*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

Landlord Insurance Greenville SC

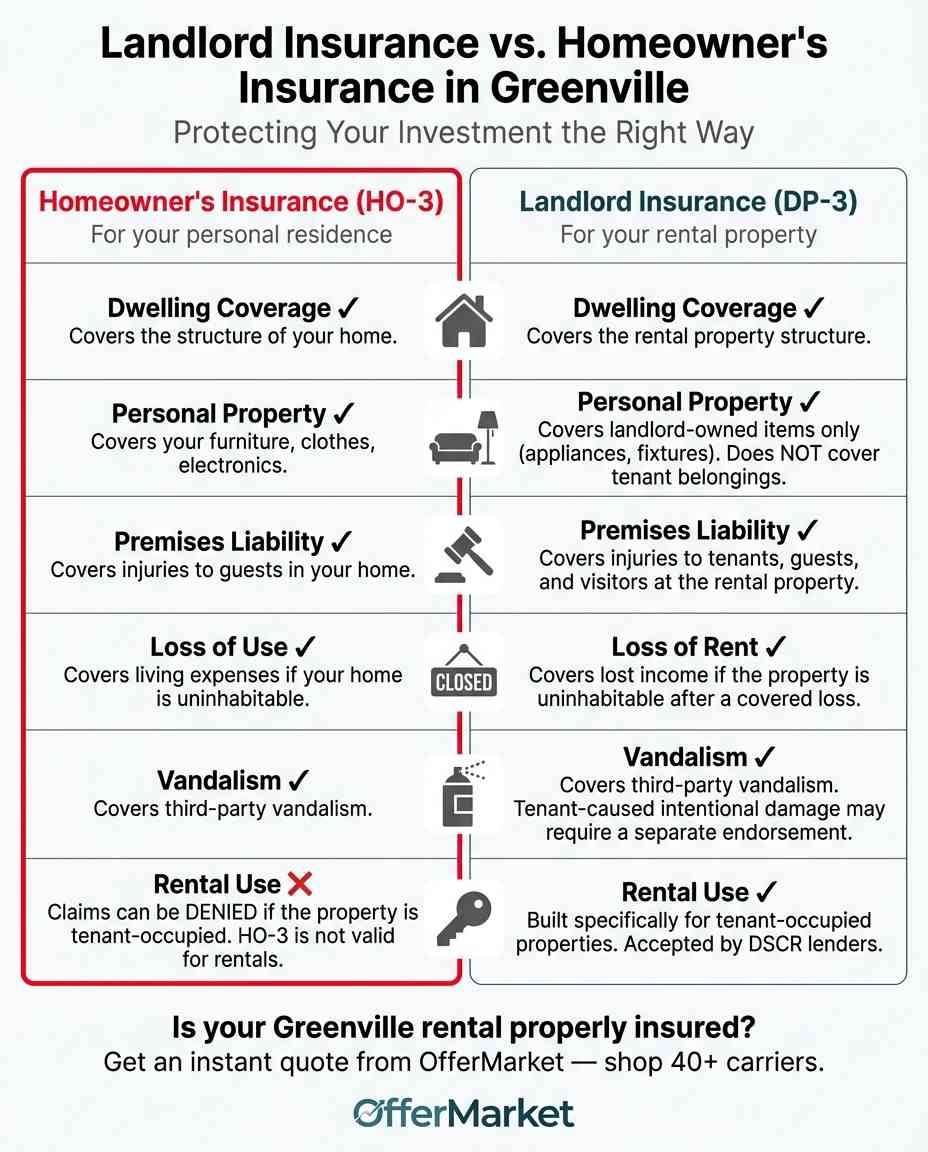

A standard homeowner's insurance policy is designed to cover an owner-occupied residence, protecting your personal property and liability as a resident. Landlord insurance, often called a Dwelling Fire Policy (DP-3), is fundamentally different; it's a business policy designed to protect your financial interest in a property that generates rental income. Using a homeowner's policy for your Greenville rental property creates a critical coverage gap. If a tenant's guest is injured or a fire occurs, your insurer could deny the claim entirely, citing that the property's use as a rental violates the terms of your personal policy. This could leave you personally responsible for hundreds of thousands of dollars in damages and legal fees.

Furthermore, if you have a mortgage on your investment property, your lender will almost certainly require you to carry a specific landlord insurance policy. Lenders for investment property loans view the property as a commercial asset and require a policy that reflects its business use. Attempting to use a homeowner's policy not only puts you at risk of a denied claim but can also lead to force-placed insurance by your lender, which is often more expensive and offers less coverage. The key takeaway is that once a property transitions from your primary residence to a rental, your insurance must also transition from a personal policy to a business policy to ensure your investment is properly protected.

Core Components of a Greenville Landlord Insurance Policy

While policies can be customized, a standard DP-3 policy for a Greenville rental property is built on four essential pillars of coverage. Understanding these components is crucial for ensuring your investment is adequately protected from common risks.

Dwelling Protection

This is the foundational coverage for your policy. It protects the physical structure of your rental property, including the foundation, roof, walls, and built-in fixtures against damage from covered perils.

Standard perils include:

- 🔥 Fire

- 🌩️ Lightning

- 💥 Internal explosion

- 🌬️ Windstorm

- 🌨️ Hail

For example, if a severe thunderstorm, common in the Upstate, causes a tree to fall and damage the roof of your rental home, dwelling protection would cover the cost of repairs, subject to your deductible.

Liability Coverage

Liability coverage is arguably one of the most critical protections for a landlord. It protects you financially if a tenant or their guest is injured on your property and you are found legally responsible. This could be anything from a slip-and-fall on an icy walkway to an injury caused by a faulty appliance you provided. Liability coverage helps pay for medical expenses, legal defense costs, and any settlements or judgments against you, up to your policy limit. Without it, a single lawsuit could jeopardize not only your rental property but your other personal assets as well.

Loss of Rental Income

Also known as "Loss of Rents" or "Fair Rental Value" coverage, this component is a financial safety net. If your rental property becomes uninhabitable due to a covered event (like a fire or major water damage), this coverage reimburses you for the lost rental income while the property is being repaired. For instance, if your Greenville duplex is damaged in a storm and your tenants have to move out for three months during renovations, this coverage would pay you the equivalent of three months' rent, helping you continue to meet your mortgage and other financial obligations.

Landlord's Personal Property

This coverage is not for your tenant's belonging. They need their own renter's insurance for that. Instead, it protects personal property you own and keep at the rental for maintenance or tenant use. This typically includes items like lawnmowers, snow blowers, and appliances such as refrigerators or washing machines that you provide as part of the lease agreement. If these items are damaged or destroyed by a covered peril, this portion of your policy helps cover the cost of replacement.

Unique Risks for Greenville, SC Rental Properties

Owning a rental property in Greenville means facing a set of risks specific to the Upstate region. A comprehensive landlord insurance policy should be tailored to address these local challenges, from weather patterns to legal regulations.

Weather Perils

The Greenville area is prone to severe thunderstorms that can bring high winds, hail, and torrential rain. Hail can cause significant damage to roofing and siding, while strong winds can topple trees onto the structure. Winter brings the risk of ice storms, which can cause pipes to burst and lead to extensive water damage. Your policy's dwelling coverage is your first line of defense against these common weather-related events.

Water Damage and Flooding

Heavy rainfall can lead to water intrusion and damage, especially in older properties with less robust drainage or sealing. It's critical to understand that standard landlord policies do not cover damage from flooding (i.e., rising surface water). If your property is in or near a designated flood zone, you will need a separate flood insurance policy through the National Flood Insurance Program (NFIP) or a private insurer.

Liability Concerns

As Greenville's population grows, so does the rental market. With more tenants comes a higher potential for liability claims. A property in a bustling area near downtown or a university may have more foot traffic and a higher risk of slip-and-fall incidents. Ensuring you have adequate liability limits is crucial to protect your assets from the increased risk that comes with a high-demand rental market.

South Carolina Landlord-Tenant Laws

Navigating state-specific regulations is a key part of being a landlord. The South Carolina Residential Landlord and Tenant Act outlines the rights and responsibilities of both parties, including maintenance obligations. Failure to meet these obligations (e.g., not repairing a faulty handrail) could make you liable for any resulting injuries.

OfferMarket shops 40+ insurance carriers, including carriers licensed and compliant with South Carolina insurance regulations. Get an instant landlord insurance quote and, if you are financing the property, a competitive loan quote in under a minute.

Get an Instant Insurance Quote

Protect your investment property with competitive rates — quote in minutes.

Get Insurance Quote →Factors Influencing Landlord Insurance Costs in Greenville

The premium for your landlord insurance policy in Greenville isn't a one-size-fits-all number. Insurers use a variety of factors to assess the risk associated with your property and calculate your final cost.

Property Characteristics

The location, age, and construction type of your rental are primary factors. A newer, masonry-constructed home in a neighborhood with a low crime rate and good fire protection will generally be cheaper to insure than an older, frame-constructed home in a higher-risk area.

Coverage Limits and Deductible

The more coverage you choose, the higher your premium will be. Increasing your dwelling coverage from $250,000 to $350,000 will raise the cost. Similarly, your deductible: the amount you pay out-of-pocket on a claim has an inverse relationship with your premium. A higher deductible ($5000 vs. $2,500) will lower your annual premium but means you take on more financial risk in the event of a claim.

Safety and Security Features

Insurers offer discounts for features that mitigate risk. Installing and maintaining smoke detectors, fire extinguishers, deadbolt locks, and a central security or fire alarm system can lead to lower premiums.

Claims History

The property's claims history, as well as your personal claims history as a property owner, can impact your rates. A property with multiple past claims may be seen as higher risk, leading to higher costs or even difficulty in securing coverage.

Type of Rental

The way you rent the property matters. A single-family residence (SFR) rented to a long-term tenant is typically the least expensive to insure. A multi-unit property like a duplex or quadplex will cost more due to the increased number of tenants and higher potential liability.

Selecting the Right Coverage for Your Investment

Choosing the right landlord insurance involves more than just finding the lowest price; it requires making strategic decisions to protect the long-term value of your asset.

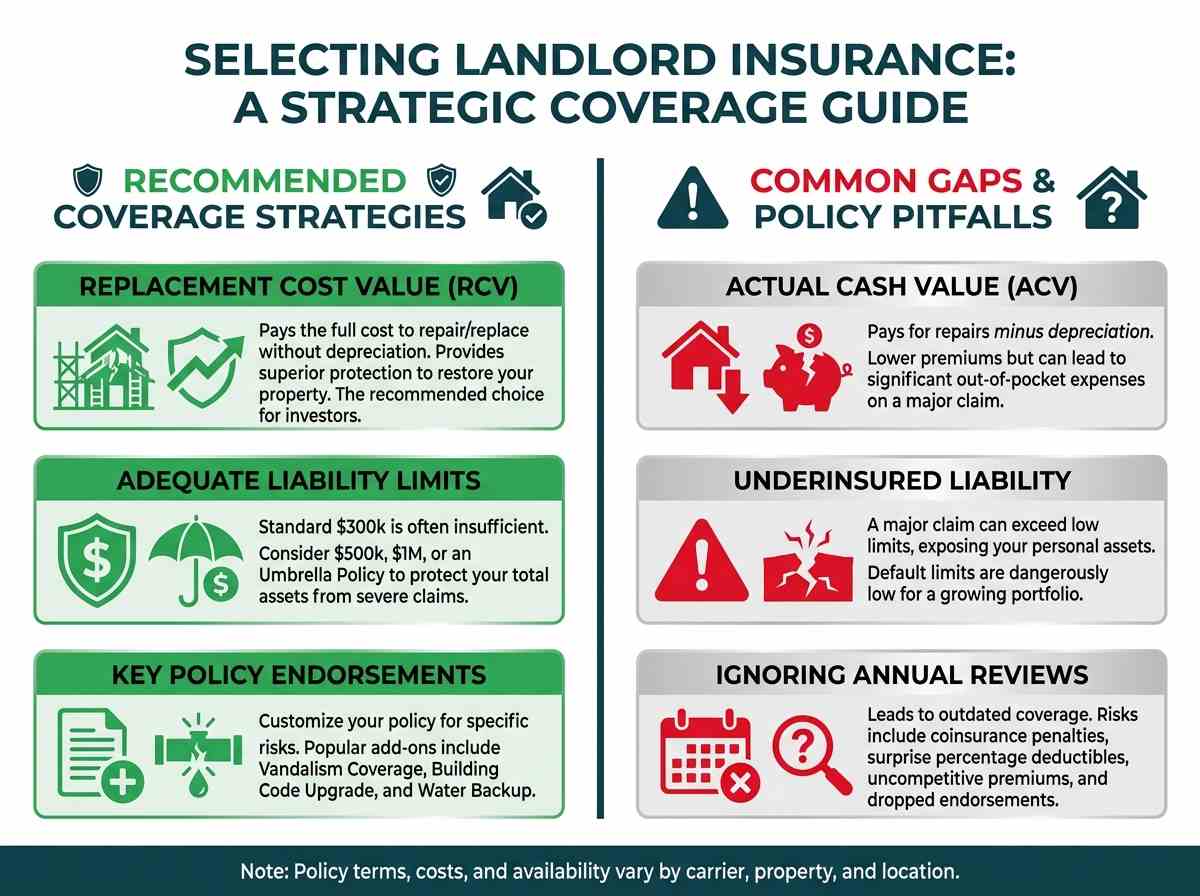

Actual Cash Value (ACV) vs. Replacement Cost Value (RCV)

This is one of the most important decisions you'll make.

Actual Cash Value (ACV): This coverage pays for the cost to repair or replace your damaged property minus depreciation. An older roof, for example, would be significantly depreciated, meaning an ACV policy would only pay a fraction of the cost of a new one. ACV policies have lower premiums but can leave you with significant out-of-pocket expenses after a major claim.

Replacement Cost Value (RCV): This coverage pays the full cost to repair or replace the damaged property with materials of similar kind and quality, without deducting for depreciation. It costs more, but it provides superior protection and ensures you can fully restore your property after a loss. For most real estate investors, RCV is the recommended choice to protect their investment's value.

Determining Adequate Liability Limits

Standard landlord policies often come with a default liability limit of $300,000. However, in today's litigious environment, this may not be enough to protect your personal assets in a severe claim. Consider the total value of your assets (including your primary home, savings, and other investments).

Many investors opt for liability limits of $500,000 or $1,000,000. For even greater protection, an umbrella policy can provide an additional layer of liability coverage (typically in $1 million increments) over and above your primary landlord and auto policies.

Common Policy Endorsements

Endorsements are add-ons that customize your policy to cover specific risks. Popular endorsements for Greenville landlords include:

Vandalism Coverage: Protects against intentional damage to your property, which is often excluded if the property is vacant for more than 30-60 days.

Building Code Upgrade: If your property is damaged and local building codes have changed since it was built, this covers the extra cost to bring the repaired sections up to the current code.

Water Backup: Covers damage caused by a sewer or drain backup, an event not typically covered by a standard policy.

The Importance of an Annual Policy Review

Your insurance needs change every year, even if nothing obvious has changed about the property. Construction costs fluctuate, replacement cost estimates shift, local risk profiles evolve, and carriers adjust their pricing and appetite. A policy that was competitive and well-structured when you bound it 12 months ago may no longer be the best option available today.

Here is what to check every year at renewal:

Dwelling coverage. Does your Coverage A still reflect what it would actually cost to rebuild the property today? If construction costs in your market have increased, your dwelling coverage may be too low, which exposes you to coinsurance penalties on a claim. If costs have come down, you may be overpaying for coverage you do not need.

Deductible structure. Are you still on a flat dollar deductible, or did the carrier switch you to a percentage-based wind/hail deductible at renewal? Percentage-based deductibles can quietly inflate your out-of-pocket costs by thousands of dollars on a single claim compared to a flat $5,000.

Liability limits. If you have added properties to your portfolio since the policy was bound, your total liability exposure has increased. A $300,000 liability limit that felt adequate for one rental may be dangerously low when you own three or five.

Loss of rent. Has your rental income increased? If your rent has gone up but your loss of rent coverage has not, you are underinsured on the income replacement side.

Endorsements. Are water backup, ordinance or law, and any other endorsements you added at binding still on the policy? Carriers occasionally drop endorsements at renewal without clear notification.

Premium competitiveness. Even if your coverage is solid, your premium may no longer be competitive. Carriers reprice their books every year. A carrier that gave you the best rate last year may have increased rates in your market while a different carrier became more aggressive.

The fastest way to run this review is to get a fresh quote through OfferMarket at renewal. In under a minute, you can shop 40+ carriers and compare quotes side by side on an apples-to-apples basis: same dwelling coverage, same deductible, same liability, same endorsements.

That comparison tells you whether your current policy is still the best fit or whether a better option has opened up. OfferMarket's in-house team reviews every quote, so you are not just comparing price. You are comparing the full coverage structure to make sure nothing has slipped through the cracks at renewal.

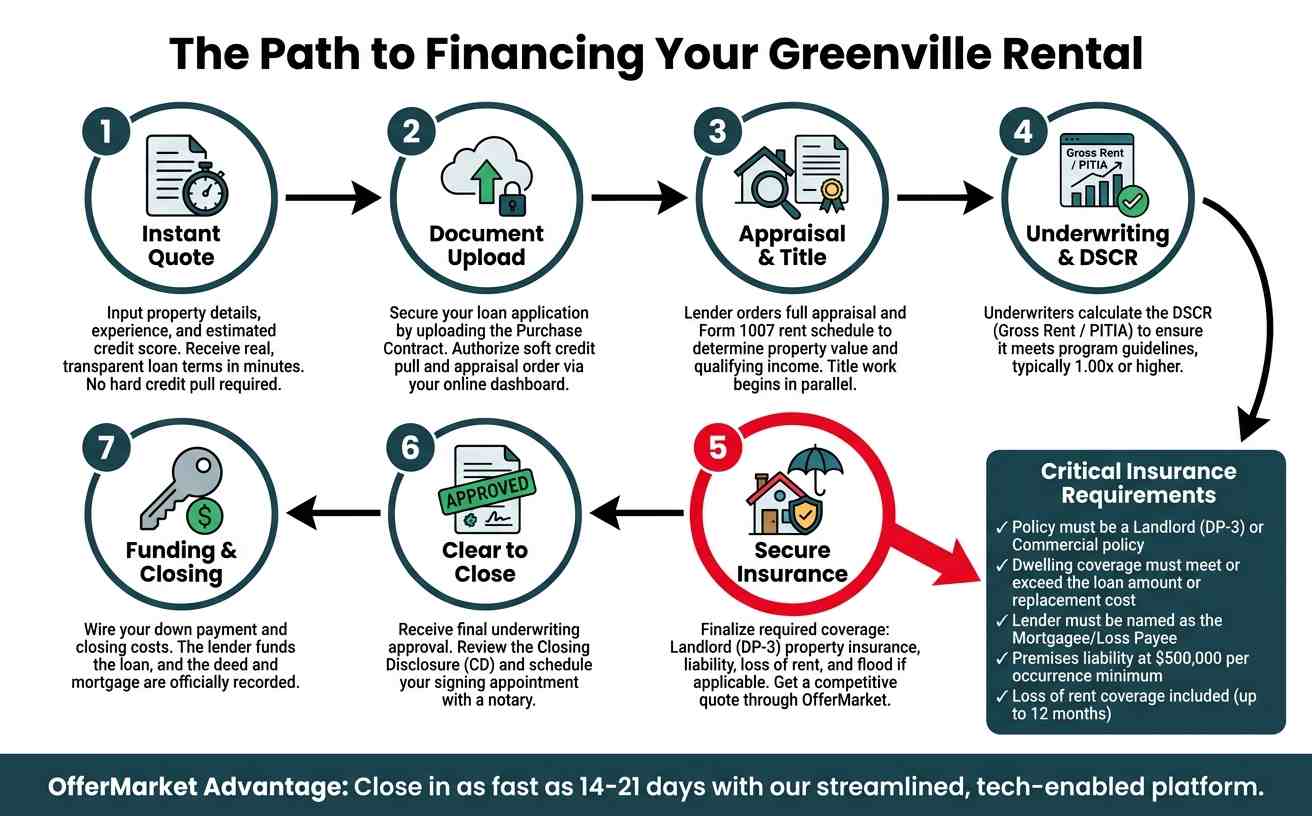

Financing for Greenville Investment Properties

Proper insurance is a non-negotiable component of financing an investment property. Lenders need to know their collateral is protected. Whether you're buying your first rental or expanding your portfolio, understanding the interplay between financing and insurance is key.

Business Purpose Loan Programs

For investors who don't plan to occupy the property, business purpose loans are the standard. These loans, such as DSCR (Debt Service Coverage Ratio) loans, are underwritten based on the property's income potential rather than the borrower's personal income.

A key requirement for closing a DSCR loan is a valid landlord insurance policy with coverage sufficient to cover the full replacement cost of the property.

Occupancy Requirements and Affidavits

Lender requirements are strict regarding occupancy.

1-4 Unit Properties: For these properties, the borrowers must sign a Business Purpose & Occupancy Affidavit at closing, legally certifying that neither they, any family member, nor any member of the borrowing entity will occupy the property at any time while the loan remains outstanding. The borrower must explicitly agree not to claim the property as a primary or secondary residence for the entire duration of the loan.

Multi-Family Properties (5+ Units): Financing for larger properties, like our multi-family loan program, is inherently for business purposes. The underwriting assumes no owner occupancy and always requires a commercial landlord insurance policy.

Short-Term Rentals (STRs): If you plan to operate a short-term rental (like an Airbnb), you must ensure your landlord policy includes a specific endorsement for this type of occupancy, as it carries different liability risks than a long-term rental. Lenders will verify this coverage is in place.

Eligible Property Types

A robust landlord insurance policy can be secured for a wide range of property types common in the Greenville market, including:

- Single-Family Residences (SFR)

- 2-4 Unit Properties

- Condominiums (requires a specific HO-6 policy tailored for landlords)

- Planned Unit Developments (PUDs)

Check your rate

See rates, terms, and max LTV for your investment property in minutes — no credit check required.

Check my rate →OfferMarket's Greenville Specific Coverage Benchmarks

When you get a landlord insurance quote through OfferMarket, the in-house team reviews every quote against these benchmarks:

- 🏠 Dwelling Coverage: Full replacement cost value with zero coinsurance

- 💵 Deductible: Flat $5,000 across all perils

- ⚖️ Premises Liability: $500,000 per occurrence minimum

- 💸 Loss of Rent: Up to 12 months of rental income

- 📋 Ordinance or Law: Included (typically 10% of dwelling coverage)

- 🚰 Water Backup: Included (typically $5,000)

- 🏗️ Loss Settlement: Replacement Cost Value on dwelling, other structures, and personal property

If any of these are missing, below benchmark, or structured in a way that would leave you exposed, the team flags it and works to correct it before the policy is bound. This is the QC layer that separates getting a quote from getting the right coverage.

How to Secure Your Greenville Rental Property

Skip the back-and-forth with insurance agents. Shop the best rates with OfferMarket and walk through a short form that takes under a minute. OfferMarket shops your details across 40+ carriers and returns competitive quotes instantly. Here is what you will need:

- 🏠 Coverage Type — Landlord or Fix and Flip

- 📍 Property Address — the rental you need insured

- 💵 Monthly Rent — current or projected

- 🏢 Entity Name — LLC, trust, or personal name

- 🏗️ Dwelling Coverage — estimated replacement cost to rebuild

- 📅 Effective Date — closing date, today, or rough estimate

- 📋 Claims History — number of claims in the last 5 years

- 📬 Mailing Address — your personal or business address

- 🎂 Date of Birth — standard carrier verification

Once you submit, OfferMarket shops 40+ carriers and returns competitive quotes. The in-house team reviews every quote to flag coverage gaps, catch percentage-based deductibles, and make sure the policy meets your lender's requirements.

Get your instant landlord insurance quote →

Get a Free, No-Obligation Quote for Your Greenville Investment Property

Protecting your Greenville rental property is the most important step you can take as a real estate investor. Don't leave your asset vulnerable to financial loss from lawsuits, storms, or accidents. Take the next step to secure your investment with a policy tailored to the unique needs of the Upstate market.

Get a free, no-obligation landlord insurance quote today and ensure your Greenville rental property is protected.

Shop 40+ Carriers for Your Greenville Rental

Enter your property address, select your coverage type, and get an instant landlord insurance quote in under a minute. OfferMarket's team reviews every quote to make sure your policy meets SC requirements and lender guidelines.

Get Insurance Quote →

OfferMarket Loans

Check your rate

60 seconds · no credit pull