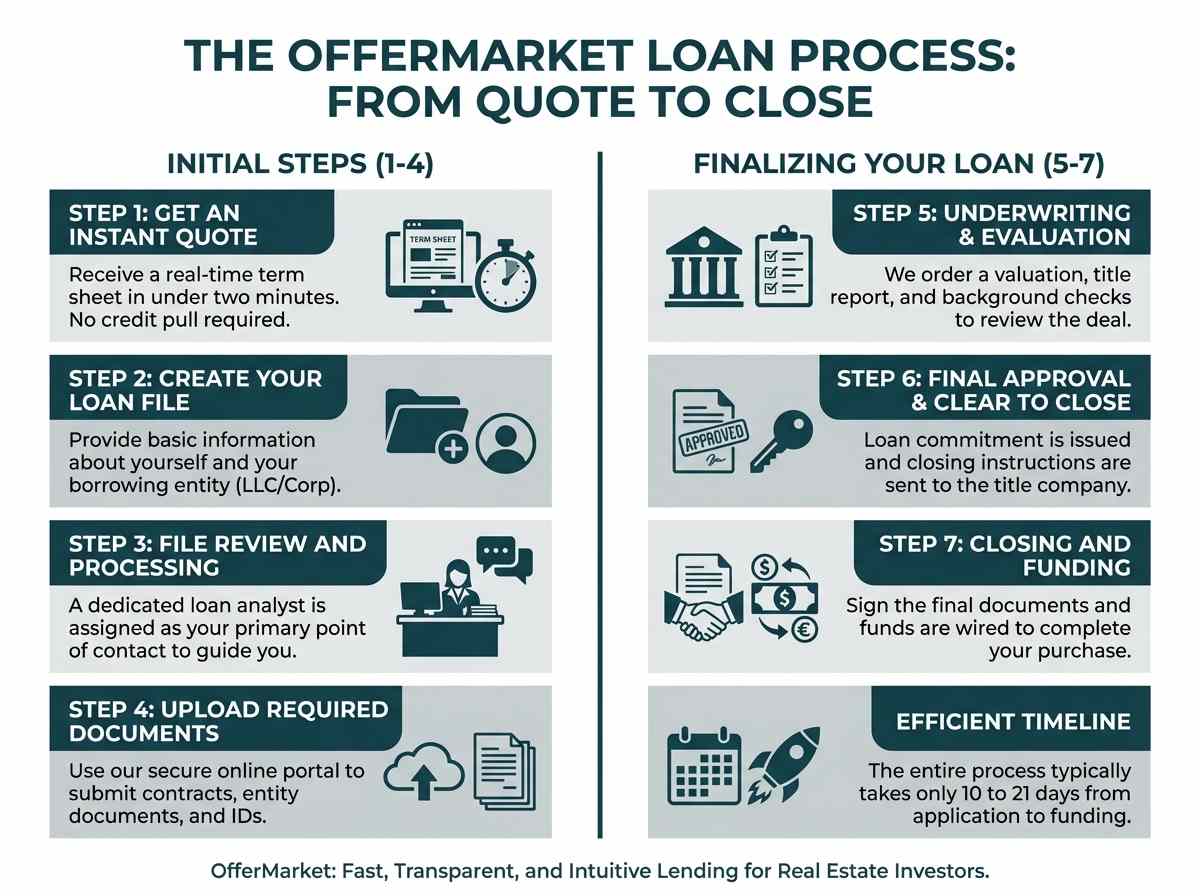

Step 1: Get an Instant Quote

Start by entering your property address and project details into our instant quote tool. In less than two minutes, you'll receive a real-time term sheet outlining your estimated loan amount, interest rate, leverage, and key terms—without a credit pull.

Step 2: Create Your Loan File

If the terms look good, proceed by creating your loan file. You'll provide basic information about yourself and your borrowing entity (typically an LLC or corporation), along with a few high-level details about the project.

Step 3: File Review and Processing

Once submitted, your file enters our processing queue and is assigned to a dedicated loan analyst. This person becomes your primary point of contact and helps guide you through the rest of the process.

Step 4: Upload Required Documents

Using our secure online portal, you’ll upload the required documents—typically including your entity formation documents, government ID, purchase contract, and renovation scope of work. Keeping these documents organized helps speed up approval.

Step 5: Underwriting and Property Evaluation

While documents are being uploaded, our team begins the underwriting process. This includes ordering a valuation (often a desktop appraisal to save time and cost) and running title and background checks. The underwriter reviews the deal to ensure it meets lending guidelines.

Step 6: Final Approval and Clear to Close

Once underwriting is complete and all conditions are satisfied, your loan receives final approval and a “clear to close.” We issue the loan commitment and send closing instructions and documents to the title company or closing attorney.

Step 7: Closing and Funding

You’ll sign the closing documents, and funds are wired to the title company to complete the transaction. From application to funding, the process typically takes 10 to 21 days, allowing investors to move quickly on opportunities.

Get Your Instant Short-Term Rental Loan Quote

Ready to take the next step? The best way to understand your specific financing options is to see the numbers for yourself. Use our free, secure quote tool to see real rates and terms for your short-term rental project in under two minutes.

There is no impact on your credit score and no obligation to proceed. Our platform allows you to compare different loan scenarios and use our integrated DSCR calculator to analyze your next deal with confidence.

If you have questions about your STR portfolio goals or a specific property, our team of loan specialists is ready to help you navigate the financing process and find the perfect loan for your investment strategy.

Get Your Instant Loan Quote

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →

OfferMarket Loans

Check your rate

60 seconds · no credit pull