How to Calculate DTI: Step-by-Step Guide to Manage Your Debt-to-Income Ratio

Last updated: April 7, 2025

Understanding your Debt-to-Income (DTI) ratio is crucial for managing your finances effectively. It gives you a clear picture of how much of your income goes towards paying off debts, helping you make informed decisions about budgeting and borrowing.

Calculating your DTI is simpler than you might think. By knowing your DTI, you can assess your financial health, improve your creditworthiness, and better prepare for significant financial commitments like buying a home or car.

In this article, you'll learn the step-by-step process to calculate your DTI, along with tips to improve it, ensuring you stay on top of your financial goals.

Understanding Debt-to-Income Ratio

What Is DTI?

Debt-to-Income (DTI) ratio measures the percentage of your gross monthly income allocated to debt repayment. It compares your total monthly debts, including mortgages, car loans, and credit card payments, to your gross monthly income. For example, if your monthly debts total $1,500 and your gross income is $5,000, your DTI is 30%.

Why Is DTI Important?

DTI assesses your ability to manage monthly debt payments relative to your income. It provides lenders with insight into your financial stability and creditworthiness. High DTI ratios can limit your access to additional credit and may result in higher interest rates. Maintaining a low DTI enhances your chances of loan approval and supports better financial health.

Materials Needed

- Gross Monthly Income Documentation: Statement showing your total earnings before taxes.

- List of Monthly Debt Obligations: Detailed records of all recurring debt payments, including mortgages, car loans, and credit card dues.

- Calculator or Spreadsheet Software: Tool for performing the necessary arithmetic calculations.

- Recent Bank Statements: Documents that provide verification of your income and debt payments.

- Identification Documents: Proof of identity required to access financial information.

Tools Required

- Gross Monthly Income Documentation: Pay stubs, tax returns, or employment letters provide accurate income figures.

- List of Monthly Debt Obligations: Include mortgages, car loans, student loans, credit card payments, and personal loans.

- Calculator or Spreadsheet Software: Utilize a basic calculator or tools like Microsoft Excel or Google Sheets for precise calculations.

- Recent Bank Statements: Verify income and debt payments with the latest bank records.

- Identification Documents: Access financial information with valid ID proofs such as a driver's license or passport.

Steps to Calculate DTI

Follow these steps to accurately calculate your Debt-to-Income (DTI) ratio.

Step 1: Determine Your Gross Monthly Income

Calculate your total income before taxes and deductions. Include all sources such as:

- Salary and wages: Use your latest pay stub.

- Bonuses and commissions: Average monthly amounts if irregular.

- Rental income: Document consistent monthly earnings.

- Investment income: Include dividends and interest.

Sum these amounts to obtain your gross monthly income.

Step 2: Identify Your Monthly Debt Payments

List all recurring debt obligations. Common debts include:

- Mortgage or rent payments: Include principal, interest, taxes, and insurance.

- Auto loans: Record monthly installments.

- Student loans: Note regular payment amounts.

- Credit card payments: Use minimum monthly payments.

- Personal loans: Include fixed monthly payments.

Total these payments to determine your monthly debt commitments.

Step 3: Calculate Your DTI Ratio

DTI = (Monthly Debt ÷ Gross Monthly Income) × 100

For example:

DTI = (2000 ÷ 6000) × 100 = 33.3%

This means 33.3% of your income goes toward debt payments.

Helpful Tips for Calculating DTI

Tips to Improve Your DTI

- Increase your gross monthly income by seeking raises, additional jobs, or passive income sources such as rental properties or investments.

- Reduce monthly debt payments by refinancing high-interest loans, consolidating debts, or negotiating lower interest rates with creditors.

- Eliminate unnecessary expenses by reviewing and cutting discretionary spending, ensuring more income is available for debt repayment.

- Prioritize high-interest debts first to lower overall debt payments and decrease your DTI ratio more effectively.

- Avoid taking on new debt while working to improve your DTI to prevent increasing your total monthly debt obligations.

Common Pitfalls to Avoid

- Omitting all debt obligations such as student loans, medical bills, or personal loans, leading to inaccurate DTI calculations.

- Using net income instead of gross income, which results in an understated DTI ratio and misleading financial assessment.

- Ignoring variable expenses like fluctuating credit card payments, causing inconsistencies in your DTI calculation.

- Failing to update your income and debt information regularly, which can lead to outdated and incorrect DTI ratios.

- Overlooking one-time payments or irregular income sources, thereby skewing the accuracy of your DTI calculation.

Common Issues and Troubleshooting

Inconsistent Income Sources

Variable income from freelance work, commissions, or seasonal jobs complicates DTI calculations. Calculate your average monthly income over the past six months to ensure accuracy. Include all income types, such as bonuses and rental earnings, to reflect your true financial situation.

Missing Debt Information

Ensure all debt obligations are accounted for to obtain an accurate DTI ratio. Include mortgages, auto loans, student loans, credit card payments, and personal loans in your monthly debt list. Overlooked debts, like medical bills or unpaid taxes, can distort your DTI and impact financial assessments.

How to Handle High DTI

Address a high DTI by increasing your gross monthly income or reducing total monthly debt payments. Increase income through salary raises, side jobs, or investment returns. Decrease debt by refinancing loans, consolidating debts, or prioritizing high-interest payments. Maintain a low DTI by avoiding new debts and regularly monitoring your financial status.

Alternative Methods for Calculating DTI

Apply the 50/30/20 Rule

The 50/30/20 rule categorizes income for budgeting purposes and can aid in estimating your DTI. Allocate 50% of your gross income to needs, 30% to wants, and 20% to savings and debt repayment. This method offers a balanced approach to managing finances and provides insights into maintaining a healthy DTI.

Use a Spreadsheet Template

Spreadsheets offer flexibility for customized DTI calculations. Create columns for each income source and debt obligation, then use formulas to sum totals. Templates from Excel or Google Sheets include pre-built formulas to simplify the process. Customization allows for detailed tracking of multiple income streams and debt types.

Consider Average Monthly Income

For irregular income sources, averaging ensures accuracy in DTI calculations. Sum your income over the past twelve months and divide by twelve to determine the average monthly income. This approach accounts for fluctuations, providing a more stable basis for evaluating your debt obligations relative to your income.

Incorporate Future Income Projections

Incorporating future income projections can provide a forward-looking DTI assessment. Estimate expected salary increases or additional income sources and include them in your calculations. This method helps anticipate changes, ensuring your DTI remains manageable as your financial situation evolves.

Adjust for Non-Recurring Expenses

Excluding non-recurring expenses ensures a more accurate DTI. Identify one-time payments like medical bills or annual subscriptions and separate them from regular debt obligations. Focusing on consistent monthly debts provides a clearer picture of your ongoing financial commitments.

Factor in Variable Debt Payments

Variable debts, such as credit card balances, require careful consideration in DTI calculations. Calculate the average monthly payment over several months to account for fluctuations. This method ensures your DTI reflects typical debt obligations, preventing skewed ratios due to temporary changes in payment amounts.

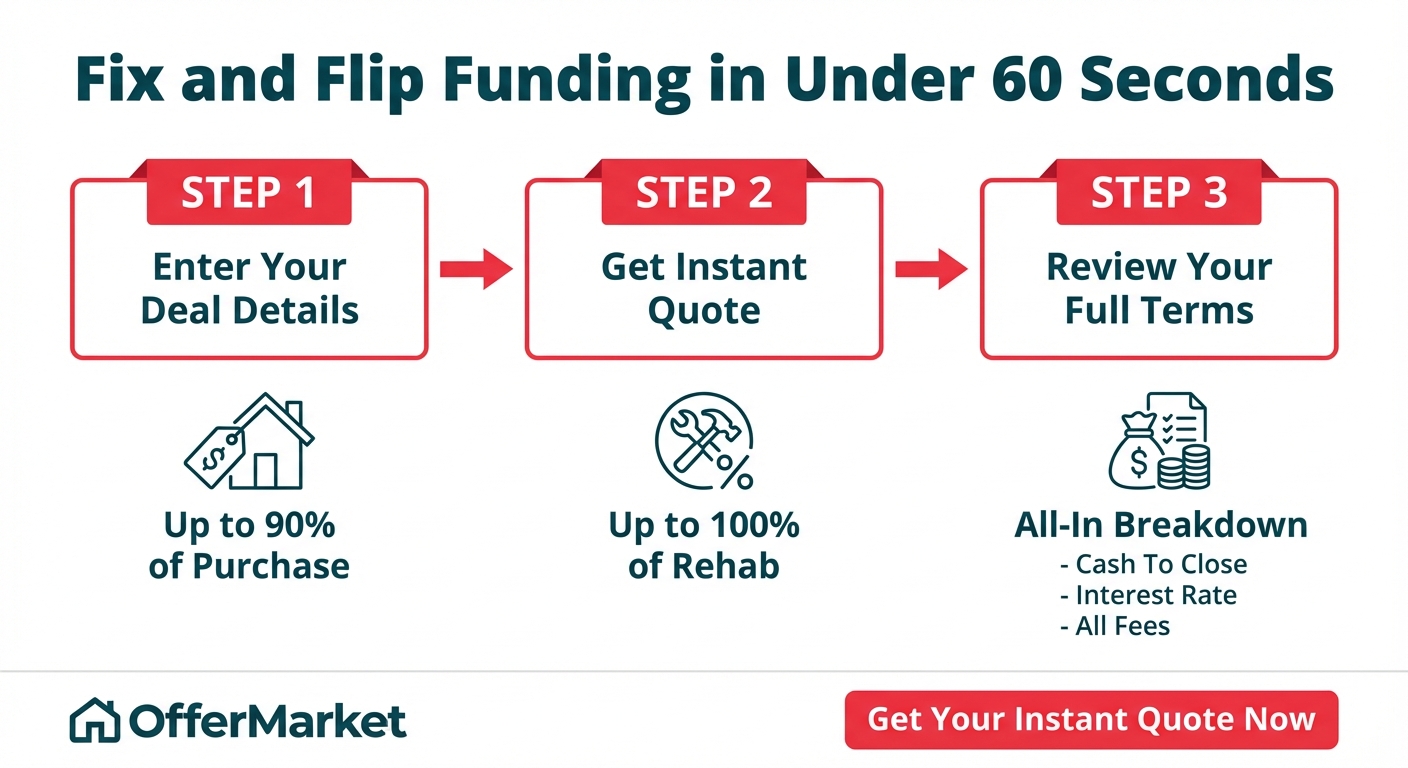

Leverage Online Calculators

Online DTI calculators offer quick and accessible alternatives. OfferMarket provides a user-friendly interfaces for inputting income and debt details. Instant results facilitate swift financial assessments, enabling you to monitor your DTI regularly without manual calculations.

Consult with a Financial Advisor

Professional guidance enhances DTI accuracy and financial planning. Financial advisors analyze your income and debt comprehensively, offering personalized methods for calculating and improving your DTI. Expert insights ensure your calculations consider all relevant factors, supporting better financial decision-making.

Conclusion

Understanding your Debt-to-Income ratio empowers you to take control of your financial health It serves as a valuable tool in managing your debts and making informed borrowing decisions By keeping your DTI low you enhance your creditworthiness and ensure better access to financial opportunities Remember to regularly monitor your DTI and implement strategies to maintain a balanced financial life

Frequently Asked Questions

What is the Debt-to-Income (DTI) ratio?

The Debt-to-Income (DTI) ratio measures the percentage of your gross monthly income that goes toward paying debts. It is calculated by dividing your total monthly debt payments by your gross monthly income and multiplying by 100. For example, if your monthly debts are $1,500 and your gross income is $5,000, your DTI is 30%. This ratio helps assess your ability to manage monthly payments and is crucial for budgeting and borrowing decisions.

Why is the DTI ratio important for financial management?

The DTI ratio is essential for understanding how much of your income is used to repay debts. It provides insight into your financial health and creditworthiness, influencing loan approvals and interest rates. A lower DTI indicates better financial stability, making it easier to secure loans with favorable terms. Monitoring your DTI helps in effective budgeting, reducing financial stress, and ensuring sustainable financial practices.

How do you calculate the DTI ratio?

To calculate the DTI ratio, follow these steps:

- Determine Gross Monthly Income: Sum all income sources, including salary, bonuses, and investments.

- Identify Monthly Debt Payments: List all debt obligations like mortgages, car loans, and credit card payments.

- Calculate DTI: Divide total monthly debt payments by gross monthly income and multiply by 100. For example, $2,000 in debt and $6,000 income results in a DTI of 33.3%.

What documents are needed to calculate my DTI ratio?

To calculate your DTI ratio, gather the following documents:

- Gross Monthly Income: Pay stubs, tax returns, or employment letters.

- Monthly Debt Obligations: Statements for mortgages, auto loans, student loans, and credit cards.

- Bank Statements: For verifying income and expenses.

- Identification Documents: To access financial information securely. Additionally, a calculator or spreadsheet software can help perform the calculations accurately.

What is a good DTI ratio?

A good DTI ratio is typically below 36%, with no more than 28% of income going to mortgage or rent payments. Lenders prefer lower DTI ratios as they indicate better financial health and lower risk of default. A DTI under 30% is generally considered favorable for loan approvals and securing lower interest rates. However, acceptable ratios can vary depending on the lender and type of loan.

How can I improve my DTI ratio?

To improve your DTI ratio:

- Increase Income: Seek raises, take on additional jobs, or explore passive income sources.

- Reduce Debt: Pay down existing debts, refinance loans to lower interest rates, or consolidate debts.

- Control Expenses: Eliminate unnecessary expenses and prioritize essential payments.

- Avoid New Debt: Refrain from taking on additional debt while working to lower your DTI. Implementing these strategies can enhance your financial stability and improve your DTI ratio over time.

What common mistakes should I avoid when calculating DTI?

When calculating DTI, avoid these common mistakes:

- Omitting Debts: Ensure all debt obligations, including medical bills and personal loans, are included.

- Using Net Income: Always use gross income, not net income, for accurate calculations.

- Ignoring Variable Expenses: Account for fluctuating expenses like utilities or variable loan payments.

- Not Updating Information: Regularly update your financial data to maintain accuracy.

- Overlooking One-Time Payments: Include any irregular or one-time payments that affect your debt obligations.

How does DTI affect loan approval and interest rates?

Your DTI ratio significantly impacts loan approval and the interest rates you receive. Lenders use DTI to assess your ability to manage monthly payments. A lower DTI increases the likelihood of loan approval and qualifies you for lower interest rates, as it indicates lower financial risk. Conversely, a high DTI may lead to loan denial or higher interest rates, making borrowing more expensive and challenging.

What strategies can help manage a high DTI?

To manage a high DTI, consider these strategies:

- Increase Income: Pursue higher-paying jobs or additional income streams.

- Reduce Debt: Pay off high-interest debts first or consolidate loans for lower payments.

- Refinance Loans: Seek refinancing options to lower monthly debt payments.

- Budget Effectively: Create and stick to a budget to control expenses and allocate more funds to debt repayment.

- Seek Financial Advice: Consult with a financial advisor for personalized strategies to lower your DTI.

Are there alternative methods for calculating DTI?

Yes, alternative methods for calculating DTI include:

- Financial Software: Use tools that automate DTI calculations for accuracy.

- 50/30/20 Budgeting Rule: Allocate 50% of income to needs, 30% to wants, and 20% to debt repayment.

- Spreadsheet Templates: Customize spreadsheets to track and calculate your DTI.

- Online Calculators: Utilize online DTI calculators for quick and easy computations. These methods can simplify the calculation process and provide different perspectives on managing your finances.

How often should I monitor my DTI ratio?

Regularly monitoring your DTI ratio is crucial for maintaining financial health. It is recommended to review your DTI at least monthly, especially after significant financial changes like a salary increase, new debt, or paying off a loan. Regular monitoring helps you stay on track with your budgeting goals, make informed borrowing decisions, and identify areas where you can improve your financial stability.

Grow your real estate portfolio with OfferMarket

OfferMarket is a real estate investing platform. Month-in-month-out, thousands of real estate professionals leverage our platform to grow and optimize their business. Our mission is to help you build wealth through real estate and we offer the following benefits to our members:

💰 Private lending ☂️ Insurance rate shopping 🏚️ Off market properties 💡 Market insights

OfferMarket Loans

Check your rate

60 seconds · no credit pull