*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Find Private Hard money Lenders Who Fund on ARV

Private hard money lenders who fund based on After-Repair Value (ARV) are essential partners for real estate investors. Unlike traditional banks that focus heavily on personal income and tax returns, ARV-based lenders underwrite the deal itself. They prioritize the property's potential profitability, allowing you to scale your business by leveraging the value you create. This guide breaks down the top ARV lenders and explains exactly how they evaluate and fund your projects.

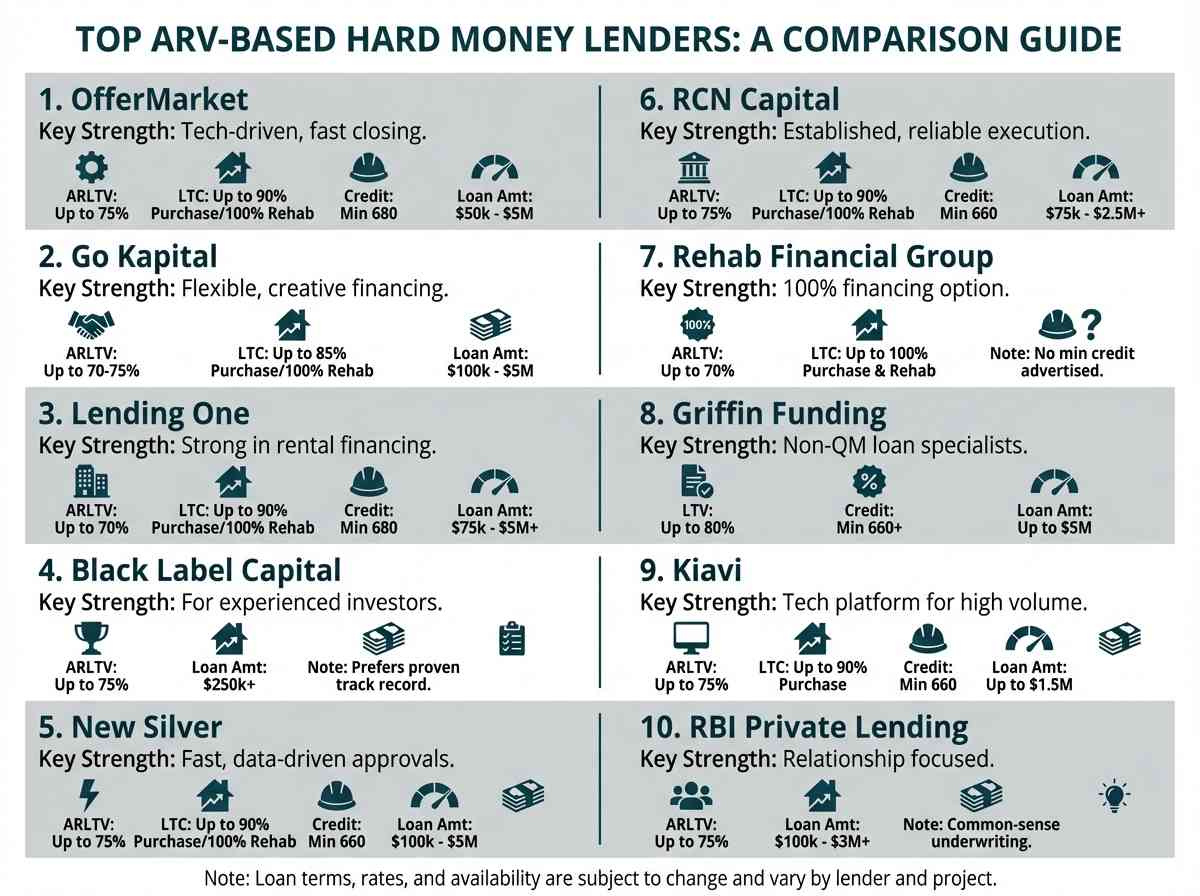

Top 10 Private Hard Money Lenders for ARV-Based Funding

Finding the right lending partner is critical for the success of your real estate investments. A great lender offers more than just capital; they provide speed, flexibility, and a deep understanding of the local market. Below is a comprehensive review of the top 10 private hard money lenders who specialize in ARV-based financing, with a focus on their products, strengths, and lending parameters.

1. OfferMarket: The Premier Choice for Modern Real Estate Investors

OfferMarket stands out as the top choice for savvy real estate investors due to its technology-first approach and unwavering focus on deal economics. We underwrite loans based on the asset's potential, specifically its After-Repair Value and projected profitability, not your personal tax returns. This philosophy allows investors to scale their operations without being constrained by traditional income verification hurdles.

Our platform is designed for speed and efficiency. Investors can get an instant quote online in minutes, utilize modern tools like desktop appraisals to save time and money, and manage construction draws through a streamlined app. This tech-driven process enables closings in as little as 10 to 21 days, a critical advantage in competitive markets.

Loan Products Offered

We offer a comprehensive suite of loan products tailored to every investor strategy, including Fix and Flip loans, DSCR loans for rentals, New Construction loans, Slow Flip loans for projects that take longer than 12 months, and HELOANs (Home Equity Loan as an Alternative to a HELOC).

Key Strengths and Specializations:

- Technology-Driven: Instant online quotes, desktop appraisals, and an app-based draw process.

- ARV-Focused Underwriting: The deal's profitability is the primary consideration.

- Speed: Closings in 10-21 days.

- Comprehensive Support: Dedicated loan officers provide expert guidance from application to closing.

Typical Loan Parameters:

- LTV/LTC: Up to 90% of purchase price and 100% of rehab costs.

- ARLTV: Up to 75% of the After-Repair Value.

- Loan Amount: $50k to $5M.

- Credit Score: Minimum 680.

Geographic Focus: Nationwide, with a strong presence in major real estate markets.

2. Go Kapital

Go Kapital is a direct private lender that offers a range of financing solutions for real estate investors. They are known for their flexible underwriting and ability to fund deals that may not fit into the strict boxes of other lenders. Their approach is relationship-based, focusing on understanding the investor's project and goals.

Loan Products Offered: Fix and Flip, Bridge Loans, Rental Loans, New Construction, and Commercial Real Estate Loans.

Key Strengths and Specializations: They specialize in providing quick and flexible capital for time-sensitive transactions. Go Kapital is often praised for its creative financing solutions and willingness to work with both new and experienced investors.

Typical Loan Parameters:

- LTV/LTC: Typically up to 85% of purchase and 100% of rehab.

- ARLTV: Up to 70-75%.

- Loan Amount: $100k to $5M.

- Term: 12-24 months.

Geographic Focus: Primarily focused on Florida and select other states.

3. Lending One

Backed by a major financial institution, Lending One combines the speed and flexibility of a private lender with the resources of a larger company. They have a strong reputation for reliability and have funded thousands of loans for real estate investors across the country.

Loan Products Offered: Rental Loans (including DSCR), Fix and Flip, New Construction, and Multifamily Bridge Loans.

Key Strengths and Specializations: Lending One is particularly strong in the rental financing space, offering competitive DSCR loans for investors looking to build a portfolio. Their technology platform helps streamline the application and closing process.

Typical Loan Parameters:

- LTV/LTC: For fix and flip, up to 90% of purchase and 100% of rehab.

- ARLTV: Up to 70%.

- Loan Amount: $75k to $5M+.

- Credit Score: Minimum 680.

Geographic Focus: Nationwide, with the exception of a few states.

4. Black Label Capital

Black Label Capital positions itself as a lender for professional real estate investors. They emphasize a partnership approach, working closely with experienced developers and flippers on their projects. Their underwriting is heavily focused on the investor's track record and the viability of the specific deal.

Loan Products Offered: Fix and Flip, Bridge Loans, New Construction, and Multifamily financing.

Key Strengths and Specializations: They excel at funding larger, more complex projects for experienced investors. Their team is comprised of real estate professionals who bring a deep understanding of development and construction to the underwriting process.

Typical Loan Parameters:

Geographic Focus: Nationwide.

5. New Silver

New Silver is a technology-forward lender that leverages data and algorithms to provide fast funding decisions. Their platform is designed to be user-friendly, allowing investors to apply and get approved in a matter of minutes, making them a strong choice for investors who value speed and efficiency.

Loan Products Offered: Fix and Flip, Rental Loans (DSCR), and Ground-Up Construction.

Key Strengths and Specializations: Their "FlipScout" tool, which helps investors analyze potential deals, and their rapid approval process are key differentiators. They offer innovative products like a 30-year rental loan and flexible construction financing.

Typical Loan Parameters:

- LTV/LTC: Up to 90% of purchase and 100% of rehab.

- ARLTV: Up to 75%.

- Loan Amount: $100k to $5M.

- Credit Score: Minimum 660.

Geographic Focus: Operates in most states across the U.S.

6. RCN Capital

RCN Capital is one of the largest and most established private lenders in the country. They have a long history of providing reliable financing for non-owner occupied residential and commercial real estate projects. Their size allows them to offer a wide range of products and lend in nearly every state.

Loan Products Offered: Fix and Flip, Long-Term Rental (DSCR), Bridge Loans, and New Construction.

Key Strengths and Specializations: RCN is known for its disciplined underwriting and consistent execution. They are a go-to lender for both new and experienced investors looking for a dependable financing partner. They also offer financing for short-term rentals (STRs).

Typical Loan Parameters:

- LTV/LTC: Up to 90% of purchase and 100% of rehab for experienced borrowers.

- ARLTV: Up to 75%.

- Loan Amount: $75k to $2.5M+.

- Credit Score: Minimum 660.

Geographic Focus: Nationwide, except for a few states.

7. Rehab Financial Group

Rehab Financial Group (RFG) carves out a unique niche by focusing exclusively on fix and flip loans. What sets them apart is their "no-down-payment" option for qualified borrowers, as they are willing to fund 100% of the purchase and rehab costs, provided the total loan amount does not exceed their ARV cap.

Loan Products Offered: Fix and Flip, Fix to Rent.

Key Strengths and Specializations: Their primary strength is their 100% financing option, which is ideal for investors who are capital-constrained but have a strong, profitable deal. They underwrite based on the property and the investor's ability to execute the project.

Typical Loan Parameters:

- LTV/LTC: Up to 100% of purchase and rehab.

- ARLTV: Up to 70%.

- Loan Amount: Varies, but focused on standard residential flips.

- Note: No income verification or minimum credit score is advertised, but they assess overall financial picture and experience.

Geographic Focus: Operates in 30+ states.

8. Griffin Funding

Griffin Funding is a mortgage company that offers a diverse range of loan products, including non-QM (non-qualified mortgage) loans and hard money options for real estate investors. They cater to a broad audience, from self-employed individuals to seasoned property investors.

Loan Products Offered: DSCR Loans, Bank Statement Loans, Fix and Flip, and VA Loans.

Key Strengths and Specializations: Their expertise in non-QM lending makes them a strong choice for investors who may not qualify for traditional financing due to unique income situations. Their DSCR program is particularly competitive.

Typical Loan Parameters:

- LTV: Up to 80% for investment properties.

- Loan Amount: Up to $5M.

- Credit Score: Varies by program, but generally 660+.

Geographic Focus: Licensed in multiple states across the U.S.

9. Kiavi

Formerly known as LendingHome, Kiavi is a major player in the private lending space, having funded tens of thousands of loans. They leverage a massive amount of data and technology to streamline the lending process, offering speed and certainty to their clients.

Loan Products Offered: Fix and Flip, Bridge, and Rental Loans.

Key Strengths and Specializations: Kiavi's technology platform provides a fast and transparent experience. They are known for their competitive rates and ability to close quickly, making them a favorite among high-volume flippers.

Typical Loan Parameters:

- LTV/LTC: Up to 90% of purchase price.

- ARLTV: Up to 75%.

- Loan Amount: Up to $1.5M.

- Credit Score: Minimum 660.

Geographic Focus: Operates in 32 states plus Washington D.C.

10. RBI Private Lending

RBI Private Lending is a relationship-focused lender that provides financing for a variety of real estate investment projects. They pride themselves on common-sense underwriting and a commitment to helping their clients succeed. They often work with investors who are building their portfolios and need a flexible financial partner.

Loan Products Offered: Fix and Flip, New Construction, Bridge Loans, and Rental Portfolio Loans.

Key Strengths and Specializations: RBI focuses on building long-term relationships with their borrowers. They are known for their responsive customer service and ability to structure loans to meet the specific needs of a project.

Typical Loan Parameters:

- LTV/LTC: Tailored to the deal and borrower experience.

- ARLTV: Up to 75%.

- Loan Amount: $100k to $3M+.

Geographic Focus: Primarily focused on the Mid-Atlantic and Southeastern U.S.

Get Your Instant Loan Quote

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →How to Find Private Hard Money Lenders Who Fund on ARV

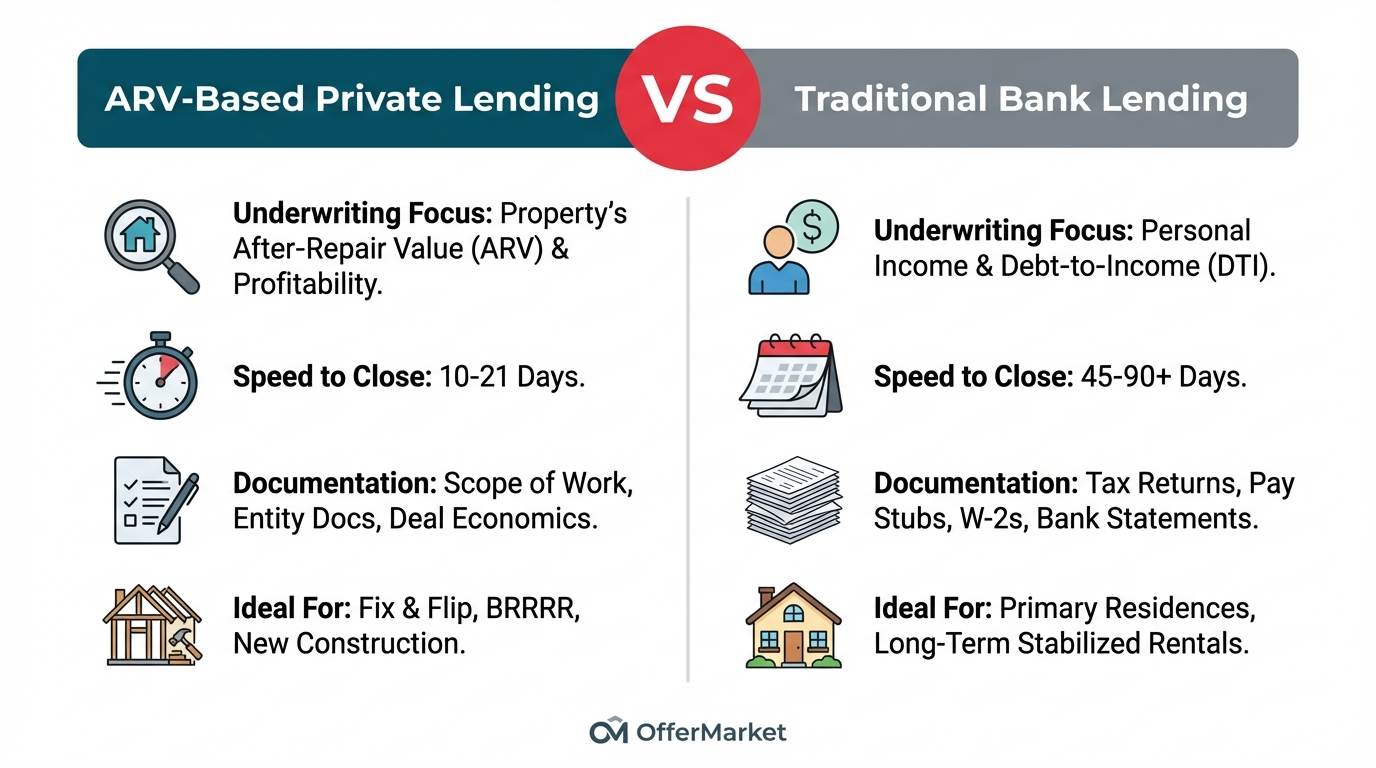

Finding the right lender goes beyond a simple Google search. It requires understanding the fundamental principles of their business model. ARV-based lenders operate on a philosophy that is fundamentally different from traditional banks.

The entire model is built on the concept of asset-based lending. This means the property itself—and the value you intend to create—is the primary collateral for the loan. While your financial history and experience are important, they are secondary to the quality of the deal. The central question an ARV lender asks is not "Can this borrower repay the loan from their income?" but rather, "Is this a profitable project that will result in a valuable asset?"

This focus on the asset's profitability is why speed and flexibility are hallmarks of private lending. Because they aren't bogged down by personal income verification and bureaucratic red tape, private hard money lenders can make decisions and deploy capital much faster. In a competitive real estate market where deals are won and lost in days, if not hours, this speed is a non-negotiable advantage. Investors with a reliable private lending partner can confidently make offers that compete with cash.

How ARV Lenders Underwrite Your Deal: The 4 Core Pillars

To secure funding, you need to present your project in a way that aligns with how private lenders think. Their underwriting process is a systematic evaluation of risk and reward, centered on four core pillars: the ARV cap, your credit profile, your experience, and the deal's economics.

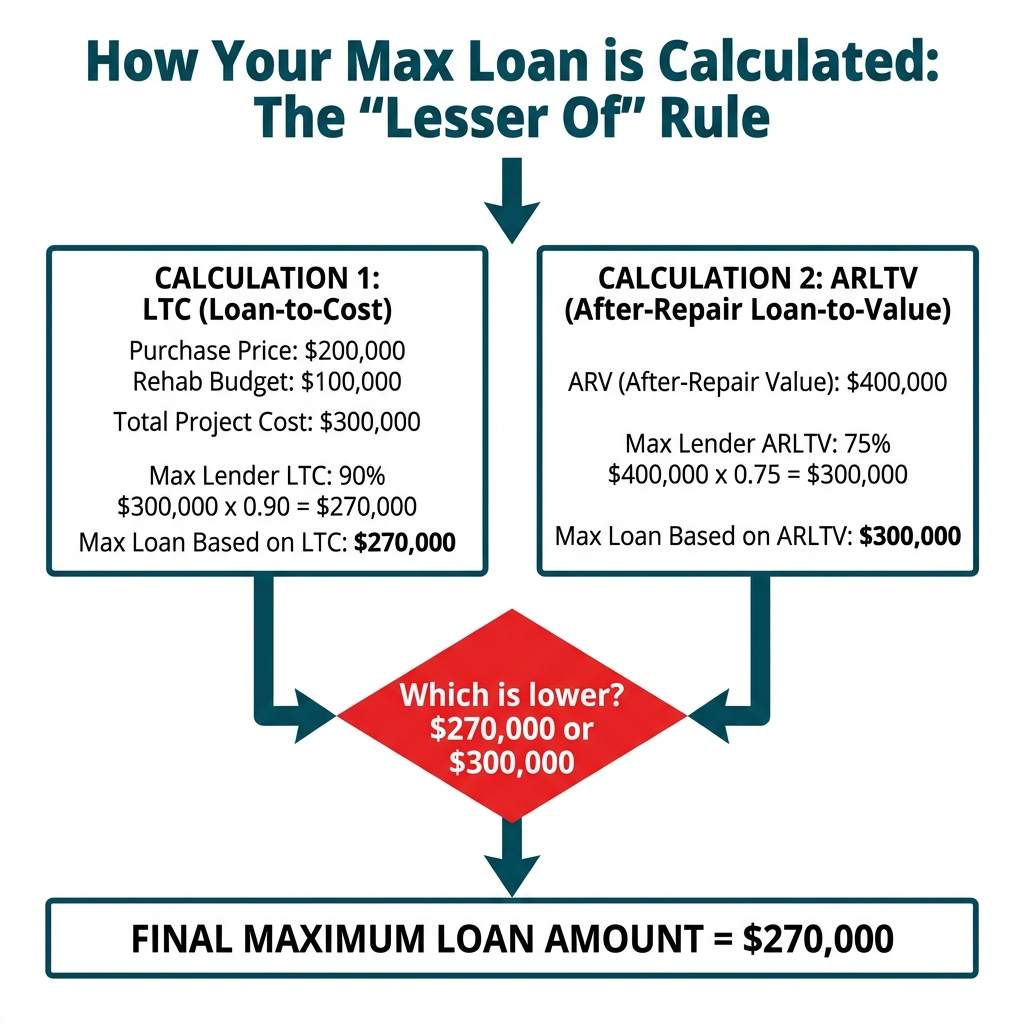

The ARV Cap: Your Maximum Loan Amount Explained

The ARV cap is the single most important metric in hard money lending. It represents the maximum percentage of the property's future value that a lender is willing to finance. This is typically expressed as the After-Repair Loan-to-Value (ARLTV).

To understand this, you must be familiar with two key terms:

Loan-to-Cost (LTC): The loan amount as a percentage of the total project cost (purchase price + renovation budget). For example, if you borrow $280,000 for a project with a total cost of $300,000, your LTC is 93.3%.

After-Repair Loan-to-Value (ARLTV): The loan amount as a percentage of the property's estimated value after all renovations are complete. If your total loan is $280,000 and the ARV is $400,000, your ARLTV is 70%.

Lenders use a "lesser of" rule to determine your final loan amount. They will approve a loan that is the lesser of their maximum LTC or their maximum ARLTV. Most private hard money lenders have a hard cap on ARLTV, typically between 70% to 75%. This cap is a crucial risk management tool for the lender. It ensures there is a sufficient equity cushion in the property to protect their investment in case of a market downturn or a sale that doesn't meet the projected ARV.

Your experience level directly influences the terms you receive. A seasoned investor with a proven track record might qualify for a 75% ARLTV, while a first-time flipper may be capped at 70%.

The Credit Score Misconception

One of the most persistent myths about hard money is that it involves "no credit check." This is false. While private lenders are not as fixated on your FICO score as a conventional bank, they absolutely run a credit report. The purpose, however, is different.

Instead of using your score to determine your fundamental ability to get a loan, they use it to assess your overall financial responsibility. They are looking for major red flags that could jeopardize the project, such as:

- Recent bankruptcies or foreclosures

- Active collections or judgments

- A pattern of late payments on major obligations

Most private hard money lenders have a minimum FICO score requirement, typically around 680. Meeting this minimum is often a prerequisite for consideration. However, a higher score unlocks better terms. Borrowers with scores of 720 or higher are viewed as lower risk and are often rewarded with higher leverage (e.g., lower down payments), better interest rates, and lower origination fees. Your credit score is not the key that opens the door, but it does determine the quality of the room you enter.

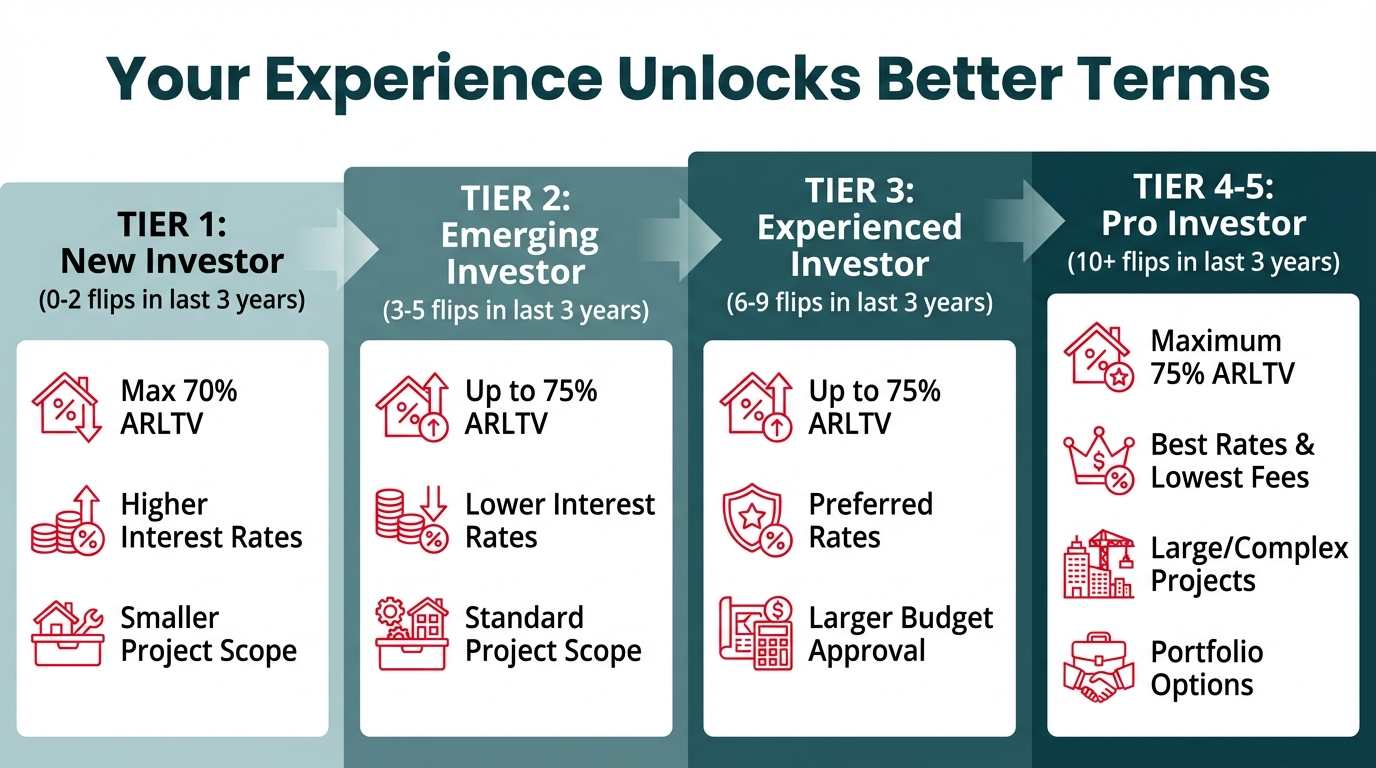

Why Experience Trumps Income

For an ARV lender, your track record as a real estate investor is far more valuable than your W-2. They want to see that you have successfully executed similar projects in the past. A verified portfolio of completed flips is the best possible proof that you can manage a budget, oversee construction, and sell a property for a profit.

To standardize this evaluation, lenders use an experience tier system. While the specifics vary, a typical structure might look like this:

- Tier 1 (New Investor): 0-2 completed projects in the last 3 years.

- Tier 2 (Emerging Investor): 3-5 completed projects in the last 3 years.

- Tier 3 (Experienced Investor): 6-9 completed projects in the last 3 years.

- Tier 4-5 (Pro Investor): 10+ completed projects in the last 3 years.

Your tier dictates the terms of your loan. A Tier 1 investor will likely face a lower ARLTV cap (e.g., 70%), a higher interest rate, and may be limited to smaller, less complex projects. In contrast, a Tier 4 Pro can access the highest leverage (up to 75% ARLTV), the best rates, and can get approved for large-scale new construction or multi-unit projects. Lenders typically use a 3-year lookback period when verifying your project history, so be prepared to provide documentation (like settlement statements) for deals completed within that timeframe.

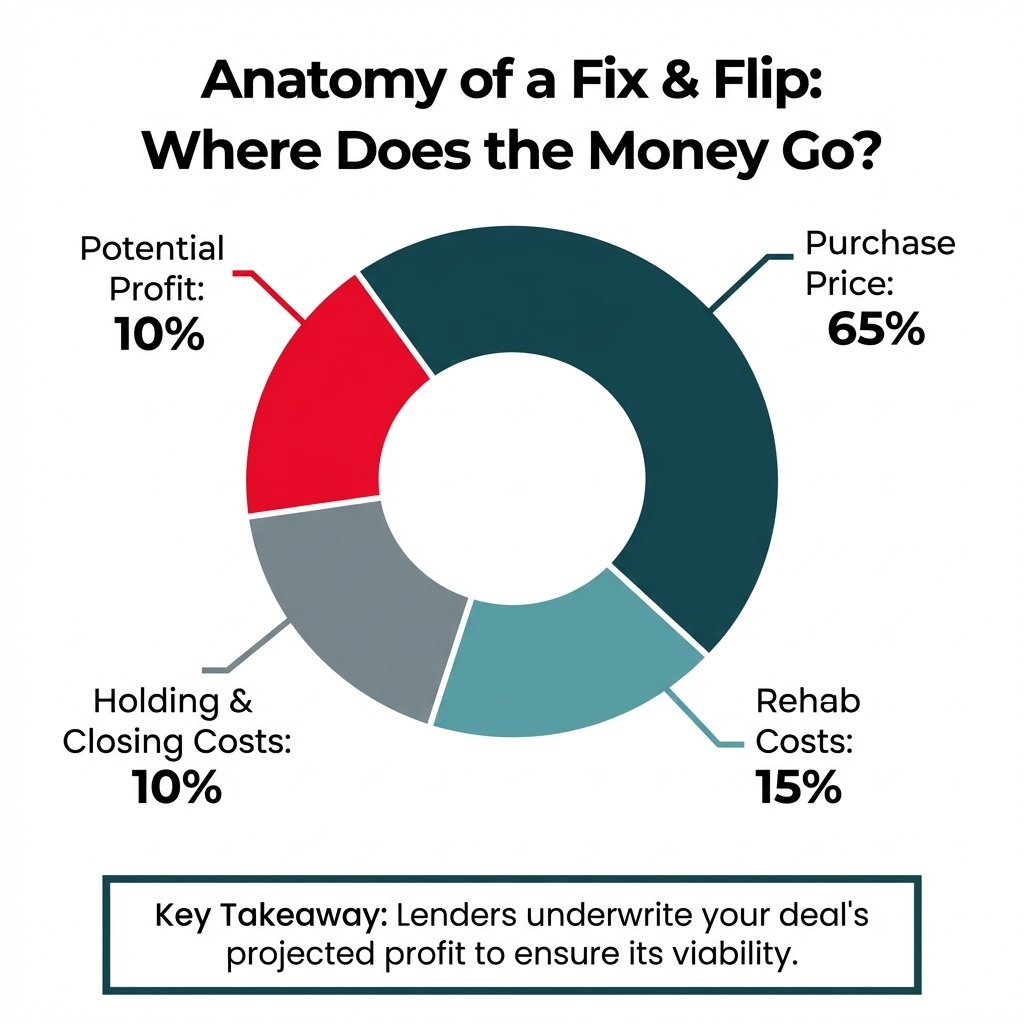

Deal Economics: Proving Your Project's ROI

Ultimately, a private lender is investing in the project's success. The asset's profitability is their true collateral. To get approved, you must prove that your deal is financially sound and has a high probability of success. This requires presenting a clear and compelling case built on solid numbers.

Lenders will scrutinize your projected Return on Investment (ROI), often requiring a minimum threshold of anywhere from 10% to 30%, depending on the market and risk level. Their underwriters will model the entire transaction from acquisition to sale, stress-testing your assumptions. They need to be confident that even if costs run slightly over or the final sale price is slightly under, there is still enough profit in the deal to ensure everyone gets paid.

To do this, you must provide:

- An Accurate ARV: Supported by strong comparable sales (comps).

- A Detailed Scope of Work (SOW): A line-item breakdown of every planned renovation.

- A Realistic Budget: Costs for materials and labor that are in line with current market rates.

A vague or poorly researched budget is a major red flag. It signals to the lender that you may not have a firm grasp on the project, increasing the risk of costly overruns and delays.

Browse Investment Properties

Find off-market and exclusive deals from motivated sellers.

See Listings →Understanding the Mechanics of a Private Hard Money Loan

While the underwriting philosophy is unique, the loan products themselves also have distinct characteristics that investors need to understand. These features are designed specifically for the short-term, value-add nature of real estate investment projects.

What Defines a Hard Money Loan?

Hard money loans are not simply "expensive mortgages." They are a specific financial tool with four defining characteristics:

Short-Term Financing: Unlike a 30-year mortgage, hard money loans typically have terms of 12-24 months. This aligns with the project timeline of a fix and flip or new construction build.

Business Purpose Only: These loans are legally designated for business or commercial purposes. You cannot use a hard money loan to buy a primary residence due to regulations like the Dodd-Frank Act.

Interest-Only Payments: To maximize cash flow during the project, hard money loans are structured with interest-only payments. The full principal balance (the "balloon payment") is due at the end of the term, which is typically paid off by selling the property or refinancing into a long-term loan.

Asset-Based Underwriting: As discussed, the loan is secured by the property's value, not the borrower's personal income.

Common Hard Money Loan Products

Private lenders offer a variety of products to suit different investment strategies. The most common include:

Fix and Flip Loans: The quintessential hard money product, providing funds for both the acquisition and renovation of a property.

Ground-Up Construction Loans: For investors building a new property from the ground up, these loans fund the land purchase and the entire construction budget, disbursed in draws as work is completed.

Short-Term Bridge Loans: These loans "bridge" a gap in financing, such as when an investor needs to close on a new purchase before selling their existing property.

Rental Loans (DSCR): For investors looking to hold a property as a rental (like in the BRRRR method), these loans are used to refinance out of a short-term fix-and-flip loan. They are qualified based on the property's ability to generate enough rent to cover the mortgage payment, a metric known as the Debt Service Coverage Ratio (DSCR).

How Construction Holdbacks and Draws Work

When you get a loan that includes renovation funds, the lender doesn't just hand you a check for the full rehab budget. Instead, those funds are placed in an escrow account, often called a construction holdback. You access this money through a draw process.

The process works like this:

- Complete Work: You pay for the initial phase of work out of pocket (e.g., demolition, framing).

- Request a Draw: You submit a draw request to the lender, detailing the work that has been completed and providing receipts or lien waivers.

- Inspection: The lender sends an inspector to the property to verify that the work claimed on the draw request has been completed to a satisfactory standard.

- Funding: Once the inspection is approved, the lender releases the funds from escrow to reimburse you for the work you've already paid for.

This cycle repeats until the project is finished. While this process has traditionally involved paperwork and delays, modern lenders like OfferMarket have streamlined it significantly. Our app-based draw system allows you to submit requests, upload photos, and track the inspection and funding process directly from your phone, getting you your capital faster so you can keep your project moving.

Get Your Instant Hard Money Loan Quote Today

Understanding the landscape of private hard money lenders and their underwriting process is the first step. The next is to see what terms you can get for your specific project. With the right lending partner, you can secure the capital you need to close deals quickly and scale your real estate investment business.

At OfferMarket, we've combined deep real estate expertise with powerful technology to create a lending experience that is fast, transparent, and tailored to the needs of modern investors.

Get Your Instant Quote: Use our online tool to see your customized loan terms in just a few minutes.

Explore Our Loan Programs: Whether you're doing a quick flip, a major new build, or adding to your rental portfolio, we have a loan product designed for your strategy.

Connect With an Expert: Have questions? Our dedicated loan officers are ready to discuss your project and help you navigate the financing process.

Access Investor Resources: Use our free calculators and guides to model your next deal and make informed decisions.

Get Your 2026 Term Sheet in 2 Minutes

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Get Your Quote →

OfferMarket Loans

Check your rate

60 seconds · no credit pull