*Quote takes 1 minute, no credit pull

Insurance*1 quote from 40+ carriers

Listings*New listings daily

21st Century ROAD to Housing Act: What It Means for Small Landlords

Last updated: June 24, 2026

In a week that delivered a rare bipartisan victory followed by an equally rare twist, Congress passed the most comprehensive housing package in decades, and then watched the President abruptly cancel the signing ceremony. For real estate investors, and especially for small landlords, the substance of the legislation matters more than the political theater surrounding it. The bill is poised to become law regardless of the signing drama, and it reshapes the competitive landscape in ways that favor independent investors. Here is what passed, where it stands, and what it means for your strategy.

What Happened This Week

The 21st Century ROAD to Housing Act cleared both chambers of Congress with overwhelming bipartisan support. The Senate passed it 85 to 5 on Monday, June 22, 2026, and the House followed the next day, Tuesday, June 23, with a 358 to 32 vote. By any measure, that is a decisive, cross-party mandate in an otherwise divided Congress.

President Trump was scheduled to sign the bill into law on Wednesday, but abruptly canceled the ceremony, stating that he would withhold his signature until Congress passes the SAVE America Act, an elections-related bill he has characterized as a national emergency. In his words, the housing signing was "cancelled until such time as we pass the desperately needed SAVE AMERICA ACT," which he called a National Emergency.

Why the Bill Is Likely to Become Law Anyway

Here is the part investors should focus on. The cancellation of a signing ceremony is not the same as a veto. Under the Constitution, once a bill has passed both chambers and been presented to the President, he has a 10-day window, excluding Sundays, to sign or veto it. If he does neither while Congress remains in session, the bill automatically becomes law without his signature.

House Speaker Mike Johnson reiterated that the bill will become law within 10 days. The President has not indicated any intent to veto it, only to delay his signature as leverage on a separate issue. So while the politics are dramatic, the practical expectation is that this becomes law. Investors should plan around the substance, not the signing-day headlines.

What Is Actually in the Bill

Considered the most comprehensive housing package in decades, the legislation focuses on expanding housing supply and lowering costs without authorizing new federal spending. The key provisions are summarized below.

| Provision | What It Does |

|---|---|

| Restricting institutional investors | Limits large corporate investors (those owning 350 or more properties) from purchasing certain single-family homes, with a grandfather clause protecting properties acquired before enactment. No forced sell-off of existing inventory. |

| Cutting red tape | Modernizes and streamlines federal environmental review for housing projects to reduce construction delays and costs. |

| Unlocking housing supply | Creates an annual competitive grant program for local governments and tribes that demonstrably increase housing supply through zoning changes, streamlined permitting, and density bonuses. |

| Supporting manufactured housing | Reforms standards to reduce the cost of mobile and manufactured homes, and modernizes FHA loan limits to expand financing options for accessory dwelling units (ADUs). |

| Converting vacant buildings | Establishes a pilot program to help communities convert vacant commercial and industrial properties into affordable housing. |

What It Means for Small Landlords

For small, independent landlords, the bill offers a mix of financial support, reduced red tape, and a more favorable competitive environment. Because it specifically targets large corporate investors, the mom-and-pop operator stands to benefit from several provisions in particular.

Less competition from institutional investors. The bill prohibits institutional investors who already own 350 or more properties from purchasing additional single-family homes. For a small landlord looking to acquire, this levels the playing field by removing the deep-pocketed Wall Street firms and private equity groups that have driven up prices and won bidding wars in recent years.

Funding for property repairs. The legislation incorporates the Whole-Home Repairs Act, creating a HUD pilot program that authorizes federal grants and forgivable loans to help low-to-moderate-income homeowners and small landlords fix up aging properties, address health hazards such as lead paint, and complete deferred maintenance.

Easier access to the Section 8 market. The bill streamlines initial inspection requirements for new landlords participating in the Housing Choice Voucher (Section 8) program, reducing delays and making it easier and faster to start collecting guaranteed voucher rental income.

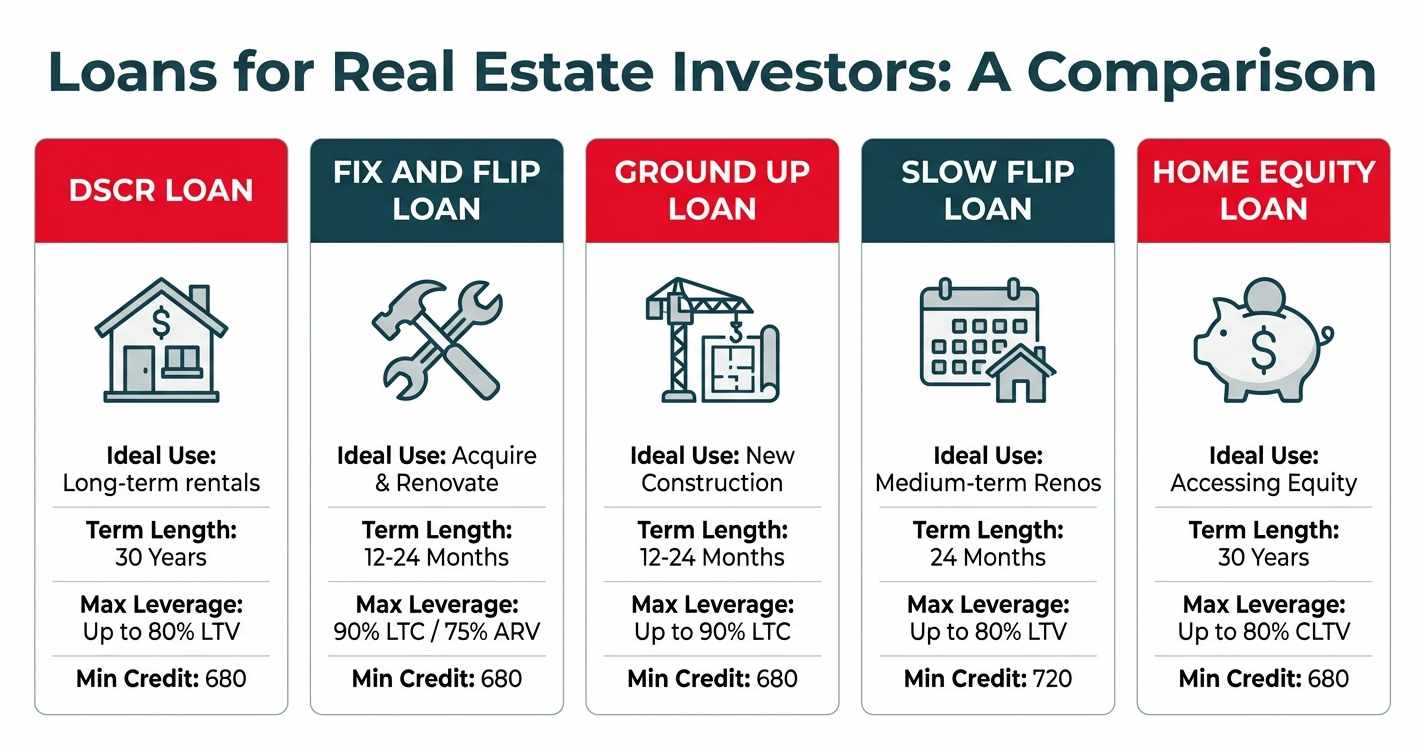

Expanded ADU financing. By modernizing FHA loan limits to expand financing options for accessory dwelling units, the bill reinforces a strategy small investors are already using to add income to a single lot. If you are exploring ADUs, our guide to the DSCR Loan for ADU explains how to finance and qualify ADU rental income, and our ADU glossary entry covers the basics.

A Note on Build-to-Rent

One market signal worth flagging. The stocks of large institutional operators such as AMH and Invitation Homes rebounded after a previously proposed seven-year window to sell new-construction build-to-rent inventory was eliminated from the final bill. With that constraint gone, build-to-rent is expected to grow substantially under this legislation, since new construction is treated differently from buying up existing single-family homes.

The Risks and Unintended Consequences

No bill this sweeping comes without tradeoffs, and several industry experts and economists are bracing for consequences that investors should keep on their radar.

A chilling effect on new construction. By capping institutional investors at 350 properties, the bill aims to stop Wall Street from buying up existing neighborhoods. But institutional capital is the primary driver behind build-to-rent communities, and if mega-investors are spooked or pull funding, the paradoxical result could be less new single-family supply and upward pressure on rents for families who cannot afford to buy.

Slower-than-expected price relief. Building homes takes time. Changes to environmental review and local zoning will take years to translate into actual rooftops, while demand-side measures could pump more buyers into the market before new supply exists, potentially keeping prices stubbornly high for the next year or two.

Disproportionate local funding. The competitive grant program effectively grades municipalities on their zoning reforms. Wealthy, well-resourced cities with large planning departments can readily rewrite codes to win these grants, while smaller, rural, or lower-income municipalities may lack the administrative bandwidth to compete, and could miss out entirely.

A shock to homeowner equity. Years of aggressive corporate purchasing inflated home values through bidding wars. Banning those buyers is a win for prospective purchasers, but for current owners who bought at the top, or retirees relying on inflated equity, the sudden exit of deep-pocketed cash buyers could cause localized dips or stagnation in values.

Greater vulnerability in the rental market. By pushing institutions out, the bill leans heavily on small landlords to fill the gap. That is good for independent investors, but mom-and-pop operators generally lack the cash reserves to weather economic shocks, tax hikes, or non-paying tenants. If small landlords are forced to sell during a downturn, it could create localized instability in rental availability and quality.

Closing Thoughts

Depending on your specific market and strategy, some of these macroeconomic risks may actually present localized acquisition opportunities. The clear throughline of the legislation is that it treats small-scale, mom-and-pop landlords as essential providers of rental housing. It actively shields you from the restrictions placed on massive corporate investors while offering new financial tools, repair funding, and regulatory relief to help you maintain properties and find tenants.

The signing-day drama will dominate the news cycle, but the substance is what shapes your next deal. With the institutional buyer cap, expanded ADU financing, and a friendlier acquisition environment for independent investors, the 21st Century ROAD to Housing Act, once enacted, tilts the playing field toward exactly the kind of investor who reads this newsletter. Plan around the provisions, watch how your local market absorbs them, and position yourself to act where others hesitate.

This article is for informational purposes and reflects a fast-moving legislative situation as of June 24, 2026. Details may change as the bill is enacted and implemented. Consult qualified legal, tax, and financial advisors regarding your specific situation.

Join 25,000+ Real Estate Investors

Sign up for your free OfferMarket account and join 25,000+ residential real estate investors. Membership is free and includes the following benefits:

- Low cost private lending

- Off market deal flow

- Insurance rate shopping

- Weekly market insights

OfferMarket Loans

Check your rate

60 seconds · no credit pull