*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

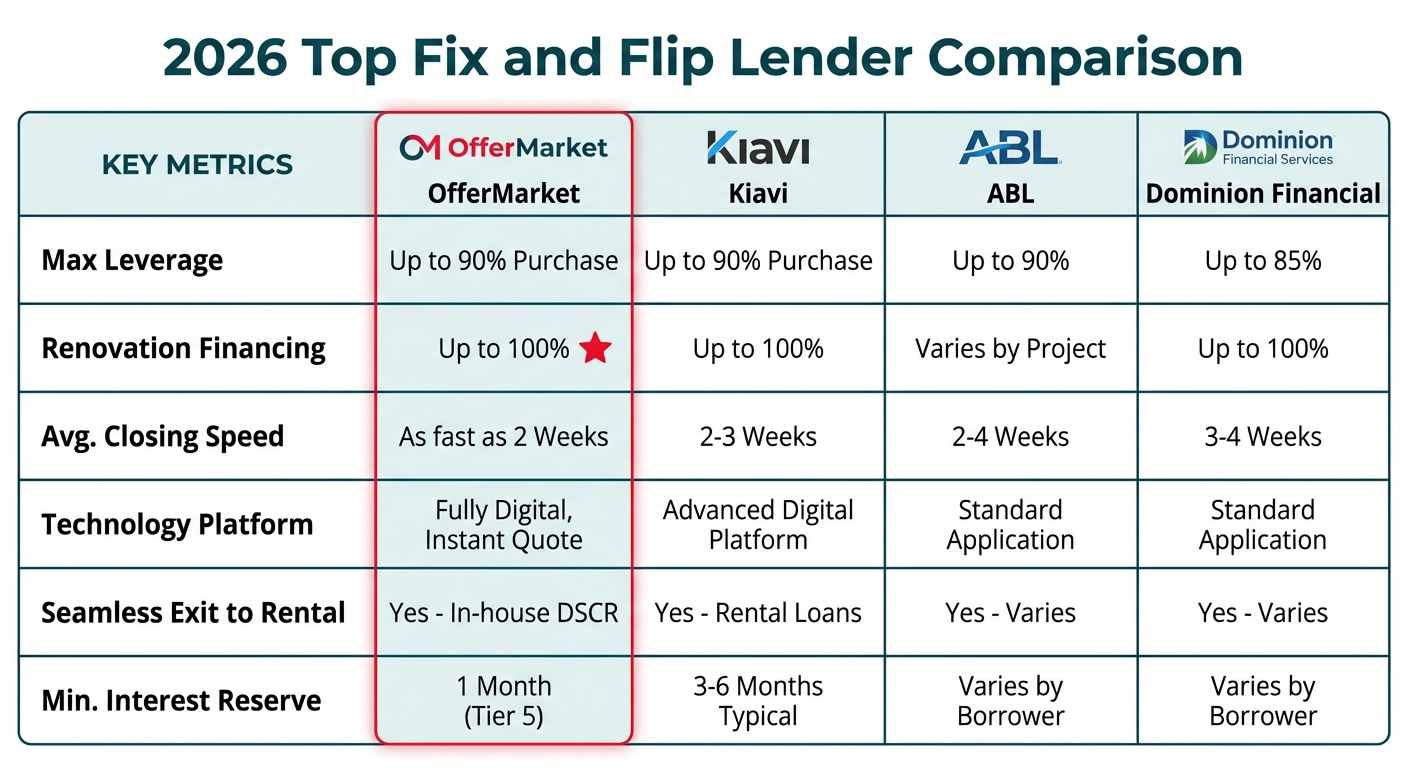

The List of Best Fix and Flip Lenders in 2026

Finding the best fix and flip lender is the single most critical step in ensuring your project's profitability and timeline. The right financial partner provides not just capital, but speed, flexibility, and a clear exit strategy. The wrong one can drown your project in delays, restrictive draw schedules, and unexpected costs that erode your profits. This guide provides a comprehensive framework for finding and vetting elite fix and flip lenders who can accelerate your business growth, not hinder it.

We've analyzed the market to identify the lenders who consistently deliver on the metrics that matter most to serious investors: leverage, speed, and reliability. This list considers loan terms, technological efficiency, customer service, and exit financing options.

The list of Best Fix and Flip Lenders in 2026

When selecting a lender, experienced investors look beyond the headline interest rate. They scrutinize leverage (LTC and renovation financing), the speed and flexibility of the draw process, the efficiency of the underwriting and appraisal process, and the availability of a seamless exit into a long-term rental loan. Here are the top lenders who excel in these critical areas for 2026.

OfferMarket

OfferMarket distinguishes itself as a fintech lender built by investors, for investors. Their platform is engineered for speed and transparency, offering an instant quote for fix and flip loans that provides clear terms upfront. They are a top choice for elite investors due to their high leverage, offering up to 90% of the purchase price and 100% of renovation costs. A key differentiator is their integrated DSCR loan program, which provides a seamless exit for investors looking to hold their rehabbed properties as rentals, bypassing traditional seasoning requirements. Their tech-forward approach minimizes paperwork and accelerates closing times to as little as two weeks.

RBI Private Lending

RBI Private Lending is known for its straightforward and reliable lending process. They focus on providing quick, asset-based loans for non-owner-occupied residential properties. With a reputation for transparency, they often appeal to investors who value a clear fee structure and direct communication. While they may not have the same level of automation as larger fintech platforms, their experienced team provides personalized service, making them a solid choice for investors in their operating regions.

Dominion Financial Services

Dominion Financial Services is a large, established lender with a national presence. They offer competitive leverage and a wide range of loan products for real estate investors, including fix and flip, new construction, and rental loans. Their size allows them to handle high volumes, and they have a well-defined process for underwriting and draws. Investors working with Dominion can expect a professional and structured experience, though it may sometimes feel more corporate and less flexible than smaller, more specialized lenders.

Asset Based Lending

Asset Based Lending (ABL) is a prominent hard money lender operating in many states across the US. They are known for their speed and ability to fund complex deals that traditional banks might reject. ABL offers competitive terms for fix and flip projects, including financing for purchase and renovation. They also provide new construction and rental property loans, giving investors multiple financing options under one roof. Their team is experienced in real estate, which can be a valuable resource for borrowers.

Longhorn III Investments LLC

Based in Texas but with a growing national footprint, Longhorn Investments has built a strong reputation for reliable funding and excellent customer service. They specialize in hard money loans for residential rehab projects. Their process is known for being fast and efficient, and they pride themselves on closing loans quickly to help investors secure deals in competitive markets. They are a relationship-focused lender, which can be beneficial for repeat borrowers.

Capital Fund 1

Operating primarily in the Southwest, Capital Fund 1 is a direct private money lender that has funded thousands of loans. They are known for their ability to close extremely fast, sometimes in as little as 24-48 hours, which is a significant advantage for investors needing to act quickly. They offer a variety of loan products, and their underwriting is asset-based, focusing more on the property's value than the borrower's credit history. This makes them an excellent option for investors with strong deals but less-than-perfect credit.

CV3 Financial Services

CV3 Financial Services is another lender that emphasizes speed and efficiency. They provide short-term financing solutions for real estate investors, including fix and flip loans. Their process is designed to be streamlined, helping investors avoid the lengthy delays associated with traditional financing. They offer competitive leverage and are focused on building long-term relationships with their clients, providing a reliable source of capital for future projects.

Conventus Lending

Conventus Lending is a direct private lender that offers a suite of products for real estate investors. They are known for their flexible underwriting and ability to structure loans to meet the specific needs of a project. They offer both fix and flip and bridge loans, as well as rental financing. Their focus on custom solutions makes them a good partner for investors with unique or complex projects that don't fit into a standard lending box.

Kiavi

Kiavi (formerly LendingHome) is one of the largest and most technologically advanced fix and flip lenders in the nation. Their online platform provides a highly automated and efficient borrowing experience, from application to closing. They offer competitive rates and high leverage, making them accessible to a broad range of investors. Their scale and technology allow them to process a high volume of loans quickly, and they have a wealth of data and resources available to their clients.

The Elite Investor's Vetting Framework for 2026

In today's competitive real estate market, the old way of choosing a lender based solely on the lowest interest rate is a recipe for disaster. Elite investors—those who consistently scale their operations and maximize ROI—understand that the true cost of a loan goes far beyond the rate. They employ a sophisticated vetting framework that prioritizes the factors that actually drive project success: leverage, speed, flexibility, and exit strategy.

The 2026 market is defined by tight inventory, fluctuating material costs, and compressed timelines. This environment demands a financial partner who acts as a strategic asset, not a bureaucratic hurdle. A lender who can't fund quickly means you lose deals to cash buyers. A lender with a rigid draw process can halt construction and inflate carrying costs. A lender without a clear exit path can trap your capital and prevent you from scaling.

This framework is about moving beyond the surface-level numbers and analyzing a lender's operational DNA. It's about finding a partner whose systems are designed to accelerate your velocity of capital.

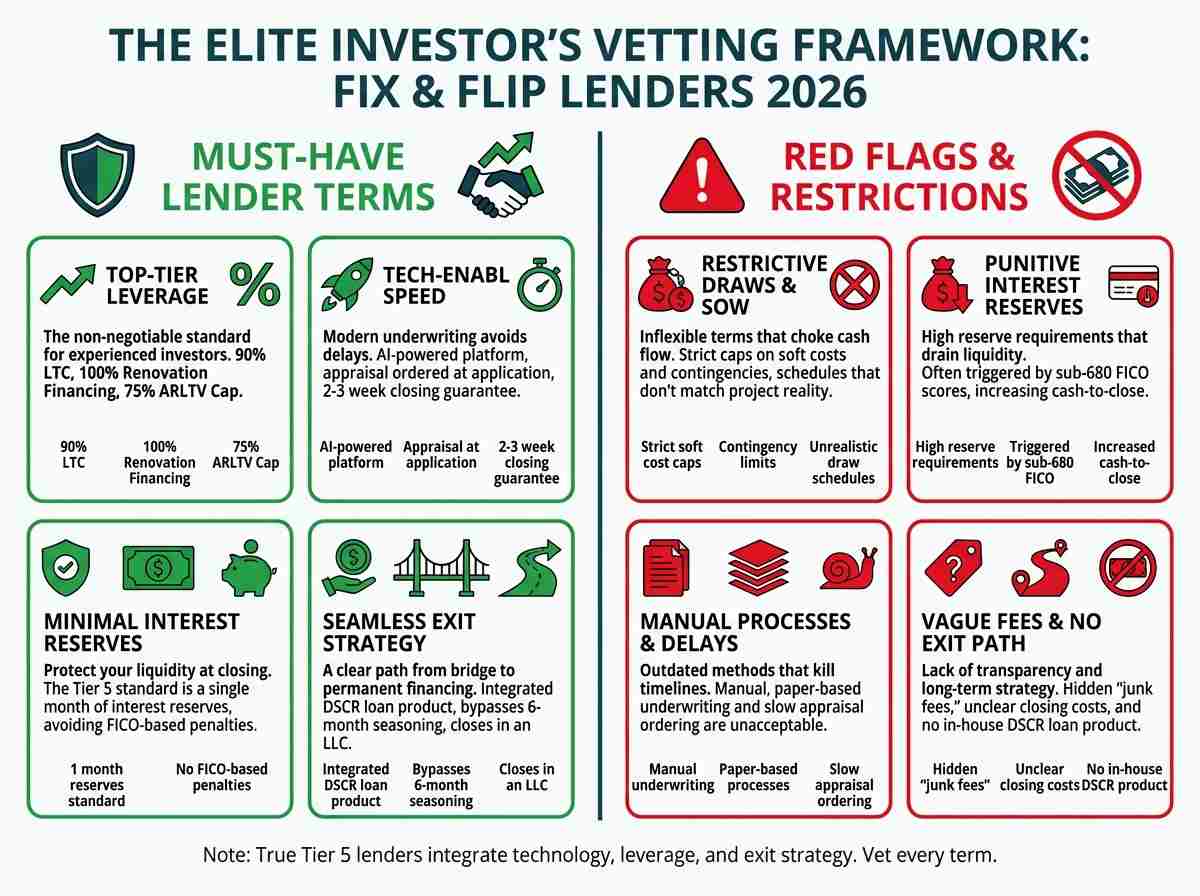

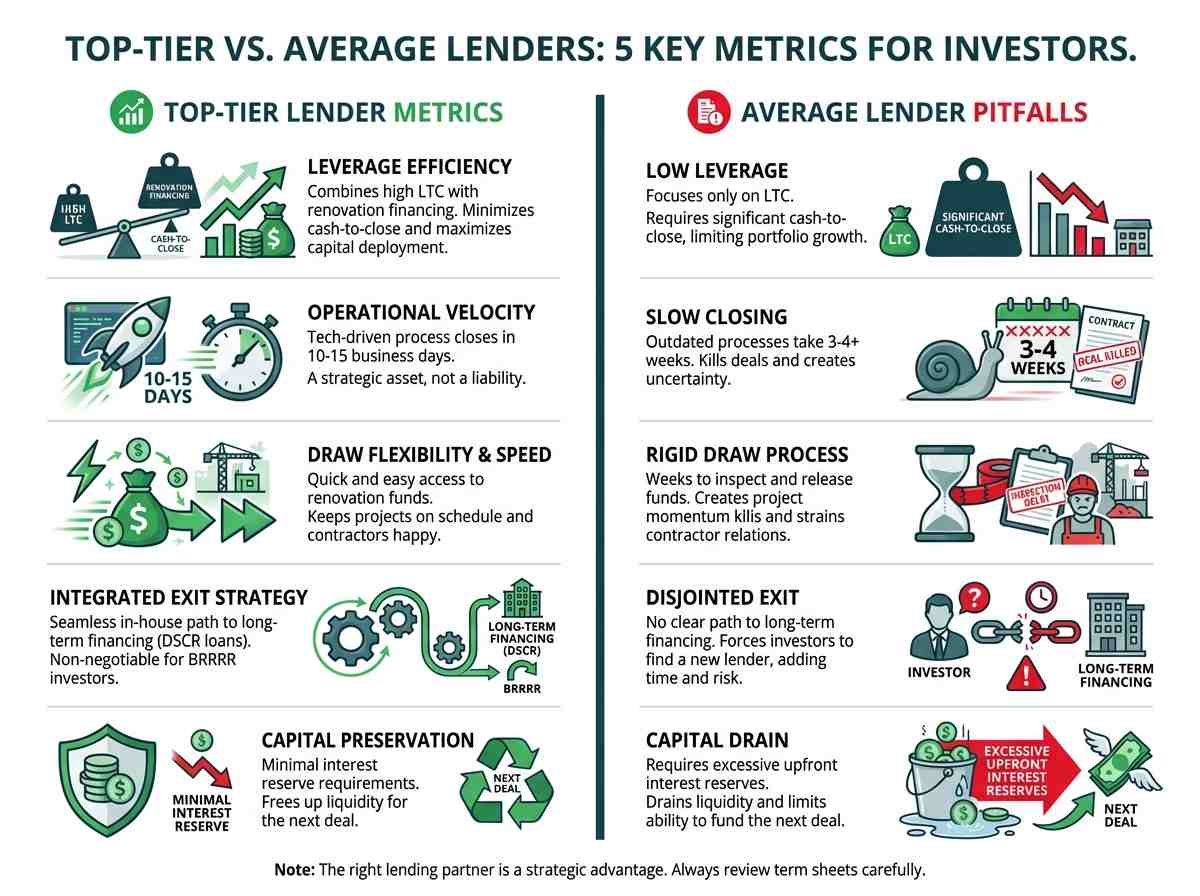

Key Metrics That Separate Top-Tier Lenders

The difference between an average lender and a top-tier lender is stark. Here are the core metrics that elite investors scrutinize:

- Leverage Efficiency: Not just the Loan-to-Cost (LTC), but the combined power of LTC and renovation financing. The goal is to minimize your cash-to-close and maximize capital deployment across multiple projects.

- Operational Velocity: The time from application to closing. In 2026, any lender taking more than 3-4 weeks is a liability. Top-tier lenders leverage technology to close in 10-15 business days.

- Draw Flexibility & Speed: How quickly and easily can you access your renovation funds? A lender who takes weeks to inspect and release a draw can kill your project's momentum and strain relationships with contractors.

- Exit Strategy Integration: Does the lender offer a seamless, in-house path to long-term financing, like a DSCR loan? This is non-negotiable for investors using the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy.

- Capital Preservation: How does the lender handle interest reserves? Requiring excessive reserves upfront is a direct drain on your liquidity, limiting your ability to fund your next deal.

How to Position Yourself as a Tier 5 Investor

Lenders categorize borrowers based on experience to determine risk and, consequently, loan terms. While the exact tiers may vary, the concept is universal. "Tier 5" represents the most experienced, top-level investor who commands the best possible terms.

- Tier 1-2 (Beginner): 0-2 completed flips in the last 24 months.

- Tier 3-4 (Intermediate): 3-9 completed flips in the last 24 months.

- Tier 5 (Elite): 10+ completed flips in the last 24 months.

To position yourself as a Tier 5 investor, you need to meticulously document your track record. This means creating a professional "deal sheet" or portfolio that includes:

- Property Addresses: A clear list of every project.

- HUD-1 Settlement Statements: Provide both the purchase and sale statements for each property. This is non-negotiable proof of a completed "flip."

- Project Summaries: A brief overview of each deal, including purchase price, renovation budget, sale price, and net profit.

- Before & After Photos: Visual proof of the value you create.

Presenting this organized package to a potential lender immediately signals your professionalism and experience, allowing you to bypass beginner-tier terms and start the conversation at the elite level. Even if you're not at 10+ flips yet, a well-documented portfolio for 5-9 flips can often get you access to near-Tier 5 terms from the right lender.

Demand Top-Tier Leverage

Leverage is the engine of real estate investing. For fix and flip investors, maximizing leverage isn't about taking on undue risk; it's about strategic capital allocation. The less of your own cash you have to tie up in a single deal, the more deals you can pursue simultaneously, exponentially increasing your potential returns. Elite investors don't just accept a lender's standard terms; they demand top-tier leverage that reflects their experience and reduces their cash-to-close to the bare minimum.

Defining Tier 5 Experience: 10+ Completed Projects

As established, lenders reserve their best terms for the most experienced investors. The industry benchmark for reaching this top tier—what we call Tier 5—is typically having successfully completed and sold at least ten fix and flip projects within the last 24-36 months.

Why this number? Because after ten deals, an investor has demonstrated a consistent ability to:

- Accurately estimate After Repair Value (ARV).

- Create and manage a realistic renovation budget (Scope of Work).

- Navigate the construction process and manage contractors.

- Successfully market and sell a property.

- Repeat the entire process profitably.

This track record significantly de-risks the loan from the lender's perspective, justifying higher leverage and more favorable terms. If you have this experience, you should never settle for the same loan product offered to a first-time flipper.

The Non-Negotiable Terms: 90% LTC and 100% Renovation Financing

For a Tier 5 investor, the conversation with a lender should start at 90% Loan-to-Cost (LTC) and 100% financing for renovation costs. Let's break down why this combination is so powerful.

- Loan-to-Cost (LTC): This metric is based on the total project cost, which is the purchase price plus the renovation budget. A 90% LTC loan means the lender will cover 90% of this total cost. However, most lenders cap the purchase portion of the loan. A top-tier lender will offer up to 90% of the purchase price specifically.

- Renovation Financing: The best lenders will finance 100% of your budgeted renovation costs. This is crucial for preserving your liquid cash for other needs like carrying costs, unexpected repairs, or the down payment on your next project.

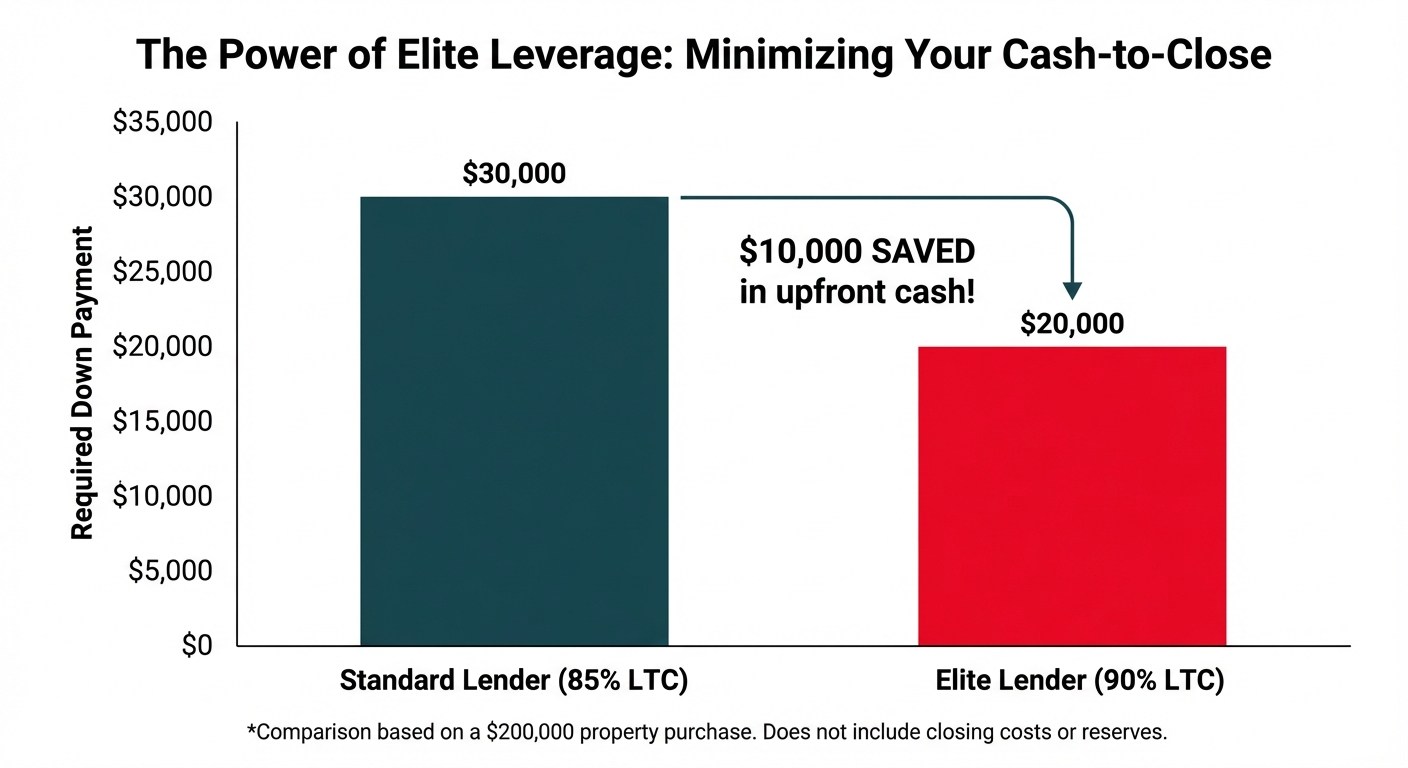

Example: The Power of Elite Leverage

Let's compare standard terms vs. elite terms on a typical project:

- Purchase Price: $200,000

- Renovation Budget: $50,000

- Total Project Cost: $250,000

Scenario 1: Standard Lender (85% of Purchase, 100% of Reno)

- Loan for Purchase: $200,000 * 85% = $170,000

- Loan for Reno: $50,000 * 100% = $50,000

- Total Loan Amount: $220,000

- Your Down Payment: $200,000 - $170,000 = $30,000

- (Plus closing costs and reserves)

Scenario 2: Tier 5 Lender (90% of Purchase, 100% of Reno)

- Loan for Purchase: $200,000 * 90% = $180,000

- Loan for Reno: $50,000 * 100% = $50,000

- Total Loan Amount: $230,000

- Your Down Payment: $200,000 - $180,000 = $20,000

- (Plus closing costs and reserves)

By securing Tier 5 terms, you keep an extra $10,000 in your pocket. For an investor doing 5-10 deals a year, that's $50,000 to $100,000 in additional liquidity to grow your business. This is why demanding 90/100 leverage is non-negotiable.

Understanding the 75% After Repair Loan to Value (ARLTV) Cap

While you demand high LTC, the lender protects themselves with a cap based on the After Repair Value (ARV). The industry standard cap is that the total loan amount cannot exceed 75% of the ARV. This is a critical guardrail that ensures the project remains profitable and the lender is protected in case of a market downturn.

ARLTV Calculation:

- Total Loan Amount / After Repair Value ≤ 75%

Let's continue our example.

- Total Loan Amount (Tier 5): $230,000

- Required ARV: $230,000 / 0.75 = $306,667

This means for the lender to approve your $230,000 loan, the property's appraisal must show a credible ARV of at least $306,667. This is a sanity check on your deal. If your projected ARV is lower than this, it's a red flag that your profit margin may be too thin (or your renovation budget too high), and the deal might not be worth pursuing. An experienced investor uses the lender's 75% ARLTV cap as a final validation of their own underwriting.

Vetting for Exceptions to Standard Renovation Budget Caps

Many lenders impose arbitrary caps on the renovation budget, often limiting it to a certain percentage of the purchase price or a fixed dollar amount (e.g., $100,000). This can be a major problem for projects requiring heavy renovation, like full gut jobs or additions.

An elite lender understands that the renovation budget should be dictated by the project's needs and the potential ARV, not by an arbitrary rule. When vetting a lender, you must ask:

"What are your specific limits on the size of the renovation budget? Can you provide an exception for a well-documented, high-return project if the deal still meets the 75% ARLTV requirement?"

A top-tier lender will have a process for approving larger renovation budgets on a case-by-case basis. They will want to see a highly detailed Scope of Work (SOW) from a licensed contractor and a strong appraisal to support the high ARV, but they won't kill a great deal because of a rigid, one-size-fits-all rule. This flexibility is a hallmark of a true lending partner.

Scrutinize Scope of Work (SOW) & Draw Restrictions

Financing the purchase is only half the battle. The real test of a fix and flip lender lies in how they manage and disburse the renovation funds. A lender with a cumbersome, inflexible draw process can become the biggest bottleneck in your project, single-handedly causing delays, inflating carrying costs, and damaging your relationships with contractors. Elite investors know that the structure of the draw process is just as important as the interest rate on the loan.

The draw process is how you, the investor, get access to the renovation funds held in escrow by the lender. Typically, you complete a portion of the work, pay your contractors out of pocket, and then submit a "draw request" to the lender. The lender then sends an inspector to verify the work is complete and releases the funds to reimburse you. A bad process can choke your project's cash flow and bring it to a grinding halt.

How Lenders Can Choke Project Cash Flow with Restrictive Draws

Inefficient lenders create cash flow problems in several ways:

- Slow Inspections and Disbursements: A lender that takes 7-10 business days (or longer) to schedule an inspector, receive the report, and release funds creates a massive lag. If you have contractors demanding payment on a weekly basis, this delay can force you to float tens of thousands of dollars, straining your liquidity.

- Unrealistic Draw Schedules: Some lenders dictate a rigid, predetermined draw schedule (e.g., 4 draws of 25% each) that doesn't align with the actual phases of construction. A real project might require 30% of the funds for the initial rough-in phase but only 10% for final finishes. A lender who won't adjust the draw amounts to match your SOW forces you to cover the difference.

- Excessive Holdbacks: Lenders will often hold back 10% of each draw until the very end of the project. While some holdback is standard, an overly aggressive policy can further strain your cash flow during the project.

- High Draw and Inspection Fees: Every draw comes with fees. A lender who charges high fees for inspections, processing, and wire transfers is nickel-and-diming your profit margin. These can add up to thousands over the course of a project.

A top-tier lender, like OfferMarket, utilizes technology to streamline this process. They allow for online draw requests, have a network of inspectors that can be dispatched quickly (often within 48 hours), and use digital payment systems to get funds into your account within 24 hours of a passed inspection.

The "10% Rule" for Soft Costs, Demolition, and Contingencies

When you create your renovation budget, it's not just about materials and labor. There are significant "non-construction" costs that are critical to the project. An inexperienced lender may refuse to finance these, forcing you to pay for them entirely out of pocket. You must vet a lender's policy on these specific line items.

A flexible, investor-friendly lender will typically allow up to 10% of the total renovation budget to be allocated to a combination of the following:

- Soft Costs: These include expenses like architectural plans, engineering reports, and permit fees. These are often required before any physical work can even begin.

- Demolition: The cost to gut a property and haul away debris. This is a real, necessary construction expense.

- Contingency: This is a crucial buffer for unexpected issues, like discovering mold, needing to replace a subfloor, or other surprises. A 5-10% contingency line item is a sign of a well-planned project.

A lender who refuses to finance a reasonable contingency is not operating in the real world of construction and should be avoided.

Understanding the 25% Combined Cap on Non-Construction Costs

Beyond the 10% rule for the items above, there's a broader category of costs. You need to clarify the lender's total cap on all non-construction and "soft" line items combined. A competitive lender will generally cap these at around 25% of the total renovation budget.

This 25% cap would include the initial 10% (permits, demo, contingency) plus other items like:

- Project management fees

- Landscaping allowances

- Specific appliance packages

- Other non-labor, non-material costs

When you submit your SOW, be sure to categorize your expenses clearly. If your soft costs exceed the lender's cap, you need to know upfront so you can decide whether to cover the excess yourself or find a more flexible lending partner.

Aligning the Lender’s Draw Process with Your Project Timeline

The ultimate goal is to ensure the lender's process serves your project, not the other way around. Before you sign any loan documents, you must have a frank discussion about the draw process and get clear answers.

Actionable Vetting Steps:

- Request a Sample Draw Form: Ask to see their exact draw request form and a sample inspection report. Is it a one-page streamlined request, or a mountain of bureaucratic paperwork?

- Confirm the Timeline in Writing: Get a written confirmation of their service level agreement (SLA) for the draw process. Ask: "From the moment I submit a draw request, what is your guaranteed maximum turnaround time to have funds in my bank account?" A good answer is 3-5 business days. Anything over a week is a red flag.

- Discuss Custom Draw Schedules: Present a hypothetical project SOW. Explain that you'll need a large first draw for deposits and rough-ins, followed by smaller draws. Gauge their reaction. If they immediately push back and insist on a rigid, equal-payment schedule, they are not a flexible partner.

- Clarify All Fees: Ask for a complete fee schedule for the draw process. This includes inspection fees, draw processing fees, wire fees, and any other potential charges.

By scrutinizing the draw process with the same rigor you apply to the interest rate, you can avoid the cash flow traps that derail even the most promising fix and flip projects.

Evaluate 2026 Appraisal and Tech Speed

In the fast-paced 2026 real estate market, speed is not a luxury; it's a competitive necessity. The ability to close a loan in two to three weeks versus six to eight weeks is often the difference between winning a deal and losing it to another buyer. The single biggest variable and frequent bottleneck in the entire lending process is the property appraisal. An elite investor must partner with a lender who has mastered the appraisal process through superior technology and operational efficiency.

The Role of AI and Automation in Modern Underwriting

Legacy lenders still rely on manual, paper-based underwriting. An underwriter receives a file, physically reviews documents one by one, and a single file can sit on someone's desk for days waiting for review. This is an outdated and inefficient model.

Modern fintech lenders like OfferMarket leverage technology to dramatically accelerate this process:

- Automated Document Recognition: AI-powered systems can instantly scan and verify documents like bank statements, entity documents, and purchase contracts, flagging any inconsistencies for human review.

- Digital Data Verification: Instead of relying on paper copies, these platforms can connect directly (with borrower permission) to bank accounts and other data sources to verify assets and information in real-time.

- Algorithmic Risk Assessment: Sophisticated algorithms can perform an initial risk assessment based on thousands of data points, allowing human underwriters to focus their time on the more complex aspects of the loan file.

This automation doesn't replace the need for experienced underwriters, but it equips them with tools to process loans exponentially faster and with greater accuracy. A lender who still asks you to fax documents is a lender who cannot compete on speed.

Why the Appraisal is the Biggest Hurdle to Fast Funding

Even with the fastest underwriting, the entire process can grind to a halt waiting for the appraisal. Here's why it's such a common problem:

- Appraiser Shortages: In many markets, there is a high demand for qualified real estate appraisers, leading to backlogs. It can take a week or more just to get an appraiser to accept the assignment.

- Scheduling Delays: The appraiser then has to coordinate access to the property with the seller, agent, or tenant, which can add more delays.

- Report Writing Time: After the physical inspection, the appraiser needs time to research comparable sales (comps), analyze the data, and write the comprehensive report, which can take several days.

- Review and Revisions: Once the lender receives the report, their internal review team or the underwriter may have questions or require revisions, sending it back to the appraiser and adding more time to the clock.

This entire sequence can easily take three weeks or more with an inefficient lender, completely destroying your closing timeline.

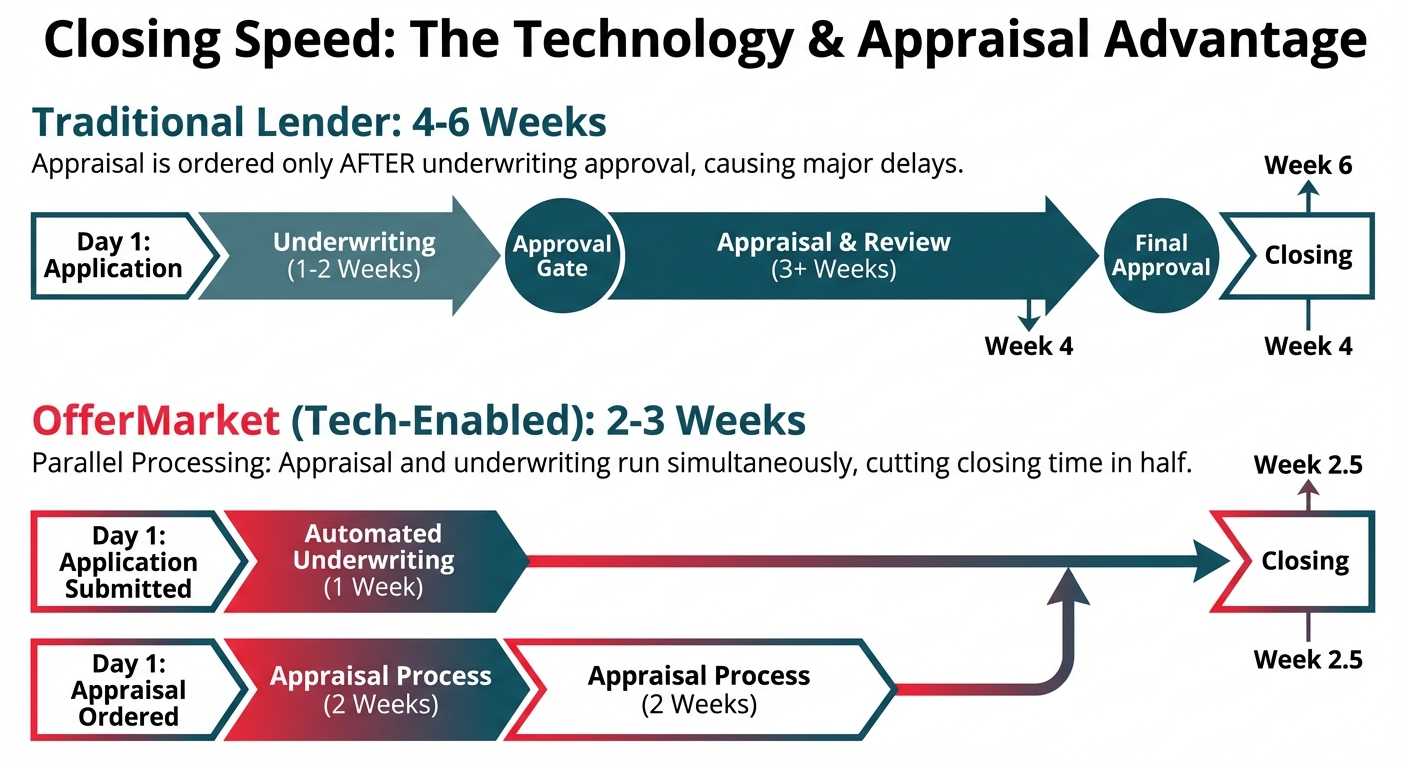

Mandating Appraisal Orders at the Time of Application

This is the single most important strategy for compressing the closing timeline. Most lenders will not order the appraisal until after the loan has been fully underwritten and received preliminary approval. This is a sequential process that builds in weeks of unnecessary delay.

An elite, tech-forward lender will allow—and encourage—you to order the appraisal the very same day you submit your loan application. By paying the appraisal fee upfront, you are signaling that you are a serious borrower committed to the deal.

This "parallel processing" approach is a game-changer:

- Traditional (Slow) Process: Application -> Document Submission -> Underwriting (1-2 weeks) -> Approval -> Appraisal Order (3+ weeks) -> Final Approval -> Closing. Total Time: 4-6 weeks.

- Elite (Fast) Process: Application + Appraisal Order -> Document Submission + Underwriting (1 week) -> Appraisal Report Received (2 weeks) -> Final Approval -> Closing. Total Time: 2-3 weeks.

By running the two longest parts of the process—underwriting and appraisal—simultaneously, you can cut your closing time in half. When vetting a lender, your question must be direct:

"Does your platform allow me to pay for and order the appraisal immediately upon submitting my application, or do I have to wait for underwriting approval?"

If the answer is that you have to wait, you are dealing with an inefficient lender who will not be able to provide the speed you need to compete.

Guaranteeing a 2 to 3-Week Closing Timeline Through Technology

A lender's confidence in their closing timeline is a direct reflection of their investment in technology and process optimization. A top-tier lender should be able to commit to a 10-15 business day closing window, provided you are a responsive borrower.

This guarantee is only possible through a combination of:

- An efficient, automated underwriting platform.

- The ability to order the appraisal on Day 1.

- A robust, pre-vetted national panel of appraisers (an AMC or Appraisal Management Company) that they have leverage with.

- An integrated digital closing process that allows for e-signatures and streamlined coordination with the title company.

When a lender can confidently promise a fast closing, it's not a sales pitch; it's evidence of a superior operational infrastructure that will be a strategic asset to your real estate business.

Protect Liquidity from Interest Reserve (IR) Penalties

An often-overlooked detail that can have a significant impact on your required cash-to-close is the lender's policy on interest reserves. While it may seem like a minor accounting detail, an excessive interest reserve requirement is a direct drain on your liquidity, tying up capital that could be used for your current project's carrying costs or the down payment on your next deal. Elite investors understand this and seek out lenders with the most favorable and logical interest reserve policies.

Defining Interest Reserves and Their Impact on Cash-to-Close

An interest reserve (IR) is a portion of the loan funds that the lender sets aside at closing to cover the monthly interest payments for a predetermined number of months. Instead of you paying the interest each month out of your bank account, the lender pays themselves from this reserve account.

From the lender's perspective, it's a risk mitigation tool. It guarantees they will receive their interest payments for the initial, riskiest phase of the project. However, from your perspective, it's your loan money that you can't access.

The crucial point is this: the interest reserve is added to your cash-to-close.

Example:

- Loan Amount: $250,000

- Interest Rate: 10% per annum

- Monthly Interest Payment: ($250,000 * 10%) / 12 = $2,083

- Lender's IR Requirement: 6 months

- Total Interest Reserve: $2,083 * 6 = $12,500

This $12,500 is added to your down payment and other closing costs. It's cash you must bring to the closing table, effectively increasing your upfront investment and reducing your liquidity.

The Tier 5 Standard: A Single Month of Interest Reserves

For an experienced Tier 5 investor with a strong track record and good credit, a large interest reserve is punitive and unnecessary. You have proven your ability to manage projects and cash flow. Therefore, the elite standard you should seek is a single month of interest reserves.

Some of the most competitive lenders may even waive the reserve requirement entirely for their top-tier borrowers, allowing you to make the monthly interest payments directly. This is the ideal scenario, as it maximizes your day-one liquidity.

When vetting a lender, don't just ask if they require an interest reserve. Ask:

"For a Tier 5 borrower with a 740+ FICO score, what is your standard interest reserve requirement? Is it possible to have it waived entirely?"

A lender who insists on a 6-month reserve for a top-tier borrower, regardless of their credentials, has a rigid, one-size-fits-all risk model and is not a true partner for a scaling investor.

How FICO Scores Trigger Punitive Reserve Requirements

Your FICO score is the primary lever that lenders use to adjust interest reserve requirements, especially for borrowers who are not in the top experience tier. While hard money loans are "asset-based," your personal credit is still a key indicator of your financial responsibility and ability to manage debt.

Lenders create internal risk tiers based on FICO scores, and the interest reserve requirements scale up as the score goes down.

Typical FICO-Based IR Structure:

- 740+ FICO: 1 month (or potentially waived)

- 700-739 FICO: 3 months

- 680-699 FICO: 4-6 months

- < 680 FICO: 6+ months, or may not qualify

A lower credit score signals higher risk to the lender, so they protect themselves by holding more of your money upfront to cover payments. This is why maintaining a strong personal credit profile is critical, even when you are borrowing through an LLC.

Calculating the Liquidity Impact of a Sub-680 Credit Score

The difference in required cash-to-close between a borrower with excellent credit and one with fair credit is substantial. Let's revisit our example with the $2,083 monthly interest payment.

Investor A (760 FICO):

- IR Requirement: 1 month

- Cash-to-Close for IR: $2,083

Investor B (670 FICO):

- IR Requirement: 6 months

- Cash-to-Close for IR: $12,500

Investor B must bring an additional $10,417 to closing simply because of their lower credit score. This is a massive penalty. That $10,417 is "dead money" for the first six months of the project—it can't be used for repairs, marketing, or another down payment.

Before applying for a loan, it's crucial to know your credit score and to ask potential lenders for their specific, FICO-based interest reserve matrix. This transparency allows you to accurately forecast your cash-to-close and identify lenders whose policies will unnecessarily penalize you. The best lenders are transparent about these policies and work with you to find the best possible terms for your specific financial picture. You can check your credit score for free from various sources, such as Credit Karma or directly from credit card providers.

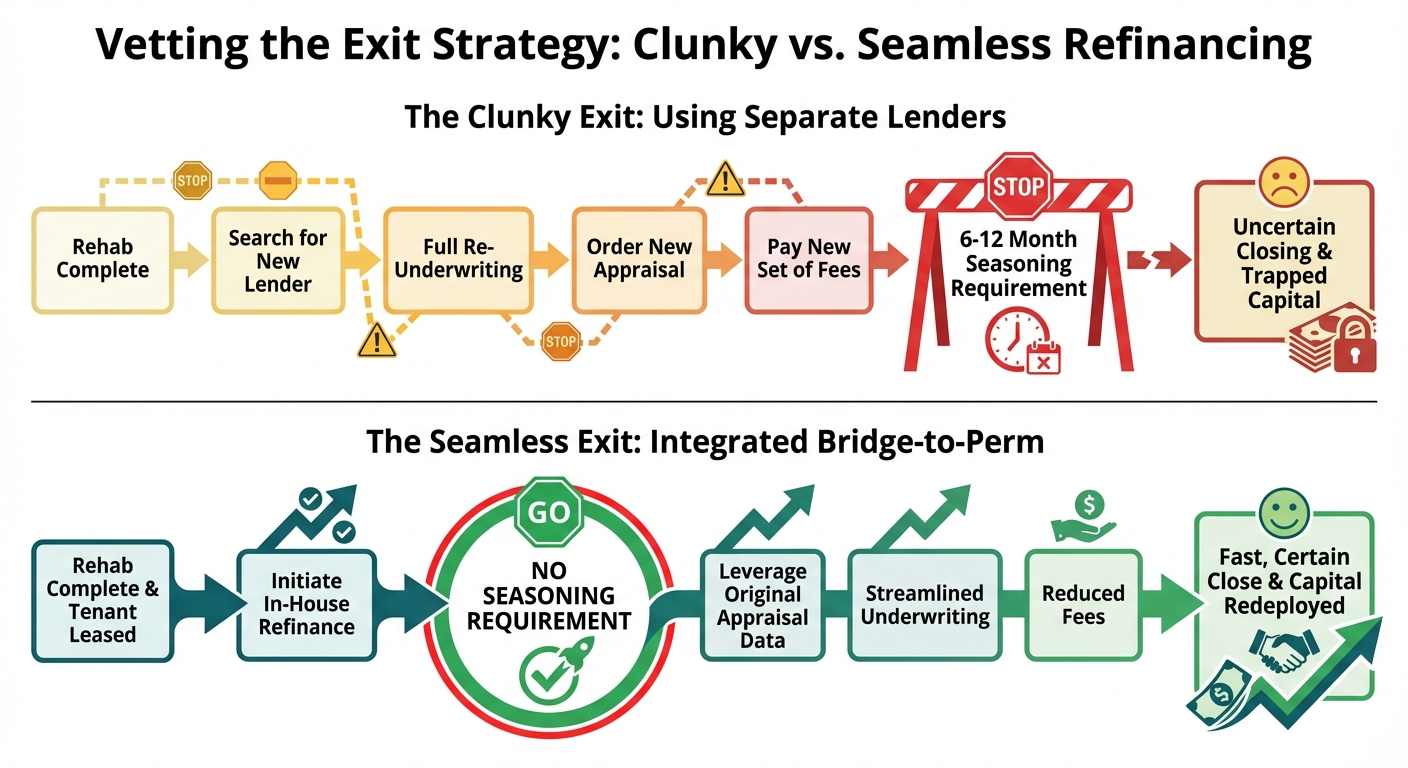

Confirm Exit Optionality & Credit Shielding

The fix and flip loan is just the first step. What happens when the renovation is complete? Elite investors think two steps ahead, ensuring their short-term financing has a clear and efficient path to the next phase, whether that's selling the property or converting it into a long-term rental. They also structure their financing to protect their personal credit and borrowing capacity, allowing them to scale without limits. Vetting a lender on their exit strategies is just as important as vetting their origination process.

The Importance of a Seamless Bridge-to-Perm Financing Path

For investors using the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy, the "refinance" step is the most critical. This is where you pay off the short-term, higher-interest fix and flip loan with a long-term, lower-interest permanent loan, typically a DSCR (Debt Service Coverage Ratio) loan.

The problem is that using two different lenders for this process can be slow, expensive, and uncertain.

- New Underwriting: The new lender will re-underwrite the entire file from scratch.

- New Appraisal: They will almost always require a brand new appraisal.

- New Fees: You'll pay a new set of points, processing fees, and closing costs.

- Seasoning Issues: Many permanent lenders have "seasoning" requirements, forcing you to own the property for 6-12 months before they will refinance it.

The ideal solution is to work with a lender who offers both fix and flip and DSCR loans in-house. This creates a "bridge-to-perm" program where the transition is seamless. Lenders like OfferMarket, who control the entire lifecycle, can offer significant advantages.

The "Fast-Track Rehab Exception" for DSCR Refinancing

A key feature of a top-tier bridge-to-perm program is the "Fast-Track Rehab Exception," which is an exception to traditional seasoning requirements. Lenders who offer this recognize that the value of the property was created through the renovation you just completed with their funds.

This exception allows you to refinance into a long-term DSCR loan as soon as two conditions are met:

- The Certificate of Occupancy (or equivalent) is issued, proving the renovation is complete and the property is habitable.

- A lease agreement is signed with a tenant, proving the property is generating income.

Once these are in place, the lender can immediately begin the refinance process, allowing you to pay off the fix and flip loan and lock in a 30-year fixed rate. This can happen in as little as 30-60 days after the rehab is finished, rather than waiting 6-12 months.

Bypassing the 6-Month Seasoning Requirement for Cash-Out

The "seasoning" rule is a policy from traditional mortgage lenders, stemming from guidelines set by entities like Fannie Mae. It's designed to prevent loan fraud by ensuring a property's value is stable before allowing a homeowner to extract equity. However, for a BRRRR investor, this rule is a major roadblock.

Your entire strategy is based on "forcing appreciation" through renovation and then pulling that newly created equity out to use for your next deal. Waiting six months to do a cash-out refinance traps your capital and slows your velocity.

A lender with a true in-house bridge-to-perm program will use the new, post-renovation appraised value for the DSCR loan, allowing you to execute a cash-out refinance based on the ARV.

Example:

- Purchase + Rehab Cost: $250,000

- New Appraised Value (ARV): $350,000

- DSCR Loan LTV: 75% of ARV

- New DSCR Loan Amount: $350,000 * 75% = $262,500

- Payoff Fix & Flip Loan: -$250,000

- Cash Out to You at Closing: $12,500 (less fees)

This process allows you to pull out your initial investment and often some profit, which can then be immediately redeployed into the next project. This is the engine of the BRRRR strategy, and it's only possible with a lender who offers a seasoning exception.

Mandating LLC Closing to Protect Personal Borrowing Capacity

This is a non-negotiable point for any serious investor looking to scale. You must borrow through a business entity, typically a Limited Liability Company (LLC).

There are two primary reasons for this:

- Liability Protection: Closing in an LLC separates your personal assets from your business activities. If something goes wrong on the project and a lawsuit arises, your personal home, savings, and other assets are protected.

- Credit Shielding: Most fix and flip loans from top-tier private lenders are business-purpose loans made to an entity. As such, they do not report to your personal credit bureaus (Experian, TransUnion, Equifax). This is critically important.

If you take out multiple hard money loans in your personal name, your credit report will show a large amount of short-term, high-interest debt. This will drastically lower your credit score and, more importantly, increase your personal Debt-to-Income (DTI) ratio. When you then try to get a conventional mortgage for your own primary residence, you may be denied because your DTI is too high, even though the business loans are backed by income-producing assets.

By borrowing through an LLC, you keep your business and personal finances separate. This preserves your personal credit score and DTI, ensuring you can still access traditional financing for your personal needs. Any "fix and flip lender" who insists on closing the loan in your personal name is not a true business-purpose lender and should be avoided by anyone with plans to scale.

Comparing Fix and Flip Lender Types

The term "fix and flip lender" is a broad category that encompasses several different types of capital providers. Each has its own unique set of pros and cons, and the best choice for you depends on your experience level, project type, and long-term goals. Understanding the landscape of lender types is the first step in narrowing your search.

Hard Money Lenders

Hard money lenders are the most common and well-known source of financing for fix and flip projects. These are private lending companies that provide short-term, asset-based loans. The "hard" in hard money refers to the hard asset—the property itself—which is the primary collateral for the loan.

Pros:

- Speed: Their main advantage. Hard money lenders can often close a loan in 7-15 business days, a fraction of the time it takes a traditional bank.

- Asset-Based Underwriting: They focus more on the viability of the deal (especially the ARV) than on the borrower's personal income or credit score. This allows investors with strong deals but weaker personal financials to get funded.

- Flexibility: They are more willing to fund properties in distress (e.g., those needing heavy renovation) that a conventional lender wouldn't touch. They also finance renovation costs.

Cons:

- Higher Costs: Speed and flexibility come at a price. Interest rates are typically higher (e.g., 9-13%) than conventional loans, and they charge origination points (typically 1-3% of the loan amount).

- Short Terms: Loans are usually for 6-24 months, with penalties for extensions. They are not a long-term financing solution.

- Variable Quality: The hard money space is loosely regulated, and the quality of lenders varies dramatically. It's crucial to vet them thoroughly to avoid predatory lenders.

Private Money Lenders

Private money is similar to hard money, but it typically comes from a single individual or a small, informal group of investors rather than an established lending company. This could be a friend, family member, colleague, or a wealthy individual you meet through a real estate networking group.

Pros:

- Relationship-Based: The entire deal is based on your relationship with the lender. If they trust you, they may offer incredibly flexible and favorable terms.

- Negotiable Terms: Everything is on the table—interest rate, points, term length, draw schedule. You can structure a deal that is highly customized to your specific project.

- Potential for 100% Financing: A private money lender who knows and trusts you may be willing to fund 100% of the entire project, eliminating any need for a down payment.

Cons:

- Difficult to Find and Scale: Finding reliable private money lenders takes significant time and networking. Furthermore, a single individual has limited funds, so you can't scale your business by relying on just one or two private lenders.

- Risk to Relationships: Doing business with friends or family can be risky. A project that goes wrong can permanently damage personal relationships.

- Lack of Infrastructure: A private individual won't have the professional infrastructure for things like processing draws, inspections, or servicing the loan, which can create administrative headaches.

Institutional Lenders (Banks and Credit Unions)

These are the traditional financial institutions that provide conventional mortgages. While they are the go-to for primary home loans, they are generally a poor fit for fast-paced fix and flip projects.

Pros:

- Lowest Costs: If you can qualify, a traditional bank will offer the lowest interest rates and fees.

- Regulated and Reliable: They are heavily regulated, providing a high degree of consumer protection and predictability.

Cons:

- Extremely Slow: Their underwriting process is meticulous and slow, often taking 45-90 days to close. You will lose deals waiting for them to fund.

- Strict Underwriting: They have rigid requirements for borrower credit score, DTI, and income verification. They are not asset-based.

- Won't Fund Distressed Properties: Banks typically will not lend on properties that are uninhabitable or require significant repairs. They also generally do not finance the renovation costs.

- Seasoning Requirements: As discussed, they have strict seasoning rules that make the BRRRR strategy nearly impossible.

Fintech Lending Platforms

This is the modern evolution of the hard money lender. Fintech (Financial Technology) platforms, like OfferMarket and Kiavi, combine the speed and flexibility of traditional hard money with the efficiency, scale, and user experience of a technology company. They are quickly becoming the standard for serious, scaling investors.

Pros:

- Unmatched Speed and Efficiency: By using technology to automate underwriting, document processing, and communications, they can offer the fastest and smoothest borrowing experience, from instant quotes to 2-week closings.

- Transparency and Convenience: Their online platforms allow you to apply, upload documents, request draws, and track your loan status 24/7 from anywhere. Pricing and terms are often displayed upfront.

- Data-Driven Decisions: They leverage vast amounts of data to make smarter, faster underwriting decisions, often resulting in more competitive terms for qualified borrowers.

- Integrated Services: Many offer a full suite of products, including fix and flip, rental (DSCR), and new construction loans, providing a one-stop-shop for investors and seamless exit strategies.

Cons:

- Less Personal Interaction: The process is tech-forward, which may be a negative for investors who prefer face-to-face interaction. However, the best platforms still have dedicated loan officers available.

- Can Be Less Flexible on "Story" Deals: While data-driven, their models can sometimes be less flexible than a traditional relationship-based private lender when it comes to unique or unusual deal structures that don't fit neatly into their algorithm.

For the modern real estate investor looking to scale their business efficiently, a fintech lending platform offers the best combination of speed, leverage, and reliability.

Core Loan Structures and Metrics Explained

To effectively compare loan offers and vet lenders, you need to be fluent in the language of fix and flip financing. Understanding the core metrics and how they interact is essential for accurately calculating your costs, projecting your profits, and choosing the right loan product for your project.

Loan-to-Cost (LTC) vs. Loan-to-Value (LTV)

These are two of the most fundamental but often confused metrics in real estate lending.

Loan-to-Cost (LTC): This ratio compares the loan amount to the total cost of the project.

- Formula:

LTC = Loan Amount / (Purchase Price + Renovation Costs) - Usage: LTC is the primary metric used for fix and flip and construction loans because the future value is not yet realized. Lenders use it to ensure you have "skin in the game." A lender offering 90% LTC is lending you 90% of the total project budget.

- Formula:

Loan-to-Value (LTV): This ratio compares the loan amount to the current appraised value of the property.

- Formula:

LTV = Loan Amount / Appraised Value - Usage: LTV is the primary metric for traditional mortgages and refinances on stable, completed properties. For example, a cash-out refinance on a rental property will be based on a percentage of its current appraised value.

- Formula:

The Role of After Repair Value (ARV) and ARLTV

For fix and flip loans, the most important valuation is the After Repair Value (ARV).

After Repair Value (ARV): This is a professional appraiser's opinion of what the property will be worth after you have completed all the planned renovations. The appraiser determines this by analyzing comparable sales (comps) of similar, recently renovated properties in the same neighborhood. Your entire project's profitability hinges on accurately estimating the ARV. You can get a rough estimate of ARV using tools like OfferMarket's ARV calculator.

After Repair Loan-to-Value (ARLTV) or LTV of ARV: This is the lender's ultimate backstop. It's a ratio that compares the total loan amount to the ARV.

- Formula:

ARLTV = Total Loan Amount / ARV - Usage: As mentioned earlier, most lenders cap the ARLTV at 75%. This ensures that even if they lend you 90% of your cost, the total loan is still a safe percentage of the property's future stabilized value. It protects the lender if the market declines or your costs run over.

- Formula:

Deconstructing Interest Rates, Points, and Lender Fees

The cost of a hard money loan is comprised of more than just the interest rate.

- Interest Rate: This is the annual cost of borrowing the money, expressed as a percentage. For fix and flip loans, this is almost always "interest-only," meaning your monthly payments only cover the interest accrued, not any of the principal balance. Rates can be fixed or variable.

- Origination Points (or "Points"): These are an upfront fee paid to the lender at closing for originating, or creating, the loan. One point is equal to one percent of the total loan amount.

- Example: On a $250,000 loan, 2 points would equal a $5,000 fee due at closing.

- Lender Fees: This is a catch-all category for other charges from the lender, which can include:

- Underwriting Fee: A flat fee for processing and underwriting the loan file.

- Processing Fee: Another administrative charge.

- Document Prep Fee: A fee for drawing up the loan documents.

- Junk Fees: Be wary of a long list of small, vaguely named fees. A transparent lender will consolidate these into one or two clear charges.

When comparing loan offers, you must calculate the Annual Percentage Rate (APR), which is a standardized metric that includes the interest rate plus all points and fees, giving you a truer picture of the all-in cost of the loan.

Evaluating Term Lengths, Extensions, and Prepayment Penalties

- Term Length: This is the duration of the loan. For fix and flip projects, terms are typically short, ranging from 6 to 18 months. You should choose a term that gives you a realistic buffer to complete the renovation and sell the property.

- Extension Options: What happens if your project is delayed? You must ask a lender about their extension policy before you sign.

- Do they offer extensions?

- What is the cost? (Typically 0.5 to 2 points for a 3-6 month extension).

- Is the extension guaranteed, or is it at their discretion?

- Prepayment Penalties: This is a fee a lender may charge if you pay off the loan early. While common in long-term loans like DSCR loans (often called a "prepayment privilege"), they are a major red flag for a short-term fix and flip loan. The entire goal is to get in and out quickly. A lender who penalizes you for doing exactly that is not an investor-friendly partner. You should seek out loans with no prepayment penalty.

The 7 Must-Ask Questions for Every Lender

When you're on the phone with a potential lender, you are interviewing them for a critical role on your team. You need to go beyond the surface-level questions about rates and points. The questions you ask should be designed to reveal their operational efficiency, flexibility, and overall philosophy. Here are seven essential questions to ask every lender you vet, along with what to look for in their answers.

1. How do you structure and fund construction draws?

- Why it's important: As we've covered, the draw process can make or break your project's timeline and cash flow. This question probes the heart of their post-closing operations.

- What a good answer sounds like: "We have an online portal where you submit your draw request and a detailed SOW. We guarantee an inspector will be out within 48 hours. Once the inspection is passed, we release funds via ACH within 24 hours. The total turnaround time is typically 3-5 business days. We can also customize the draw schedule to match the cash flow needs of your specific project, front-loading it if necessary for deposits and materials."

- What a bad answer sounds like: "You just email us when you need money. We'll get an inspector out there when one is available, usually in a week or two. After we get the report, our accounting department will cut a check." This indicates a slow, manual, and unpredictable process.

2. What are your exact seasoning requirements for a cash-out refinance into a DSCR loan?

- Why it's important: This question directly tests their exit strategy capabilities for BRRRR investors. It separates the true integrated lenders from those who are just a source of short-term debt.

- What a good answer sounds like: "We have no seasoning requirement. As soon as your renovation is complete, you have a signed lease, and the property is generating income, we can begin the refinance into our in-house DSCR loan. We will use the new 'as-rehabbed' appraisal value to calculate your cash-out, allowing you to pull your capital out and move to the next deal."

- What a bad answer sounds like: "We don't do DSCR loans, you'll have to find another lender for that." or "You'll have to wait at least six months after you finish the project to meet standard seasoning guidelines." This signals a dead-end for your capital.

3. Does your platform allow me to order the appraisal upon application?

- Why it's important: This is the key to unlocking a fast closing. It's a direct question about their operational efficiency and whether they run processes in parallel or sequentially.

- What a good answer sounds like: "Absolutely. We encourage it. The same day you submit your application and pay the fee, we will get the appraisal ordered with our Appraisal Management Company. This allows us to run the underwriting and appraisal processes simultaneously, which is how we are able to close loans in as little as 10-15 business days."

- What a bad answer sounds like: "No, our policy is to wait until the loan has been fully underwritten and conditionally approved. We need to make sure the deal is solid before we spend money on an appraisal." This is the hallmark of a slow, traditional lender.

4. Will this loan be reported to my personal credit profile?

- Why it's important: This question is about protecting your personal borrowing capacity and DTI ratio. For any investor looking to scale, the answer must be no.

- What a good answer sounds like: "No. As long as you close in a valid business entity like an LLC or corporation, this is a business-purpose loan. We do not report these loans to the personal credit bureaus—Experian, TransUnion, or Equifax."

- What a bad answer sounds like: "Yes, we require all loans to be made to an individual and they will appear on your credit report." or "We might report it if the loan goes into default." The first is unacceptable, and the second is vague and risky.

5. What are your specific interest reserve requirements based on FICO tiers?

- Why it's important: This uncovers a major component of your required cash-to-close and reveals how they price risk. It forces transparency beyond the headline rate.

- What a good answer sounds like: "We have a clear matrix. For borrowers with a 740+ FICO, we only require one month of interest reserves. From 700-739, it's three months, and from 680-699, it's six months. We're happy to share the exact numbers with you." This is transparent and predictable.

- What a bad answer sounds like: "It depends. The underwriter will decide once they review the file." This lack of transparency means you can't accurately forecast your costs and may be hit with a surprise requirement just before closing.

6. What are all-in closing costs beyond points and interest?

- Why it's important: This question is designed to uncover hidden "junk fees." Origination points are just one piece of the puzzle. You need to know the full cost of getting the loan.

- What a good answer sounds like: "Beyond the origination points, we charge a single, flat underwriting and processing fee of $1,295. That's it from our side. The other costs will be standard third-party fees like the appraisal, title insurance, and attorney fees, which we will detail on your loan estimate." This is simple and transparent.

- What a bad answer sounds like: "Well, there's a processing fee, a doc prep fee, a wire fee, an admin fee, a funding fee..." A long list of small fees is a red flag that they are trying to obscure the true cost of the loan.

7. Can you provide an exception to your standard renovation budget limits?

- Why it's important: This tests their flexibility. Real estate deals don't always fit in a neat box. You need a partner who can underwrite the deal on its merits, not just on a rigid set of rules.

- What a good answer sounds like: "Our standard guidelines have limits, but we absolutely make exceptions for strong projects. If you have a heavy rehab deal but your SOW is detailed, your contractor is credible, and the ARV strongly supports the budget while staying under 75% ARLTV, our underwriters can approve it. We look at it on a case-by-case basis."

- What a bad answer sounds like: "No, our system automatically caps renovation budgets at 50% of the purchase price, no exceptions." This indicates a rigid lender who will not be able to accommodate the unique opportunities you find in the market.

Red Flags: Identifying Inefficient Lenders

Just as important as knowing what to look for is knowing what to avoid. Partnering with the wrong lender can be a costly mistake that ties up your capital and puts your projects at risk. As you vet potential lenders, be on high alert for these red flags that signal an inefficient, outdated, or potentially predatory operator.

Vague Fee Structures and Hidden "Junk Fees"

Transparency is a hallmark of a reputable lender. If you can't get a straight answer on costs, run the other way.

- The Red Flag: A loan estimate or term sheet with a long list of small, vaguely named fees like "admin fee," "funding fee," "wire fee," "processing fee," and "document storage fee." This practice, known as "fee stacking," is designed to obscure the total cost and make it difficult to compare offers.

- What to Look For Instead: A clean, simple fee structure. A top-tier lender will typically charge origination points and a single, clearly defined underwriting or processing fee. All other costs should be standard, third-party charges (e.g., appraisal, title, attorney) that are passed through without markup.

Manual, Paper-Based Underwriting Processes

In 2026, a lender's reliance on technology is a direct indicator of their efficiency.

- The Red Flag: A lender who asks you to fax documents, requires "wet signatures" on everything, or has no online portal for you to upload documents and track your loan's progress. If their application process feels like it's from 1998, their draw and closing processes will be just as slow.

- What to Look For Instead: A sleek, intuitive online platform. You should be able to get an instant quote, complete the entire application online, securely upload all necessary documents, and see the real-time status of your loan from application to funding.

Inflexible Draw Schedules That Don't Match Construction Reality

A lender who doesn't understand construction will impose a draw process that hinders it.

- The Red Flag: A lender who insists on a rigid, pre-set draw schedule (e.g., exactly five draws of 20% each) regardless of your project's specific needs. Or a lender who refuses to fund a draw for materials stored on-site, only reimbursing for work that is 100% complete and installed.

- What to Look For Instead: A partner who will work with you to customize the draw schedule based on your contractor's SOW. They should understand that a large initial draw is often needed for deposits and materials, and they should have a clear process for funding draws that aligns with the realities of a construction project.

No Integrated Exit Strategy or DSCR Loan Product

A lender who only offers short-term fix and flip loans is providing a product, not a solution.

- The Red Flag: When you ask about refinancing into a long-term rental loan, they say, "We don't handle that, you'll have to find another lender when you're done." This leaves you stranded at the most critical point of the BRRRR strategy and exposes you to seasoning requirements and the hassle of starting the entire loan process over from scratch.

- What to Look For Instead: A lender who enthusiastically explains their in-house DSCR loan program. They should be able to clearly articulate the streamlined process, the benefits of using the original appraisal data, and their policy of waiving seasoning requirements for their rehab borrowers. This shows they are invested in your long-term success.

Why OfferMarket is the Lender for Elite Investors

After thoroughly analyzing the metrics that matter—leverage, speed, flexibility, and exit strategy—OfferMarket consistently emerges as the preferred lending partner for sophisticated, scaling real estate investors. Our platform and loan products were not designed by bankers, but by active real estate investors who understand the friction points and bottlenecks that can hinder growth. We built the solution we always wanted for ourselves.

Unlocking Tier 5 Leverage and 100% Renovation Financing

We recognize and reward experience. For qualified investors with a proven track record, we provide access to our top-tier loan programs, offering up to 90% of the purchase price and 100% of the renovation costs, capped at 75% of the ARV. This aggressive leverage structure is designed to minimize your cash-to-close, freeing up your capital to pursue more opportunities and scale your portfolio faster.

Tech-Forward Platform for Rapid Underwriting and Closing

Our proprietary technology platform is the engine of our speed. From our instant fix and flip loan quote that provides transparent terms in minutes, to our streamlined online application and automated underwriting, every step is optimized for efficiency. We empower you to order the appraisal on day one, running it in parallel with underwriting to achieve closing timelines of as little as two weeks. Our online portal makes managing your loan and requesting draws simple and fast, ensuring your projects stay on track and on budget.

Seamless In-House Bridge to DSCR Exit Financing

We are a complete capital partner for your investment lifecycle. We don't just get you into a deal; we provide a clear and seamless exit. Our in-house DSCR loan program is fully integrated with our fix and flip financing. For our BRRRR investors, this means no seasoning requirements. As soon as your rehab is complete and you have a tenant, we can begin the cash-out refinance process, allowing you to pull out your equity and redeploy it into your next project without delay.

Get an Instant, Transparent Quote for Your Next Project

Stop wasting time with slow, inefficient lenders. Experience the difference of a platform built for modern real estate investors. Get a transparent, no-obligation quote for your next fix and flip project in under two minutes and see the terms you qualify for instantly.

Take Action: Analyze Your Next Flip

Knowledge is only powerful when applied. Now that you have the elite framework for vetting fix and flip lenders, it's time to put it into practice on your next deal. The right tools can make all the difference in analyzing profitability and securing the best financing.

Use the OfferMarket Fix and Flip Calculator for Profitability Analysis

Before you even make an offer, run the numbers through our comprehensive Fix and Flip Calculator. This powerful tool goes beyond simple ARV estimates. It allows you to input your purchase price, detailed renovation budget, and financing terms to accurately project your potential ROI, net profit, and required cash-to-close. Analyze different scenarios to ensure your deal is profitable before you commit.

Secure Your Instant Preliminary Loan Terms

Once you've confirmed the deal's potential, take the next step. In just a few minutes, you can get an instant preliminary quote from OfferMarket. See the interest rate, points, and leverage you can expect based on your experience and the property details. This is real, actionable data you can use to finalize your offer and move forward with confidence.

Connect with a Dedicated Lending Advisor

Have questions about your specific project? Our team of experienced lending advisors is ready to help. They are not just salespeople; they are seasoned professionals who can help you structure your loan, navigate complex scenarios, and ensure you are positioned for success.

Fund Your Next Project in as Little as Two Weeks

Don't let financing be the bottleneck that costs you your next profitable deal. With OfferMarket, you have a strategic partner dedicated to providing the speed, leverage, and flexibility you need to thrive in today's market. Get started today and experience a lending process designed for elite investors.

OfferMarket Loans

Check your rate

60 seconds · no credit pull