*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

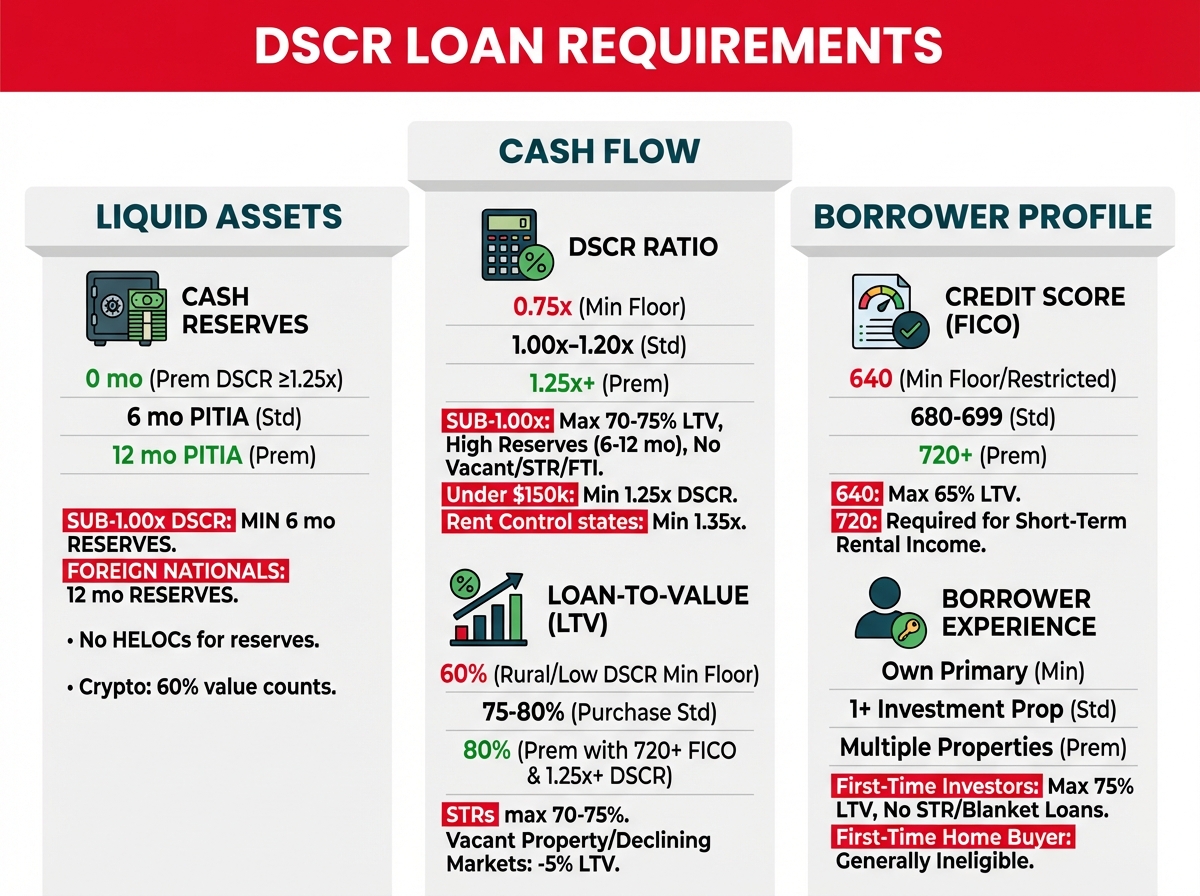

Hard Money Loan Interest Rate 2025

Last updated: 5 minutes ago

You want a financing option that closes quickly and helps you seize opportunities others miss. Hard money loans might be your best bet especially when you need fast capital to fund your rental or fix and flip projects.

As you plan your next real estate investment, it's crucial to understand how changes in interest rates affect your bottom line. By staying ahead of any shifts you can adjust your strategy and ensure your real estate business keeps thriving.

Hard Money Loan Interest Rate Pricing Formula

Shifting Trends In Hard Money Loan Interest Rate 2025

Changing Factors For Hard Money Loan Costs In 2025

Hard money loan rates for 2025 may move in new ways as demand for quick financing grows and supply of funds adjusts. You might notice lenders offering quotes that are a few points higher than past years because short-term conditions can push borrowing costs upward. Some lenders might tighten approval guidelines for borrowers who want money for fix-and-flip or rental projects. This shift may raise your upfront costs along with monthly payments. For instance, if you used to find rates at 10%, you might see rates closer to 12% or more. You may want to check local lending networks and online portals to compare offers for better terms. Real estate data firms have noted that market watchers are tracking changes in building costs. When materials get pricier or sales slow, lenders could feel less confident about short-term real estate projects. Because of that, you may see stricter terms and fees. Despite these changes, some borrowers still choose hard money loans to close deals without jumping through lengthy steps at banks. You could weigh your profit goals against the higher interest charges. If the rise in rates allows you to complete a project more quickly, it might still be worthwhile.

Possible Moves By Lenders To Adjust Rates

Lenders who specialize in hard money loans may adjust rates in 2025 by shifting the loan-to-value (LTV) they’re willing to extend. If property values appear uncertain, you might receive lower LTV offers or see higher points tacked onto the loan. For example, if a lender once gave you 70% LTV at a rate of 10%, you might now see 65% LTV with a rate near 12%. This change may help some lenders keep their risk lower in case a borrower needs an exit plan that takes longer than expected. You can contact lenders who know local market data to get the best sense of costs in your area. Each lender might look at your track record, your personal finances, and the type of real estate you plan to finance. You may spot some lenders who remain open to creative loan structures if you show a history of completing successful projects. You could also see new lenders appear, adding more financing options that might affect rate offerings. Staying flexible with your plans can help you deal with these shifting terms while looking for ways to improve returns.

Impact Of Supply And Demand On Hard Money Loan Pricing

In 2025, you might see how supply and demand can push loan pricing higher or lower. If more investors seek fast funding for flips or rental upgrades, lenders can raise rates or charge bigger fees. On the flip side, if borrowing slows, a few lenders may trim rates to attract new clients. Some might even add special deals to stand out. This pattern could vary from city to city. A region with high real estate activity may have lenders that keep costs higher because they know there’s enough interest from borrowers. Meanwhile, in an area with lower activity, you might see discounts to stir more business. Observing these local factors can help you decide when to apply for a hard money loan. You can contact real estate groups in your region and ask about trends in loan approvals. The more knowledge you gather, the better you can budget for the year ahead. Even if rates seem higher than before, a quick close might offset the added interest if you get a property under contract without delays.

Strategic Steps To Manage Rising Rates

You can plan ahead for 2025 by monitoring rate forecasts through industry news and data sources. If you plan to flip properties, you might want a smaller project to reduce how much you borrow. That can keep interest charges lower, which helps your profit. You could also factor in a potential rate jump when you add up total costs. For instance, setting aside extra funds for loan fees might help you avoid a cash pinch later. If you see a lender offering an option to pay more points upfront for a lower rate, you can weigh that trade-off. A one-point fee might give you a rate that’s a bit less, saving you money if you keep the loan long enough. Real estate groups sometimes hold events where lenders share insights about current conditions. You could attend and ask questions about rate trends. This gives you a direct look at how lenders price loans and what they look for in an applicant. You might hear ways to boost your chances of landing a lower rate, like showing better credit or providing extra collateral. Such actions could add to your savings on your next deal.

Outlook For Hard Money Loan Interest Rate 2025 And Real Estate Projects

Higher rates in 2025 may not always stop real estate investors from using these loans. If a project’s upside appears promising, a short-term loan could still make sense for you, even at a higher cost. You can focus on shorter timelines for your rehab work or look for properties that have strong local demand. That helps you close your sale or refinance plan quickly, which reduces the time you pay interest. Though rates might remain above normal bank financing, the fast funding and fewer approval steps often draw investors who need speed. You might also spot new trends, like more lenders stepping into the market. This could lead to fresh loan programs with different rates or fee structures. Tracking these changes could help you decide how to plan your next move. As 2025 continues, real estate watchers will likely pay close attention to price swings, rental demand, and any shifts in economic conditions. If rate pressures ease, you might find an opening to lock in a better deal. If rate pressures grow, you can adapt by focusing on smaller, safer projects.

Strategies To Secure Competitive Rates

Staying prepared for shifting interest trends in 2025 is a key part of making your hard money loan costs manageable. Rates around 10% to 14% may appear high, yet practical methods can cut your expenses if you compare different lenders and present a reliable track record. Local market activity also impacts typical offers. Some lenders in busy markets may quote higher figures to cover risks, while others in calmer areas may offer reduced percentages. Exact numbers differ from one region to another. Looking at public data from real estate boards can provide insight into average loan charges. Lenders sometimes publish short-term promotions, so reviewing regular updates is useful. Working with a clear plan can position you to land offers that meet your goals.

Comparison Shopping

Comparing lenders helps you spot the best rates. Each lender sets its own rates, ranging from 9% up to 14% or higher, based on location and market demand. Talking to at least 3 different lenders provides a clearer sense of the average you can expect. Some lenders might include hidden fees, so direct inquiries about origination points or underwriting costs help you avoid unexpected charges. Getting written estimates is important since you can save 1% to 2% by identifying the one that offers the most favorable terms. Lenders that specialize in fix-and-flip deals sometimes include a lower rate if your project fits a specific profile. Lenders that cater to rentals might quote a different structure, including short balloon payments or interest-only plans. Industry data from regional real estate associations can be another source of insights on typical rates for your type of project. Gather those details. Compare them side by side. Pick the deal that supports your budget while allowing you to move quickly.

Building Strong Financial Credentials

Showcasing a well-prepared financial record increases your odds of getting favorable rates. Lenders often look at your credit score, which might be 600 or higher, to gauge repayment habits. Scores above 680 can open doors to lower rates or fewer upfront fees. Demonstrating past successes in real estate also adds credibility. This can be proof of previous flip projects that gained profit or rental ventures that have stable income. Having proof of funds and a sensible exit plan is influential. Some lenders ask for 20% to 30% down based on the property value, so ensuring cash reserves is critical. Collecting documents in advance, such as bank statements or contract proposals, shows readiness. Making your case is straightforward once all items are in order. Taking these steps sets a positive tone for negotiations and positions you to request a more competitive quote for your hard money funding.

Key Factors Influencing Hard Money Loan Interest Rate in 2025

| Factor | Description | Potential Impact on Rate | Suggested Strategies |

|---|---|---|---|

| Market Demand | Increased demand for quick funding in active markets | Higher rates due to competition among borrowers | Compare multiple offers; plan smaller projects |

| Lending Environment | Shifts in local economic conditions and building costs | Stricter terms and additional fees | Monitor local trends; prepare detailed project plans |

| Loan-to-Value (LTV) Adjustments | Changes in lender confidence affecting LTV ratios offered | Lower LTV can lead to increased borrowing costs | Strengthen financial documentation; negotiate terms |

| Approval Guidelines | Tighter scrutiny on borrower history and project viability | More fees and higher interest rates for riskier profiles | Maintain a strong credit score; provide clear documentation |

| Fee Structures | Inclusion of extra fees such as origination or processing charges | Increased overall cost of the loan | Request detailed fee breakdowns; ask for written estimates |

Potential Risks And Challenges

Market Shifts

In 2025, you might see shifting costs when seeking a hard money loan. Lenders could raise interest charges if demand is high. On the other hand, if market activity slows, you might see fewer funding sources or tighter terms. This can affect your fix-and-flip or rental strategy. If interest costs climb, you might pay more each month. That can reduce your profits. To stay ready, you might track news from finance sites or talk with peers who watch rates. Some areas might see faster changes than others, so your region can become unpredictable. You might consider short-term plans if you see signs of higher rates.

Credit Worries

Poor credit can lead to higher costs when you seek a hard money loan. If your score dips, some lenders might add extra charges. That can affect your bottom line if interest rate concerns in 2024 remain high. You might find yourself stuck with fewer choices or short approval periods. Some lenders might require large down payments to reduce risk. Shifts in credit rules can also make things more complex. You might see stricter checks on income documents or past property deals. Prepare by checking your credit reports ahead of time. This can help you catch errors and boost your standing.

High Payment Pressure

You could face higher monthly amounts if interest rates push up in 2025. Hard money loans often come with bigger charges than standard loans. If you have a narrow margin on your fix-and-flip, this can strain your finances. Late fees might soar if you miss due dates. This can create a tight spot if property prices fall or if buyers wait longer to commit. You might want to plan for a backup reserve in case you run into delayed payments. Each extra point in your rate can chip away at your returns. Keep a close watch on your budget details.

Pricing Surprises

Some lenders might charge extra fees that catch you off guard in 2025. You might see upfront points, processing charges, or other added costs in the hard money loan process. These expenses can increase your effective rate. If you're not prepared, you might spend more than planned once the loan is active. Interest charges could climb if the demand for quick funding grows. You might also pay a penalty if you pay off the loan too soon. To shield your returns, review each line of your agreement. This can help you spot any problems before you take on new debt.

Conclusion

You stand at the edge of a changing lending environment with plenty of opportunities if you act smart and stay informed. Adapting to emerging patterns lets you minimize potential rate hikes and position yourself to secure the funds you need. Alongside solid financial credentials and careful research, you’ll increase the likelihood of closing lucrative deals quickly while mitigating risks. Staying patient and remaining watchful of shifts in lender guidelines can help you grow your real estate portfolio without getting caught off guard by rising costs.

Frequently Asked Questions

What makes hard money loans appealing for real estate?

Hard money loans offer quick access to capital and flexible approval criteria, making them useful for fast-paced real estate deals like fix-and-flips or rental property acquisitions. They focus more on property value than personal credit. While rates can be higher than traditional loans, the speed and fewer requirements can be worth it if you plan to repay quickly and manage your investment effectively.

How might interest rates change in 2025?

Rates may rise as demand for fast financing grows, and lenders adjust to market conditions. Borrowers could see rates climb from around 10% to 12% or higher, depending on credit history and property type. Staying informed of market trends can help you prepare for potential increases and make better choices for your real estate investments.

What are some strategies to handle rising rates?

Monitoring market forecasts and considering smaller or quicker projects can help reduce borrowing costs. Also, comparing offers from multiple lenders allows you to find competitive terms. Attending real estate events and networking can provide current insights, letting you adjust tactics as rates shift. Sound planning and flexibility remain key to adapting in a changing lending environment.

How can I secure better loan terms with lenders?

Build a solid financial profile by maintaining good credit and a proven track record. Prepare detailed project plans that demonstrate potential success. Compare at least three lenders to avoid hidden fees and to identify the most favorable terms. Showcasing past real estate achievements can help negotiate lower interest rates or higher loan-to-value ratios, leading to more cost-effective financing.

Are there hidden fees I should watch out for?

Yes, some lenders include origination fees, prepayment penalties, or additional closing costs in their agreements. These fees can significantly increase the effective interest rate, impacting profitability. Carefully review your lender’s fee structure and ask for a breakdown of all charges. Doing so helps you better estimate your total loan cost and avoid unpleasant surprises that could erode your investment returns.

What risks do hard money borrowers face in 2025?

Potential risks include stricter approval guidelines, higher interest rates, and unexpected fees, which can increase monthly payments. Poor credit can limit loan options or lead to more expensive terms. Market fluctuations may also affect property values, impacting your project’s profitability. Conduct thorough research, keep your credit in good shape, and review every detail of the loan agreement before proceeding.

Should I still consider hard money if rates rise?

Yes, hard money loans can remain valuable for time-sensitive deals where fast funding is crucial. Quick closings can help you capitalize on promising properties before competitors act. If higher interest rates are offset by strong returns or short holding periods, the overall benefit may still justify the cost. Evaluate each deal’s profitability carefully to ensure you’re making a sound investment.

Grow and optimize your portfolio with OfferMarket

OfferMarket is a real estate investing platform focused on serving rental property investors, small builders, flippers and wholesalers. We focus exclusively on 1-4 unit residential properties in non-rural markets.

We hope you will accept our invitation to join us and over 20,000 registered members.

Membership is entirely free and comes with the following benefits:

🏚️ Off market properties 💰 Private lending ☂️ Landlord insurance rate shopping 💡 Market insights

Our mission is to help you build wealth through real estate and we look forward to contributing to your success.

OfferMarket Loans

Check your rate

60 seconds · no credit pull